Uber stock surges after Nvidia partnership announcement

Introduction & Market Context

Insteel Industries Inc (NYSE:IIIN), the nation’s largest manufacturer of steel wire reinforcing products for concrete construction applications, presented its investor overview on October 16, 2025. The presentation comes after the company’s recent Q4 2025 earnings release, which showed mixed results with year-over-year improvements but missed analyst expectations.

The company’s stock has experienced volatility following the earnings announcement, dropping 17% in pre-market trading after reporting an EPS of $0.74 against a forecast of $0.79, and revenue of $177.4 million versus an expected $180.97 million. Despite this setback, Insteel’s shares have recovered slightly to $31.15, still well above their 52-week low of $22.49.

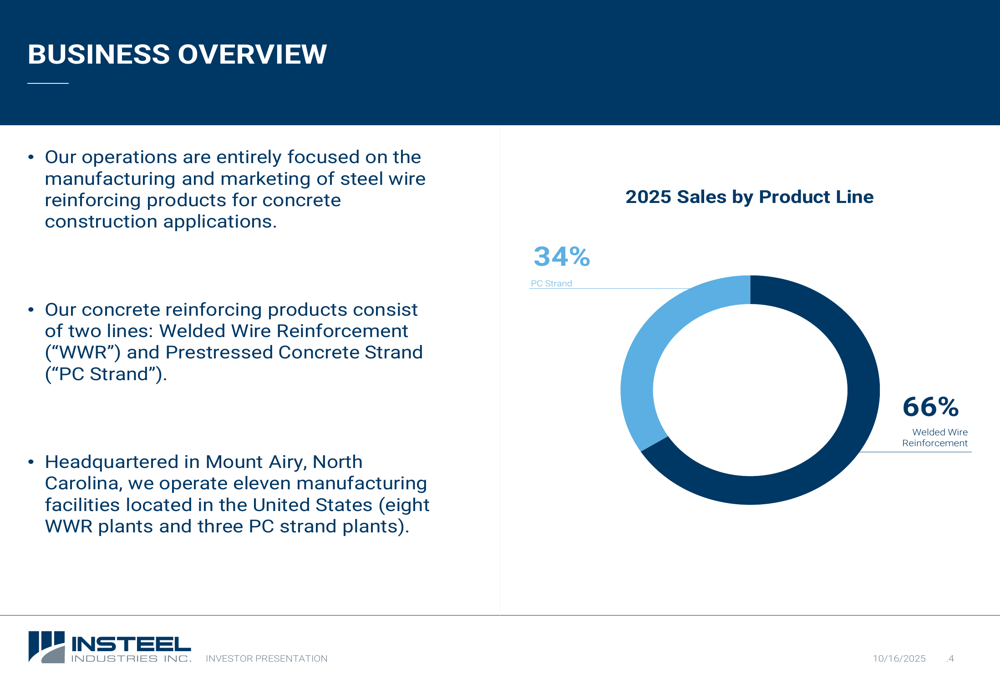

Founded in 1953 and headquartered in Mount Airy, North Carolina, Insteel operates 11 manufacturing facilities across the United States, employing 1,007 people. The company’s business is focused on two main product lines: Welded Wire Reinforcement (WWR) and Prestressed Concrete Strand (PC Strand).

As shown in the following chart, Welded Wire Reinforcement represents the majority of Insteel’s business, accounting for 66% of 2025 sales, while PC Strand contributes the remaining 34%:

Quarterly Performance Highlights

Insteel’s Q4 2025 results showed significant year-over-year improvement despite missing analyst expectations. The company reported net earnings of $14.6 million for the quarter, up from $4.7 million in the same period last year. Quarterly shipments increased by 9.8% year-over-year, while average selling prices rose 20.3%.

