SoFi shares rise as record revenue, member growth drive strong Q3 results

Introduction & Market Context

Insight Enterprises (NASDAQ:NSIT) presented its Q2 2025 earnings results on July 31, 2025, revealing a strategic pivot toward artificial intelligence while navigating modest revenue declines. The company’s stock has been trading near its 52-week low of $105.78, with a slight post-earnings decline of 1.59% in aftermarket trading, reflecting mixed investor sentiment about the company’s transformation efforts.

The presentation emphasized Insight’s evolution from a traditional IT provider to what it calls a "solutions integrator," with a particular focus on AI-powered offerings. This strategic shift comes as the company faces headwinds in its traditional business segments, with overall revenue declining by 3% year-over-year.

Quarterly Performance Highlights

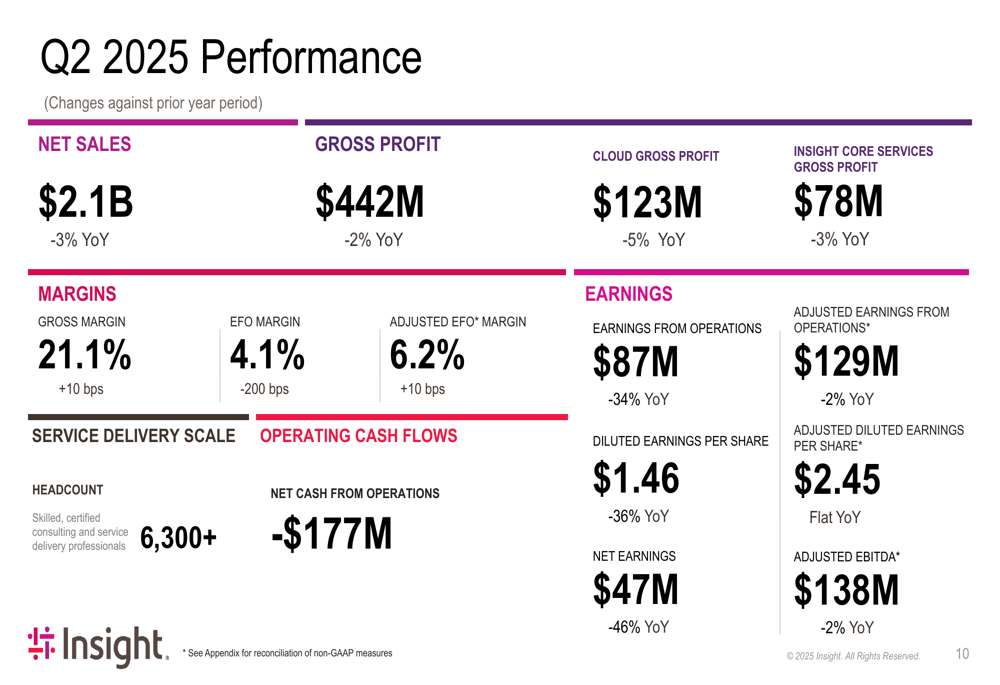

Insight reported Q2 2025 net sales of $2.1 billion, representing a 3% year-over-year decline. Gross profit decreased by 2% to $442 million, though gross margin improved slightly by 10 basis points to 21.1%. The company’s adjusted earnings per share remained flat at $2.45 compared to the same quarter last year.

