Street Calls of the Week

Introduction & Market Context

Insmed Incorporated (NASDAQ:INSM) presented its second-quarter 2025 earnings results on August 7, showing continued revenue growth for its flagship product ARIKAYCE, while highlighting advancements across its clinical pipeline. Despite the positive developments, the stock traded down 4.37% in premarket to $106.40, reflecting investor concerns about the company’s widening operating losses.

The biopharmaceutical company, which focuses on rare diseases and serious unmet medical needs, emphasized its "three for three" success with late-stage assets demonstrating clinical success, while maintaining a strong cash position of approximately $1.9 billion to fund future growth initiatives.

Quarterly Performance Highlights

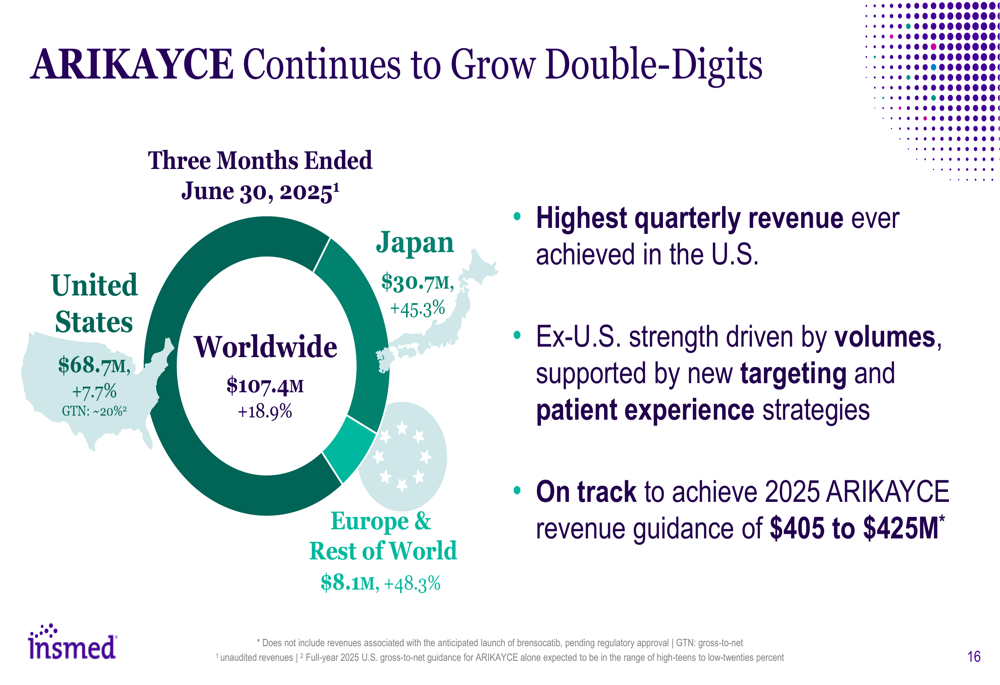

Insmed reported worldwide ARIKAYCE revenue of $107.4 million for Q2 2025, representing an 18.9% increase compared to the same period last year. The company achieved its highest quarterly revenue ever in the U.S. market at $68.7 million, a 7.7% year-over-year increase.

International markets showed particularly impressive growth, with Japan revenue surging 45.3% to $30.7 million and Europe & Rest of World climbing 48.3% to $8.1 million. Management attributed the strong ex-U.S. performance to new targeting and patient experience strategies.

As shown in the following revenue breakdown:

The company remains on track to achieve its 2025 ARIKAYCE revenue guidance of $405 to $425 million, demonstrating confidence in continued growth despite increasing competition in the respiratory space.