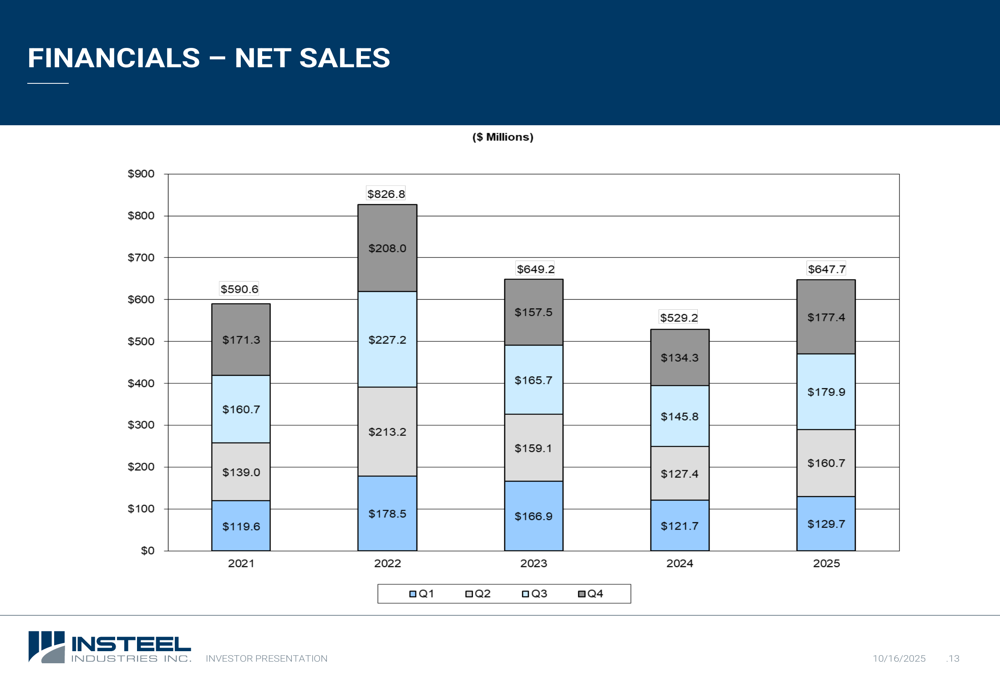

For the full fiscal year 2025, Insteel generated total net sales of $647.7 million, representing a 22.4% increase from $529.2 million in 2024. The company’s quarterly sales pattern shows a steady recovery throughout 2025, with Q3 and Q4 being particularly strong:

