Adaptimmune stock plunges after announcing Nasdaq delisting plans

Introduction & Market Context

IIFL Finance Ltd (BSE:IIFL) presented its Q1 FY26 performance results on July 30, 2025, revealing a quarter of strategic realignment and selective growth. The non-banking financial company reported a 9% quarter-on-quarter increase in consolidated profit after tax, though year-on-year comparisons showed a 19% decline. Trading at ₹485.25 after a slight dip of 1.22% following the announcement, IIFL Finance continues to navigate a challenging financial landscape while implementing strategic shifts in its loan portfolio.

The company has introduced a new executive leadership team focused on elevating governance and management capabilities, including the appointment of Mr. B.P. Kanungo as Independent Director and several key executives across departments including AI & Innovation, Audit, Legal, and specific business segments.

Quarterly Performance Highlights

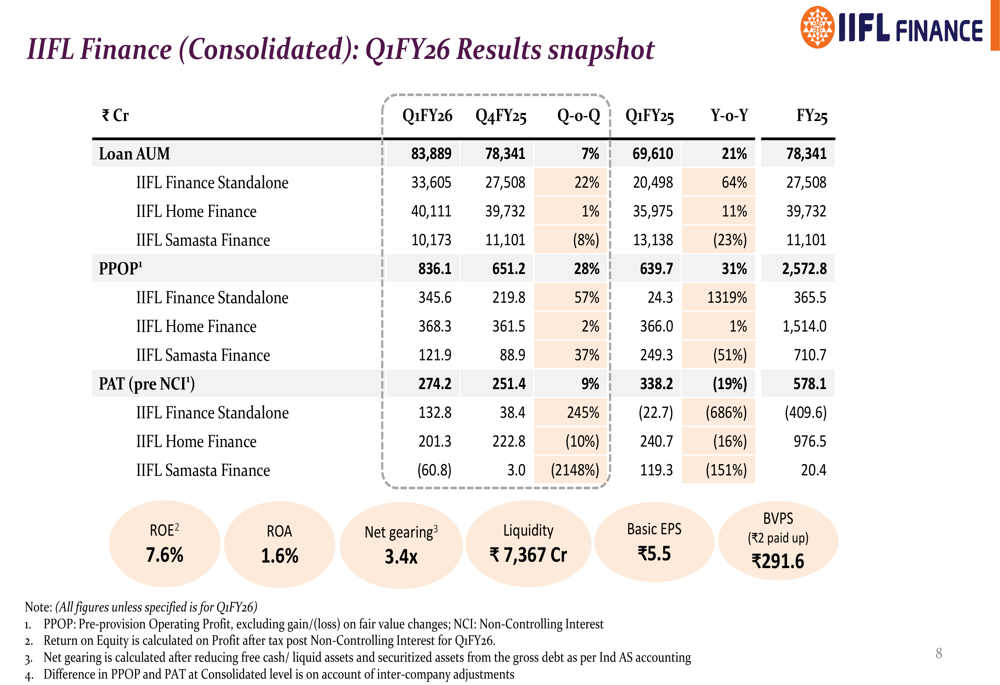

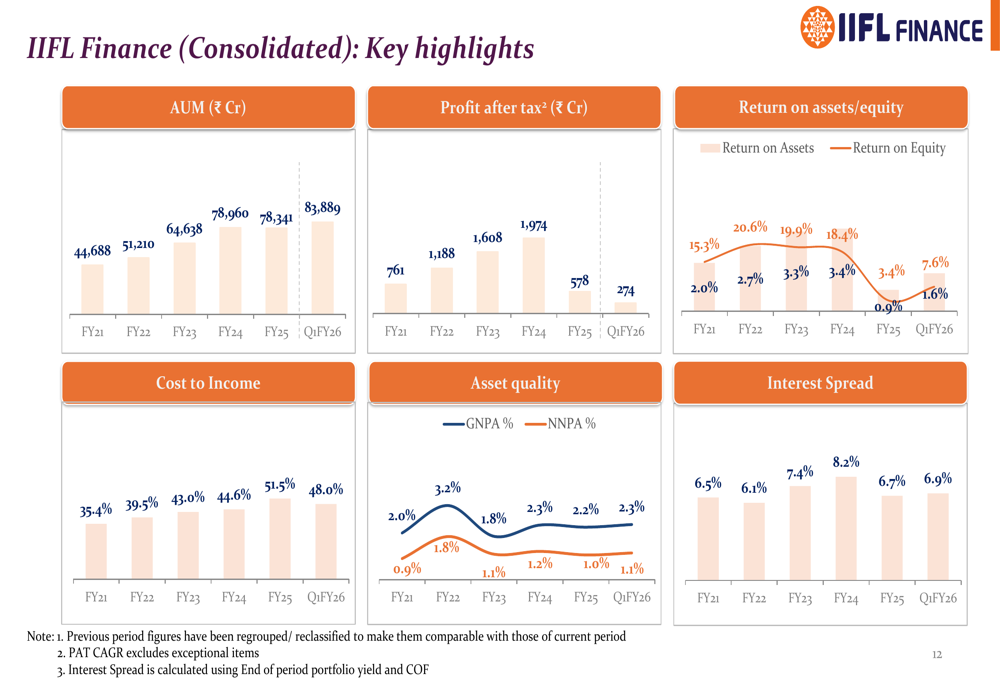

