Helen of Troy beats Q2 estimates, shares rise on better-than-expected results

Ingevity Corporation (NYSE:NGVT) reported its first quarter 2025 financial results on May 6, showcasing significant margin expansion and earnings growth despite lower sales, as the company’s strategic repositioning efforts continue to yield positive results.

Executive Summary

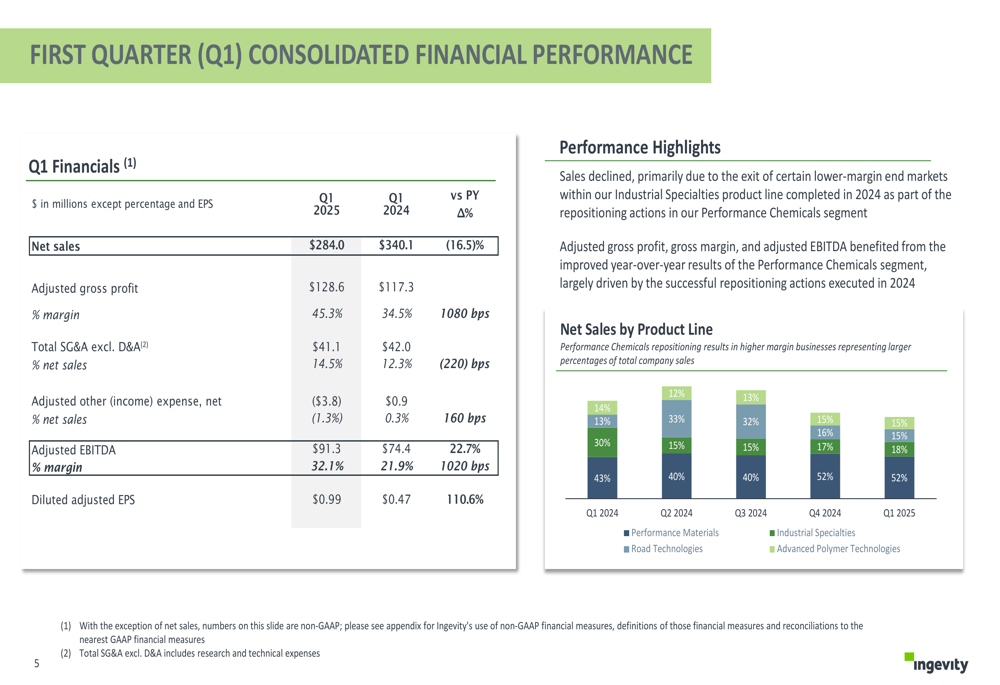

Ingevity delivered its fourth consecutive quarter of higher year-over-year margins in Q1 2025, with adjusted EBITDA margin expanding by 1,020 basis points to 32.1%. While net sales declined 16.5% to $284.0 million compared to $340.1 million in Q1 2024, diluted adjusted earnings per share more than doubled to $0.99 from $0.47 in the prior-year period, representing a 110.6% increase.

The company also announced that David H. Li was named President and CEO effective April 7, 2025, as Ingevity continues to execute on its strategic repositioning plan, particularly in the Performance Chemicals segment.

As shown in the following consolidated financial performance chart, the company’s margin expansion was substantial despite the revenue decline:

Quarterly Performance Highlights

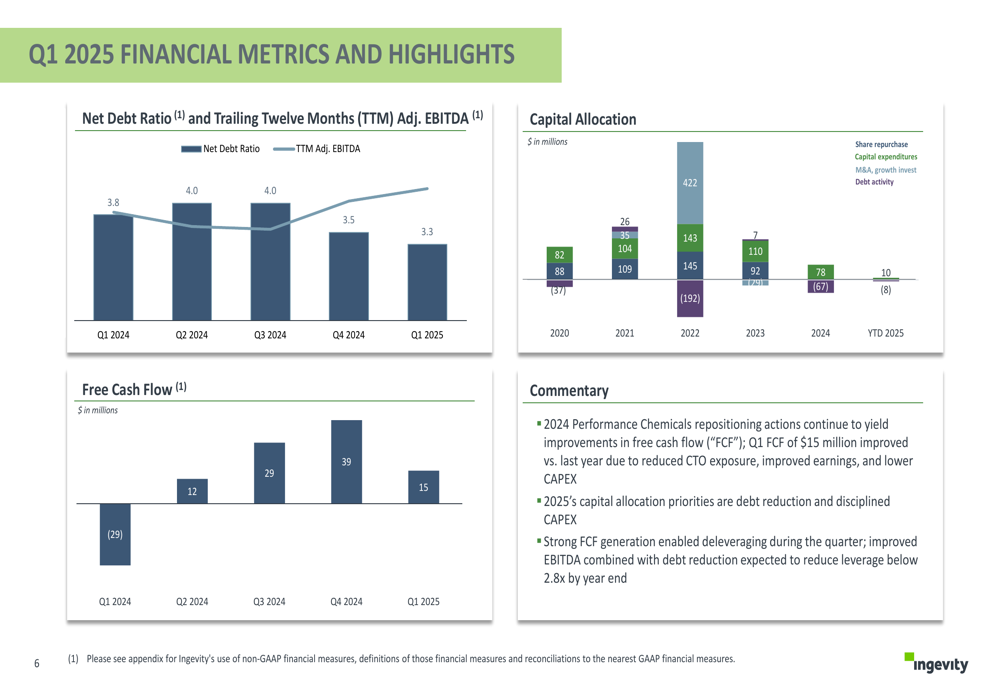

Ingevity’s Q1 2025 results demonstrated significant improvement in profitability metrics, with adjusted gross profit margin increasing to 45.3%, representing a 1,080 basis point improvement year-over-year. The company also reported positive free cash flow of $15 million in Q1 2025, compared to negative $29 million in Q1 2024.

The improved cash flow and earnings helped Ingevity reduce its net debt ratio from 3.8x in Q1 2024 to 3.3x in Q1 2025, with management expecting further deleveraging to below 2.8x by year-end.

The following chart illustrates the company’s improving financial metrics:

"2024 Performance Chemicals repositioning actions continue to yield improvements in free cash flow," the company noted in its presentation. "Q1 FCF of $15 million improved versus last year due to reduced CTO exposure, improved earnings, and lower CAPEX."

Segment Performance Analysis

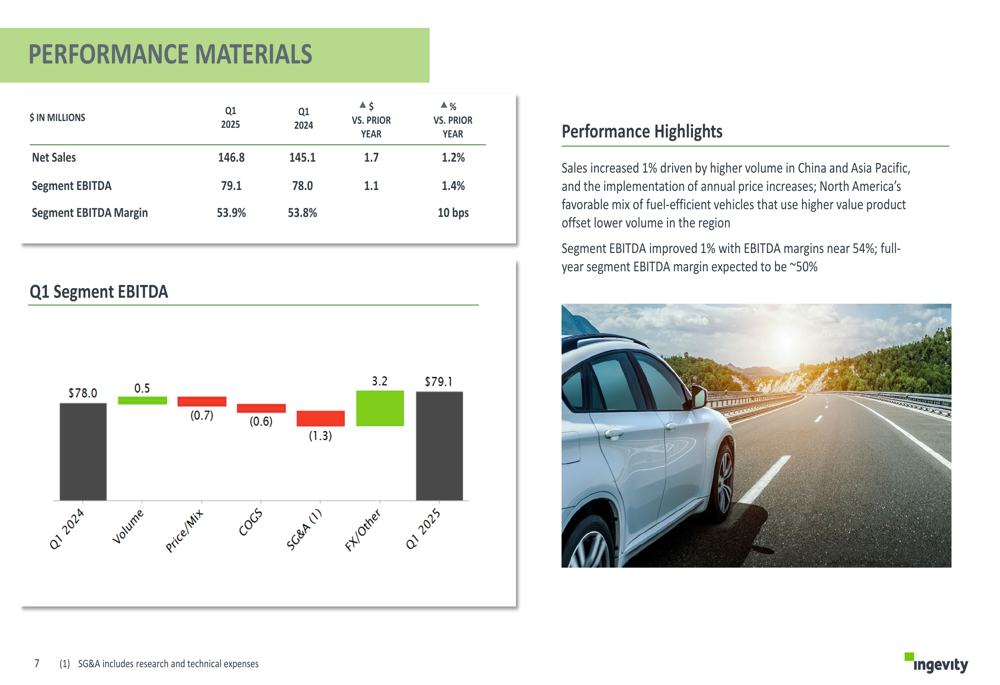

Ingevity’s three business segments delivered mixed results, with Performance Materials continuing to be the standout performer.

The Performance Materials segment, which now accounts for 52% of total sales, reported a 1.2% increase in net sales to $146.8 million and a 1.4% increase in segment EBITDA to $79.1 million. This segment maintained its impressive EBITDA margin of 53.9%, marking its seventh consecutive quarter with margins exceeding 50%.