As shown in the following financial performance summary:

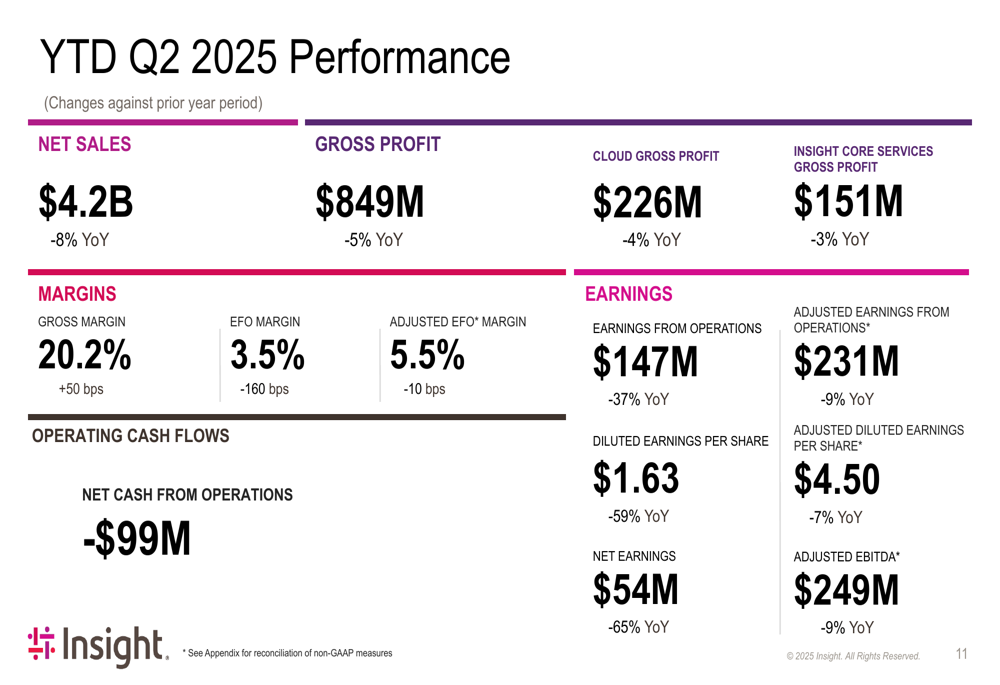

For the first half of 2025, the company’s performance showed more pronounced declines, with net sales down 8% to $4.2 billion and gross profit falling 5% to $849 million compared to the first half of 2024. Year-to-date adjusted diluted earnings per share decreased by 7% to $4.50.

The services segment, which is central to Insight’s strategic transformation, showed more resilience than the overall business. Services net sales declined by just 2% year-over-year to $426 million in Q2, while maintaining strong gross margins. The company highlighted its "Insight Core Services" as a key focus area, though this segment also experienced a 3% decline in gross profit.

