Nvidia and TSMC to unveil first domestic wafer for Blackwell chips, Axios reports

Introduction & Market Context

Ingersoll Rand Inc (NYSE:IR) presented its Q2 2025 earnings results on August 1, 2025, highlighting raised full-year guidance despite mixed quarterly performance. The industrial equipment manufacturer’s stock tumbled 7.65% following the announcement, with pre-market trading showing a 5.67% decline, suggesting investors remain concerned about the company’s growth trajectory despite management’s optimistic outlook.

The presentation comes amid a challenging macroeconomic environment with tariff uncertainties and supply chain disruptions continuing to impact industrial manufacturers. While Ingersoll Rand maintains its position as a "premier growth compounder with iconic brands," investors appear skeptical about the company’s ability to maintain momentum in the face of organic growth challenges.

Quarterly Performance Highlights

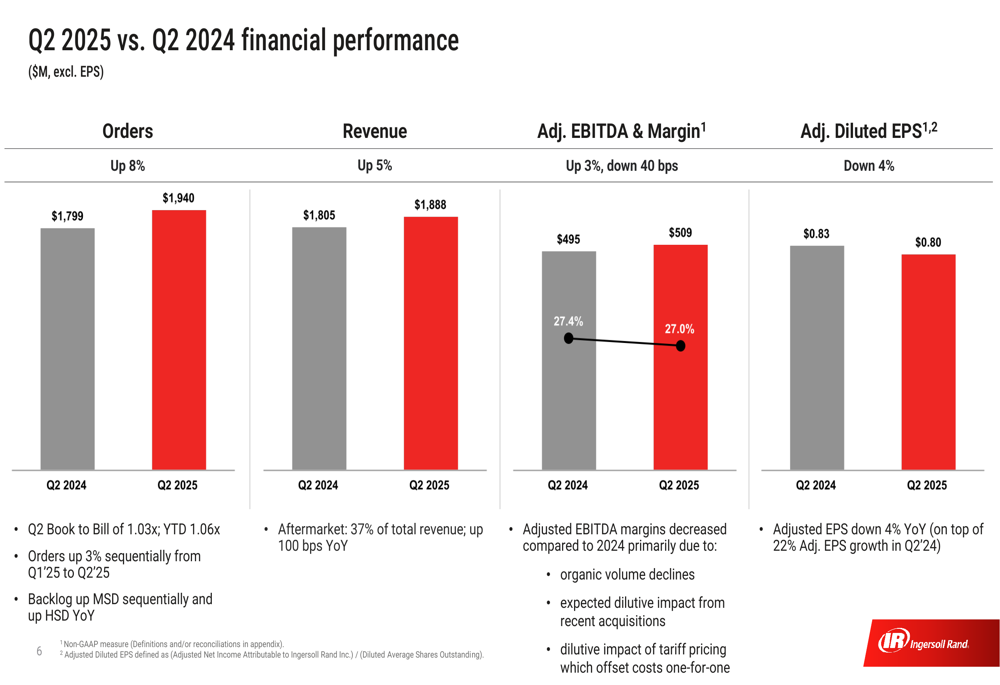

Ingersoll Rand reported mixed financial results for Q2 2025, with strong order growth but declining earnings per share. Orders increased 8% to $1,940 million and revenue grew 5% to $1,888 million compared to Q2 2024. Adjusted EBITDA rose 3% to $509 million, while adjusted diluted EPS declined 4% to $0.80.

As shown in the following quarterly performance comparison:

The company maintained a book-to-bill ratio of 1.03x for Q2 and 1.06x year-to-date, indicating continued demand momentum. Aftermarket business represented 37% of revenue, providing stability to the overall business model. However, adjusted EBITDA margins decreased due to organic volume declines and the dilutive impact from recent acquisitions.

