Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

Instabank ASA (OB:INSTA) reported its second quarter 2025 results on August 15, highlighting record-high lending growth and continued profitability despite increased expenses related to strategic initiatives. The Nordic challenger bank, founded in 2016, has been expanding its product offerings and geographical footprint as it transitions from a specialized consumer finance bank to a diversified commercial banking operation.

Shares of Instabank were trading at 2.93 NOK as of August 14, up 2.09% and near the 52-week high of 2.94 NOK, suggesting positive market reception of the company’s growth trajectory and strategic direction.

Quarterly Performance Highlights

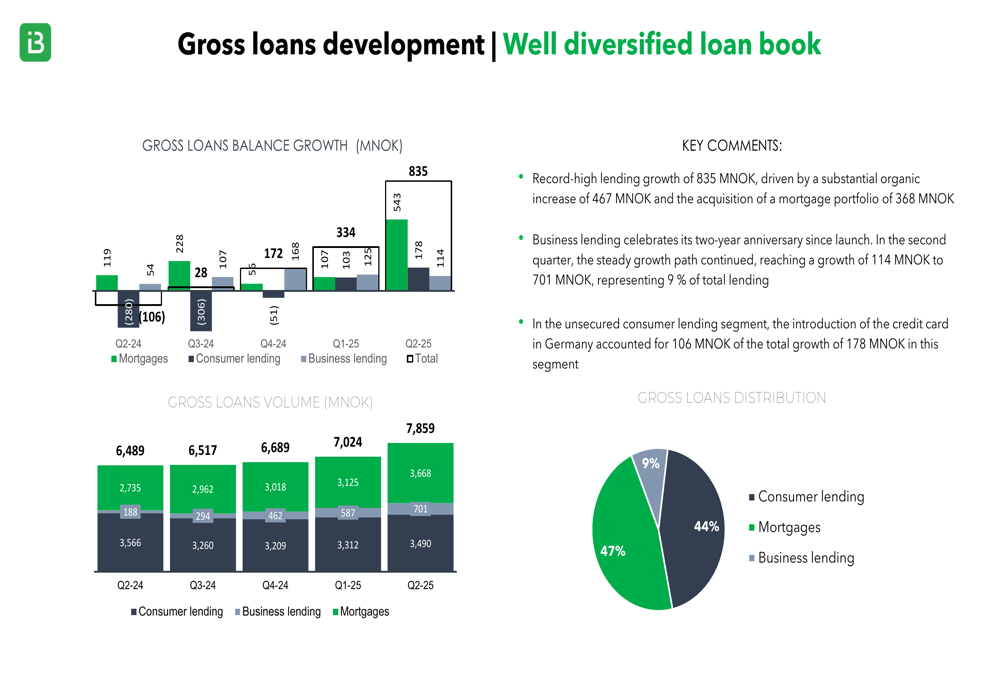

Instabank achieved record-high growth in gross lending of 835 MNOK during Q2 2025, driven by strong organic growth of 467 MNOK and a mortgage portfolio acquisition of 368 MNOK. The company also successfully launched its credit card offering in Germany, marking a significant step in its European expansion strategy.

Profit before tax reached 28.9 MNOK, with an adjusted figure of 36.7 MNOK when excluding extraordinary events related to strategic growth investments. These extraordinary expenses included higher-than-usual loss provisions due to IFRS 9 provisioning in Germany and significant investments in external advisory and legal fees for the Finnish banking license application process.

As shown in the following chart of gross loans development and diversification:

The company’s loan portfolio has become increasingly diversified, with mortgages now representing 47% of gross loans, consumer lending at 44%, and business lending at 9%. Notably, the business lending segment, which celebrated its two-year anniversary, has proven to be Instabank’s most profitable segment, contributing 21% of operating profit while representing only 9% of the loan portfolio.

