BigBear.ai appoints Sean Ricker as chief financial officer

Introduction & Market Context

Insmed Incorporated (NASDAQ:INSM) presented its first-quarter 2025 earnings results on May 8, highlighting continued strong growth for its flagship product ARIKAYCE while preparing for potential approval of its pipeline candidate brensocatib. The company’s stock was trading at $67 in pre-market, down 1.87% following the presentation, according to available market data.

The biopharmaceutical company, which focuses on rare diseases and serious unmet medical needs, maintained its position of strength in the treatment of refractory Mycobacterium avium complex (MAC) lung disease while advancing multiple mid- to late-stage clinical programs.

Quarterly Performance Highlights

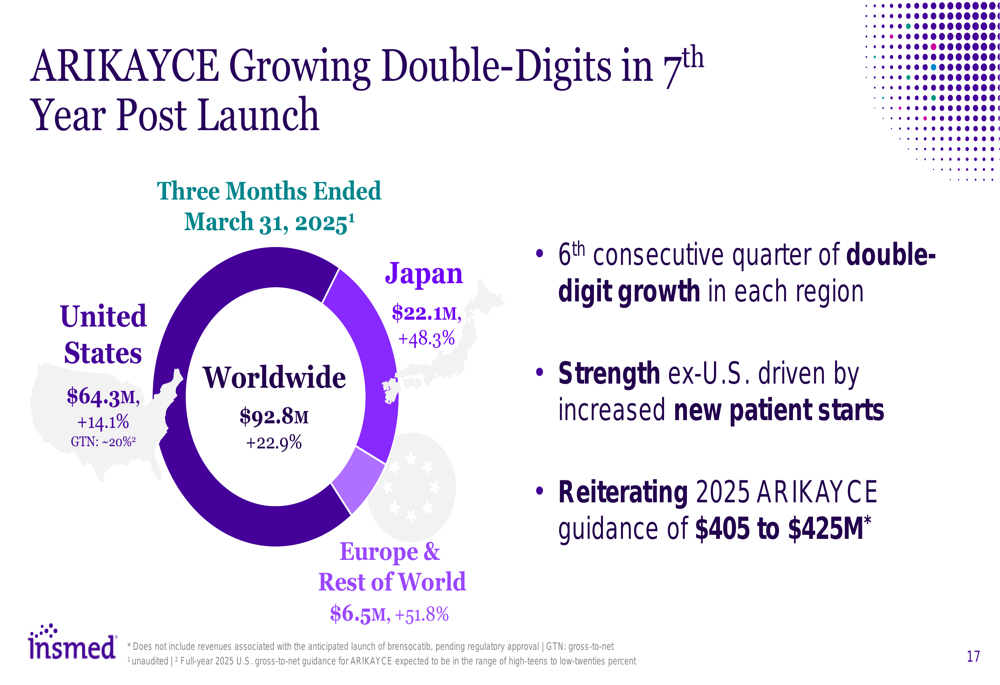

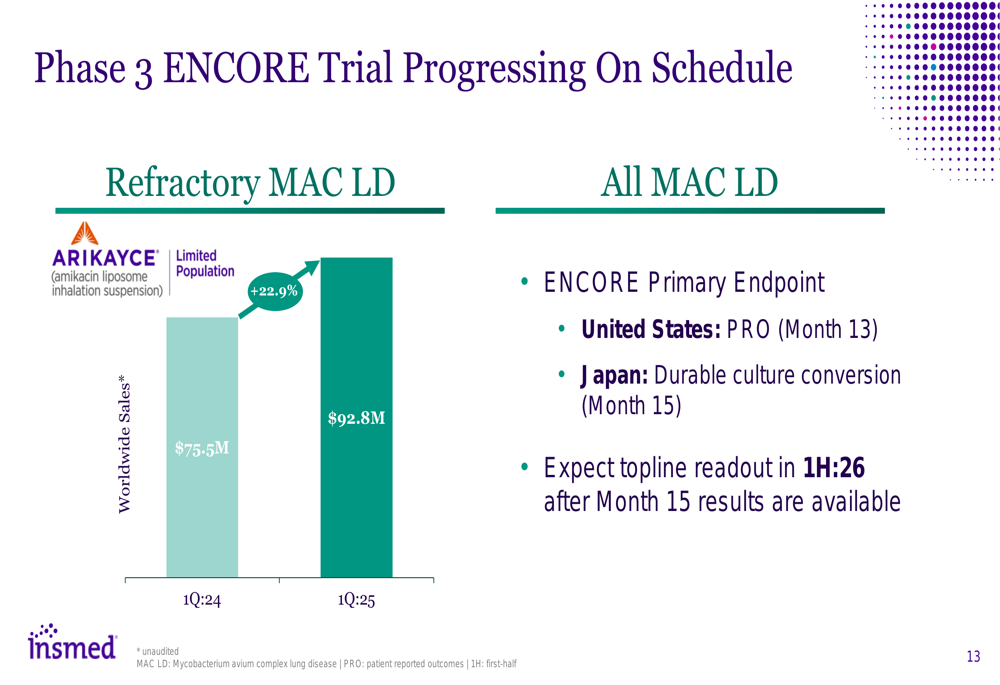

Insmed reported worldwide ARIKAYCE sales of $92.8 million for Q1 2025, representing a 22.9% increase compared to the same period last year. This marks the sixth consecutive quarter of double-digit growth across all regions, demonstrating sustained commercial momentum for the product in its seventh year post-launch.

As shown in the following chart of quarterly revenue performance:

The United States remained the largest market with sales of $64.3 million, up 14.1% year-over-year. However, the most impressive growth came from international markets, with Japan surging 48.3% to $22.1 million and Europe & Rest of World increasing 51.8% to $6.5 million. The company attributed the strength outside the U.S. to increased new patient starts.

Based on this performance, Insmed reiterated its 2025 ARIKAYCE revenue guidance of $405 million to $425 million, suggesting continued confidence in the product’s growth trajectory.

