Street Calls of the Week

Introduction & Market Context

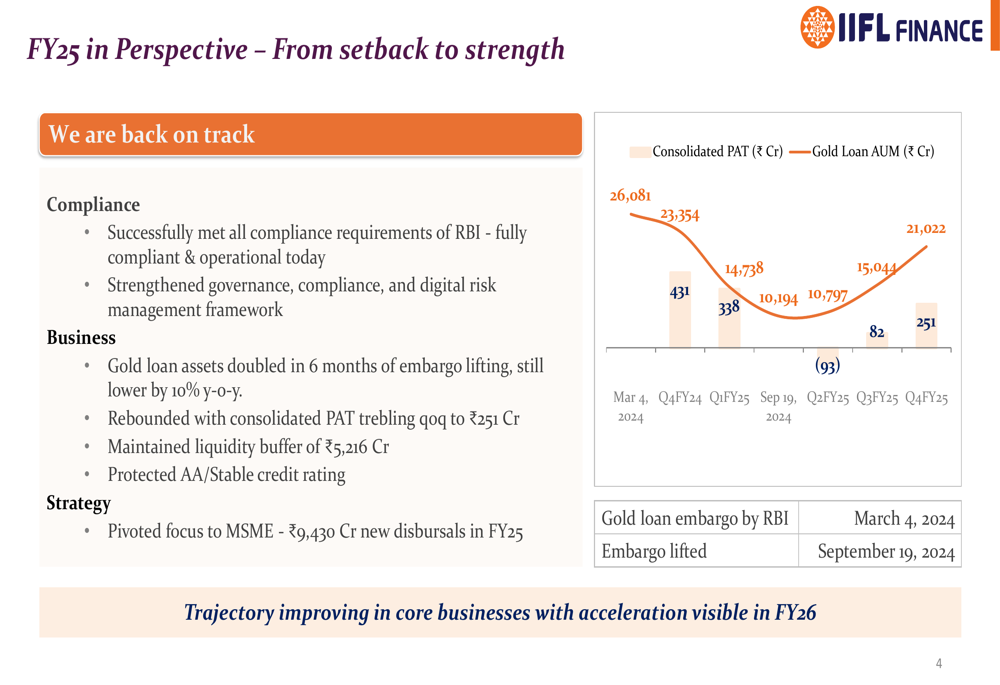

IIFL Finance Ltd (NSE:IIFL) presented its Q4FY25 and FY25 performance review on May 8, 2025, highlighting a significant quarter-on-quarter recovery following regulatory challenges. The company has been rebuilding its business after an RBI-imposed embargo on gold loans that lasted from March 4 to September 19, 2024. Despite the setback, IIFL Finance maintained its credit rating and has strategically pivoted toward MSME lending while working to restore its gold loan portfolio.

