Street Calls of the Week

Introduction & Market Context

Indutrade AB (STO:INDT) shares fell 5.42% on April 25, 2025, despite the industrial conglomerate reporting stable margins and modest growth in its first-quarter presentation. The company’s stock closed at 273.2 SEK after dropping 14.8 SEK during the session, suggesting investors may have expected stronger performance amid ongoing market uncertainty.

President and CEO Bo Annvik, along with CFO Patrik Johnson, presented results showing the company achieved 5% total order intake growth, though organic growth was limited to just 1% as macroeconomic headwinds continued to affect certain business segments.

Quarterly Performance Highlights

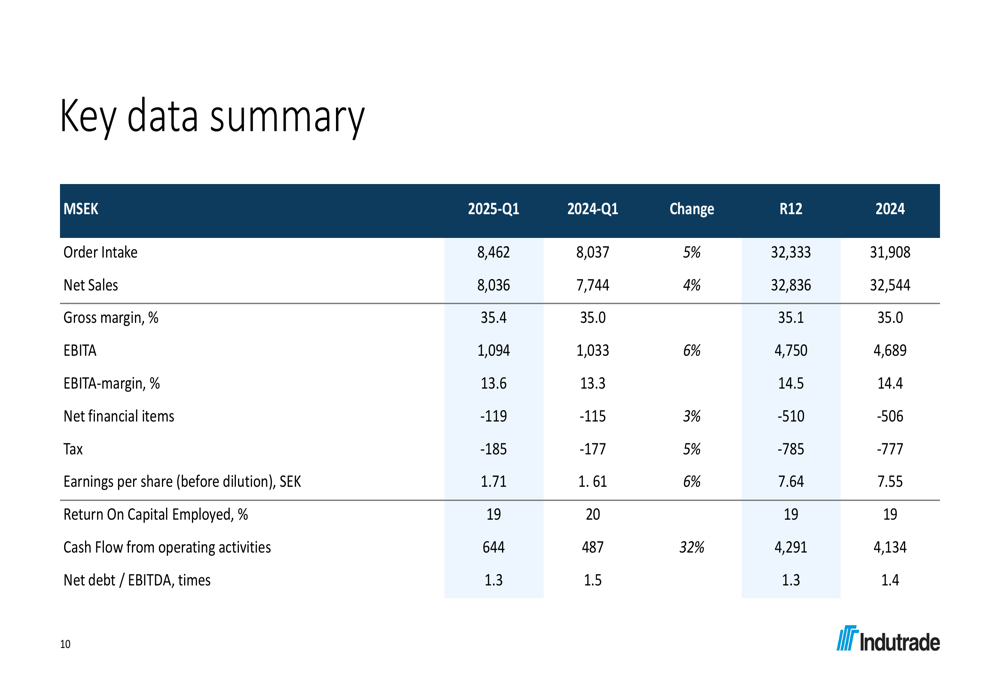

Indutrade reported net sales of 8.0 billion SEK for Q1 2025, representing a 4% total increase compared to the same period last year. Organic sales growth was flat (0%), with acquisitions contributing 4% to the overall growth figure.

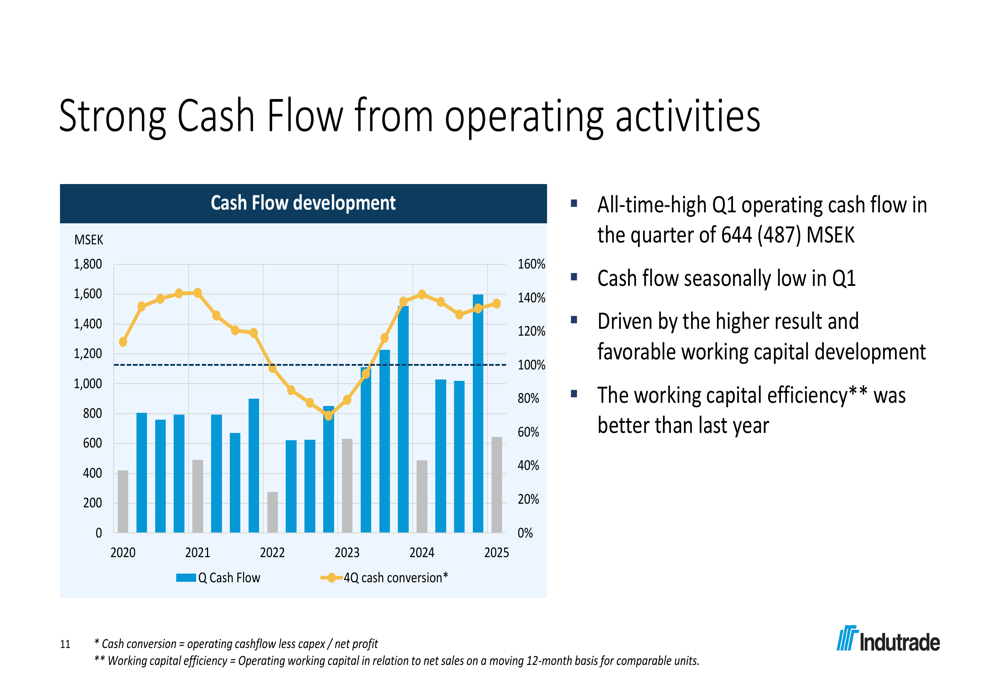

The company highlighted its EBITA margin improvement to 13.6%, up from 13.3% in Q1 2024, while noting record first-quarter operational cash flow of 644 million SEK, a substantial 32% increase from the 487 million SEK reported in the previous year.