Strategic Initiatives

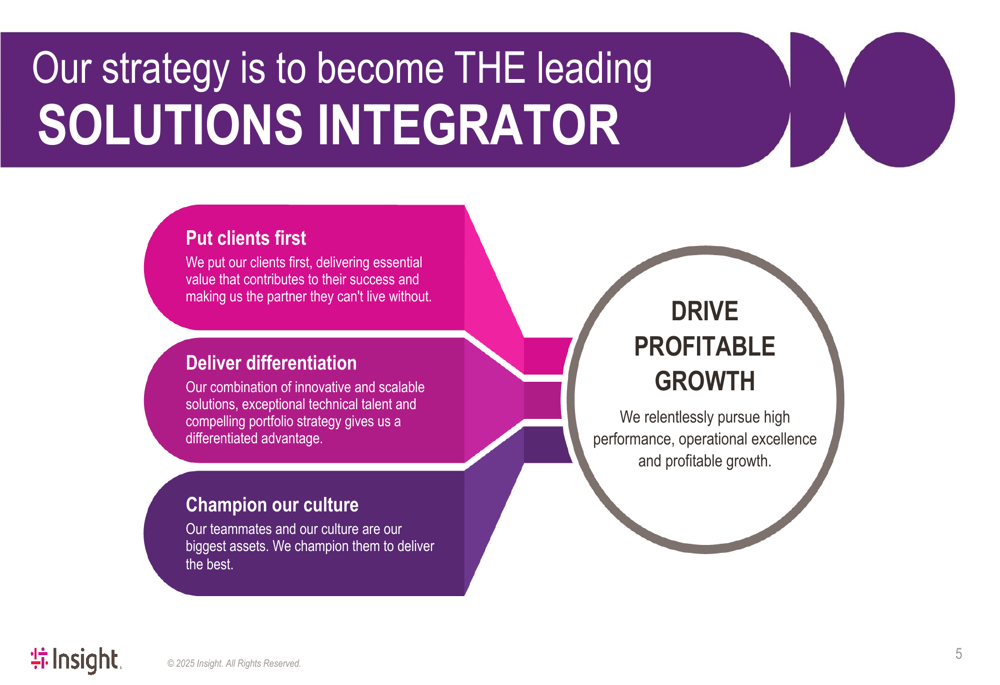

Insight’s presentation emphasized its transformation into a "solutions integrator" rather than a traditional reseller or systems integrator. The company outlined four strategic pillars driving this evolution:

These strategic pillars are further elaborated to show how they interconnect to drive profitable growth:

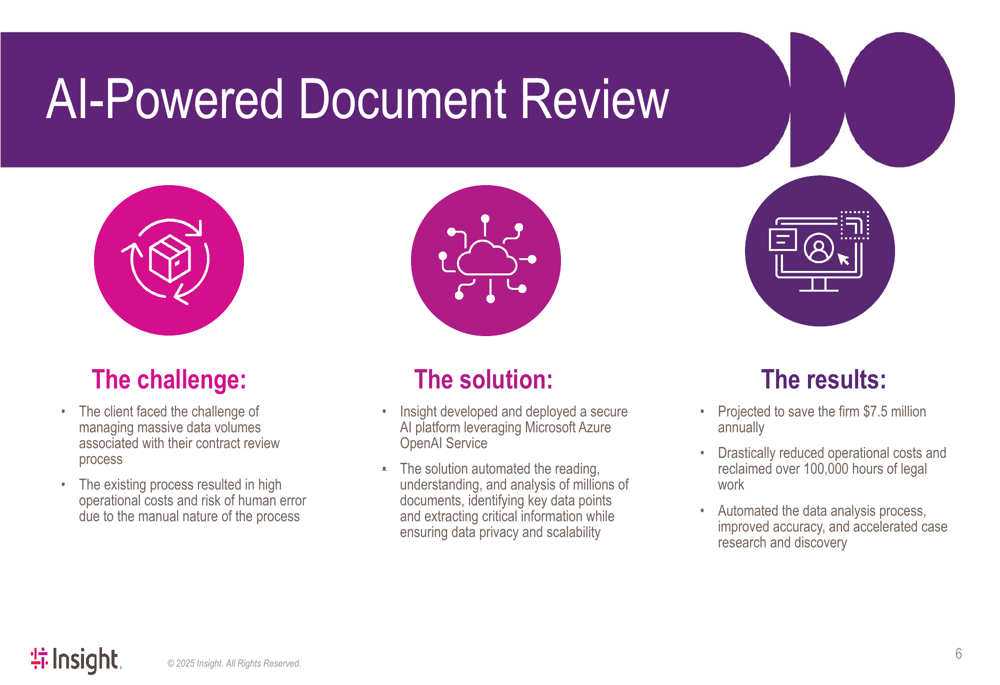

The company showcased its AI capabilities through case studies, including an AI-powered document review solution that reportedly saved a client $7.5 million annually and reclaimed over 100,000 hours of legal work. This example illustrates Insight’s focus on developing practical AI applications that deliver measurable business outcomes.

During the earnings call, CEO Joyce Mullen emphasized this strategic direction, stating, "We are adapting our ambition to becoming not only the leading solutions integrator but the leading AI-first solutions integrator." The presentation materials reflect this commitment with multiple AI-focused case studies and implementation examples.