Quarterly Performance Highlights

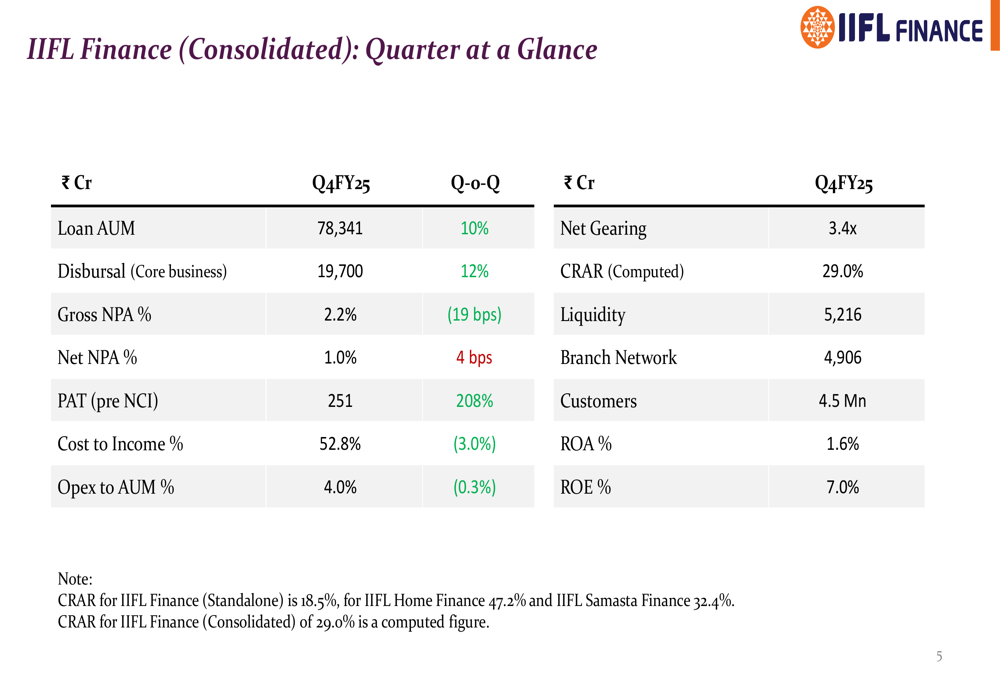

IIFL Finance reported a consolidated profit after tax (pre-NCI) of ₹251 crore for Q4FY25, representing a substantial 208% increase quarter-on-quarter, though still 42% lower than the same quarter last year. The company’s loan assets under management reached ₹78,341 crore, growing 10% from the previous quarter but showing a marginal 1% decline year-on-year.

As shown in the following consolidated financial highlights, the company maintained stable asset quality with gross NPAs at 2.2%, an improvement of 19 basis points quarter-on-quarter:

The company’s gold loan business, which was directly impacted by the regulatory embargo, has shown signs of recovery. As illustrated in the performance overview chart below, gold loan assets doubled in the six months following the lifting of the embargo, though they remain 10% lower year-on-year:

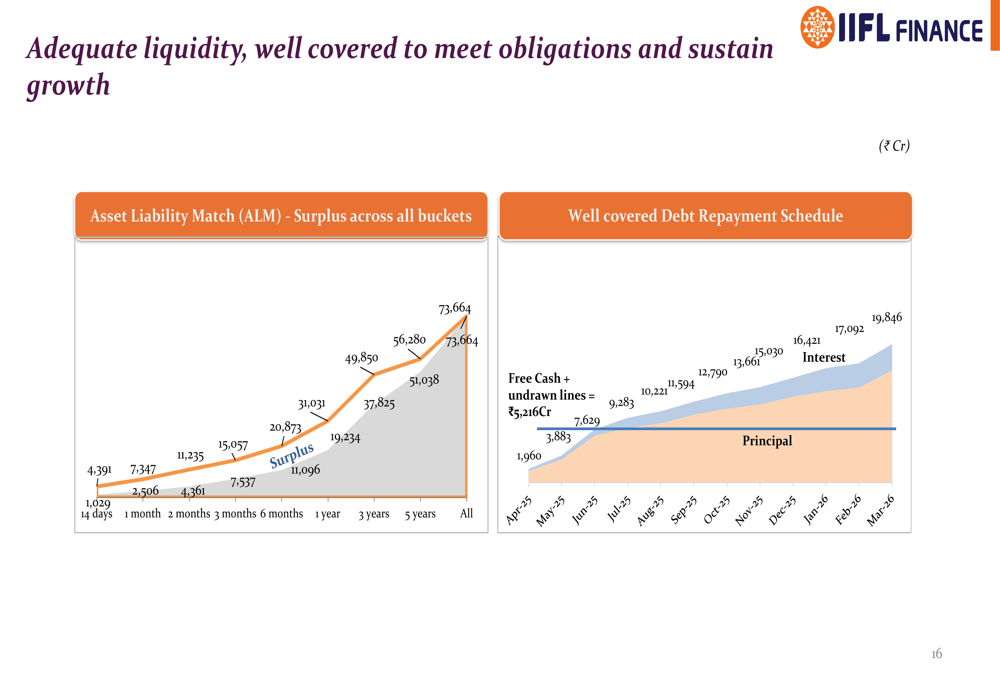

IIFL Finance maintained a strong liquidity buffer of ₹5,216 crore and a computed Capital to Risk-Weighted Assets Ratio (CRAR) of 29.0%. The company’s cost-to-income ratio improved to 52.8%, down 3.0% quarter-on-quarter, while operating expenses as a percentage of average AUM decreased to 4.0%, a reduction of 0.3% from the previous quarter.