Pipeline and Clinical Developments

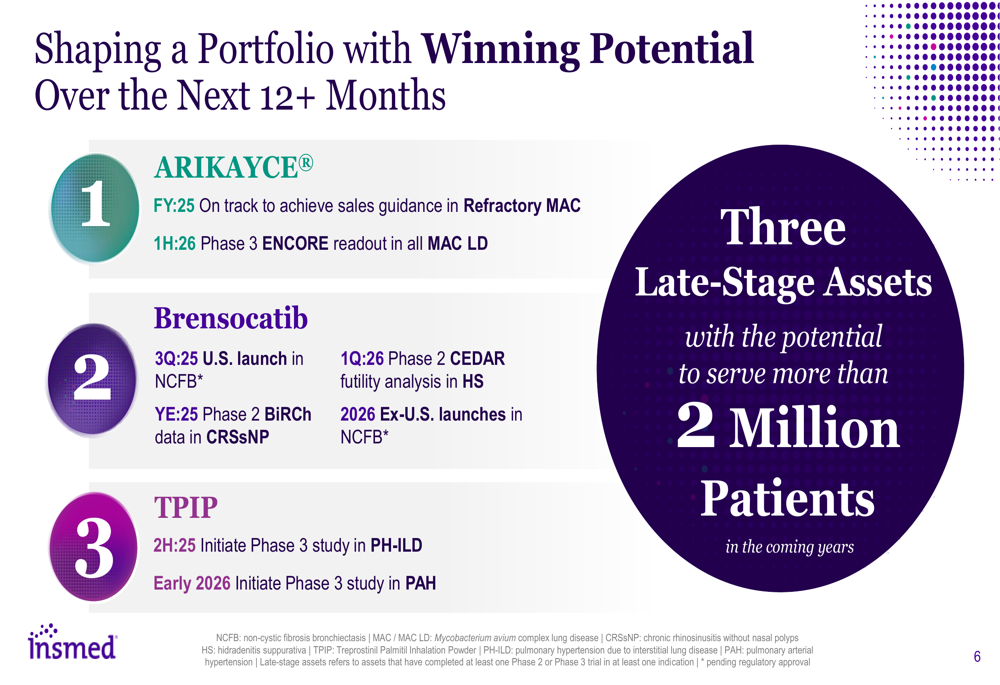

Insmed highlighted significant progress across its late-stage pipeline, with particular emphasis on brensocatib and TPIP (Treprostinil Palmitil Inhalation Powder).

The company is preparing for the U.S. launch of brensocatib for non-cystic fibrosis bronchiectasis (NCFB) in Q3 2025, with Chief Operating Officer Roger Adsett noting that approximately 90% of surveyed physicians intend to prescribe the drug to patients with two or more pulmonary exacerbations. The company has already trained and deployed an expanded salesforce more than 10 months ahead of approval.

The following slide outlines Insmed’s portfolio and key milestones for the next 12+ months:

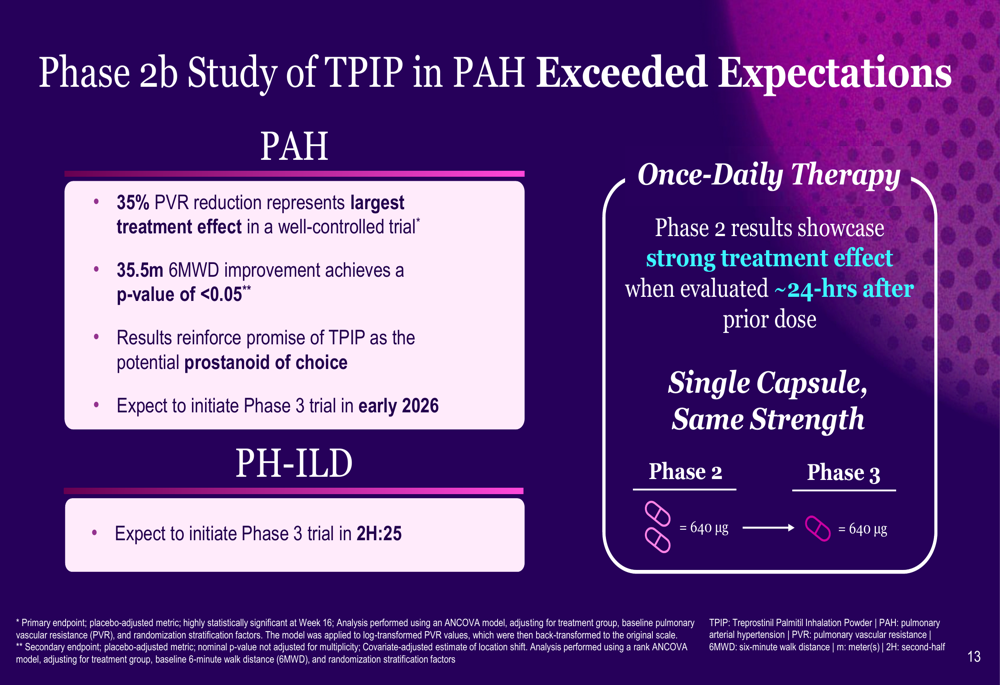

Perhaps the most impressive clinical update came from the Phase 2b study of TPIP in pulmonary arterial hypertension (PAH), which showed a 35% reduction in pulmonary vascular resistance (PVR) and a 35.5-meter improvement in 6-minute walk distance (6MWD). Management characterized these results as "the largest treatment effect in a well-controlled trial" for PAH.

The TPIP clinical results are detailed in this slide:

Based on these positive results, Insmed plans to initiate a Phase 3 study for TPIP in pulmonary hypertension associated with interstitial lung disease (PH-ILD) in the second half of 2025, followed by a Phase 3 study in PAH in early 2026.

Financial Position and Outlook

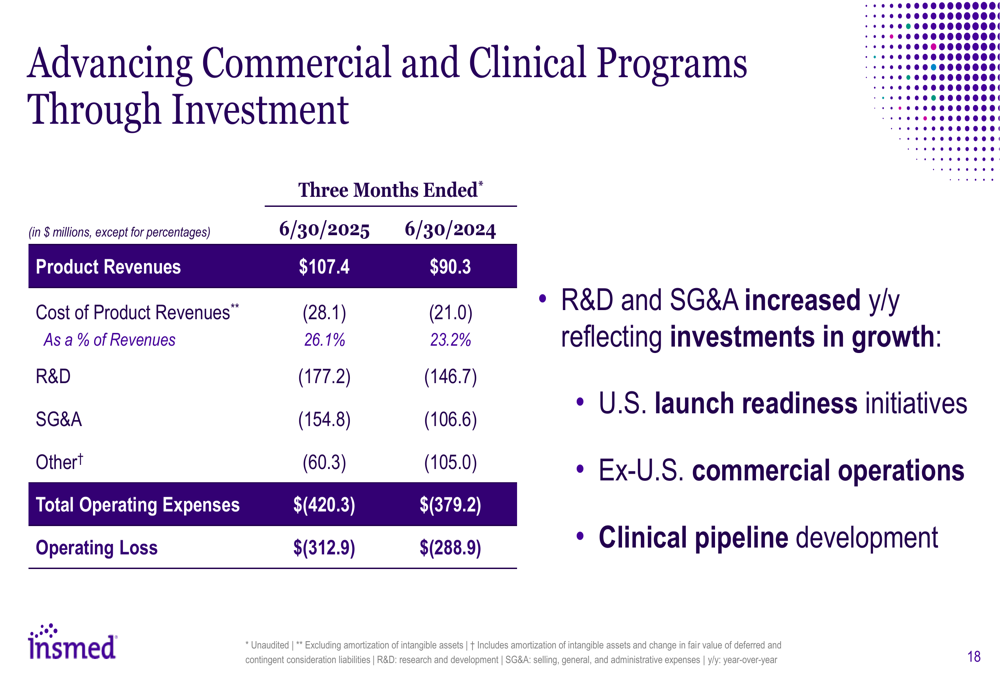

While revenue growth remained strong, Insmed’s operating expenses increased significantly year-over-year. R&D expenses rose to $177.2 million in Q2 2025 compared to $146.7 million in Q2 2024, while SG&A expenses jumped to $154.8 million from $106.6 million in the prior-year period.

