Bill Gross warns on gold momentum as regional bank stocks tumble

Introduction & Market Context

Innate Pharma (NASDAQ:IPHA) presented its H1 2025 business update and financial results on September 17, 2025, highlighting a strategic refocus on its highest-value clinical assets. The company’s stock has experienced pressure over the past year, trading at €1.79 as of the presentation date, down 1.67% for the session and near its 52-week range of €1.33-€2.50.

The presentation, led by CEO Jonathan Dickinson, outlined the company’s path forward with emphasis on three key clinical programs: IPH4502 (a novel Nectin-4 ADC), Lacutamab (which recently received FDA Breakthrough Therapy Designation), and Monalizumab (partnered with AstraZeneca).

Executive Summary

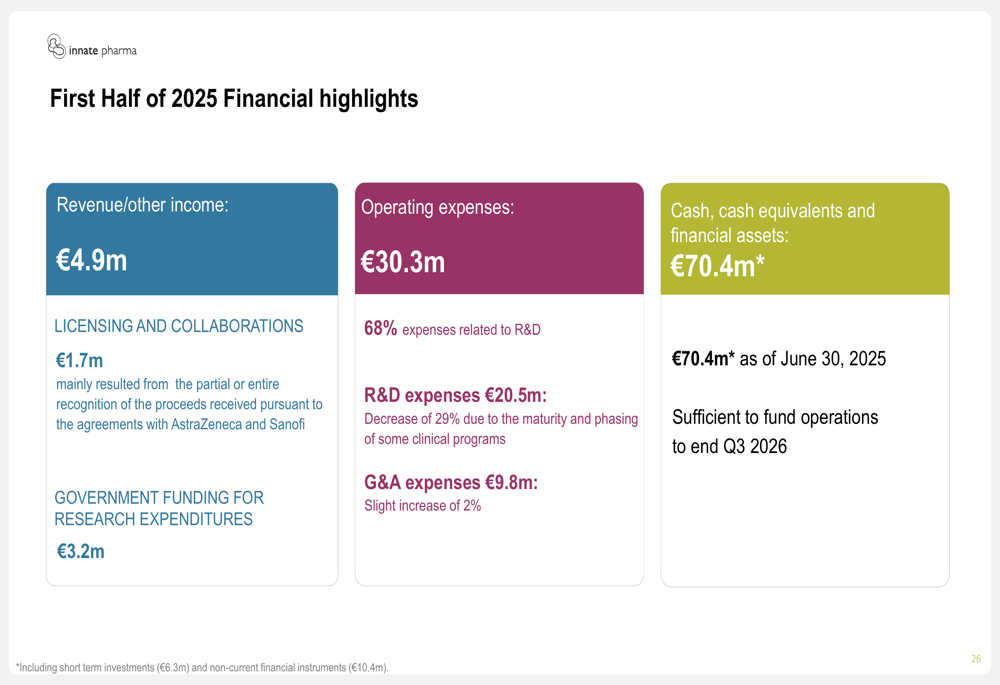

Innate Pharma reported revenue of €4.9 million for H1 2025, with operating expenses of €30.3 million. The company maintained a cash position of €70.4 million as of June 30, 2025, which management expects will fund operations until the end of Q3 2026.

"We are concentrating our investment on what we believe are our highest value clinical stage assets," stated CEO Jonathan Dickinson during the presentation, emphasizing the company’s strategic shift toward streamlining operations while advancing its most promising programs.

The company’s strategy leverages its scientific expertise in antibody engineering, focusing on innate immunity, Natural Killer cell biology, and next-generation antibodies to address cancers with high unmet medical needs.

