Goldman Sachs chief credit strategist Lotfi Karoui departs after 18 years - Bloomberg

Introduction & Market Context

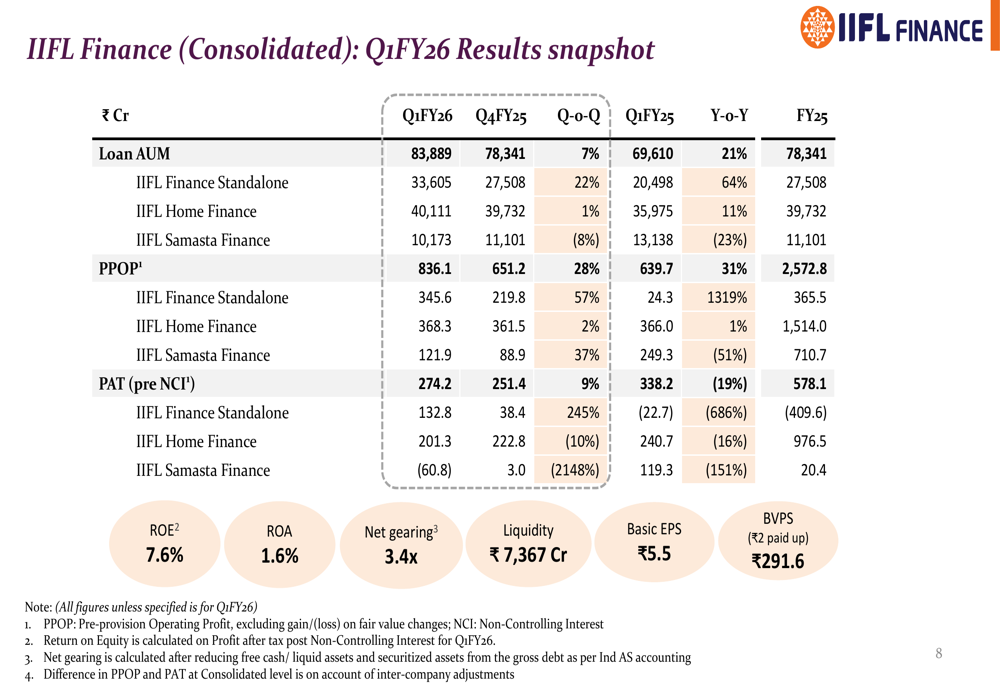

IIFL Finance Ltd (NSE:IIFL) presented its Q1FY26 results on July 30, 2025, showcasing a quarter of modest recovery with consolidated profit after tax (pre-NCI) growing 9% quarter-on-quarter to ₹274 crore. The company’s stock closed at ₹514.90, down 2.15% on the day of the presentation, reflecting investor caution despite the positive growth indicators.

The financial services company has been implementing strategic changes following regulatory challenges, with a notable milestone being the lifting of the RBI embargo on its gold loan business in September 2024, which has contributed to the company’s gradual recovery trajectory.