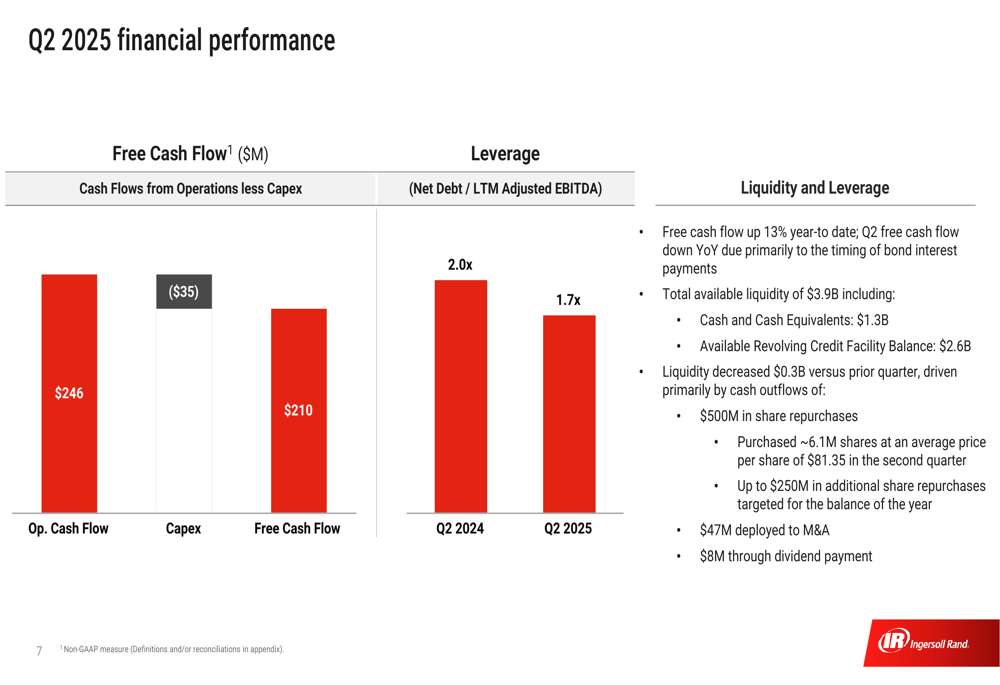

Free cash flow showed strength at $210 million for the quarter, up 13% year-to-date, while the company’s leverage ratio improved to 1.7x from 2.0x in the prior year period. Total (EPA:TTEF) available liquidity stood at $3.9 billion, including $1.3 billion in cash and cash equivalents, though liquidity decreased by $0.3 billion versus the prior quarter primarily due to $500 million in share repurchases.