Clinical Pipeline Progress

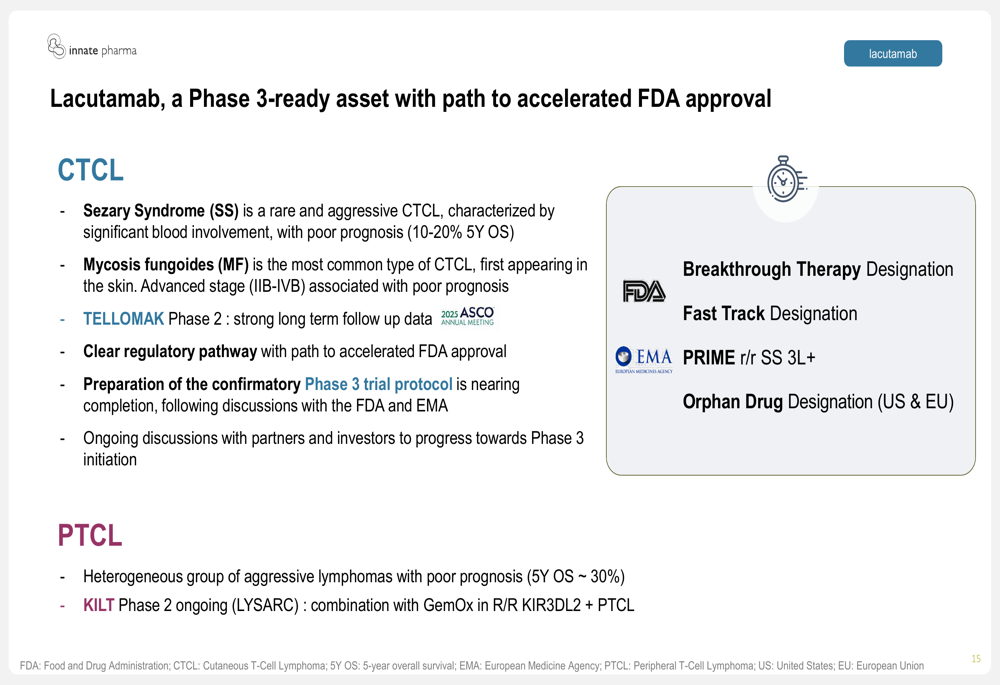

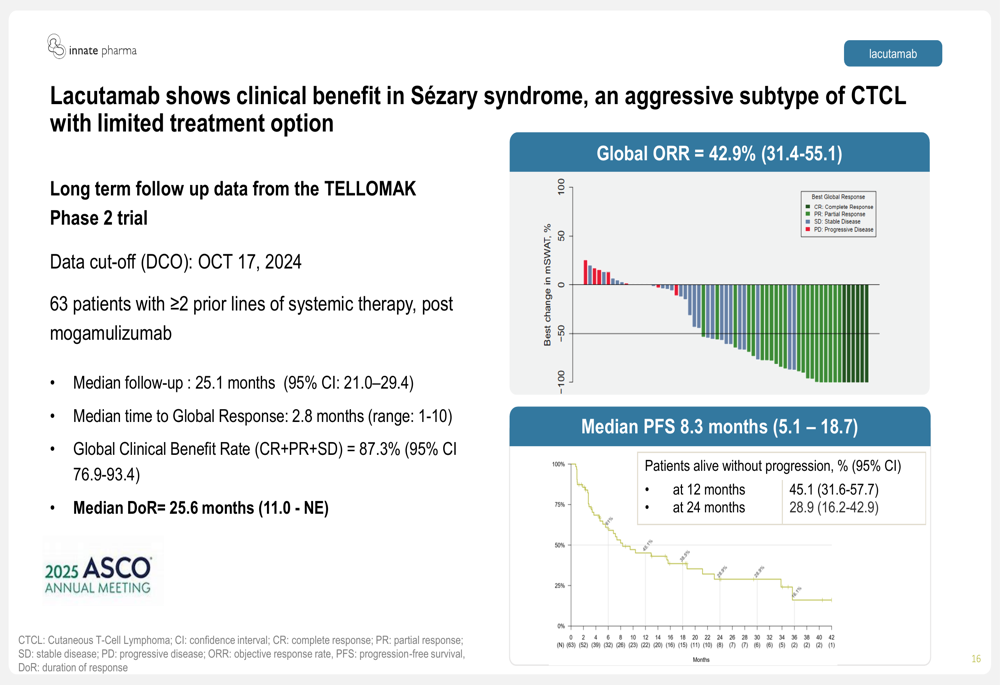

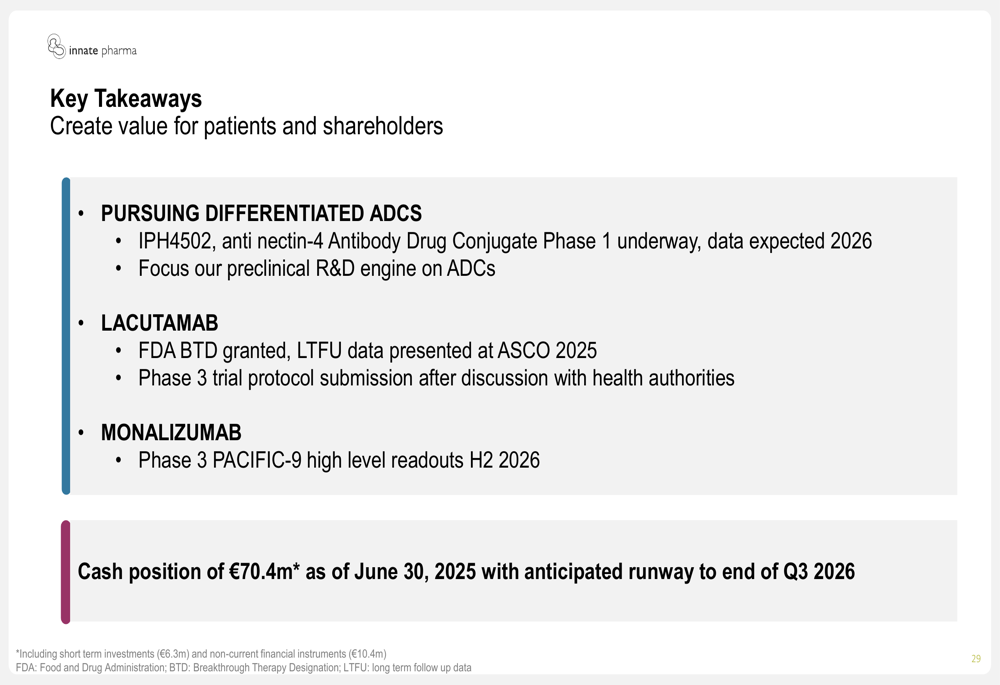

Lacutamab, Innate’s most advanced asset, has emerged as a Phase 3-ready candidate with a path to accelerated FDA approval for treating cutaneous T-cell lymphoma (CTCL). The presentation highlighted impressive long-term follow-up data from the TELLOMAK Phase 2 trial, showing a global clinical benefit rate of 87.3% in Sézary syndrome patients with a median duration of response of 25.6 months.

"Lacutamab has the potential to fundamentally reshape the care of CTCL patients," noted Dickinson, pointing to the asset’s potential for earlier use in the treatment paradigm. The company is preparing the confirmatory Phase 3 trial protocol following discussions with health authorities.

The clinical benefit data presented for Lacutamab in Sézary syndrome demonstrated meaningful activity in this difficult-to-treat patient population, with a global objective response rate of 42.9% and median progression-free survival of 8.3 months.