Quarterly Performance Highlights

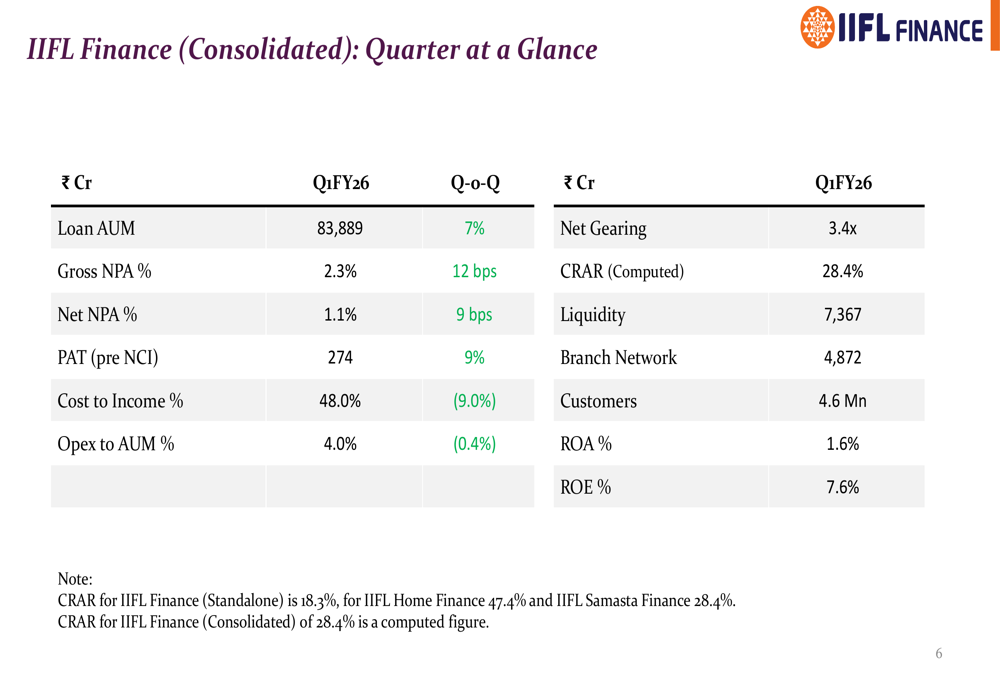

IIFL Finance reported a 7% quarter-on-quarter growth in loan assets under management (AUM), reaching ₹83,889 crore in Q1FY26. The company also demonstrated improved operational efficiency with cost-to-income ratio decreasing by 9% to 48.0% and operating expenses to AUM ratio declining by 0.4% to 4.0%.

As shown in the following consolidated quarterly snapshot, the company maintained healthy capital adequacy with CRAR at 28.4% and liquidity of ₹7,367 crore, while return metrics showed ROA at 1.6% and ROE at 7.6%:

The detailed financial results reveal that while net interest income stood at ₹976.5 crore, the company recorded loan losses and provisions of ₹512.5 crore, reflecting ongoing asset quality challenges:

Asset Quality Challenges and Strategic Response

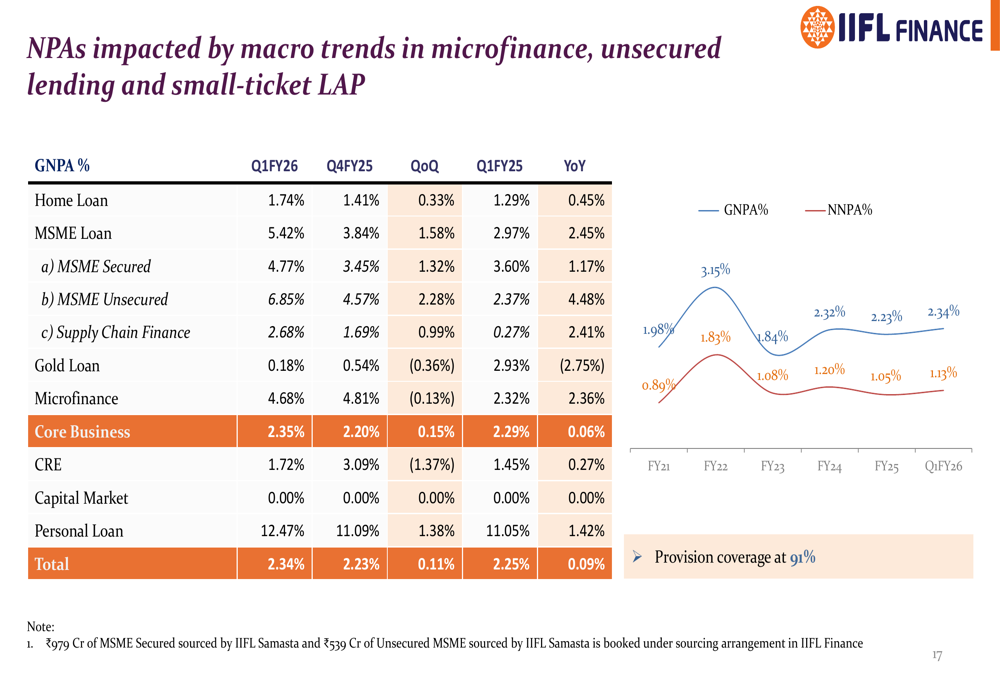

The presentation highlighted increasing non-performing assets across key segments, with consolidated gross NPA rising by 12 basis points to 2.3% and net NPA increasing by 9 basis points to 1.1%. Particularly concerning were the GNPA trends in home loans (1.74% vs 0.45% in Q1FY25) and MSME loans (5.42% vs 2.45% in Q1FY25).