Pipeline and Development Updates

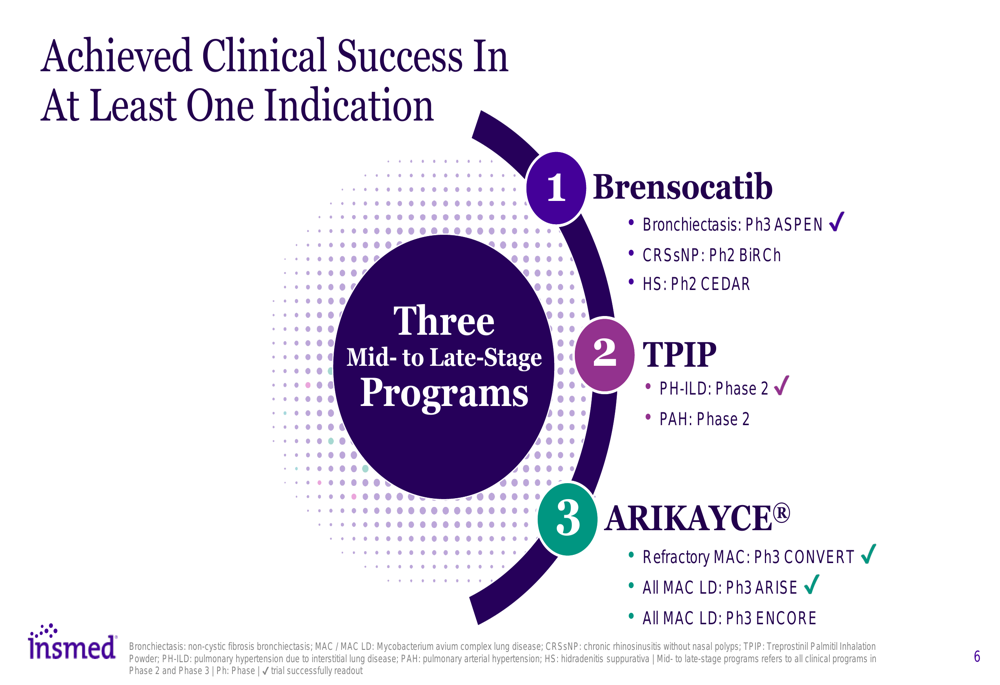

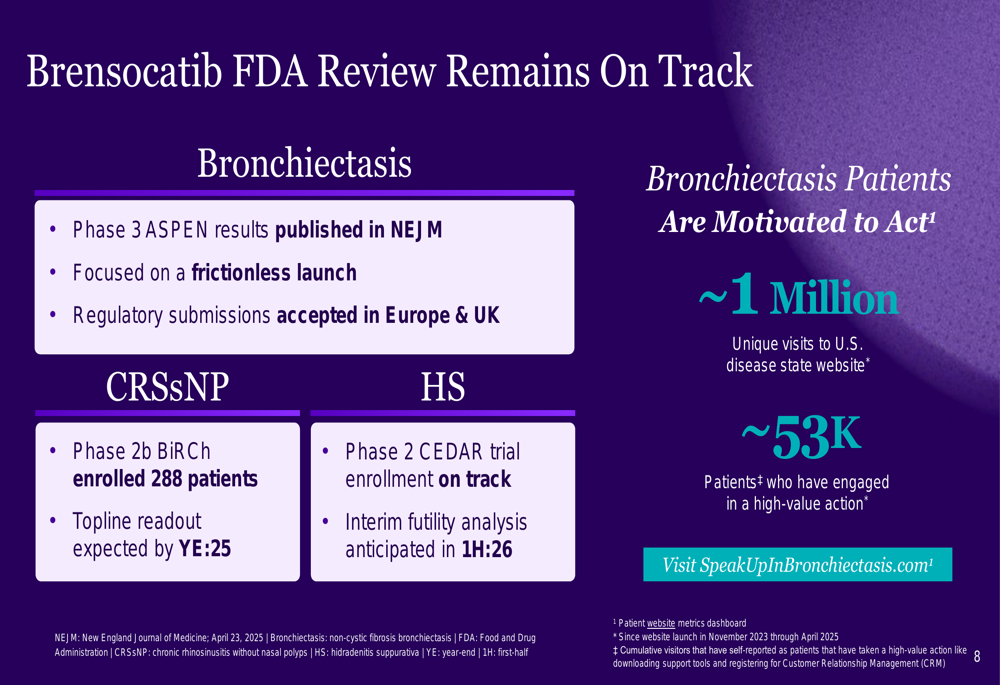

The company highlighted significant progress across its development pipeline, with particular focus on brensocatib, which is currently under FDA review for bronchiectasis with a PDUFA target action date of August 12, 2025.

The following slide illustrates Insmed’s three mid- to late-stage programs and their respective indications:

For brensocatib, Insmed reported that the Phase 3 ASPEN trial results were published in the New England Journal of Medicine, and regulatory submissions have been accepted in Europe and the UK. The company is focused on preparing for a "frictionless launch" pending approval.