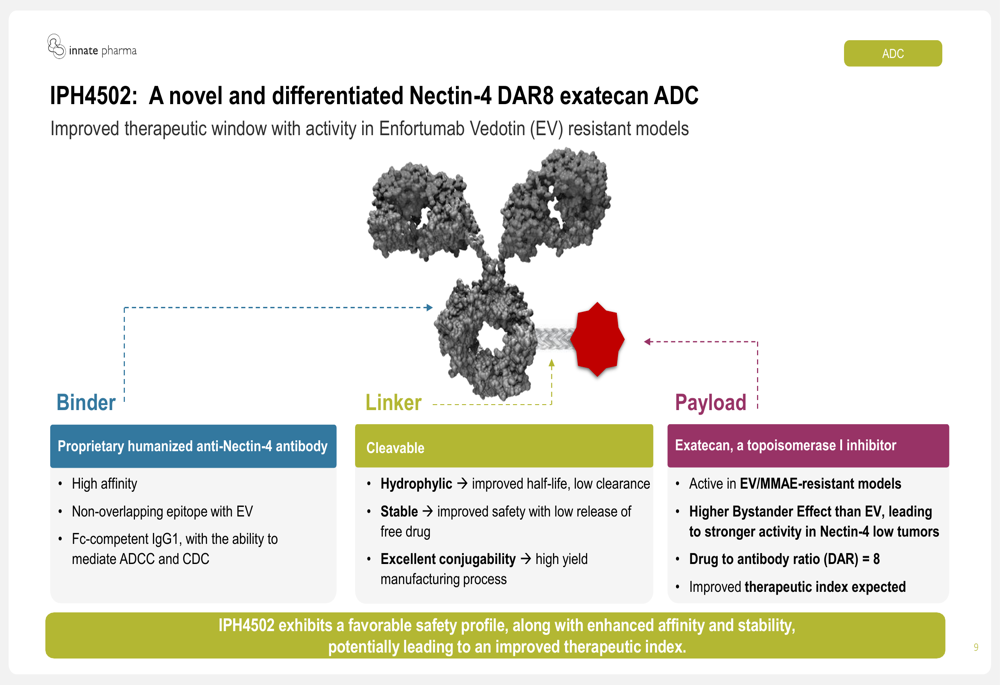

IPH4502, Innate’s novel Nectin-4 antibody-drug conjugate (ADC), represents another key focus area. The company presented preclinical data showing that IPH4502 overcomes resistance to enfortumab vedotin (EV) in urothelial carcinoma models and demonstrates anti-tumor activity across multiple cancer types.

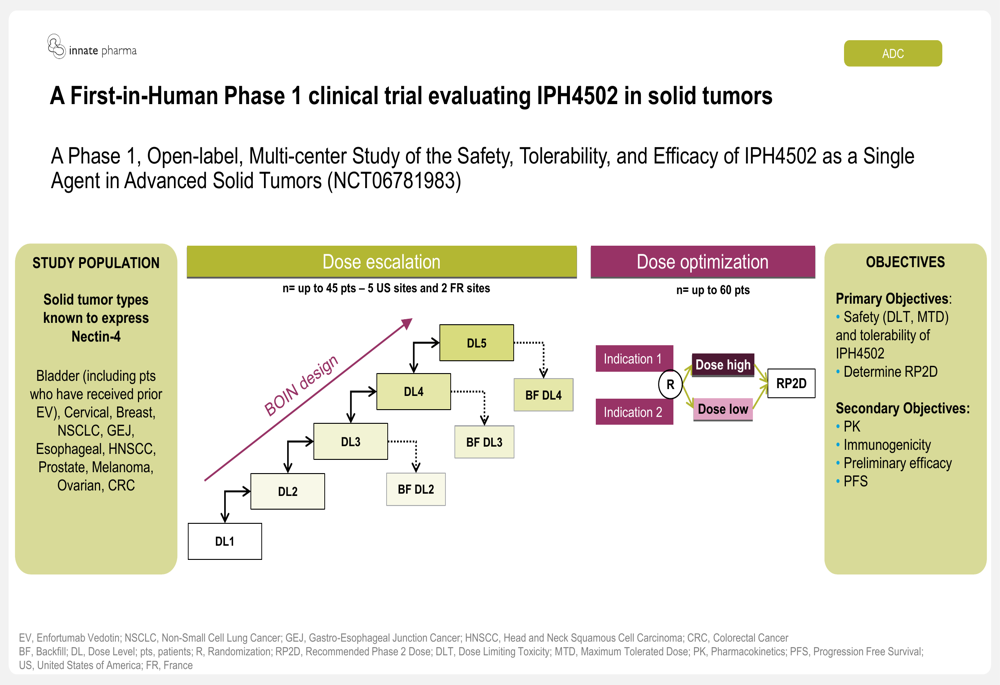

The Phase 1 trial for IPH4502 is currently underway, evaluating its safety, tolerability, and efficacy in advanced solid tumors, with preliminary data expected in 2026. The study includes patients with various Nectin-4 expressing tumors, including bladder cancer patients who have received prior EV treatment.