As shown in the following chart detailing the company’s key financial metrics:

Earnings per share increased 6% to 1.71 SEK (compared to 1.61 SEK in Q1 2024), while the company maintained a strong financial position with net debt/EBITDA ratio improving to 1.3x from 1.5x a year earlier.

Particularly noteworthy was the improvement in gross margin to 35.4% (up from 35.0%), which the company attributed to good pricing efforts despite inflationary pressures.

Business Segment Analysis

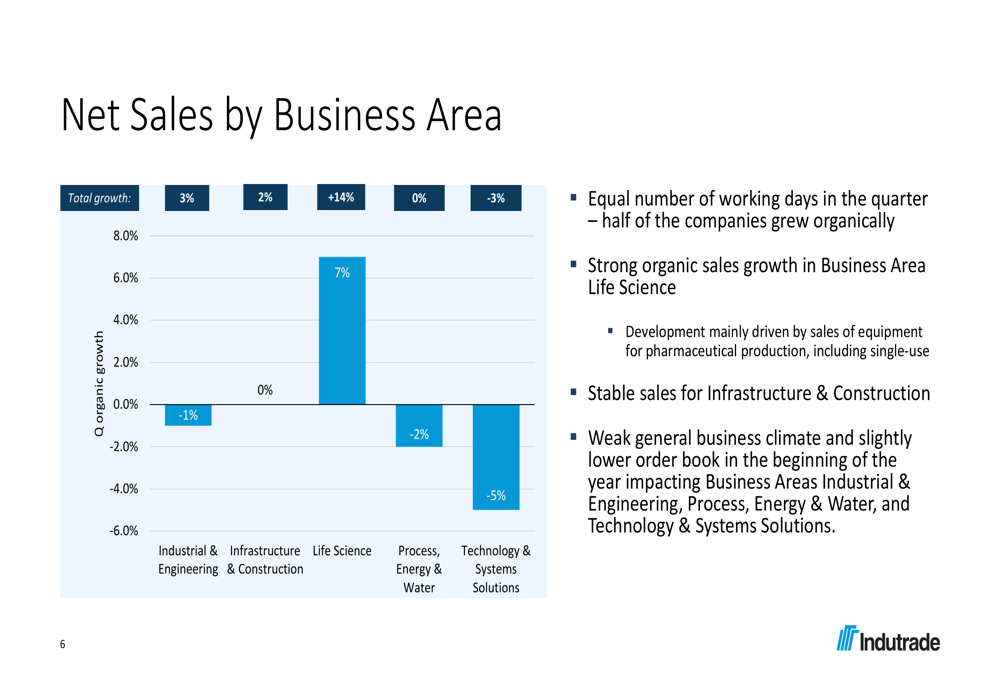

Indutrade’s performance varied significantly across its five business areas, with Life Science emerging as the clear outperformer with 7% organic growth and a strong 16.3% EBITA margin.

The following breakdown illustrates the divergent performance across business segments:

Technology & Systems Solutions faced the most significant challenges with a 5% organic sales decline, while Process, Energy & Water saw a 2% organic decrease. Industrial & Engineering reported a 1% organic decline, while Infrastructure & Construction maintained flat organic sales.

The company noted that half of its companies achieved organic growth during the quarter, with particularly strong demand from customers in pharmaceutical production, process industries, and the energy sector.