The company also provided an update on patient engagement, noting approximately 1 million unique visits to its U.S. disease state website since November 2023, with 53,000 patients engaging in high-value actions, suggesting strong market interest ahead of potential approval.

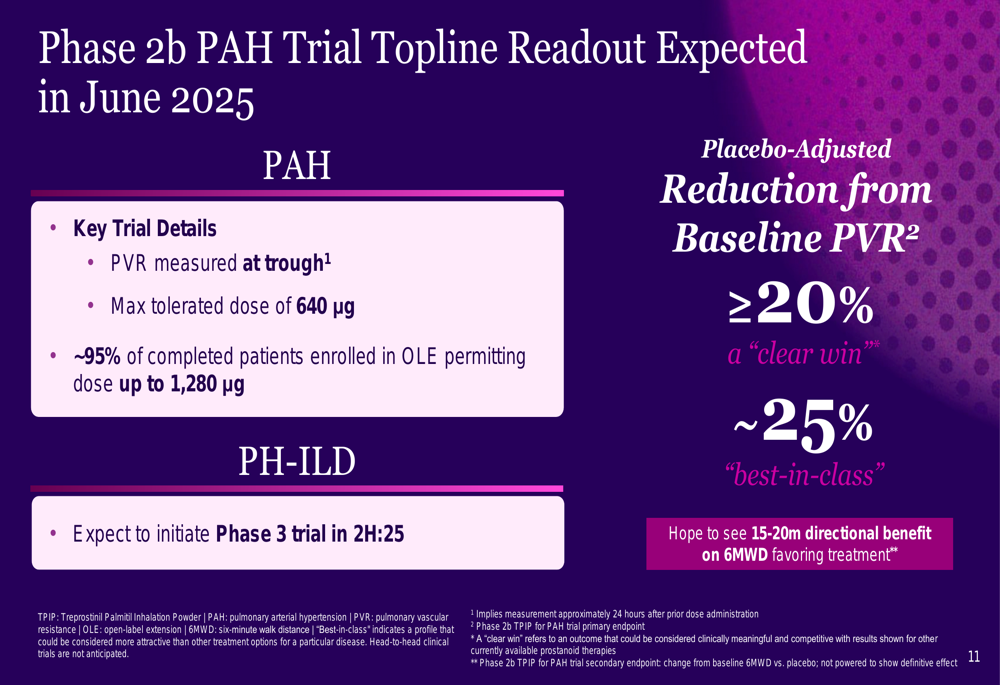

For TPIP (treprostinil palmitil inhalation powder), Insmed expects a topline readout from its Phase 2b pulmonary arterial hypertension (PAH) trial in June 2025. The company is targeting a placebo-adjusted reduction from baseline pulmonary vascular resistance (PVR) of at least 20%, which they consider a "clear win," with hopes of achieving approximately 25%, which would position the therapy as "best-in-class."

