Adaptimmune stock plunges after announcing Nasdaq delisting plans

Introduction & Market Context

INFICON Holding (SWX:IFCN) presented its Q2 2025 earnings results on July 30, showcasing sequential growth across most markets despite year-over-year margin challenges. The precision instrument manufacturer, currently trading at 100.20 CHF, reported sales of $167.4 million for the quarter, representing a modest 0.3% increase year-over-year but a more substantial 5.8% growth compared to Q1 2025.

The company’s performance reflects the broader semiconductor industry’s cautious recovery pattern, with INFICON maintaining a book-to-bill ratio above 1 while navigating significant headwinds from international trade tensions and regional market disparities.

Quarterly Performance Highlights

INFICON’s Q2 2025 results revealed a company experiencing sequential growth momentum across most segments, though with significant regional variations. Sales reached $167.4 million, essentially flat year-over-year (+0.3%) but showing 5.8% growth compared to the previous quarter.

As shown in the following quarterly highlights summary:

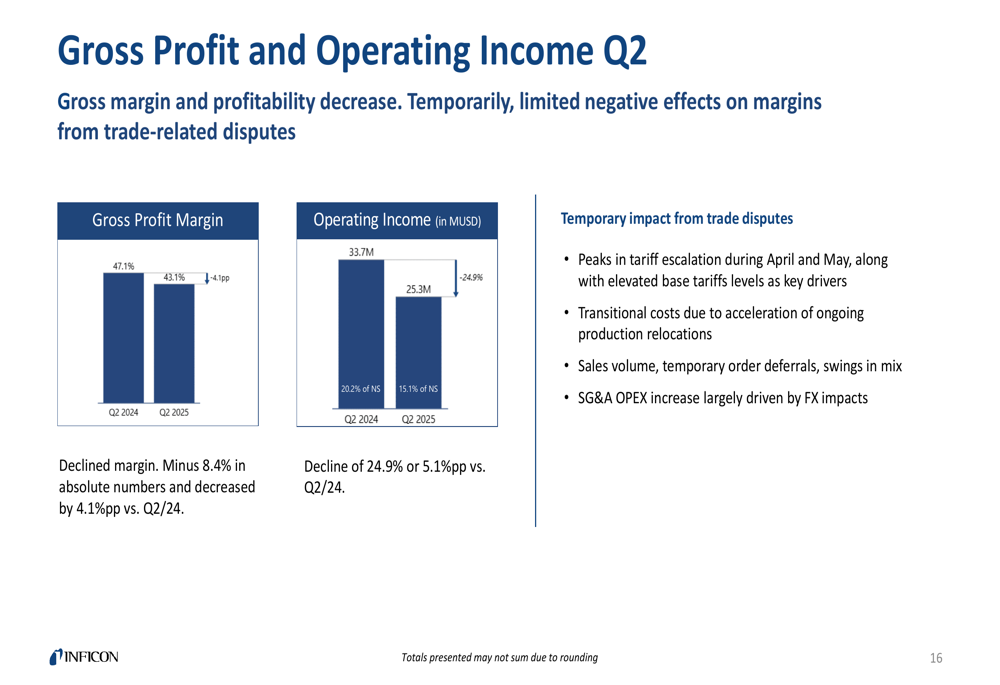

The company’s operating income reached $25.3 million, representing 15.1% of sales but marking a 24.9% decline from the same period last year. This profitability compression stemmed largely from gross margin deterioration, which fell 405 basis points year-over-year to 43.1%. Management attributed this decline to temporary impacts from trade disputes, including tariff escalation during April and May, along with transitional costs from accelerated production relocations.