Segment Analysis

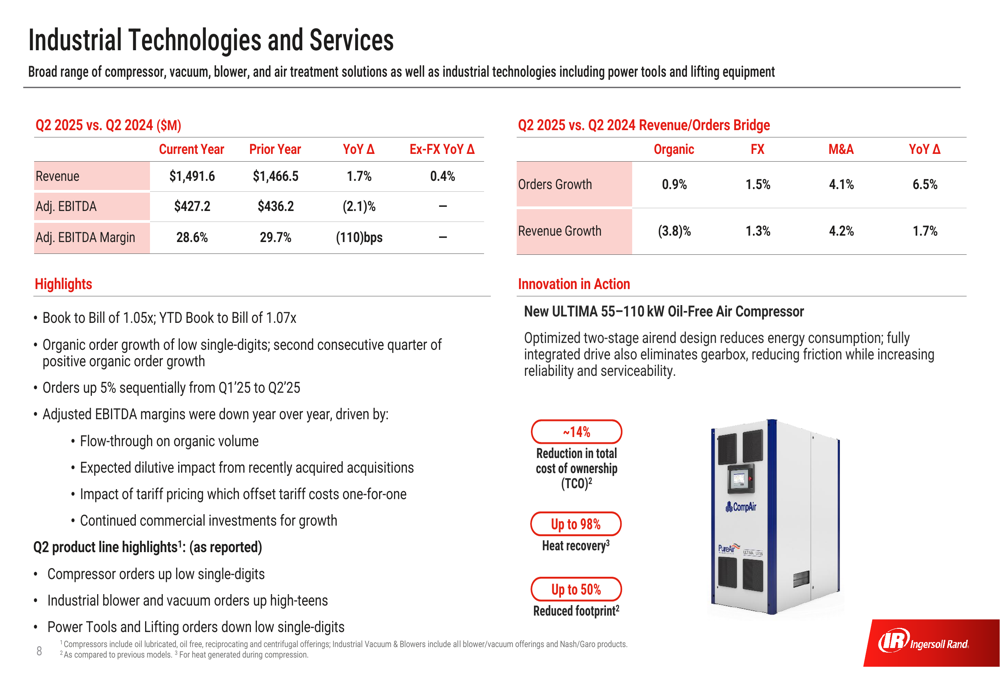

Ingersoll Rand’s two main business segments showed divergent performance in Q2 2025. The Industrial Technologies and Services (ITS) segment, which represents approximately 79% of total revenue, reported modest growth with revenue increasing 1.7% to $1,491.6 million compared to Q2 2024. Adjusted EBITDA for this segment was $427.2 million with a margin of 28.6%. Orders growth was minimal at 0.9%, indicating potential challenges ahead for this core business.

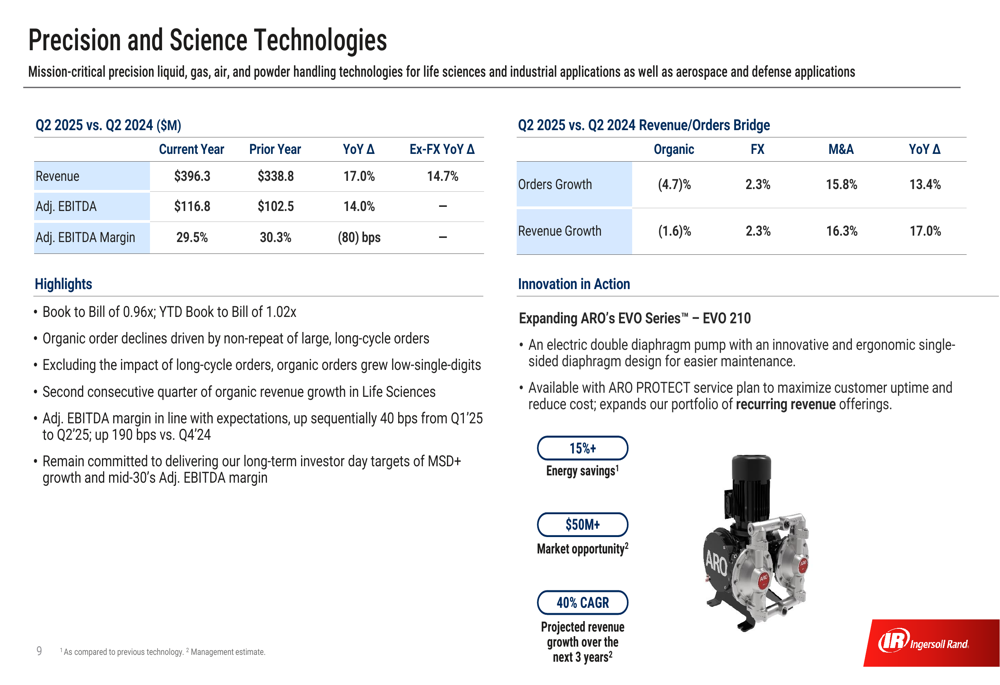

In contrast, the Precision and Science Technologies (PST) segment demonstrated robust performance with revenue increasing 17.0% to $396.3 million and adjusted EBITDA reaching $116.8 million. This segment’s stronger growth partially offset the slower performance in the larger ITS segment, highlighting the importance of the company’s diversified business model.