IIFL Finance reported consolidated profit after tax (pre-NCI) of ₹274.2 crore for Q1 FY26, representing a 9% increase quarter-on-quarter but a 19% decline year-on-year. The company’s loan assets under management (AUM) grew to ₹83,889 crore, showing healthy growth of 7% quarter-on-quarter and 21% year-on-year.

As shown in the following snapshot of Q1 FY26 results:

Pre-provision operating profit (PPOP) showed strong growth at ₹836.1 crore, up 28% quarter-on-quarter and 31% year-on-year. However, increased loan losses and provisions, which more than doubled year-on-year to ₹512.5 crore, significantly impacted the bottom line.

The company’s asset quality metrics showed slight deterioration, with gross non-performing assets (GNPA) at 2.3% (up 12 basis points quarter-on-quarter) and net NPAs at 1.1% (up 9 basis points quarter-on-quarter). Return on equity stood at 7.6%, while return on assets was 1.6%.

Detailed Financial Analysis

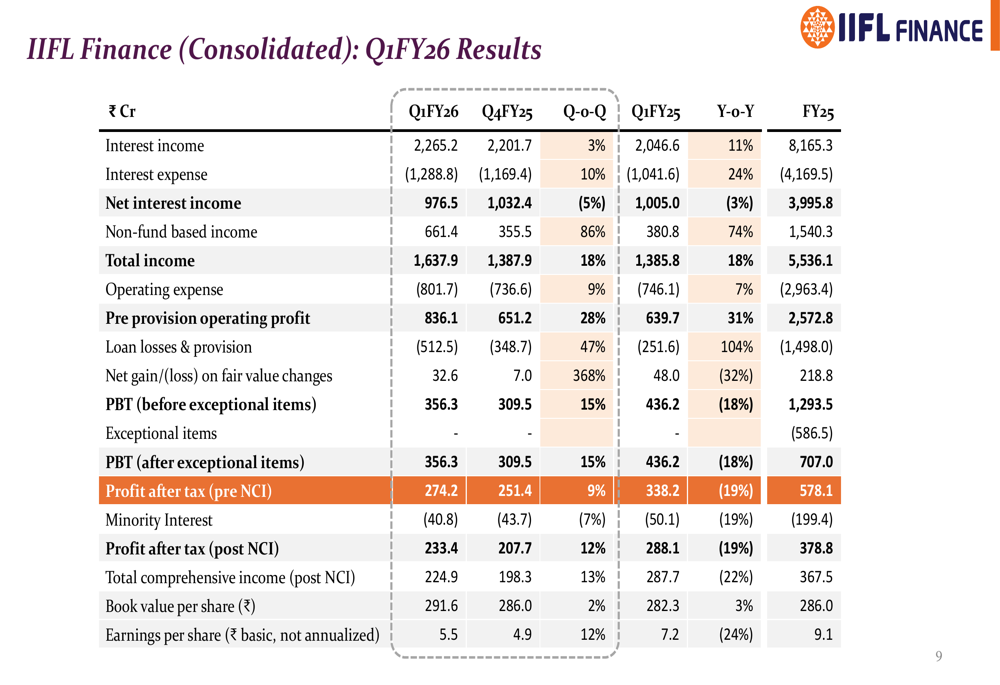

A closer examination of IIFL Finance’s Q1 FY26 financial performance reveals a mixed picture across various income streams and expenses:

Interest income grew by 11% year-on-year to ₹2,265.2 crore, while interest expenses increased by 24% to ₹1,288.8 crore, resulting in a 3% year-on-year decline in net interest income to ₹976.5 crore. However, non-fund based income showed remarkable growth of 74% year-on-year to ₹661.4 crore, helping total income rise by 18% to ₹1,637.9 crore.

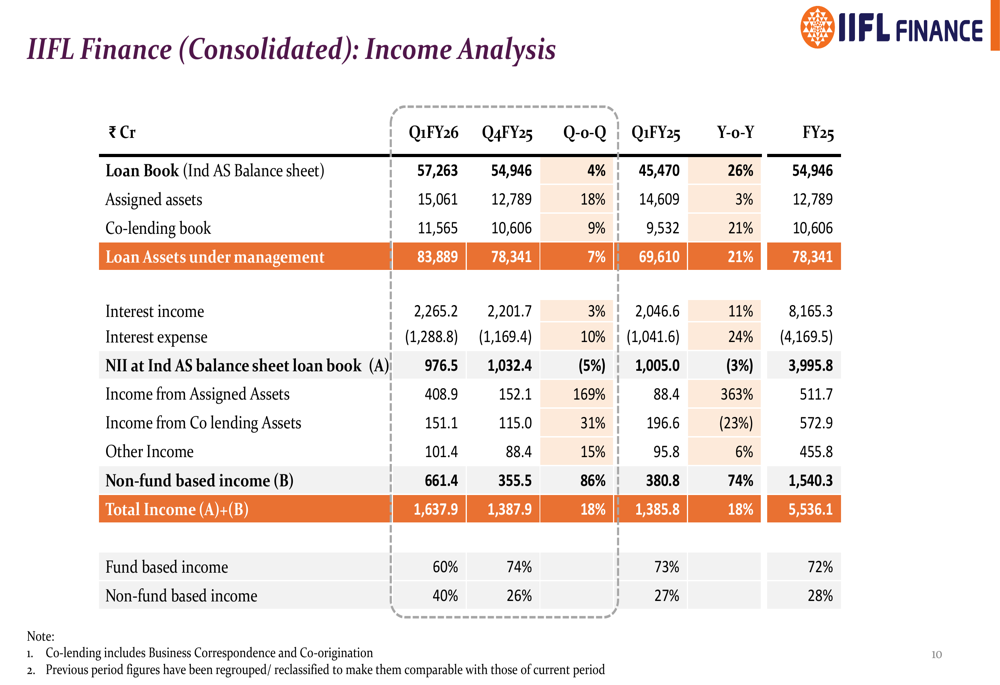

The company’s income analysis shows that while fund-based income constitutes 60% of total income, non-fund based income has grown to represent 40% of the total:

Operating expenses increased by 7% year-on-year to ₹801.7 crore, but the cost-to-income ratio improved to 48.0%, down 9.0 percentage points quarter-on-quarter. This improvement in operational efficiency is a positive sign amid challenging market conditions.