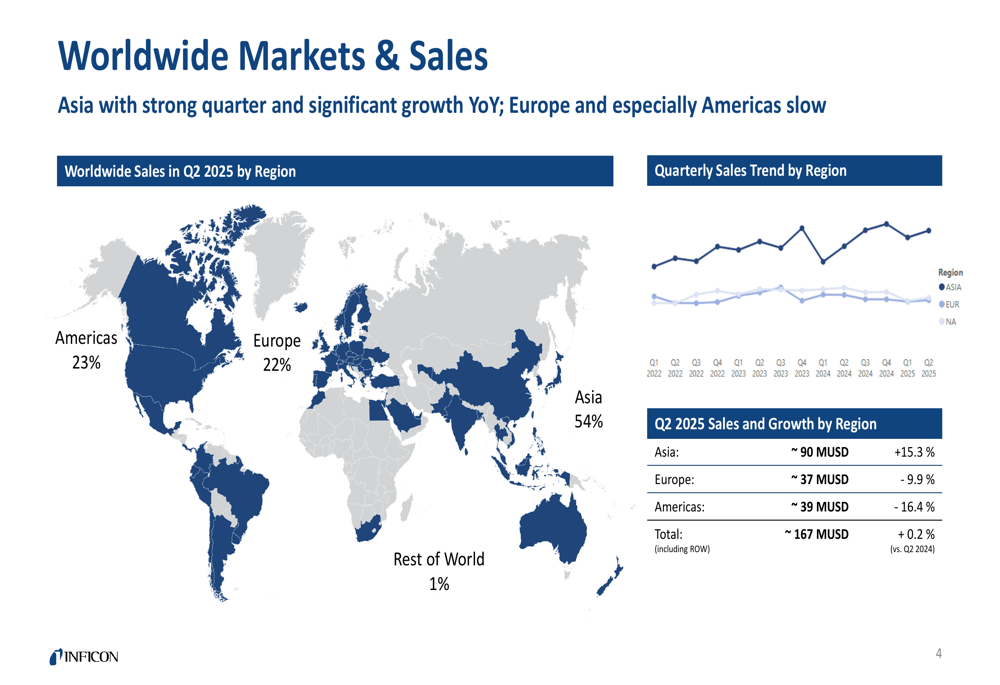

Regional performance diverged significantly, with Asia emerging as the growth engine:

Asian markets generated approximately $90 million in sales, representing 54% of total revenue and growing 15.3% year-over-year. This robust performance contrasted sharply with declines in Europe (-9.9%) and the Americas (-16.4%), which accounted for 22% and 23% of sales, respectively.

Detailed Financial Analysis

INFICON’s Q2 2025 financial performance revealed significant pressure on margins and profitability despite stable sales. The gross profit margin contracted to 43.1%, down from 47.1% in Q2 2024, representing a substantial 4.1 percentage point decline.

This margin compression flowed through to the bottom line, as illustrated in the following chart:

Operating income fell 24.9% year-over-year to $25.3 million, with management citing several factors including trade dispute impacts, transitional costs from production relocations, temporary order deferrals, and unfavorable product mix shifts. Net income declined even more sharply, falling 31.0% to $18.3 million, further impacted by negative foreign exchange effects despite a lower effective tax rate.

On the expense side, INFICON continued investing in future growth, with R&D expenditures increasing 6.3% to $13.9 million. SG&A expenses rose 3.1% to $32.9 million, primarily due to unfavorable currency impacts while underlying costs remained tightly managed.

