United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Indosat Tbk (IDX:ISAT) presented its second quarter 2025 results on July 30, highlighting a stable performance with marginal revenue decline but improved profitability through cost efficiencies. The company’s stock declined 1.32% following the presentation, trading at IDR 2,240, reflecting cautious investor sentiment despite the company’s strategic investments in artificial intelligence and network expansion.

The Indonesian telecommunications provider is operating in a market that appears to be stabilizing after industry consolidation, with rational competition allowing for SIM card price increases and reduced promotional activity.

Quarterly Performance Highlights

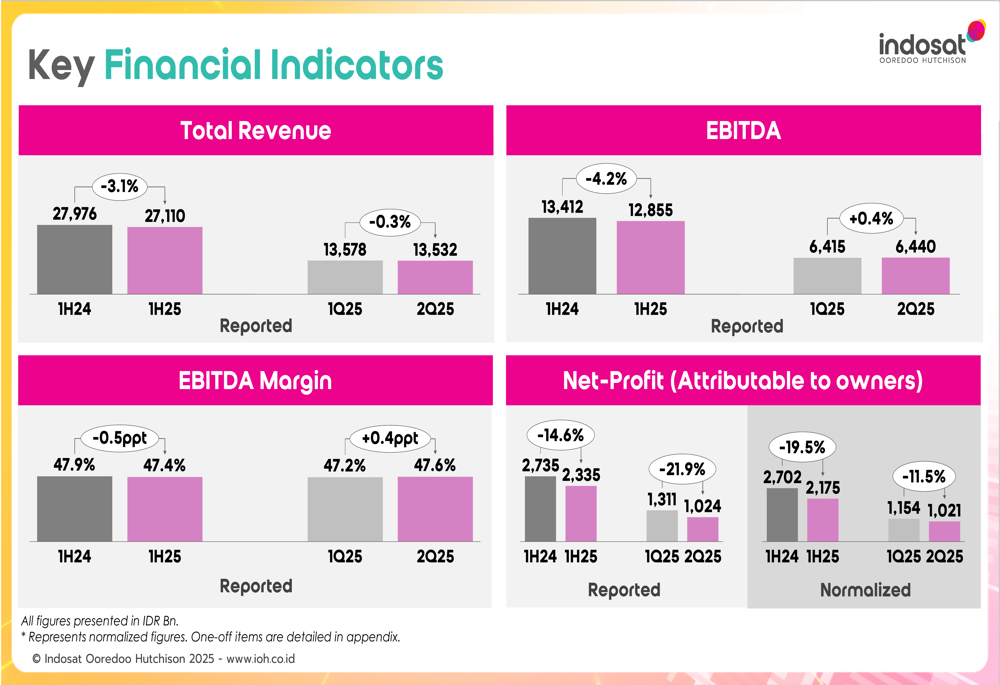

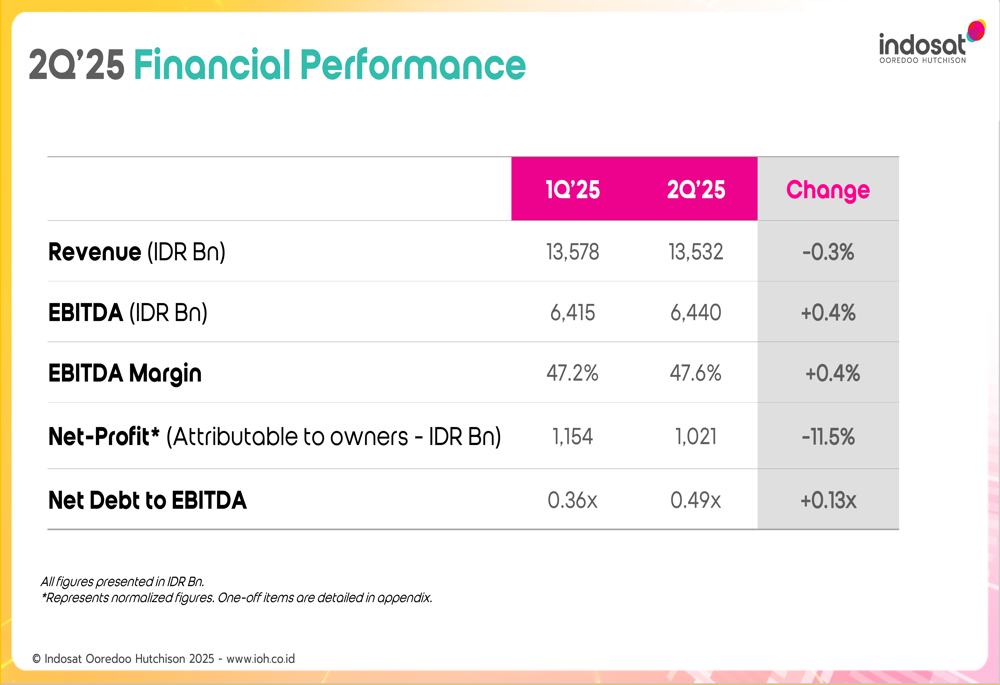

Indosat reported relatively steady financial performance in Q2 2025, with revenue slightly declining by 0.3% quarter-over-quarter to IDR 13,532 billion, which management attributed to post-festive seasonality. Despite this modest revenue dip, the company managed to improve its EBITDA by 0.4% to IDR 6,440 billion, resulting in an EBITDA margin expansion of 0.4 percentage points to 47.6%.