The Phase 3 ENCORE trial for ARIKAYCE in all MAC lung disease patients is progressing on schedule, with topline readout expected in the first half of 2026 after month 15 results become available.

Financial Analysis

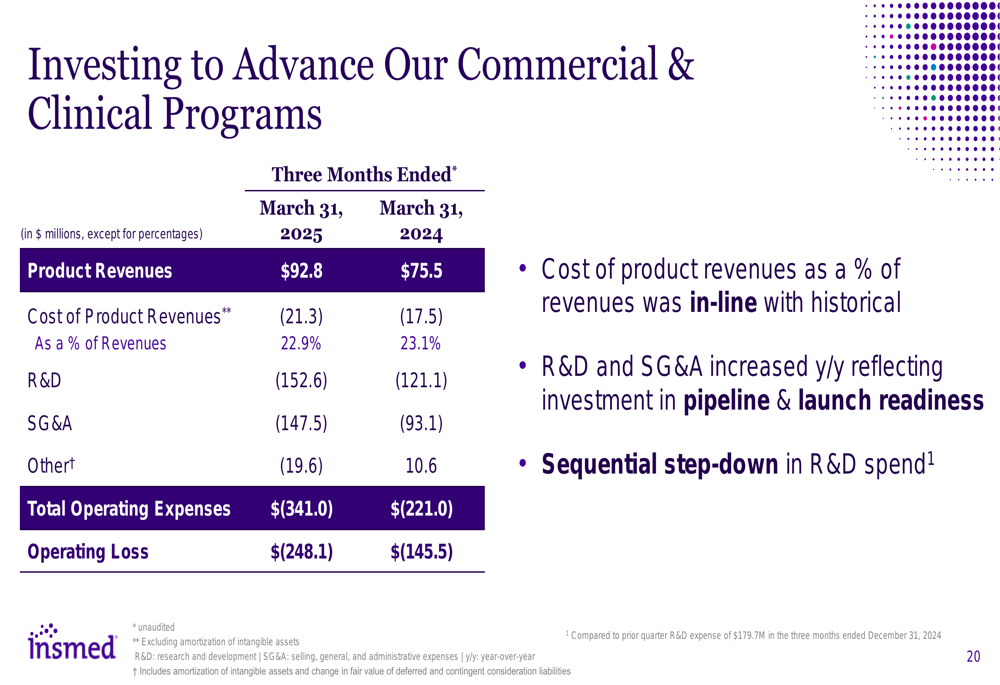

Despite strong revenue growth, Insmed reported increased operating expenses as it invests in its pipeline and prepares for potential commercial launches. For the three months ended March 31, 2025, the company reported:

Total (EPA:TTEF) operating expenses increased to $341.0 million from $221.0 million in Q1 2024, resulting in an operating loss of $248.1 million compared to $145.5 million in the prior-year period. Research and development expenses rose to $152.6 million from $121.1 million, while selling, general and administrative expenses increased to $147.5 million from $93.1 million, reflecting investments in pipeline development and launch readiness.