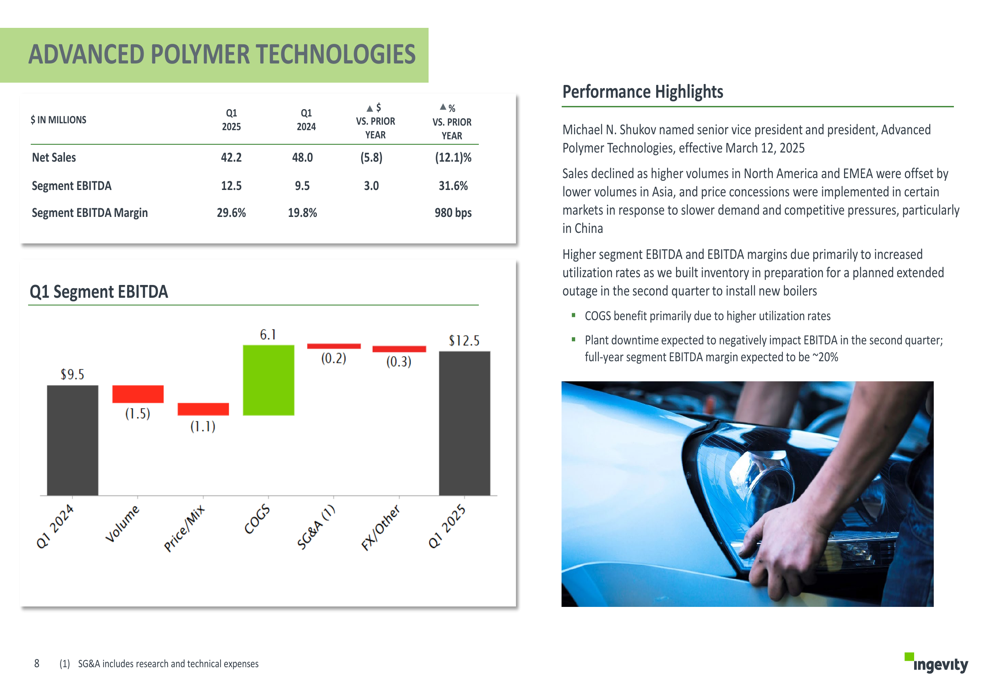

The Advanced Polymer Technologies segment experienced a 12.1% decline in net sales to $42.2 million, but segment EBITDA increased by 31.6% to $12.5 million, with margins expanding 980 basis points to 29.6%. The company attributed this improvement primarily to "increased utilization rates as we built inventory in preparation for a planned extended outage in the second quarter to install new boilers."

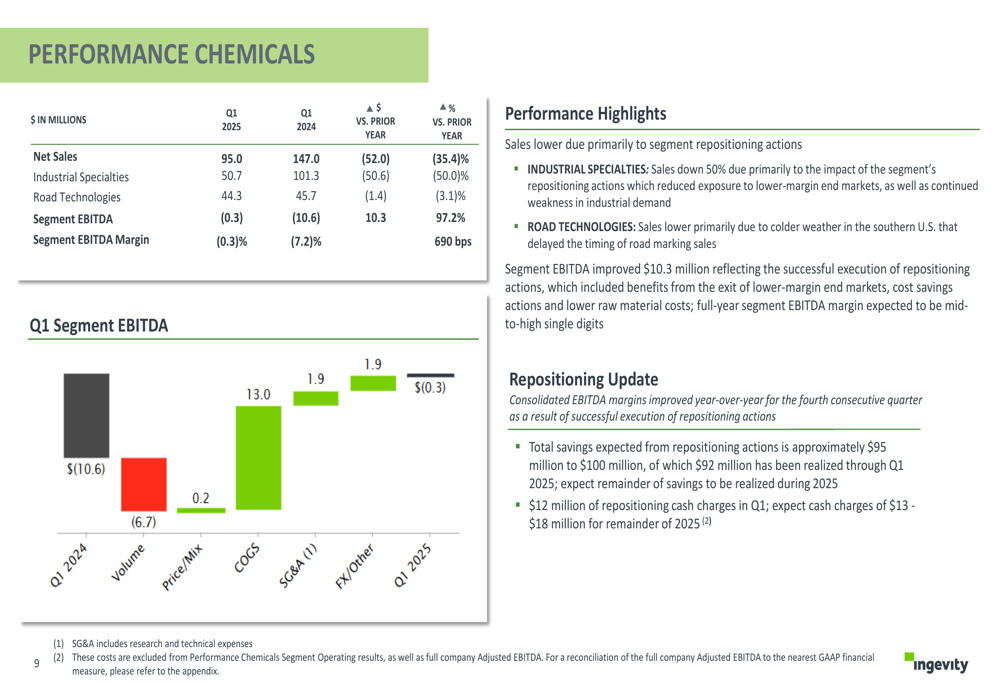

The Performance Chemicals segment, which has been the focus of Ingevity’s repositioning efforts, saw a 35.4% decline in net sales to $95.0 million. However, segment EBITDA improved dramatically from -$10.6 million in Q1 2024 to -$0.3 million in Q1 2025, representing a 97.2% improvement. The segment’s EBITDA margin improved by 690 basis points to -0.3%.