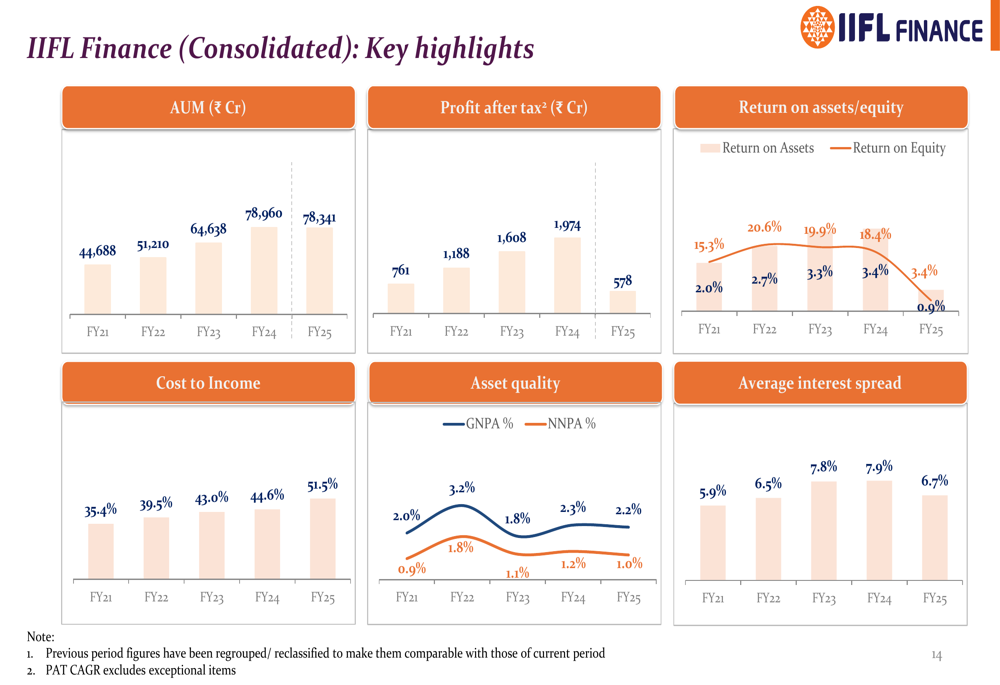

The full-year results for FY25 reflect the impact of regulatory challenges, with consolidated PAT (pre-NCI) at ₹578 crore, down 71% from FY24. Return on Equity (ROE) for FY25 stood at 3.4%, significantly lower than previous years, as shown in the following charts:

Strategic Initiatives

IIFL Finance has strategically pivoted toward MSME lending as its new growth engine, with ₹9,430 crore in new disbursals during FY25. The company is leveraging India’s vast MSME potential, citing an unmet credit demand of ₹20-25 lakh crore in this sector, with over 80% of MSMEs remaining outside formal credit channels.