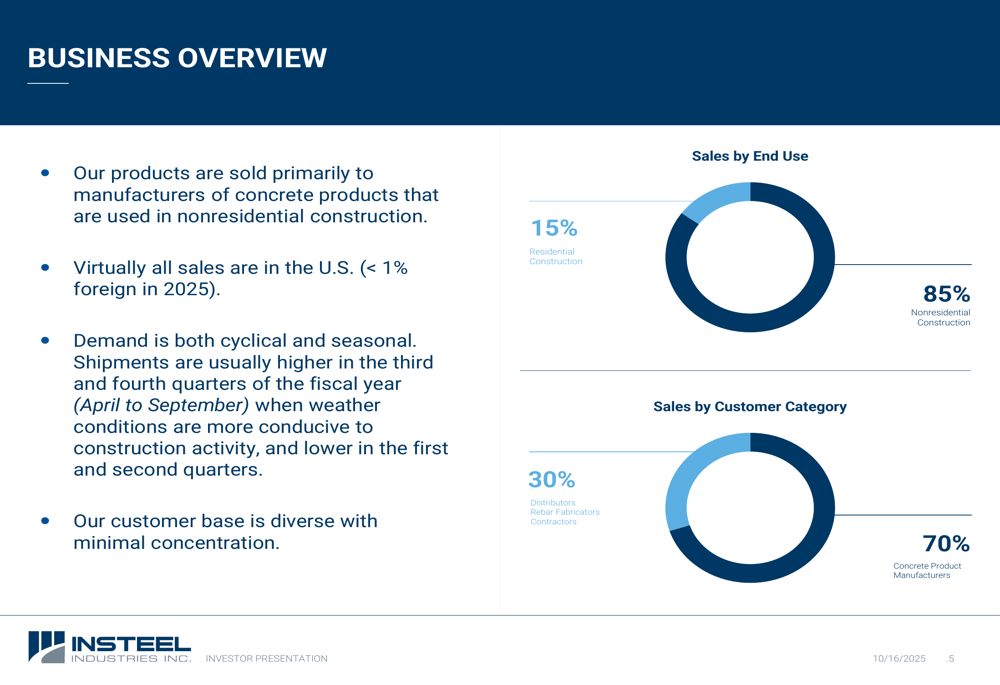

Insteel’s customer and market diversification remains stable, with 85% of sales directed to nonresidential construction and 15% to residential construction. From a customer perspective, 70% of sales go to concrete product manufacturers, while the remaining 30% are distributed among distributors, rebar fabricators, and contractors:

Detailed Financial Analysis

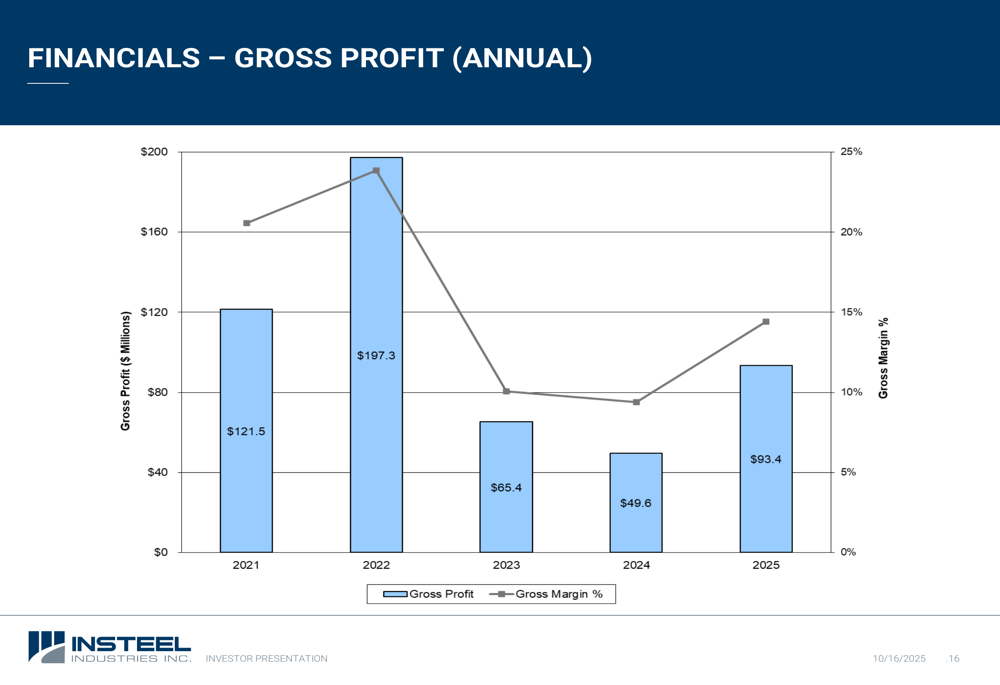

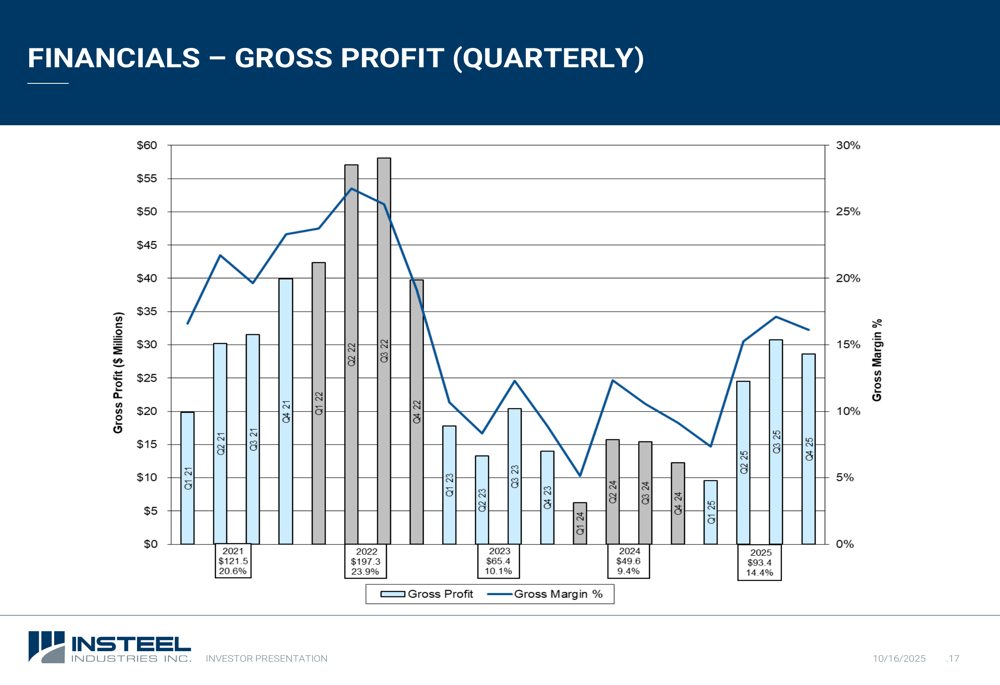

Insteel’s gross profit performance showed marked improvement in 2025, reaching $93.4 million (14.4% margin) compared to $49.6 million (9.4% margin) in 2024. This represents a 500 basis point improvement in gross margin, though still below the peak levels seen in 2021-2022:

The quarterly breakdown of gross profit reveals a consistent upward trend throughout 2025, with Q3 and Q4 showing particularly strong results. This improvement occurred despite raw materials constituting 68% of the company’s cost of sales, highlighting Insteel’s ability to manage input costs effectively:

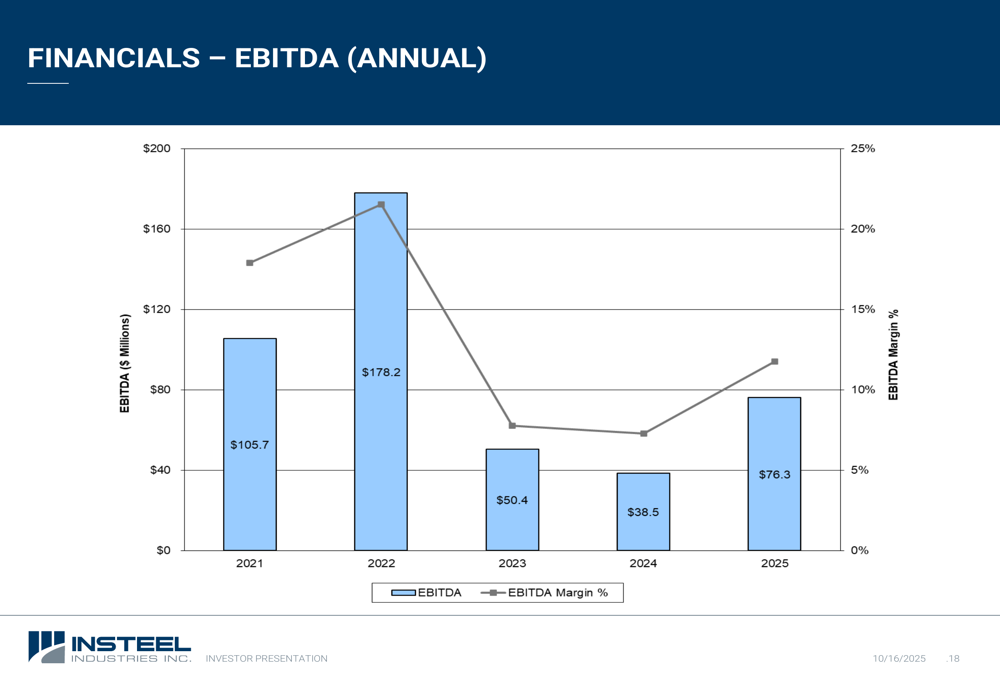

EBITDA followed a similar trajectory, nearly doubling to $76.3 million (11.8% margin) in 2025 from $38.5 million (7.3% margin) in 2024:

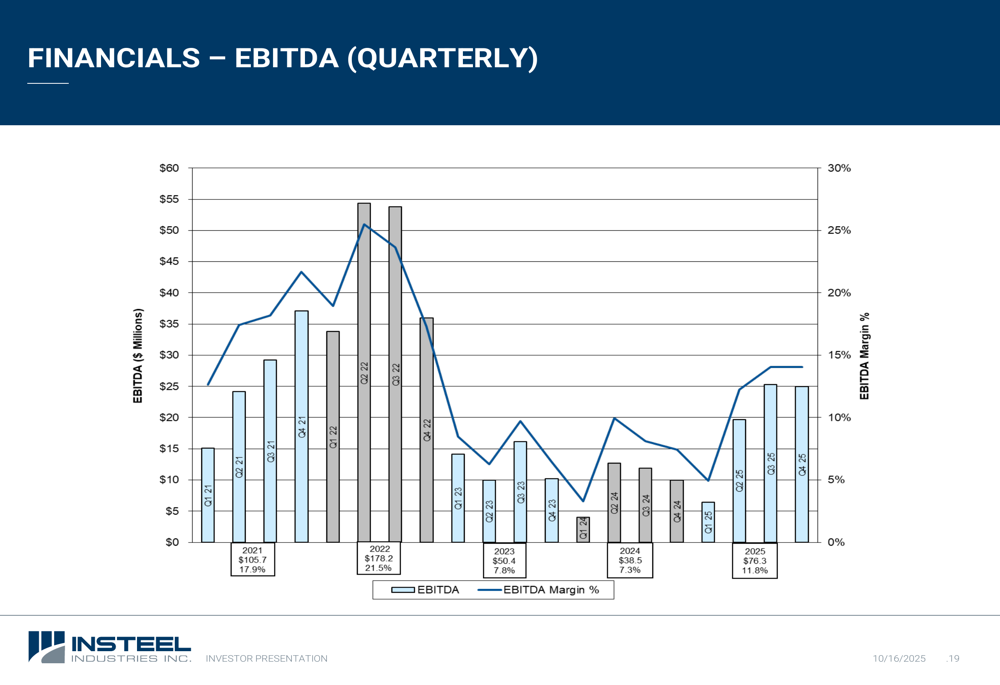

The quarterly EBITDA breakdown further illustrates the company’s improving performance throughout 2025:

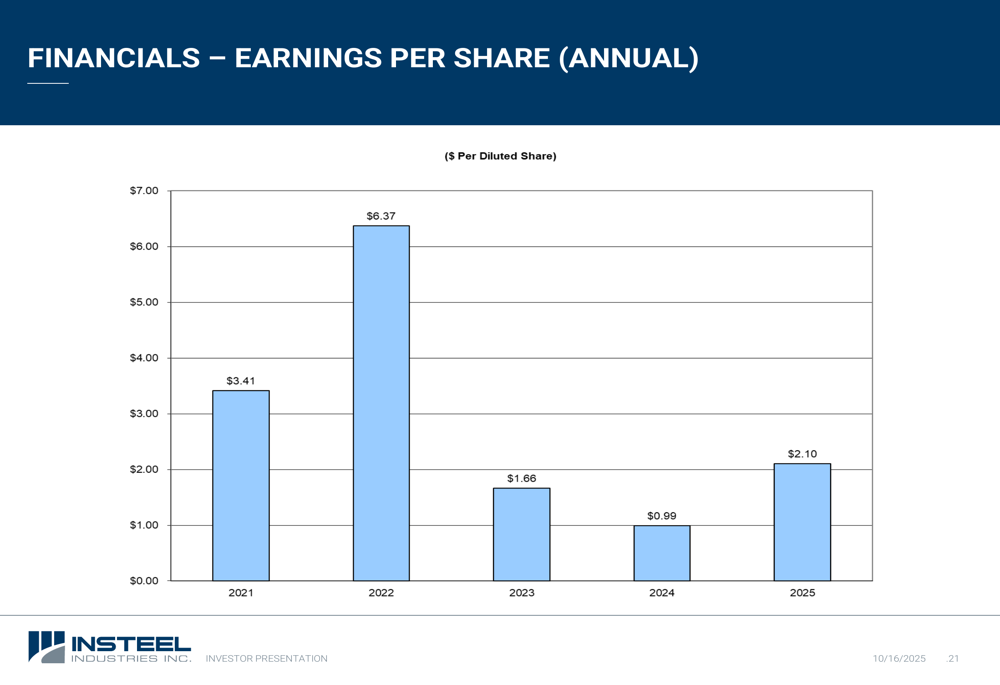

Earnings per share doubled to $2.10 in 2025 from $0.99 in 2024, though still well below the exceptional performance of $6.37 in 2022:

Strategic Initiatives

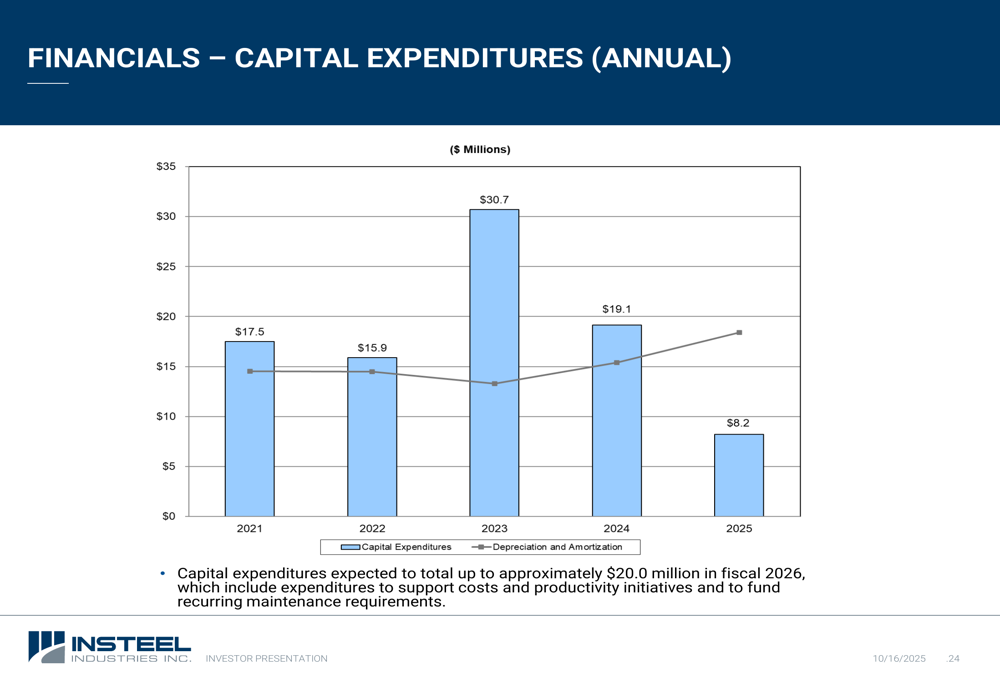

Insteel’s capital expenditures decreased to $8.2 million in 2025 from $19.1 million in 2024. However, the company plans to increase capital spending to approximately $20 million in fiscal 2026 to support cost and productivity initiatives:

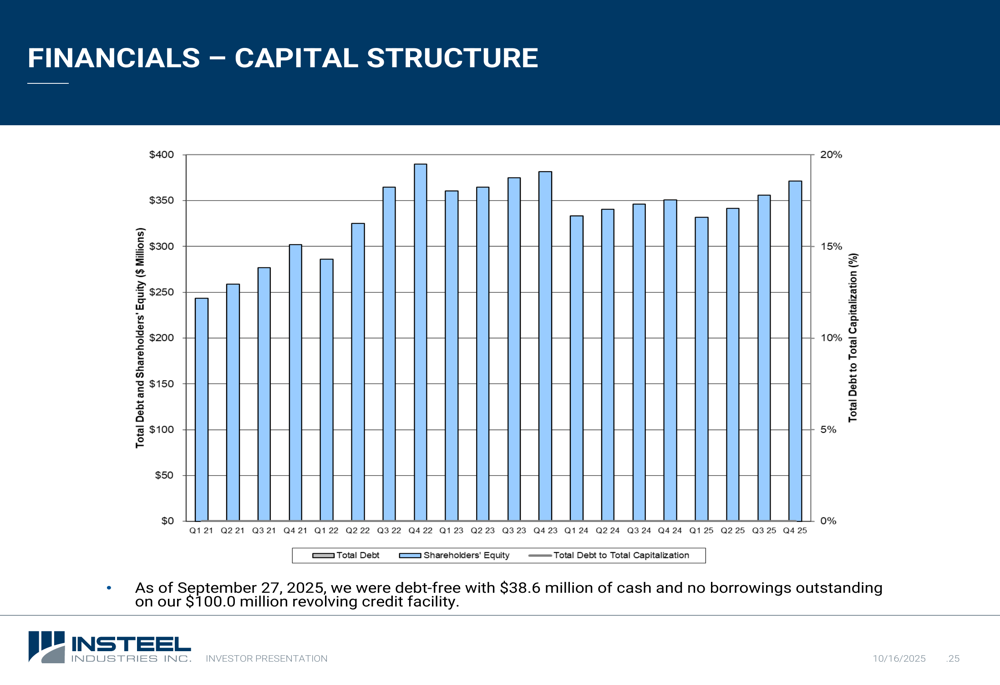

The company maintains a strong balance sheet with no debt and $38.6 million in cash as of September 27, 2025. This financial flexibility positions Insteel well for future growth opportunities:

Insteel’s growth strategy includes both organic expansion and strategic acquisitions. The company completed two acquisitions in fiscal 2025: Engineered Wire Products in October 2024 and O’Brien Wire Products in November 2024. These acquisitions align with Insteel’s focus on pursuing opportunities in existing core businesses that offer substantial synergy potential.

The organic growth strategy centers on converting traditional rebar users to Engineered Structural Mesh (ESM) for cast-in-place applications. ESM eliminates the labor-intensive process of placing and hand-tying rebar, resulting in cost savings and faster construction. Additionally, ESM’s higher yield strength (80,000 PSI versus 60,000 PSI for rebar) typically requires fewer tons of steel.

Forward-Looking Statements

Insteel expressed cautious optimism about the outlook for fiscal 2026, particularly in the nonresidential construction sector. During the earnings call, CEO H.O. Woltz III stated, "We see the activity out there and we think it will continue," highlighting the company’s confidence despite recent market challenges.

The company is monitoring key leading indicators for nonresidential building construction activity. The Architecture Billings Index (ABI) stood at 47.2 in August, up slightly from 46.2 in July but still below the 50 threshold that indicates growth. Meanwhile, the Dodge Momentum Index (DMI) showed continued strength, rising 3.4% in September and up 33% year-to-date, driven largely by robust commercial construction planning activity, particularly in data center development.

Insteel also addressed supply chain challenges during its earnings call, noting the strategic decision to source wire rod from offshore markets due to domestic supply constraints. "The underlying reason that we went to the offshore markets was the inability to assure that we had availability domestically," explained Woltz.

Looking ahead, Insteel’s investment considerations include its strong cash flow generation, highly variable cost structure, growth potential through increased capacity utilization, and national footprint. The company’s modern manufacturing facilities and competitive cost structure, combined with its financial strength and flexibility, position it well to navigate market challenges and capitalize on growth opportunities in fiscal 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.