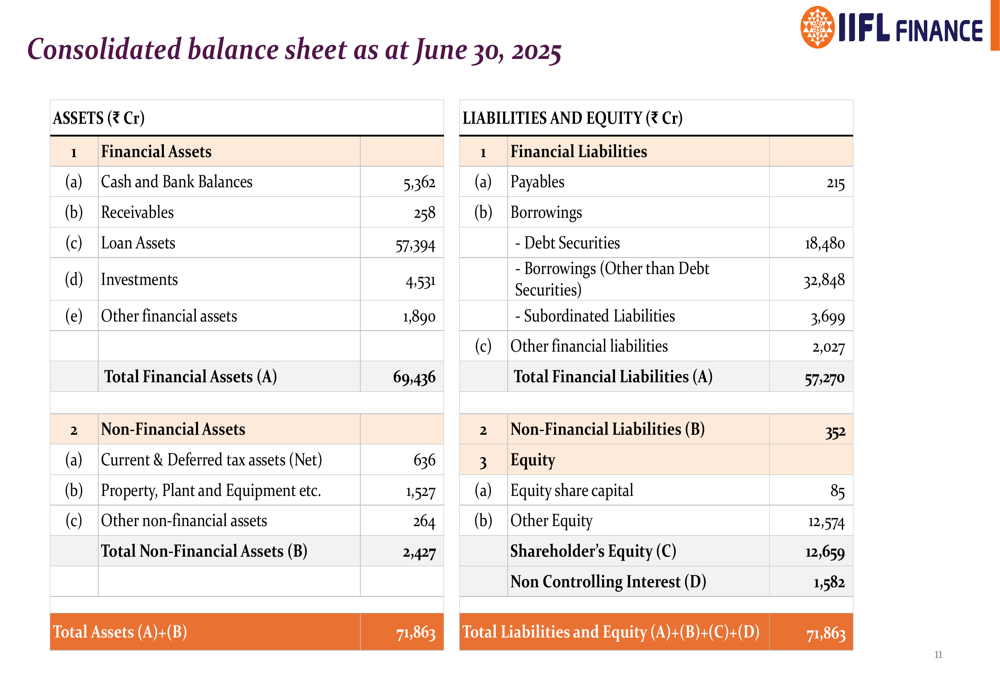

The company’s balance sheet remains robust with total assets of ₹71,863 crore as of June 30, 2025:

Strategic Initiatives & Segment Performance

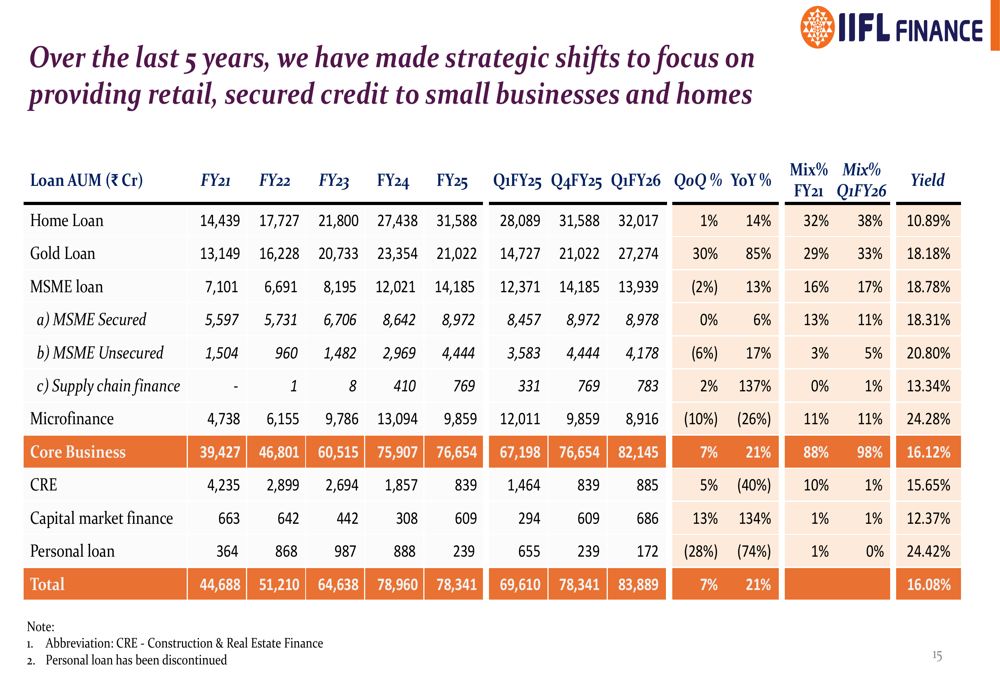

IIFL Finance’s presentation highlighted a significant revival in its gold loan business following the lifting of an RBI embargo. Gold loan AUM reached ₹27,274 crore in Q1 FY26, with GNPA in this segment improving dramatically to 0.18% from 0.54% in the previous quarter. The portfolio yield for gold loans also increased to 18.20%, indicating improved profitability in this segment.