Competitive Industry Position

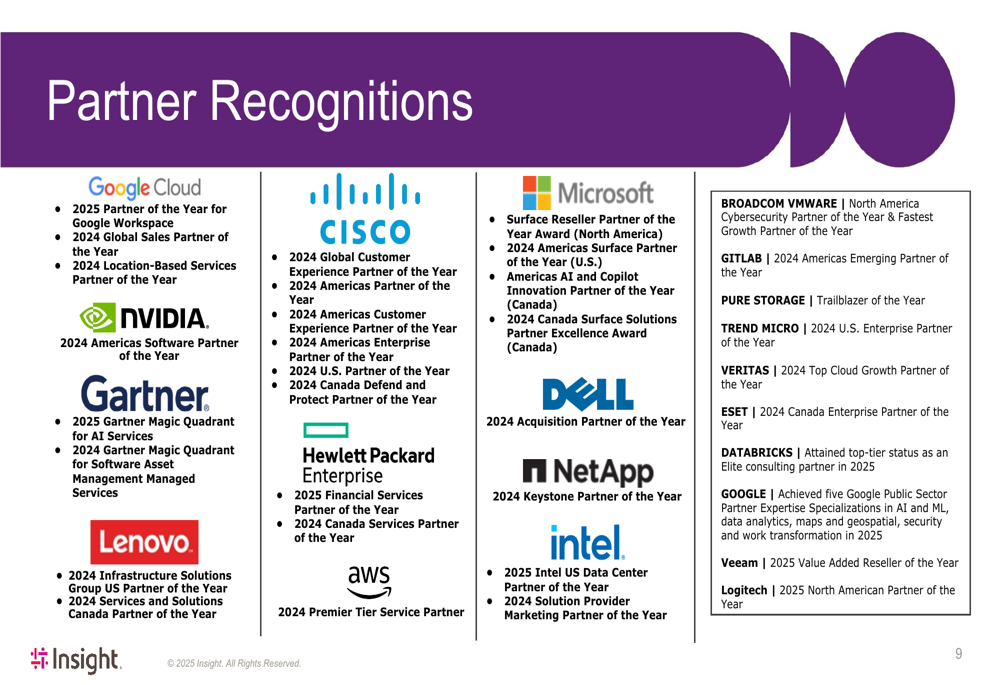

Despite financial headwinds, Insight highlighted its strong industry position through numerous awards and recognitions. The company was included in the Fortune 500 (No. 447) and ranked No. 37 in IT on Forbes’ 2024 World’s Best Employers list, among other employer accolades:

The company also showcased its strong technology partnerships, featuring recognitions from major vendors including Google Cloud, Cisco, Microsoft, Dell, and others:

These partnerships and recognitions serve to validate Insight’s market position and technical capabilities, particularly as it pivots toward more advanced AI and cloud solutions. They also suggest that despite current financial challenges, the company maintains strong relationships with key technology providers.