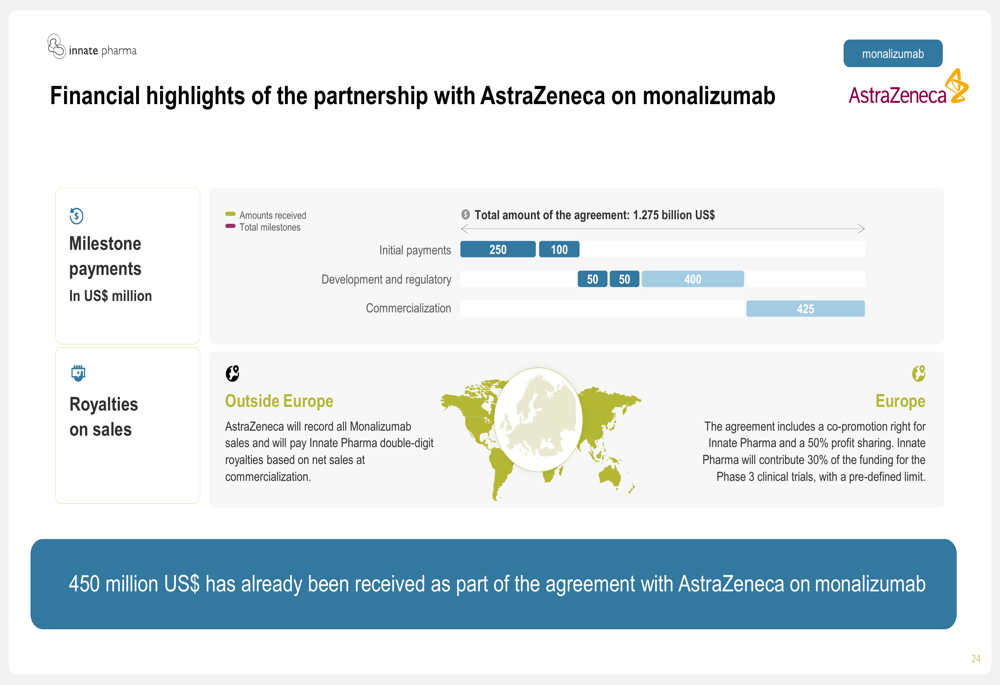

Monalizumab, partnered with AstraZeneca, continues to advance in non-small cell lung cancer (NSCLC). The Phase 3 PACIFIC-9 trial is fully recruited, with high-level readout expected in H2 2026. This program represents a significant potential value driver, with the AstraZeneca partnership worth up to $1.275 billion in total milestones.

Detailed Financial Analysis

For H1 2025, Innate reported revenue and other income of €4.9 million, consisting of €1.7 million from licensing and collaborations and €3.2 million from government funding for research expenditures.

Operating expenses totaled €30.3 million, with R&D expenses of €20.5 million (representing a 29% decrease year-over-year) and G&A expenses of €9.8 million. The reduction in R&D expenses reflects the company’s strategic refocus on its highest-value assets.

The Monalizumab partnership with AstraZeneca continues to be a significant financial asset for Innate. The company has already received €450 million of the potential €1.275 billion total deal value. Future commercialization would generate double-digit royalties on net sales, with Innate retaining co-promotion rights and 50% profit sharing.

Strategic Initiatives

Innate’s strategic path forward centers on three key areas: clinical programs, research, and organizational structure. For clinical programs, the company is investing in its highest-value assets: IPH4502, Lacutamab, and Monalizumab. In research, the focus is on advancing next-generation ADCs toward development. Organizationally, Innate is streamlining to create a fit-for-purpose structure aligned with its strategic objectives.

The company sees significant commercial opportunity for Lacutamab in reshaping CTCL care. With over 6,000 CTCL patients in the US and EU5 and approximately 1,000 Sézary syndrome patients in the US alone, Lacutamab has the potential to address a substantial market need, particularly by enabling earlier systemic therapy in the patient journey.

Forward-Looking Statements

Looking ahead, Innate outlined several key milestones expected over the coming years:

- IPH4502: Completion of Phase 1 enrollment by Q1 2026 and preliminary safety and activity data in 2026

- Lacutamab: Phase 3 trial protocol submission following discussions with health authorities, with trial initiation expected in 2026

- Monalizumab: Phase 3 PACIFIC-9 high-level readout anticipated in H2 2026

The company’s cash runway extends to the end of Q3 2026, providing sufficient funding to reach these important clinical milestones. Management emphasized that the strategic refocus on key assets is designed to maximize value creation while efficiently managing resources.

As Innate Pharma advances its pipeline and executes on its strategic initiatives, investors will be closely watching for clinical data readouts and regulatory interactions that could significantly impact the company’s trajectory. The next earnings report is scheduled for November 19, 2025, where investors can expect further updates on these initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.