Detailed Financial Analysis

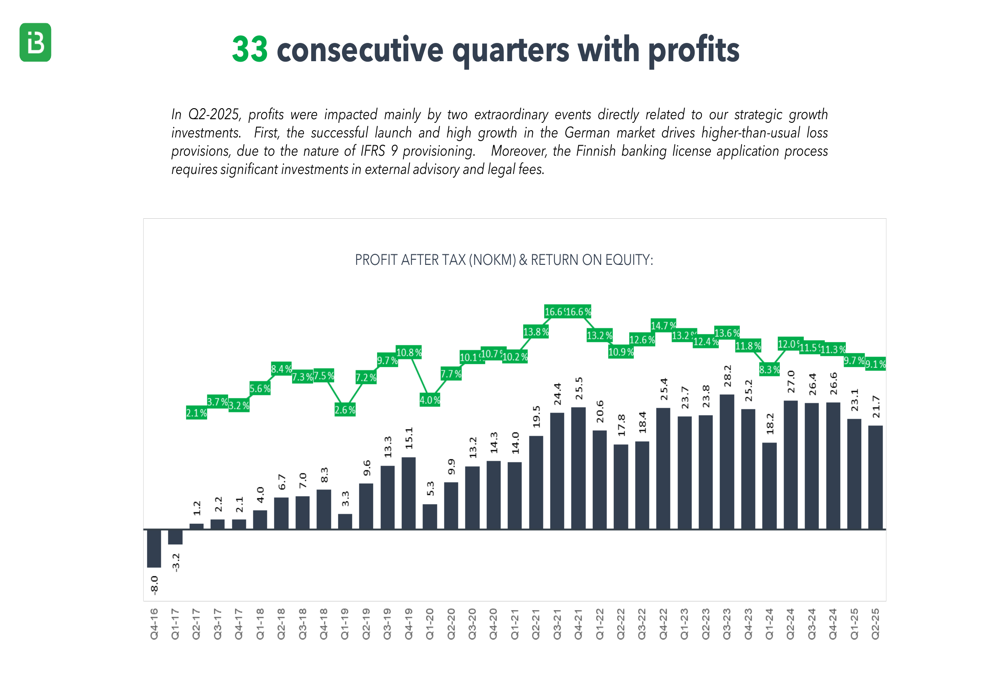

Instabank reported its 33rd consecutive quarter of profitability, demonstrating remarkable consistency despite fluctuations in the economic environment. The company’s total income grew by 9.6 MNOK from the previous quarter to 144.1 MNOK, while total interest income increased by 15.1 MNOK to 202.3 MNOK.

The following chart illustrates the company’s consistent profitability track record:

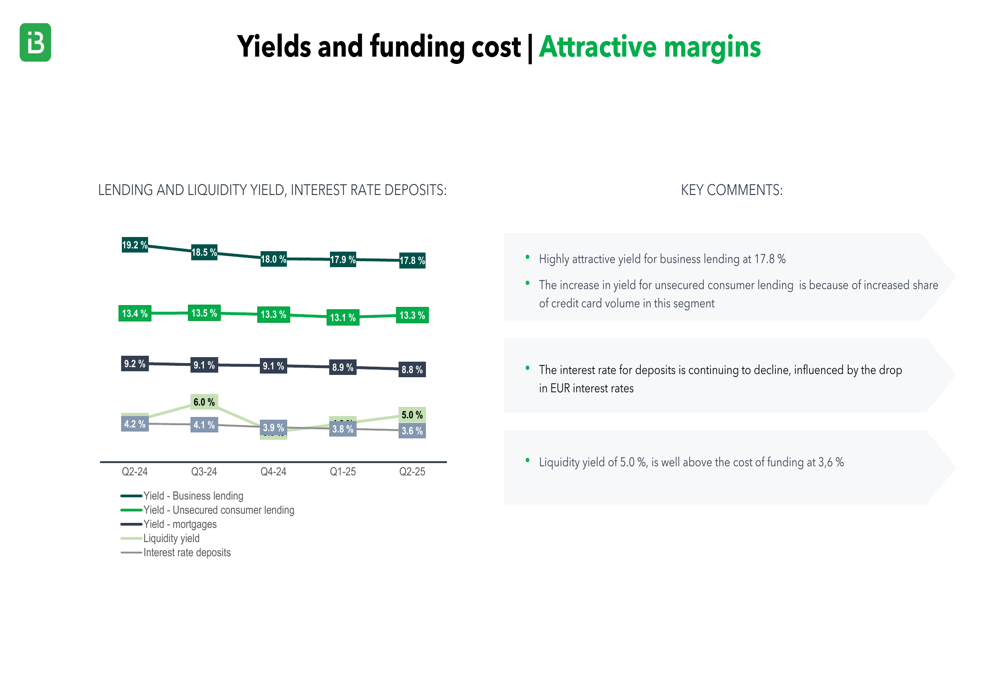

The bank maintains attractive yields across its lending segments, with business lending yielding 17.8%, credit cards 18.0%, consumer loans 12.3%, and mortgages 8.7%. Meanwhile, the interest rate for deposits continued to decline, positively impacting margins. The liquidity yield of 5.0% remains well above the cost of funding at 3.6%.

This yield structure is detailed in the following chart:

Operating expenses increased slightly to 64.2 MNOK, up 2.1 MNOK from the previous quarter. This increase was primarily attributed to marketing and operational costs for the German credit card offering (4.6 MNOK) and advisory and legal fees related to the Finnish banking license application (2 MNOK). Despite these increases, the cost-to-income ratio excluding marketing costs decreased by 3 percentage points from the previous quarter.