The following chart illustrates these NPA trends across different business segments:

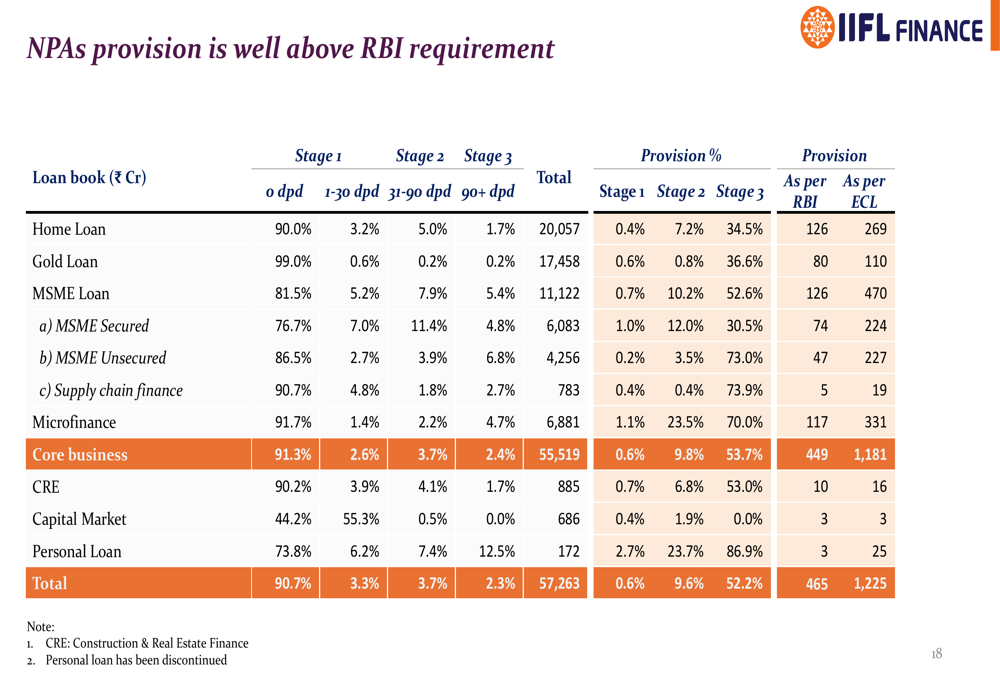

To address these challenges, IIFL Finance has implemented a comprehensive strategic roadmap. The company emphasized that its provision coverage at 91% remains well above RBI requirements, providing a buffer against potential loan losses:

The company has also strengthened its leadership team to enhance governance and management capabilities. As shown in the following slide, several key appointments have been made, including B.P. Kanungo as Independent (LON:IOG) Director and Mayank Sharma as Chief AI & Innovation Officer:

Segment Performance Analysis

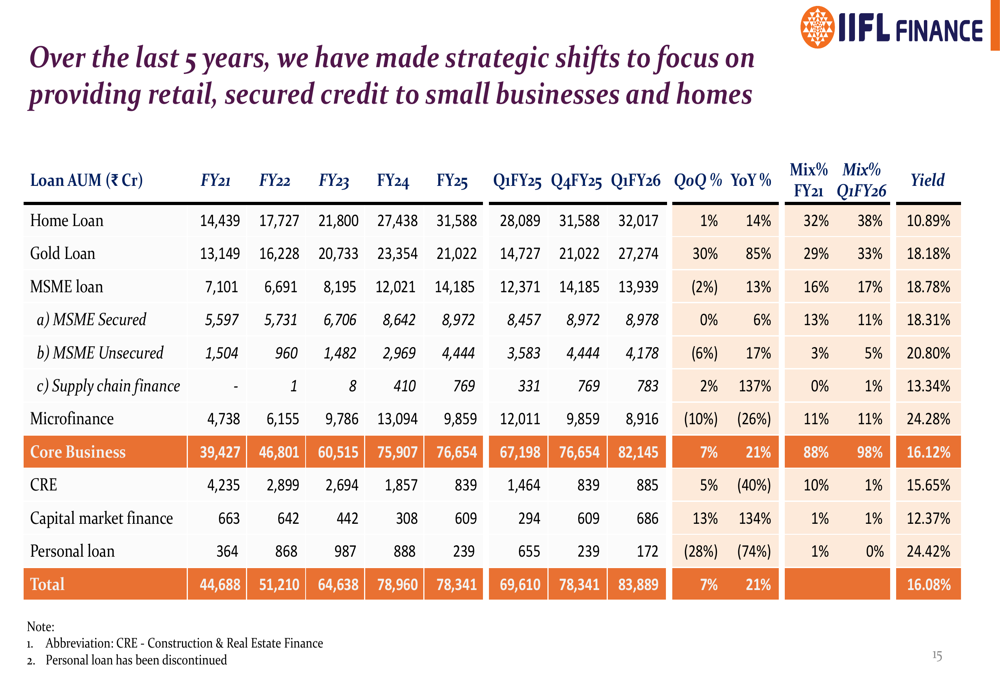

IIFL Finance’s loan portfolio continues to be dominated by home loans and gold loans, which together constitute 71% of the total AUM. Gold loans showed particularly strong performance, growing from ₹23,354 crore in March 2024 to ₹27,274 crore in Q1FY26.

The following breakdown illustrates the company’s loan AUM by product segment and their respective yields:

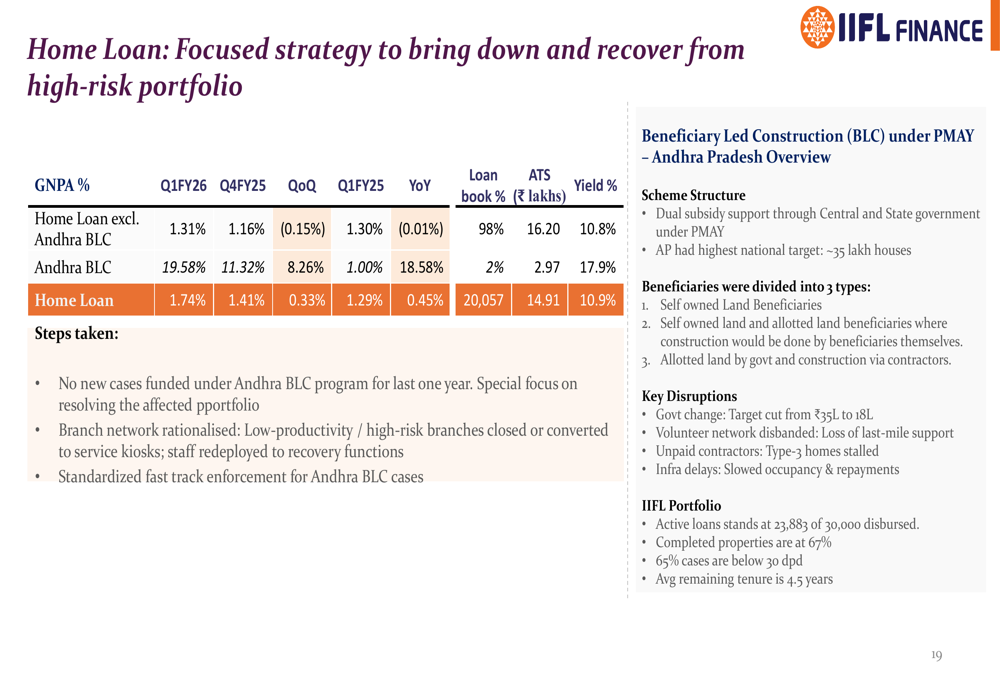

In the home loan segment, the company has identified specific challenges with the Andhra Pradesh Beneficiary Led Construction (BLC) program, which showed a concerning GNPA of 19.58%. In response, IIFL has suspended new funding under this program and implemented standardized fast-track enforcement measures:

Similarly, in the MSME segment, the company has suspended new originations of Micro LAP business sourced through IIFL Home Finance and is revising its product and policy framework to limit risk exposure.