As shown in the following chart of key financial indicators:

Net profit attributable to owners (normalized) decreased by 11.5% quarter-over-quarter to IDR 1,021 billion. This represents a shift from Q1 2025, when the company had reported a 27% quarterly increase in net profit according to previous earnings reports.

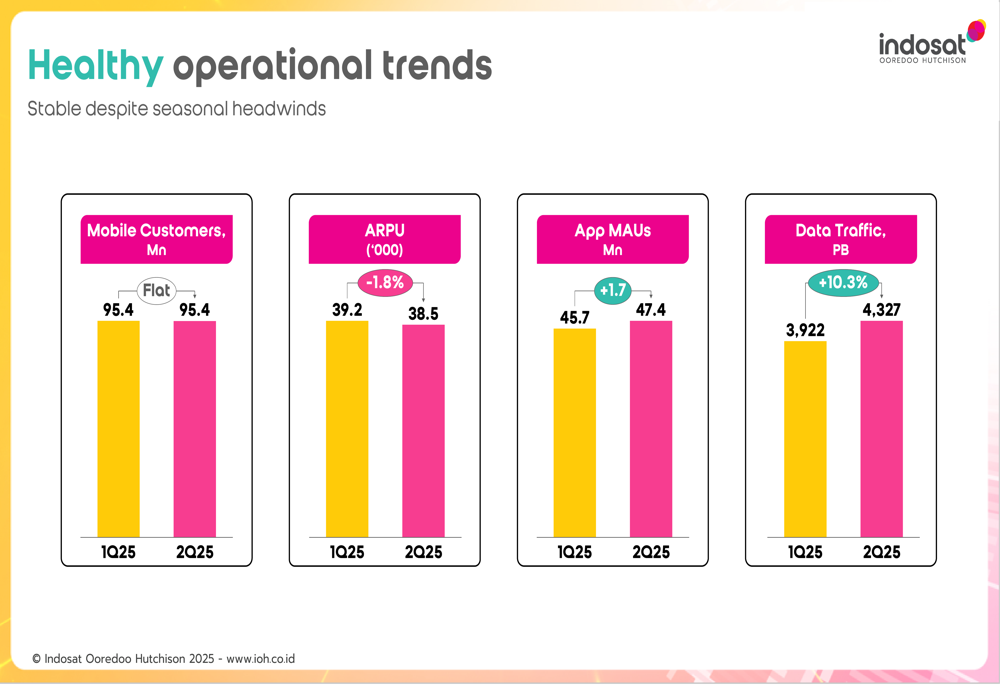

On the operational front, Indosat maintained its customer base at 95.4 million amid SIM price increases, while growing its app user base to 47.4 million from 45.7 million in the previous quarter. ARPU slightly declined by 1.8% to IDR 38,500, but data traffic continued to grow, reaching 4,327 PB from 3,922 PB in Q1.

The following slide illustrates these operational trends:

Strategic Initiatives

Indosat is positioning itself as a technology company ("Techco") rather than just a telecommunications provider, with significant investments in artificial intelligence capabilities. The company has launched an AI Centre of Excellence in partnership with Komdigi, NVIDIA (NASDAQ:NVDA), and Cisco (NASDAQ:CSCO) to develop Indonesia’s AI capabilities.