M&A Strategy and Execution

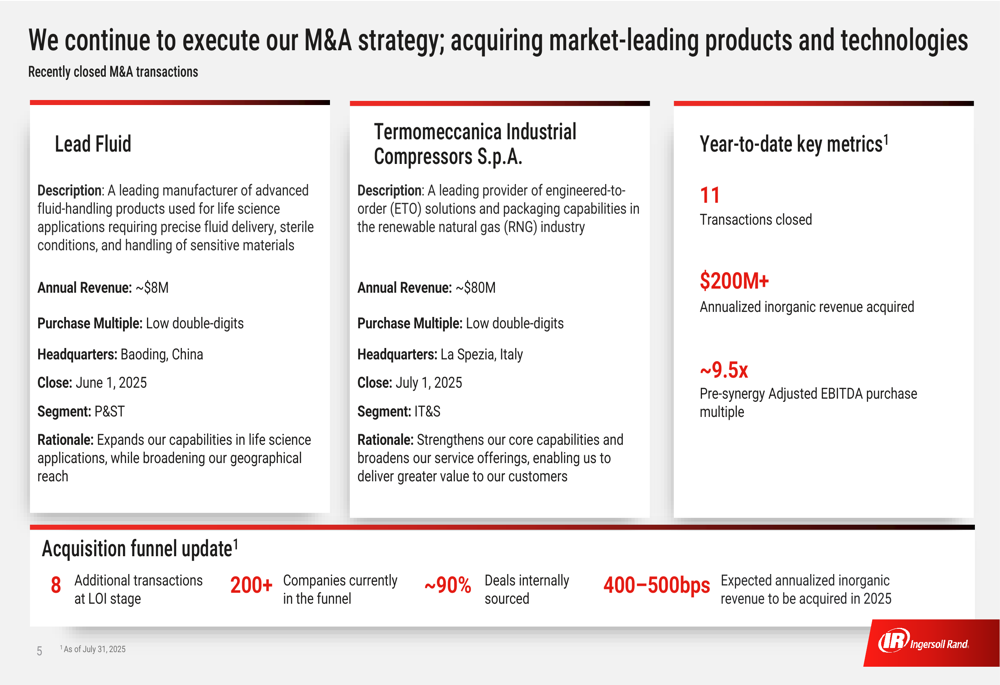

Acquisition activity remains a cornerstone of Ingersoll Rand’s growth strategy, particularly important given the challenges in organic growth. The company closed 11 transactions year-to-date, acquiring over $200 million in annualized inorganic revenue. Recent notable acquisitions include Lead Fluid and Termomeccanica Industrial Compressors S.p.A.

The company’s acquisition pipeline remains robust with 8 additional transactions at the LOI (Letter of Intent) stage and more than 200 companies currently in the funnel, suggesting continued emphasis on growth through acquisition rather than organic expansion.

Revised Guidance and Outlook

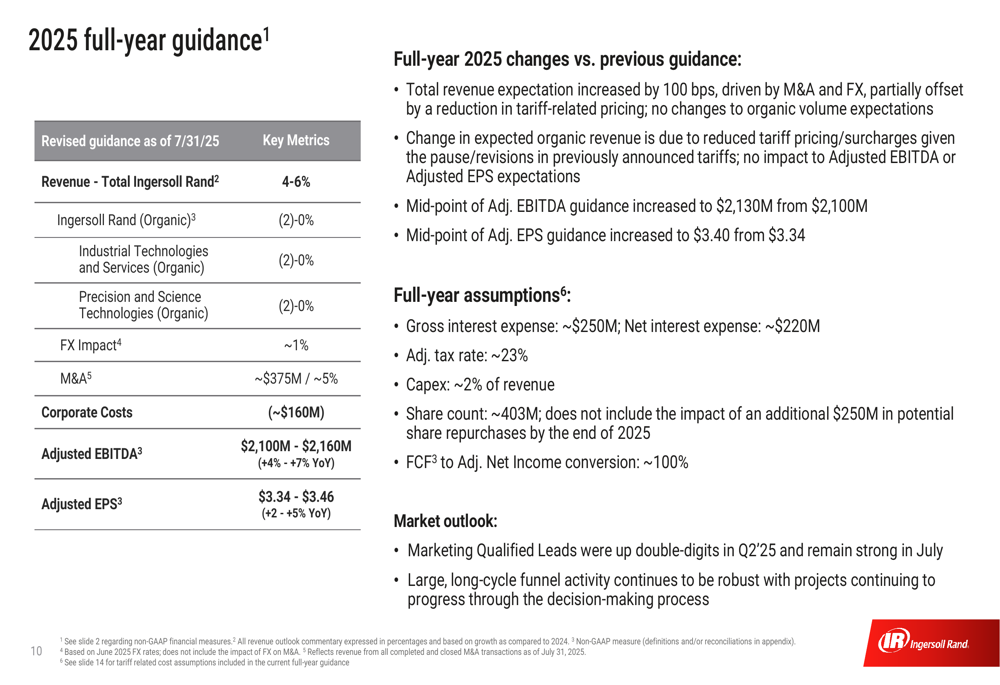

Despite mixed quarterly results, Ingersoll Rand raised its full-year 2025 guidance across key metrics. The company now expects total revenue growth of 4-6%, with organic growth between -2% and 0%, indicating continued challenges in core business growth offset by acquisitions contributing approximately $375 million. Foreign exchange impact is expected to be around 1%.