Forward-Looking Statements

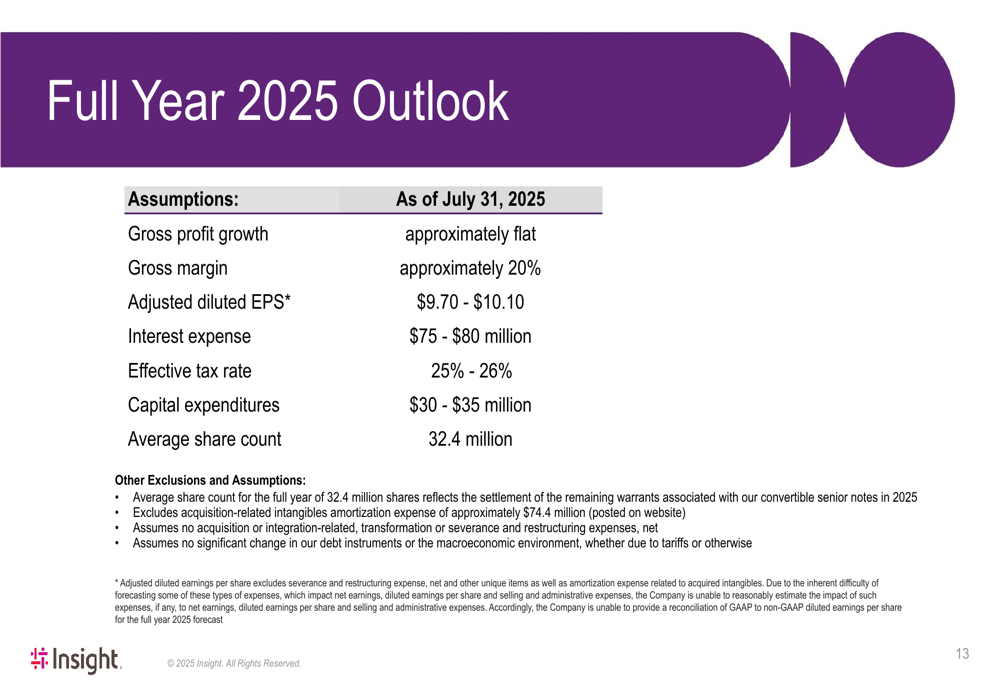

For the full year 2025, Insight provided guidance projecting approximately flat gross profit growth and gross margin of around 20%. The company expects adjusted diluted earnings per share to range between $9.70 and $10.10.

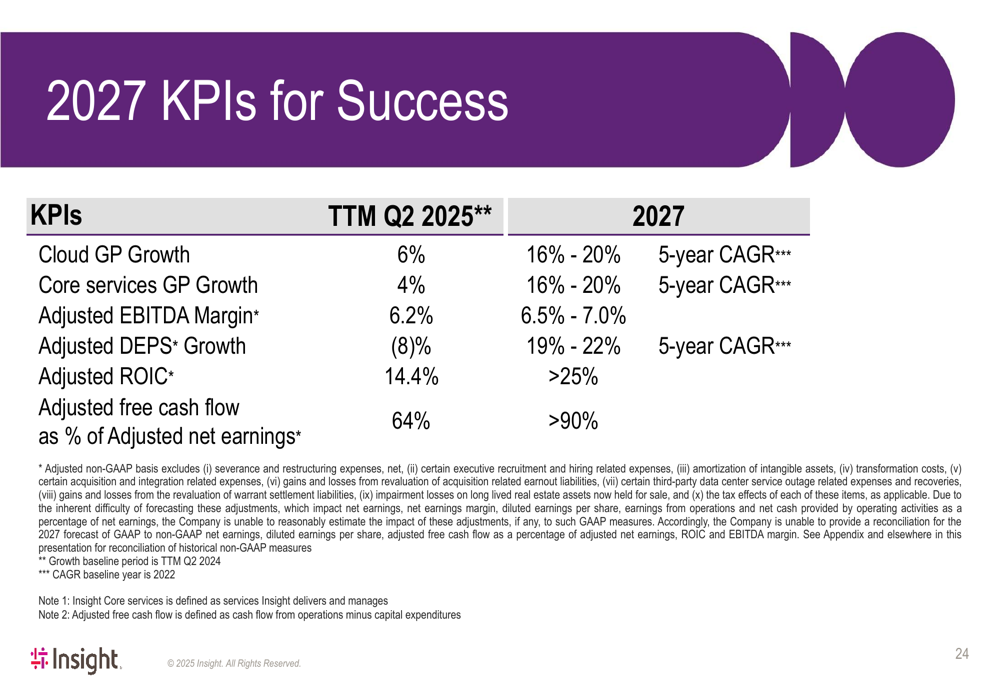

Looking further ahead, Insight outlined ambitious targets for 2027, including:

- Cloud gross profit growth of 16-20% (5-year CAGR)

- Core services gross profit growth of 16-20% (5-year CAGR)

- Adjusted EBITDA margin improvement to 6.5-7.0%

- Adjusted diluted EPS growth of 19-22% (5-year CAGR)

These targets represent a significant acceleration from current performance levels, where cloud gross profit declined by 5% and core services gross profit declined by 3% in the most recent quarter.