The company highlighted its strategic investments as shown in the following slide:

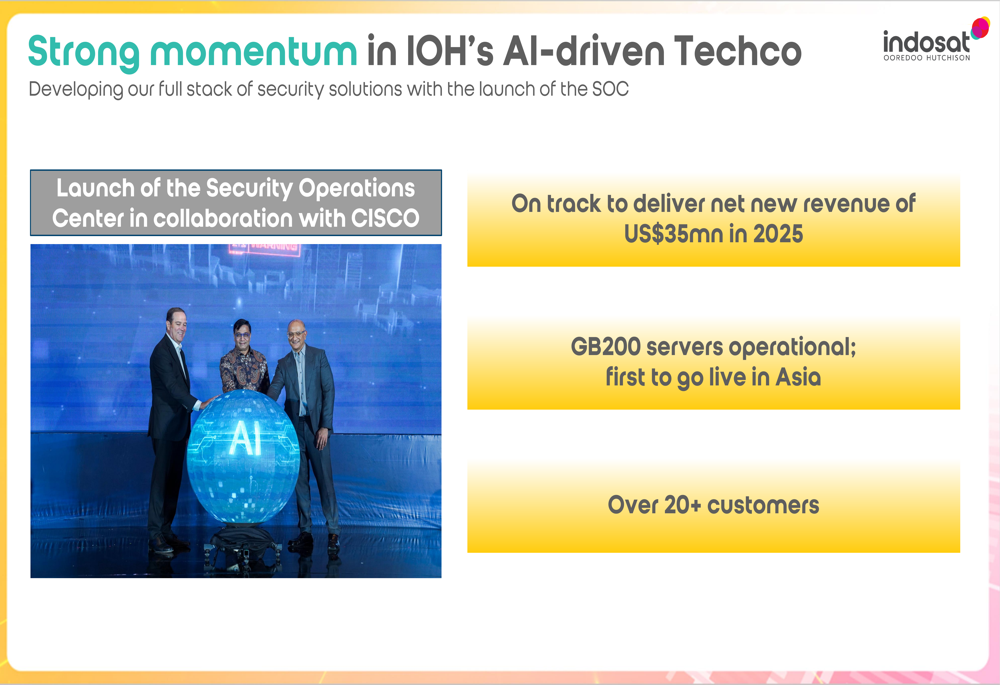

The AI initiatives are expected to generate new revenue streams, with the company on track to deliver net new revenue of US$35 million in 2025. Indosat claims to be the first in Asia to have GB200 servers operational, serving over 20 customers through its AI-driven solutions.

As illustrated in this slide on the company’s AI momentum:

Additionally, Indosat is implementing market stabilization efforts, including increasing SIM card entry prices to IDR 35,000 and leveraging AI for hyper-personalization to improve ARPU and customer engagement.

The company’s market stabilization strategy is outlined here:

Detailed Financial Analysis

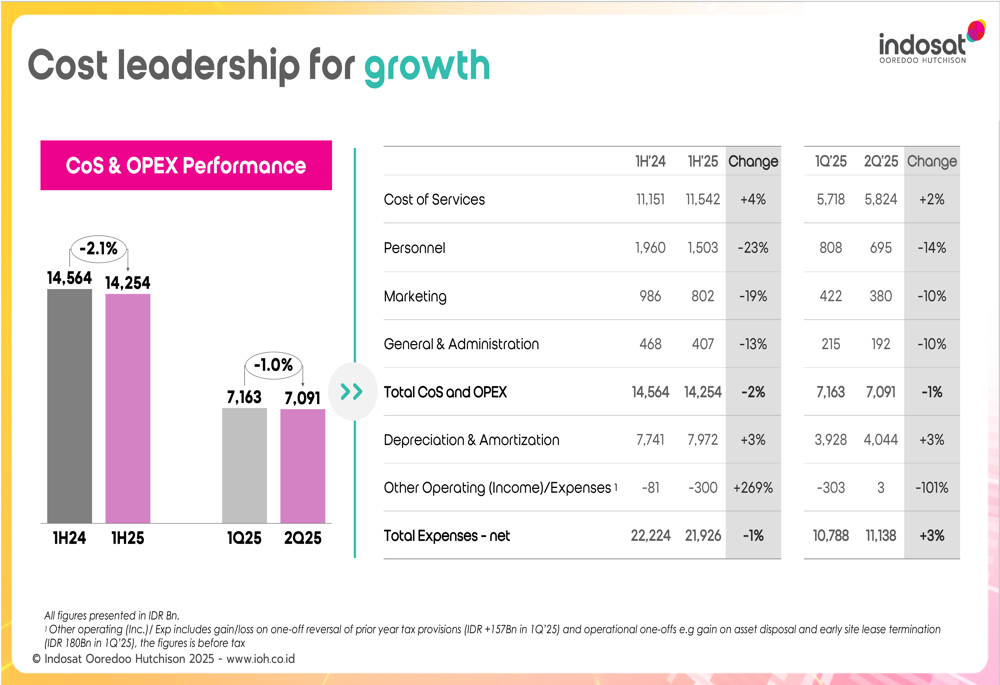

Indosat’s financial performance for Q2 2025 shows a company focused on cost efficiency while investing for future growth. The detailed financial breakdown reveals:

The company has maintained strong cost discipline, with total cost of services and operating expenses decreasing by 1% quarter-over-quarter to IDR 7,091 billion. This cost leadership strategy has been instrumental in preserving profitability despite flat revenue.

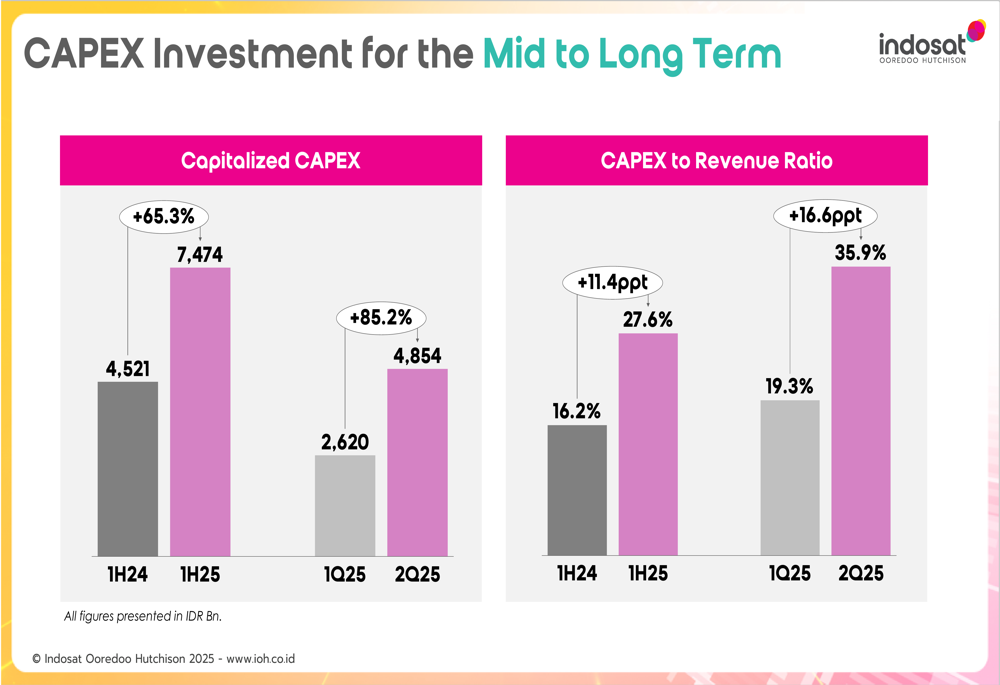

Capital expenditure has increased significantly, with 1H 2025 CAPEX reaching IDR 7,474 billion, a 65.3% increase from IDR 4,521 billion in 1H 2024. The CAPEX to revenue ratio has consequently risen to 27.6% in 1H 2025 from 16.2% in the same period last year, reflecting the company’s commitment to infrastructure investment.