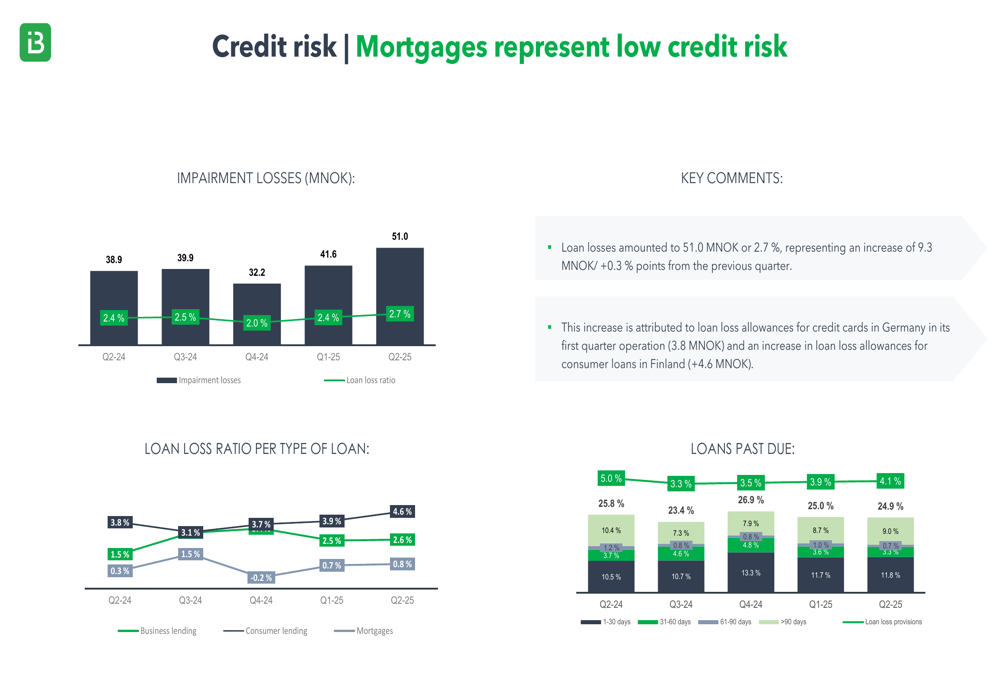

Loan losses amounted to 51.0 MNOK or 2.7% of the portfolio, representing an increase of 9.3 MNOK from the previous quarter. This increase was primarily due to loan loss allowances for credit cards in Germany in its first quarter of operation (3.8 MNOK) and an increase in loan loss allowances for consumer loans in Finland (4.6 MNOK).

The following chart shows the loan loss ratios across different lending segments:

On the capital front, Instabank strengthened its position by issuing an additional Tier 1 bond of 60 MNOK and a subordinated Tier 2 bond of 80 MNOK. The CET1 ratio stood at 17.4%, 1.3 percentage points above the regulatory capital requirement including the expected capital buffer of 2%. The total capital ratio was 23.8%, 2.0 percentage points above the total regulatory capital requirement.