Adjusted EBITDA guidance was raised to $2,100-$2,160 million, while adjusted EPS guidance increased to $3.34-$3.46. The guidance includes assumptions for $80 million in tariff costs based on tariffs as of July 1, 2025, reflecting the impact of ongoing trade tensions.

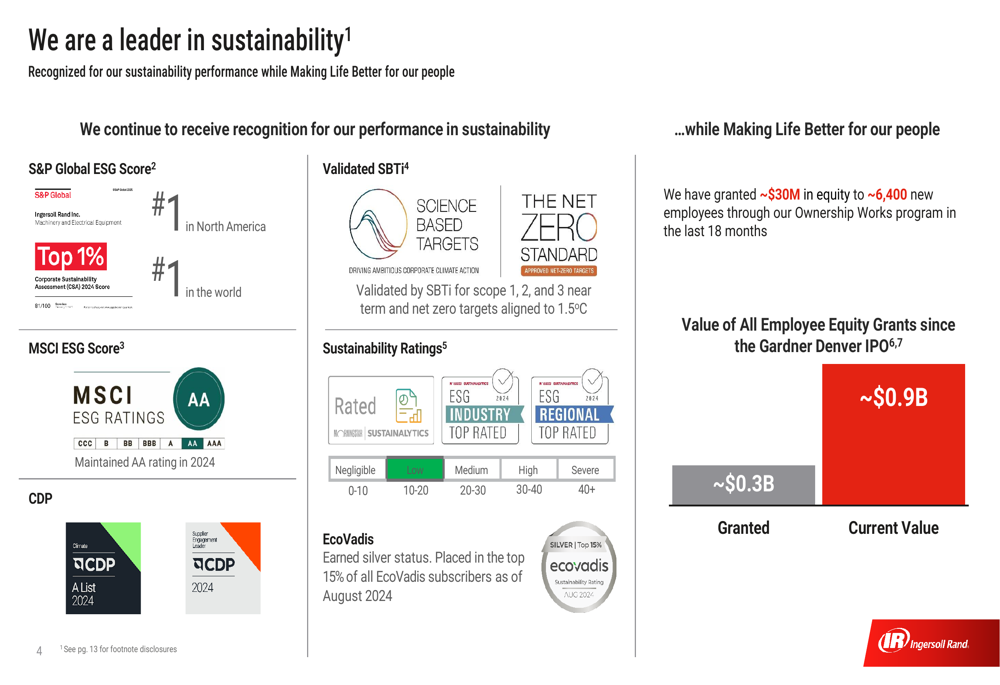

The company emphasized its sustainability leadership as a key differentiator, highlighting its top 1% S&P Global ESG Score, #1 ranking in North America and worldwide, and AA MSCI ESG Rating. These credentials may provide long-term strategic advantages despite near-term growth challenges.

Market Reaction and Challenges

Despite the raised guidance and management’s confident tone, Ingersoll Rand’s stock fell sharply following the earnings announcement. According to real-time market data, the stock was down 7.65% in regular trading, with pre-market activity showing a 5.67% decline.

The negative market reaction suggests investors remain concerned about several key challenges:

1. Organic growth remains under pressure, with full-year organic growth guidance of -2% to 0%

2. Adjusted EPS declined 4% year-over-year despite revenue growth

3. Tariff impacts creating uncertainty ($80 million cost assumption)

4. Heavy reliance on acquisitions for growth rather than core business expansion

5. Potential dilutive impact of acquisitions on margins

Management emphasized its strategic approach to navigate these challenges, focusing on "controlling what we can control" in a "dynamic environment" through the company’s IRX operating system. The company’s key takeaways highlighted remaining nimble, continuing to differentiate as an investment, executing on strategic opportunities, and maintaining disciplined capital allocation.

While Ingersoll Rand maintains a positive long-term outlook based on its strong order backlog and acquisition pipeline, the market’s immediate reaction suggests investors will need more convincing evidence of sustainable organic growth before regaining confidence in the company’s premium valuation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.