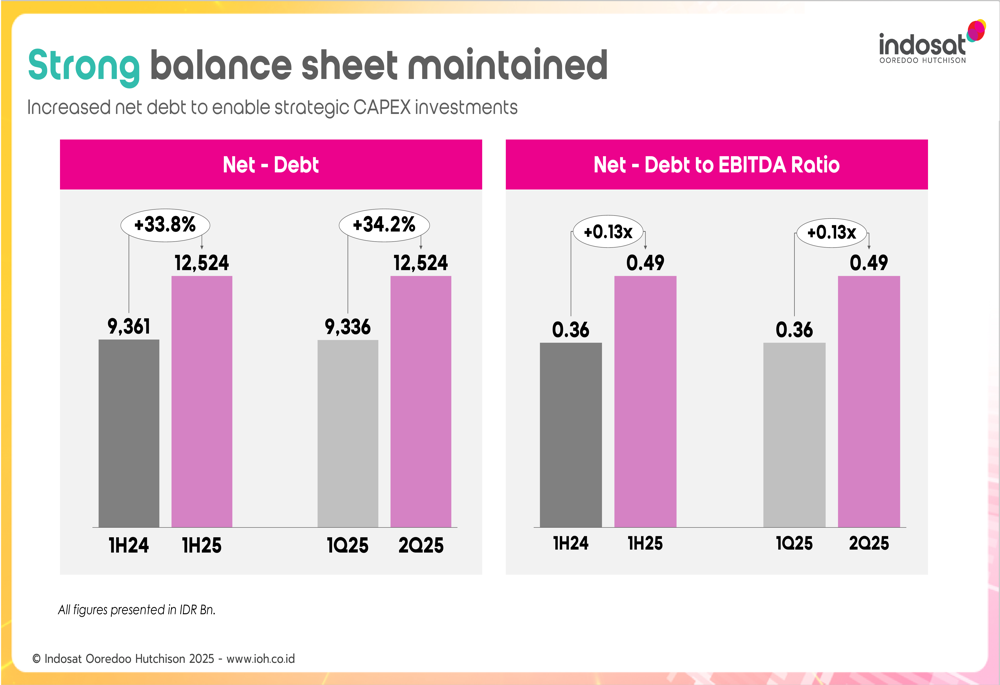

This increased investment has led to higher net debt, which stood at IDR 12,524 billion in Q2 2025, up from IDR 9,336 billion in Q1. However, the company maintains that its balance sheet remains strong with a manageable net debt to EBITDA ratio of 0.49x.

Forward-Looking Statements

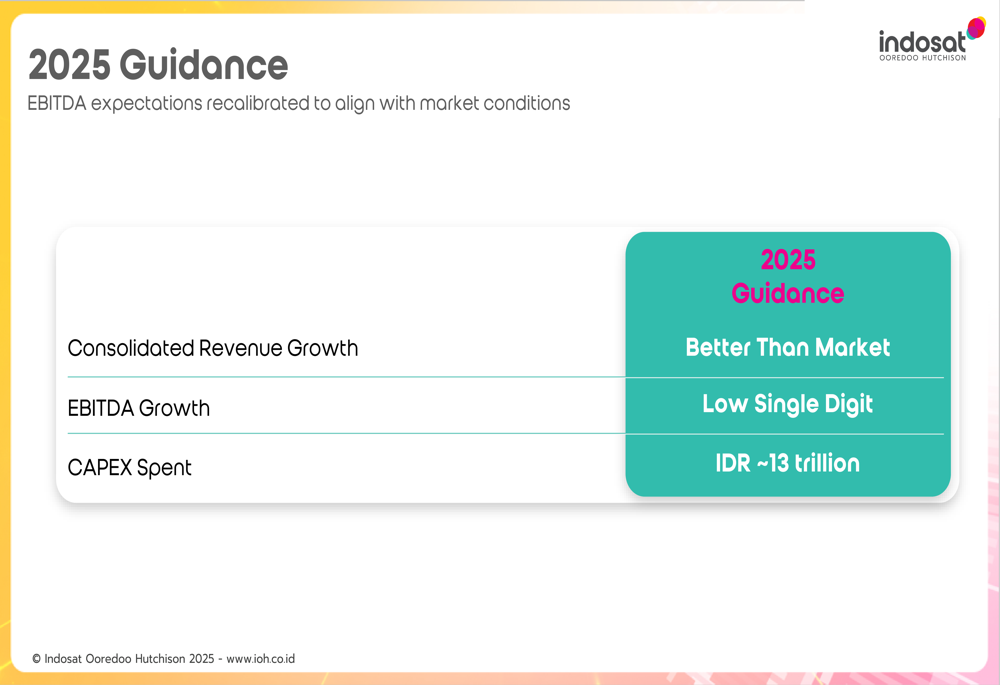

Looking ahead, Indosat provided guidance for 2025, expecting revenue growth to outperform the market, with EBITDA growth in the low single digits. The company plans to invest approximately IDR 13 trillion in CAPEX throughout 2025.

The company’s strategic focus remains on delivering world-class digital experiences while connecting and empowering Indonesians, embodied in its "Gotong Royong" (mutual cooperation) philosophy. Management emphasized its commitment to AI-driven growth, cost efficiencies, and market stabilization to improve industry health.

Indosat’s Q2 2025 results demonstrate a company in transition, balancing immediate profitability through cost management while making substantial investments in technology and infrastructure that it believes will drive future growth. The slight revenue decline and ARPU pressure highlight ongoing challenges in the competitive Indonesian telecommunications market, but the improved EBITDA margin suggests the company’s efficiency measures are yielding results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.