The company’s loan AUM breakdown shows the strategic shift toward more secure lending segments:

Home loans continue to be the largest segment at ₹32,017 crore, while gold loans have seen significant growth to become the second-largest category at ₹27,274 crore. The presentation also mentioned corrective actions for MSME, Housing, and Microfinance loans, including the discontinuation of certain loan types and focused recovery efforts.

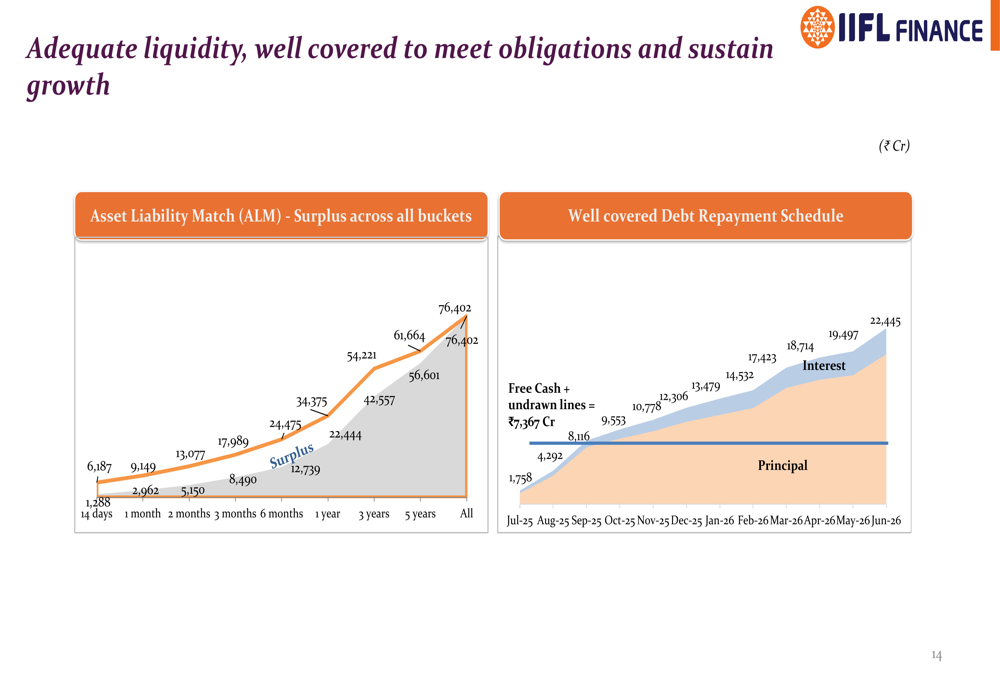

The company’s funding mix and liquidity position remain strong, with well-covered debt repayment schedules and positive asset-liability matching:

Forward-Looking Statements

IIFL Finance appears to be positioning itself for sustainable growth through a strategic realignment of its loan portfolio, with increased focus on secured lending segments like gold loans and home loans. The company’s key performance indicators show a mixed but generally improving trend:

The appointment of new executive leadership suggests a renewed focus on governance and risk management, which may help address the asset quality challenges evident in the slight increase in NPAs.

According to the earnings call information, IIFL Finance has set ambitious targets for AUM growth between 15% and 18%, with potential to reach 20% to 25%. The company expects continued growth in its gold loan segment and plans to maintain a credit cost around 3.5% for FY26, while targeting a reduction in gross NPA to below 2% by year-end.

Despite current challenges, particularly in the MSME and microfinance segments, management remains optimistic about future performance, expecting overall improvements in the second half of the fiscal year. The company’s strategic pivot toward safer, more profitable segments appears to be gaining traction, though execution risks remain as it navigates the current financial landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.