Strategic Initiatives & Market Position

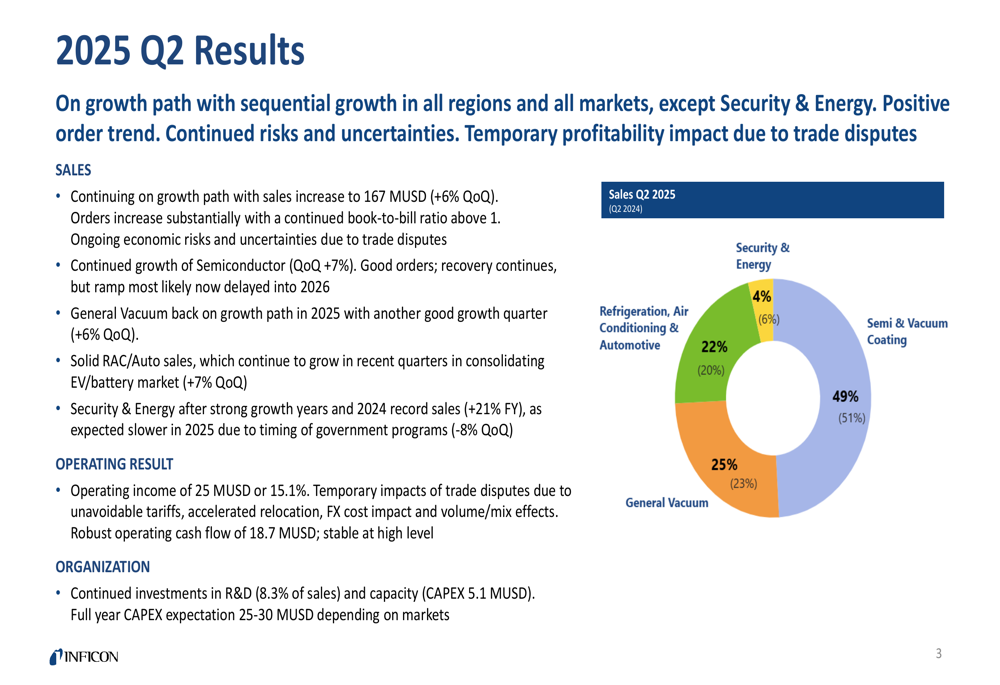

INFICON continues to maintain leadership positions across its four key market segments. In the Semiconductor & Vacuum Coating segment, which represents 49% of total sales, the company holds the #1 position in process control and #2 for pressure measurement. This segment grew 7% sequentially in Q2 and year-to-date.

The company’s market breakdown shows the following distribution:

The Refrigeration, Air Conditioning & Automotive segment, accounting for 22% of sales, grew 7% sequentially with year-to-date growth of 2%. INFICON maintains the #1 position in both the RAC and Battery markets within this segment.

General Vacuum, representing 25% of sales, showed the strongest year-over-year growth at 19% after reaching a trough in 2024, with sequential growth of 6%. Only the Security & Energy segment, which accounts for just 4% of sales, showed weakness with an 8% sequential decline and a 33% year-to-date drop, attributed to the timing of government programs.

INFICON’s global manufacturing reconfiguration continues, with the company highlighting its operational footprint across three main centers of competence in Syracuse (US), Cologne (Germany), and Balzers (Liechtenstein), complemented by eight specialized competence centers worldwide. The company noted that its Malaysia factory is now up and running, supporting the strategic production shift to manage trade tensions.