These increased investments resulted in a widened operating loss of $312.9 million for Q2 2025, compared to $288.9 million in Q2 2024, as shown in the following financial summary:

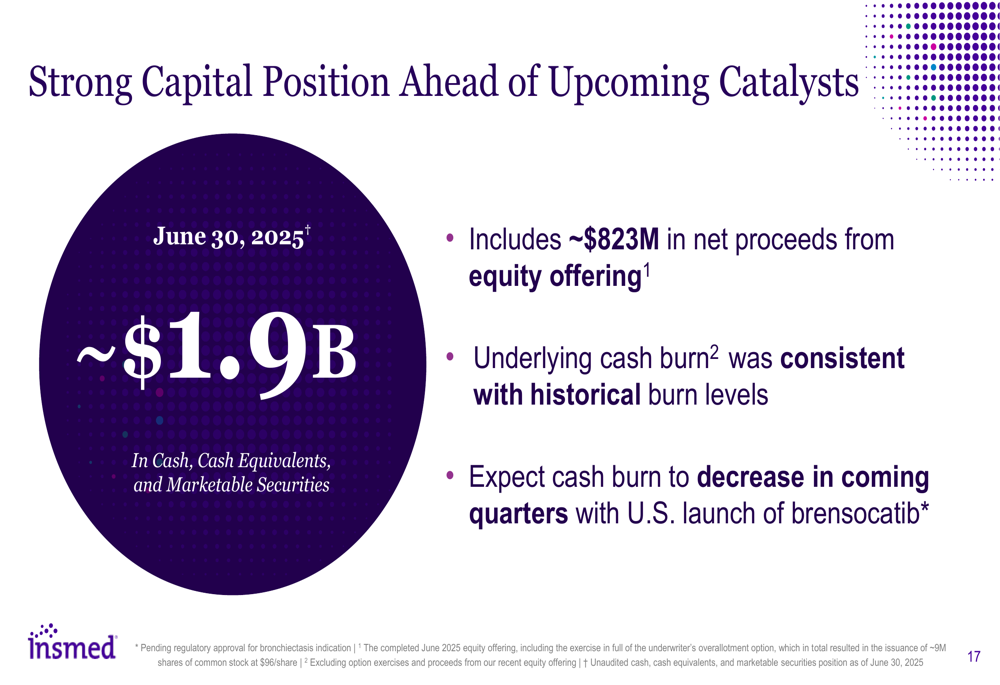

Despite the increased spending, Insmed maintains a robust capital position with approximately $1.9 billion in cash, cash equivalents, and marketable securities as of June 30, 2025. This includes approximately $823 million in net proceeds from a recent equity offering.

The company’s financial position is illustrated in this slide:

Management emphasized that cash burn is expected to decrease in coming quarters with the U.S. launch of brensocatib, which should begin generating revenue to offset some of the ongoing development costs.

Market Reaction and Analyst Perspectives

The 4.37% premarket decline in Insmed’s stock price suggests investors may be concerned about the company’s widening losses despite revenue growth. This reaction follows a pattern seen after Q1 results, when the stock fell 0.82% after reporting an EPS miss of -$1.42 versus the forecast of -$1.35.

The market appears to be weighing Insmed’s promising clinical developments and revenue growth against its significant cash burn and increased operating expenses. While the company’s $1.9 billion cash position provides substantial runway, investors may be looking for clearer signals about the path to profitability.

In closing remarks, management highlighted that the next 12+ months will bring multiple commercial, clinical, and regulatory milestones with the potential to drive value, while maintaining a commitment to "thoughtfully deploying capital to maximize opportunities for patients."

With Insmed’s stock trading between its 52-week range of $60.40 and $113.10, and now at $106.40 in premarket trading, investors will be closely watching the upcoming brensocatib launch and further clinical developments to assess whether the company can translate its promising pipeline into sustainable financial performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.