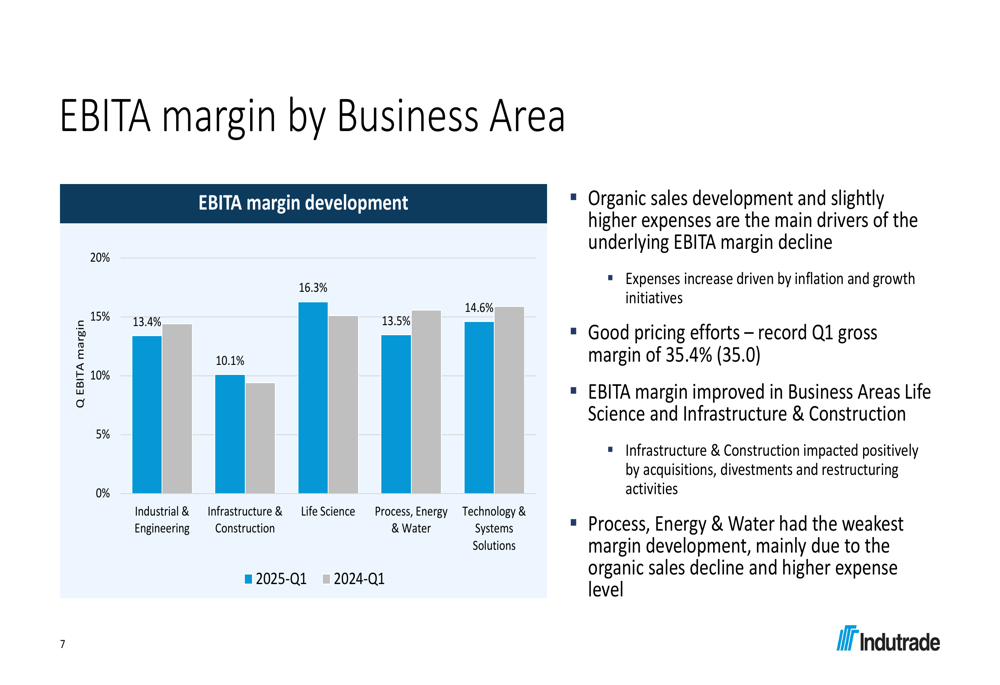

EBITA margin development also showed variation across segments:

Management attributed margin variations primarily to organic sales development and slightly higher expenses driven by inflation and growth initiatives. The presentation highlighted that Process, Energy & Water experienced the weakest margin development, mainly due to organic sales decline and higher expense levels.

Acquisition Strategy & Cash Position

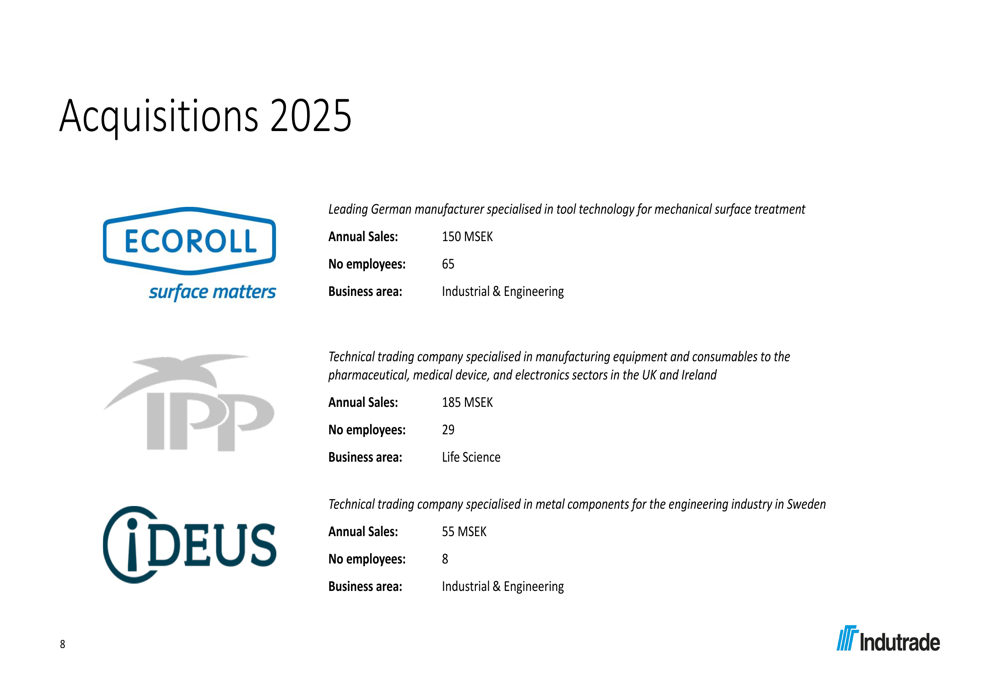

Indutrade continued its acquisition-driven growth strategy, completing three acquisitions in 2025 thus far. These include ECOROLL, a German manufacturer specializing in tool technology; IPP, a UK-based technical trading company serving pharmaceutical and medical device sectors; and ¡DEUS, a Swedish technical trading company focused on metal components.

The following slide details these recent acquisitions:

The company’s strong cash generation has supported both its acquisition strategy and balance sheet improvement. The operational cash flow reached an all-time high for a first quarter at 644 million SEK, driven by improved working capital efficiency.

As illustrated in the following cash flow development chart:

This cash flow strength has enabled Indutrade to reduce its interest-bearing net debt to 7,721 million SEK (down from 8,474 million SEK), with net debt/equity ratio improving to 47% (from 55%).

Forward-Looking Statements

Management acknowledged increased market uncertainty in their outlook, noting a slightly lower order backlog compared to previous periods. The company indicated that many of its businesses are "actively working to adapt costs to the situation prevailing in their markets," suggesting potential efficiency measures in response to challenging conditions.

The key takeaways from the presentation emphasized:

Despite the cautious tone regarding market conditions, management expressed confidence in the company’s "strong platform for long-term sustainable, profitable growth," pointing to its acquisition pipeline and operational improvements as foundations for future performance.

The market’s negative reaction to the results, despite stable margins and improved cash flow, may reflect concerns about the limited organic growth and the potential for continued market uncertainty to impact future quarters. Investors appear to be weighing the company’s acquisition-driven growth strategy against the challenges in generating organic growth across several business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.