Forward-Looking Statements

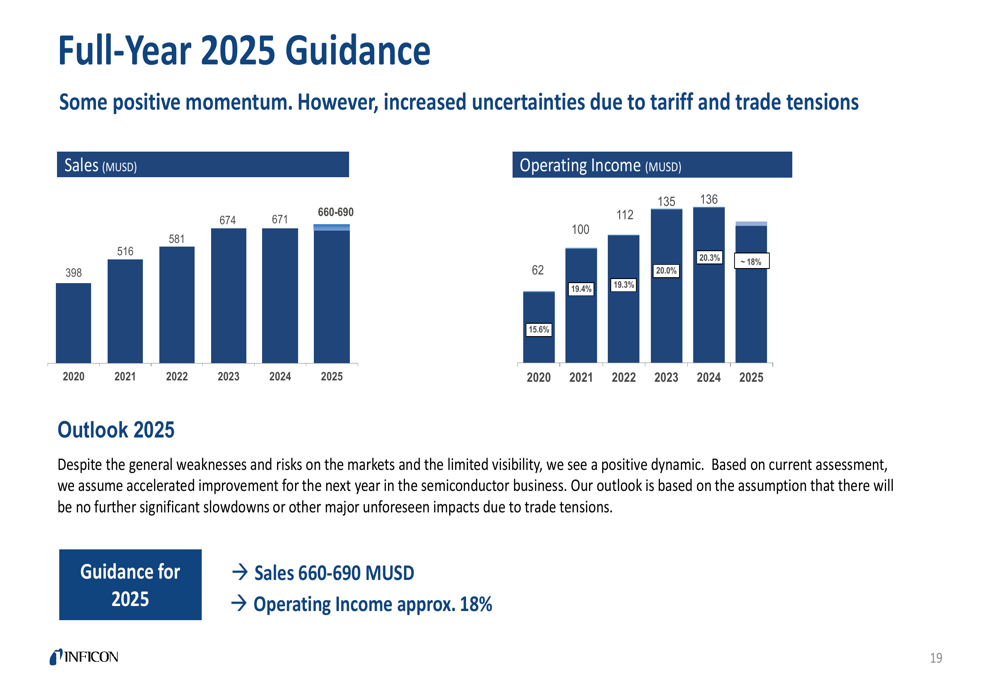

Despite near-term challenges, INFICON maintained its full-year 2025 guidance, projecting sales between $660-690 million and an operating income margin of approximately 18%. This outlook is supported by what management described as "good order entry development" across Semiconductor, RAC/Auto, and General Vacuum markets.

The company’s full-year guidance is illustrated in the following chart:

For the semiconductor segment specifically, INFICON expects market conditions to remain flat with some growth potential in 2025, though it anticipates a more significant ramp to be delayed into 2026. The RAC/Auto segment is projected to see flat to positive growth, while General Vacuum is expected to continue its growth trajectory. Only the Security & Energy segment is forecast to decrease.

Management acknowledged that recent trade tensions add uncertainty and risks to the outlook. The company is actively addressing these challenges through its global manufacturing reconfiguration, including the expansion of production capacity in Malaysia.

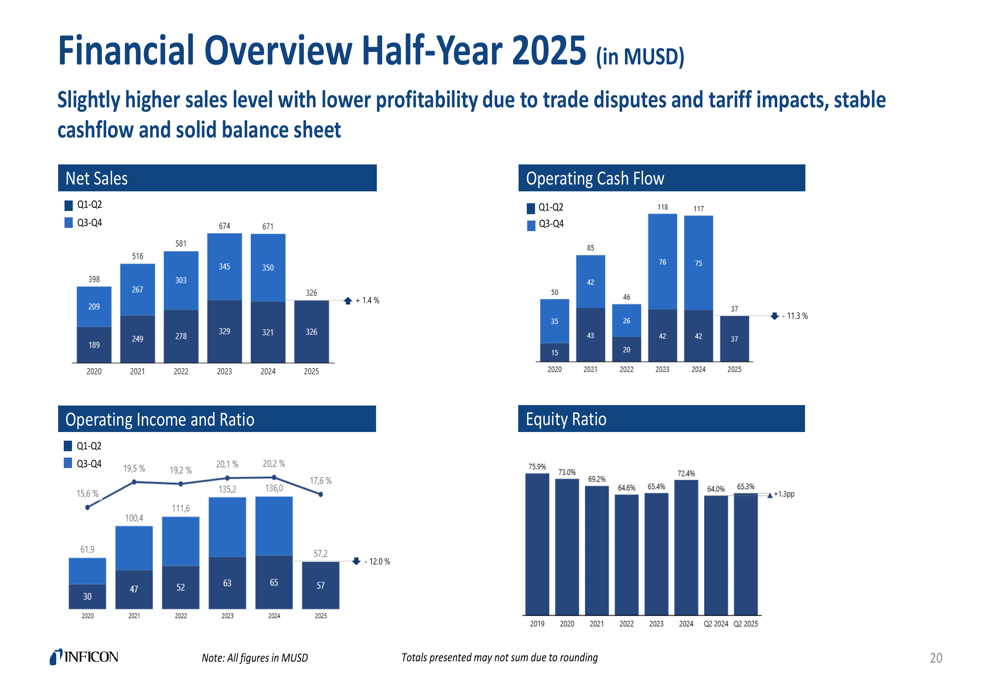

Looking at the half-year financial overview, INFICON has demonstrated resilience in maintaining its equity ratio at 65.3%, up 1 percentage point, while generating $18.7 million in operating cash flow:

With a net cash position of $38.5 million, up $24.4 million from the previous year, INFICON appears well-positioned to continue its strategic investments, with full-year capital expenditure expected to reach $25-30 million as the company continues to invest in R&D and production capacity to support future growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.