Detailed Financial Analysis

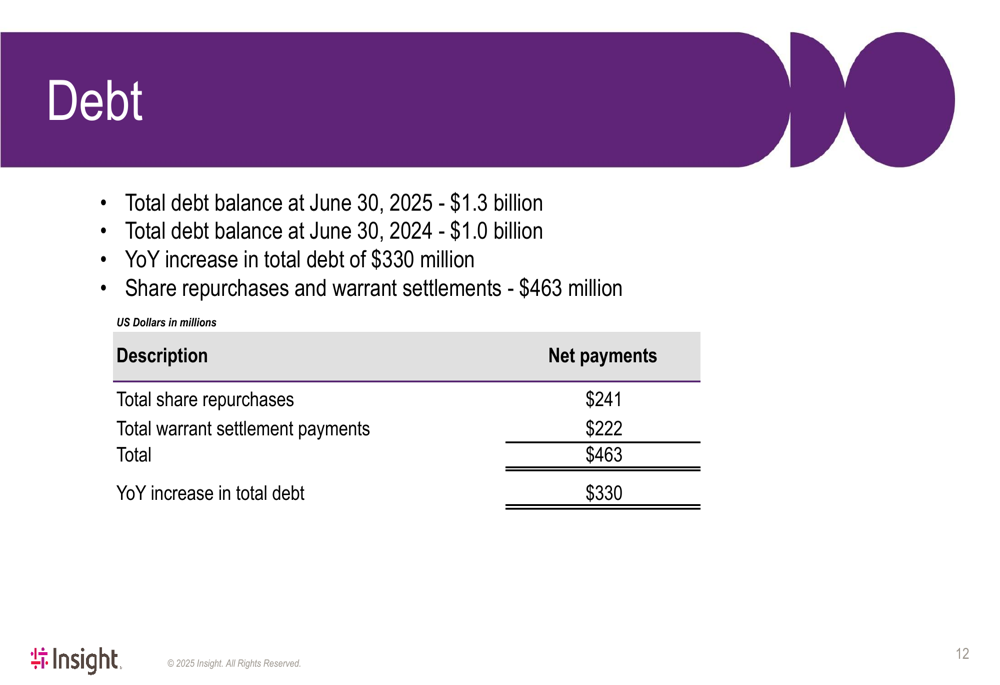

The company’s debt position increased year-over-year, with total debt rising by $330 million to $1.3 billion as of June 30, 2025. This increase was primarily driven by share repurchases and warrant settlements totaling $463 million.

Cash flow from operations was negative at -$99 million year-to-date, which could present challenges if the trend continues. However, the company maintains that it has sufficient liquidity to execute its strategic initiatives while continuing to return capital to shareholders.

The presentation included detailed reconciliations between GAAP and non-GAAP measures, highlighting significant differences between reported and adjusted figures. For Q2 2025, GAAP earnings from operations were $87 million (down 34% year-over-year), while adjusted earnings from operations were $129 million (down just 2%). Similarly, GAAP diluted EPS was $1.46 (down 36%), compared to adjusted diluted EPS of $2.45 (flat).

These discrepancies between GAAP and non-GAAP figures were primarily attributed to restructuring expenses, acquisition-related costs, and amortization of intangible assets, suggesting that the company continues to undergo significant organizational changes as part of its strategic transformation.

In conclusion, Insight’s Q2 2025 presentation reveals a company in transition, facing near-term revenue challenges while positioning itself for future growth through AI-powered solutions. The ambitious 2027 targets indicate management’s confidence in this strategic direction, though investors appear to be taking a cautious approach as reflected in the company’s stock performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.