Strategic Initiatives

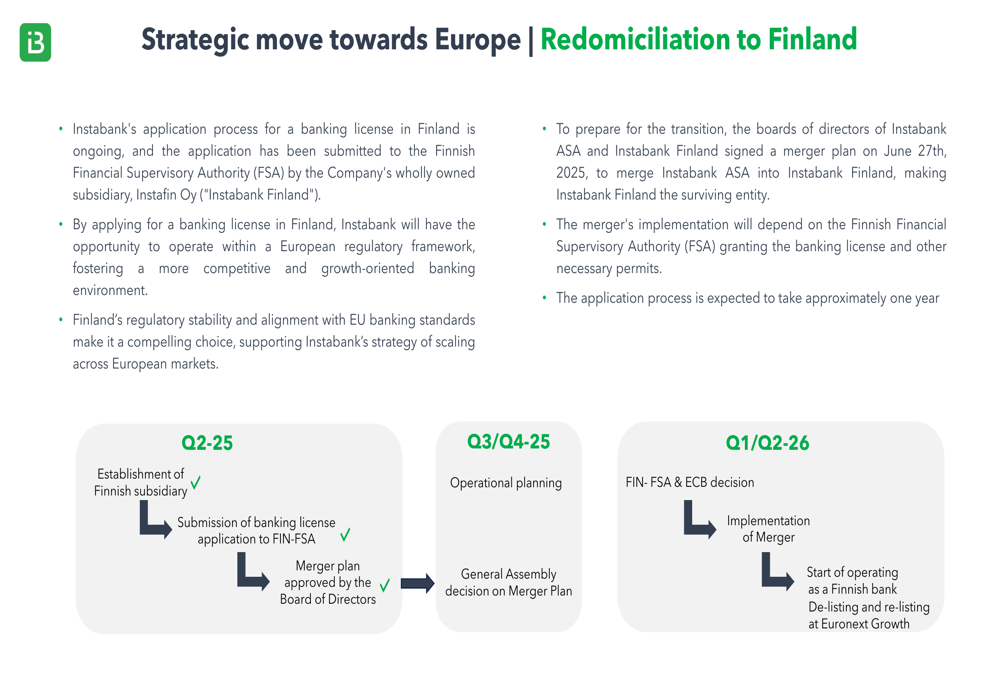

A key strategic focus for Instabank is its planned redomiciliation to Finland, which would facilitate broader European expansion. The application process for a Finnish banking license is ongoing, and the boards of directors of Instabank ASA and Instabank Finland signed a merger plan on June 27, 2025.

The timeline for this strategic move is illustrated below:

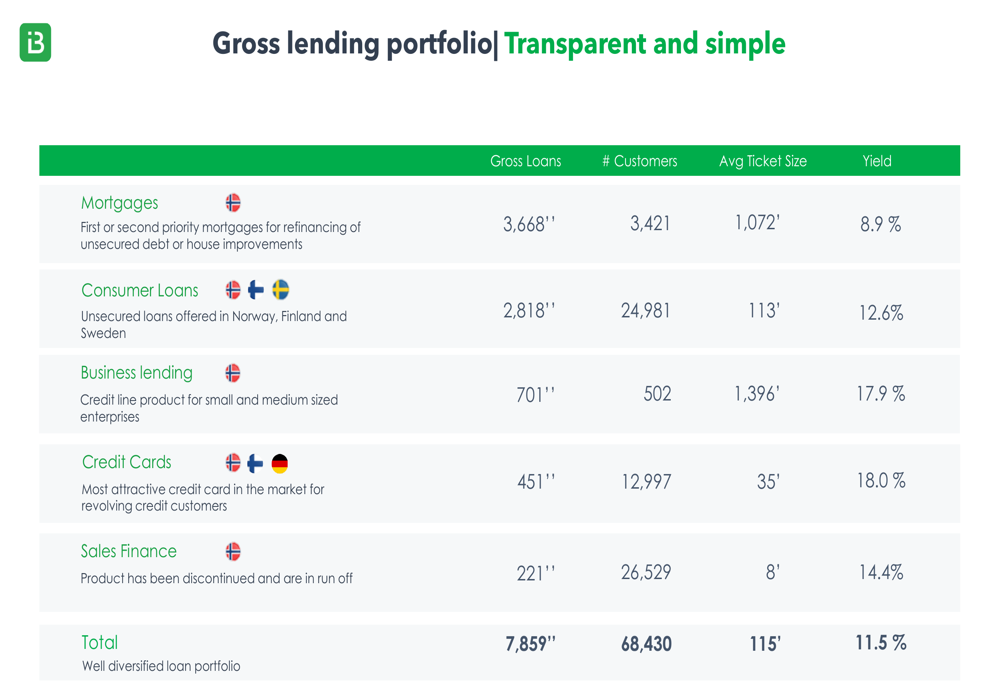

The company is also continuing its product diversification strategy, evolving from a specialized consumer finance bank to a focused commercial bank with offerings across both B2C and B2B segments. This includes savings products, consumer loans, mortgages, credit cards, and business lending.

The detailed breakdown of Instabank’s lending portfolio provides insight into the company’s diversification strategy:

The company’s funding base is similarly diversified across multiple countries, with Norway and Germany representing the largest deposit markets:

Forward-Looking Statements

Instabank provided financial guidance for 2025, targeting profit after tax of approximately 125 million NOK, return on equity above 12%, and gross loans of approximately 8.5 billion NOK. For the mid-term, the company has set more ambitious targets of profit after tax exceeding 200 million NOK, return on equity above 15%, and gross loans exceeding 10.0 billion NOK.

The company’s financial guidance is summarized in the following slide:

Management highlighted several key value propositions, including the bank’s dynamic and innovative approach, lean operational platform enabling cross-border operations, well-diversified loan portfolio, strong growth at attractive margins, proven track record of profitability, and experienced team.

As Instabank continues its strategic transformation and geographic expansion, investors will be watching closely to see if the company can maintain its growth trajectory while managing the increased expenses associated with its strategic initiatives, particularly the German credit card launch and Finnish banking license application.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.