Strategic Initiatives & Repositioning

Ingevity’s presentation highlighted the continued progress of its Performance Chemicals repositioning actions, which are expected to deliver approximately $95-100 million in total savings. The company incurred $12 million of repositioning cash charges in Q1 2025.

The strategic actions on Industrial Specialties and the CTO refinery are progressing well, according to management. These initiatives are part of Ingevity’s broader strategy to focus on higher-margin businesses and improve overall profitability.

This strategic shift is evident in the changing composition of the company’s sales mix. As shown in the Q1 consolidated financial performance slide, Performance Materials now represents 52% of net sales, followed by Advanced Polymer Technologies at 18%, with Industrial Specialties and Road Technologies each accounting for 15%.

Forward-Looking Statements & Guidance

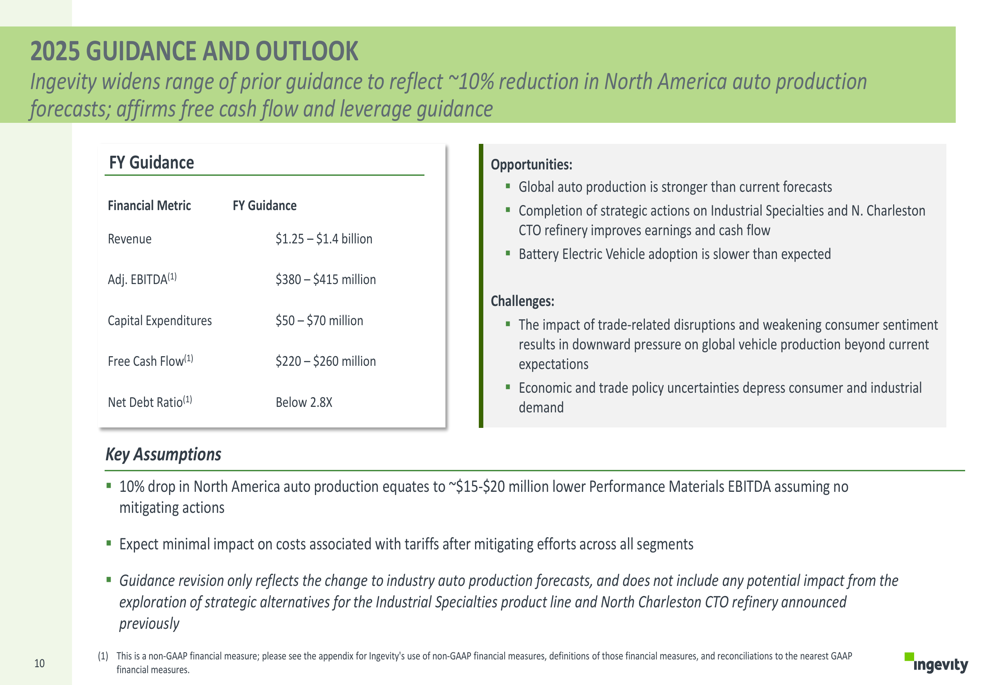

For the full year 2025, Ingevity provided guidance for revenue between $1.25-1.4 billion and adjusted EBITDA of $380-415 million. The company expects capital expenditures of $50-70 million and free cash flow of $220-260 million, with a net debt ratio target below 2.8x by year-end.

The following slide details the company’s 2025 guidance and key assumptions:

Notably, Ingevity widened its guidance range to reflect updated industry forecasts that estimate a drop in auto production in the North America market. The company stated that a 10% drop in North America auto production would equate to approximately $15-20 million lower Performance Materials EBITDA, assuming no mitigating actions.

The company also expects minimal impact on costs associated with tariffs after implementing mitigating efforts across all segments, and emphasized that the guidance revision only reflects the change to industry auto production forecasts.

For the Performance Chemicals segment, Ingevity expects full-year EBITDA margins to reach mid-to-high single digits, while Performance Materials is projected to maintain EBITDA margins of approximately 50%. The Advanced Polymer Technologies segment is expected to achieve full-year EBITDA margins of around 20%.

With these projections and the continued execution of its strategic initiatives, Ingevity appears well-positioned to further improve its financial performance throughout 2025, despite potential headwinds in the automotive industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.