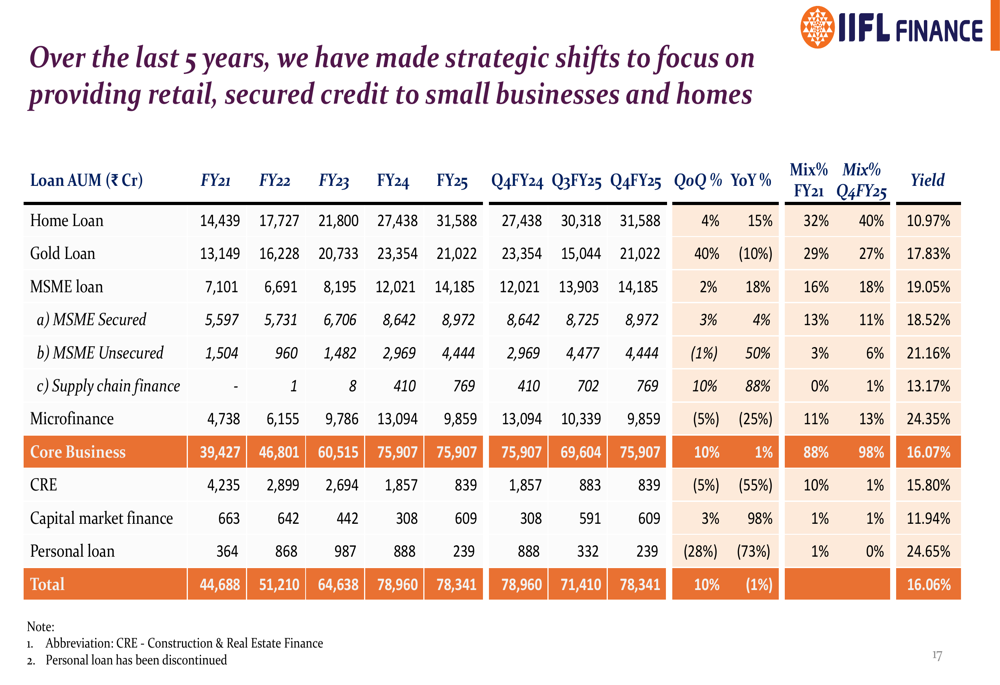

The company’s loan portfolio shows a strategic shift toward secured lending to small businesses and homes, as illustrated in the following breakdown:

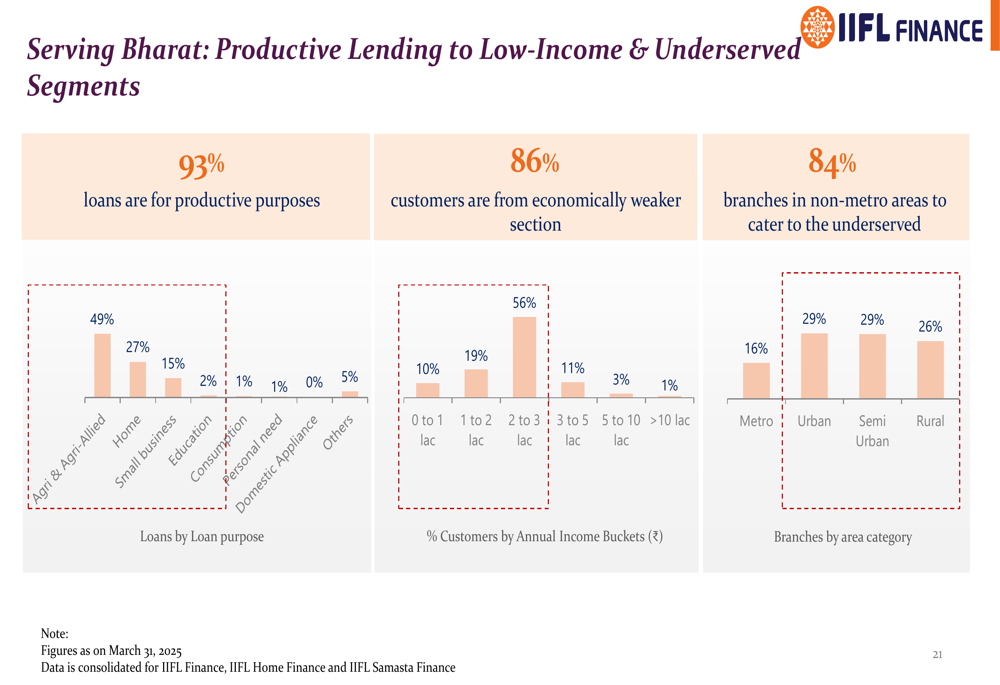

IIFL Finance emphasizes its focus on serving underserved segments of the population, with 93% of loans directed toward productive purposes and 86% of customers coming from economically weaker sections with annual incomes below ₹3 lakh. The company maintains 84% of its branches in non-metro areas to better serve these customer segments:

The company’s business model combines physical presence with digital capabilities, operating through a network of approximately 4,900 branches integrated with advanced digital platforms. This "phygital" approach is complemented by strategic partnerships with banks and fintech companies for customer acquisition and co-lending opportunities.