Liquidity and Funding Position

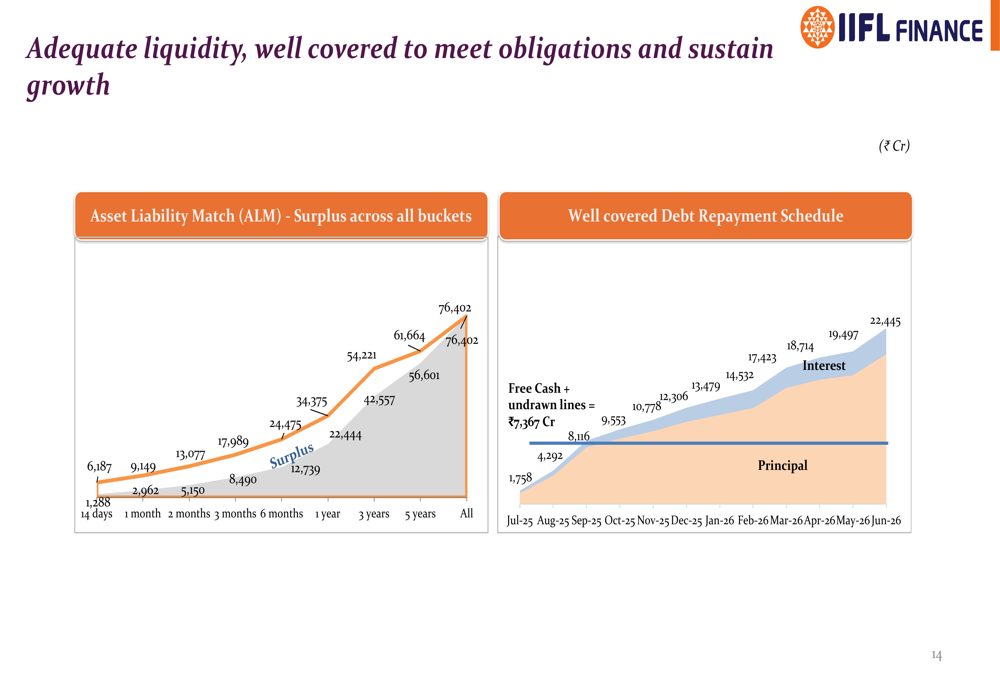

IIFL Finance maintained a strong liquidity position with adequate coverage for upcoming debt repayments. The asset liability match (ALM) shows a surplus across all time buckets, with free cash and undrawn lines totaling ₹7,367 crore:

The company’s funding mix has evolved, with increasing diversification across securitization, debentures, refinance, and term loans. The cost of borrowing has stabilized at 9.4%-9.5% in Q1FY26, while net gearing decreased from 4.8 in FY21 to 3.4 in Q1FY26, indicating a strengthening balance sheet.

Forward-Looking Statements

Looking ahead, IIFL Finance has outlined several strategic initiatives to improve asset quality and drive sustainable growth. These include recalibrating target segments in MSME secured loans, moderating leverage amongst MFI borrowers, and implementing enhanced risk management practices.

The company expressed confidence that these measures, combined with the strengthened leadership team and robust capital position, will support its next phase of growth while maintaining prudent risk management. However, the rising NPAs in key segments suggest that the company will need to navigate significant challenges in the near term to fully restore investor confidence.

As the company continues to implement its recovery strategy, investors will be closely monitoring asset quality trends and the effectiveness of the corrective measures in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.