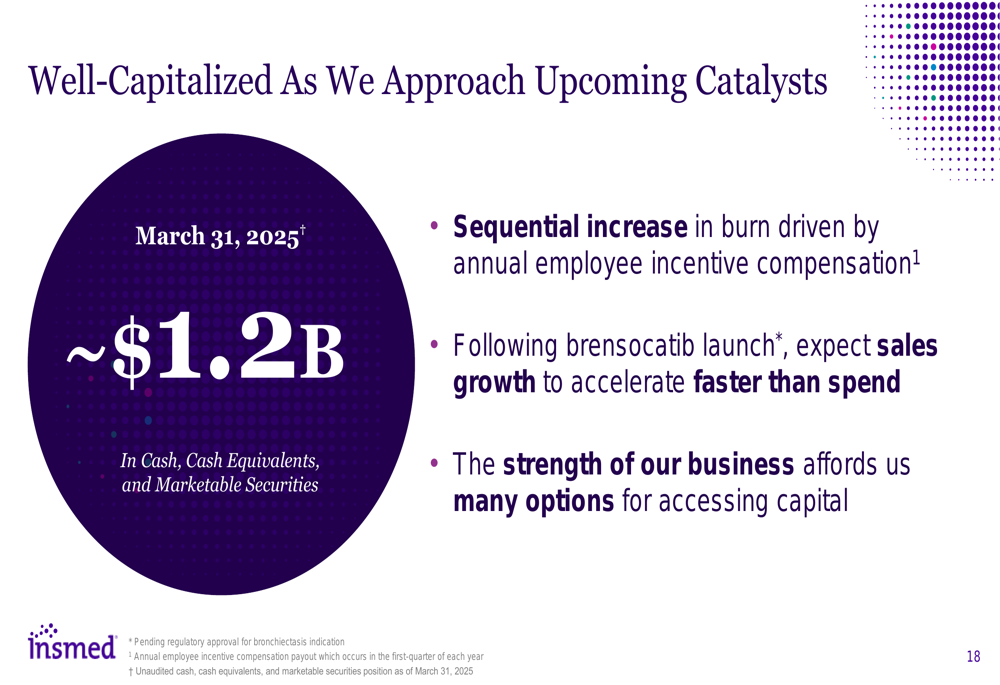

The company maintained a strong financial position with approximately $1.2 billion in cash, cash equivalents, and marketable securities as of March 31, 2025. This represents a decrease from the $1.4 billion reported at the end of Q4 2024, reflecting ongoing investments in clinical programs and commercial infrastructure.

Insmed also announced it has called the remaining convertible debt with a principal amount of approximately $570 million, representing approximately 17.8 million underlying shares if all notes are converted. The company expects this move to lower ongoing interest expense and reduce outstanding debt.

Forward-Looking Statements

Looking ahead, Insmed emphasized several key catalysts that could drive future growth:

1. Potential U.S. approval and launch of brensocatib for bronchiectasis in Q3 2025

2. TPIP Phase 2b PAH trial topline results expected in June 2025

3. Initiation of TPIP Phase 3 trial in PH-ILD in the second half of 2025

4. Continued enrollment in the Phase 2b BiRCh trial for brensocatib in chronic rhinosinusitis with nasal polyps (CRSSNP) with topline readout expected by year-end 2025

5. Ongoing Phase 2 CEDAR trial for brensocatib in hidradenitis suppurativa (HS) with interim futility analysis anticipated in the first half of 2026

The company is also working to minimize potential tariff exposure by expanding its U.S. manufacturing footprint, including establishing brensocatib secondary source manufacturing in the United States. Management anticipates a single-digit million dollar annual impact based on tariffs currently in place.

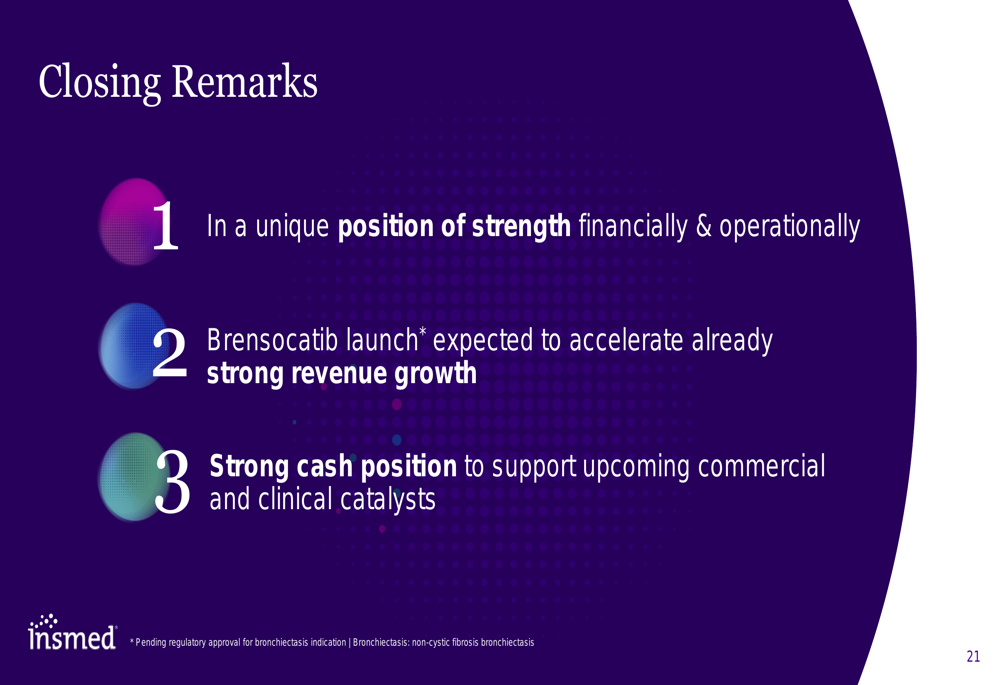

CEO Will Lewis (JO:LEWJ) emphasized the company’s unique position of strength, both financially and operationally, and expressed confidence that the brensocatib launch would accelerate already strong revenue growth. CFO Sara Bonstein highlighted that the company’s financial strength "affords us many options for accessing capital" as they approach these upcoming catalysts.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.