Forward-Looking Statements

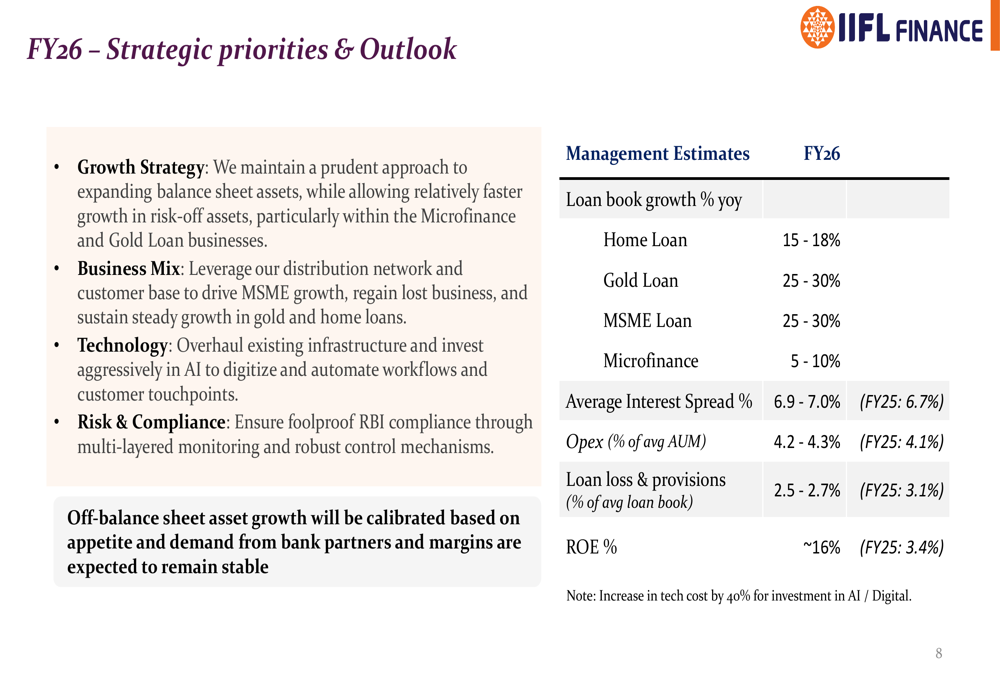

Looking ahead to FY26, IIFL Finance has outlined ambitious growth targets across its business segments. The company expects its home loan portfolio to grow by 15-18%, while gold loans and MSME loans are projected to expand by 25-30% each. The microfinance segment is expected to see more modest growth of 5-10%.

The management has provided the following estimates for FY26, targeting a significant improvement in ROE from 3.4% in FY25 to approximately 16% in FY26:

To support these growth objectives, IIFL Finance plans to increase its technology investments by 40%, focusing on AI and digital capabilities to enhance efficiency and customer experience. The company expects to maintain stable margins while improving its loan loss provisions ratio from 3.1% in FY25 to 2.5-2.7% in FY26.

Detailed Financial Analysis

IIFL Finance’s consolidated balance sheet remains robust with total assets of ₹67,644 crore as of March 31, 2025. The company’s funding mix has evolved over time, with a diversified borrowing profile that helps manage cost of funds and liquidity.

The company has maintained adequate liquidity across all time buckets in its Asset Liability Match (ALM) profile, ensuring coverage of upcoming debt repayment obligations:

Asset quality metrics show varying performance across different loan segments. While the overall gross NPA ratio stands at 2.2%, there are significant variations by product, with microfinance experiencing higher stress levels compared to secured lending products like home loans and gold loans.

IIFL Finance operates through a structure that includes two major subsidiaries: IIFL Home Finance for housing finance and IIFL Samasta Finance for microfinance operations. This structure allows for specialized focus on different customer segments while maintaining consolidated oversight.

In summary, IIFL Finance’s Q4FY25 results demonstrate a company in recovery mode following regulatory challenges, with a clear strategic direction focused on secured lending to underserved segments. While the full-year performance for FY25 shows the impact of these challenges, the quarter-on-quarter improvement and ambitious targets for FY26 suggest a potential return to stronger profitability in the coming year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.