United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Intuit Inc. (NASDAQ:INTU) released its latest corporate presentation on May 22, 2025, showcasing strong financial performance across all business segments. The financial software giant, known for its TurboTax, QuickBooks, Credit Karma, and Mailchimp offerings, has seen its stock surge 8.1% in aftermarket trading to $720, approaching its 52-week high of $714.78.

The presentation comes after Intuit’s impressive Q2 FY25 earnings report, where the company delivered an earnings per share (EPS) of $3.32, significantly exceeding analyst expectations of $2.58. Revenue for that quarter reached $4 billion, outpacing forecasts of $3.83 billion and demonstrating the company’s continued momentum.

Quarterly Performance Highlights

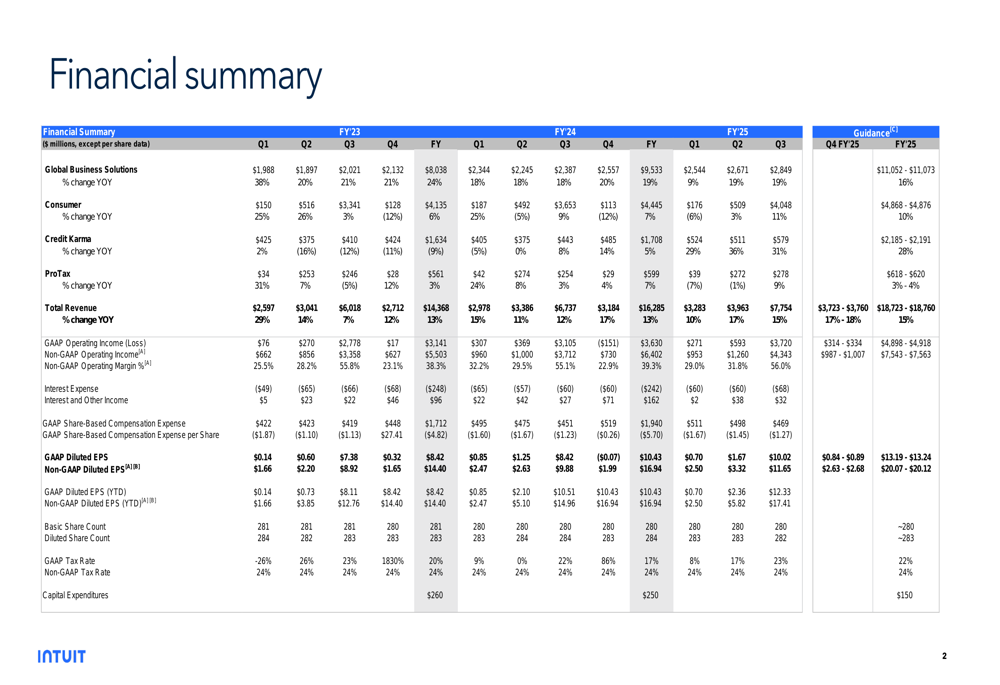

Intuit’s Q3 FY25 results show substantial growth across its business segments. The Consumer segment, which includes TurboTax, generated $4,048 million in revenue during Q3, reflecting the seasonal strength of tax filing season. Meanwhile, Global Business Solutions, which encompasses QuickBooks and related services, delivered $2,849 million in Q3 revenue.

As shown in the detailed financial summary below, Intuit is on track to achieve 17-18% year-over-year growth in total revenue for FY25:

Credit Karma continues to be Intuit’s fastest-growing segment, with projected annual growth of 28% for FY25. The segment generated $579 million in Q3 FY25, showing consistent quarterly improvement throughout the fiscal year.

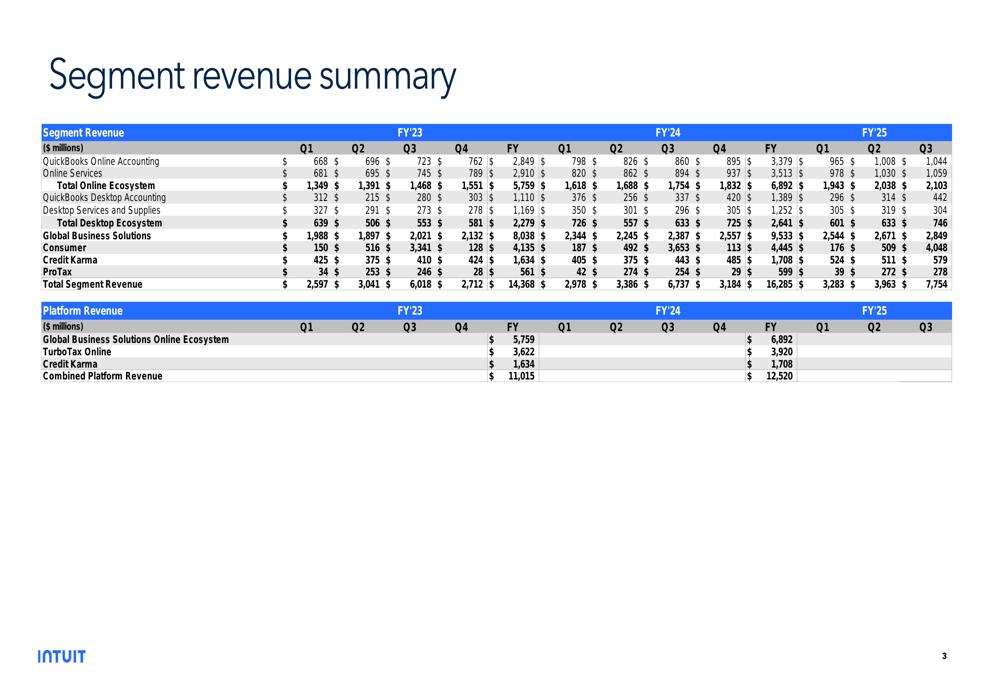

The company’s segment revenue breakdown provides further insight into the performance of specific product lines:

Detailed Financial Analysis

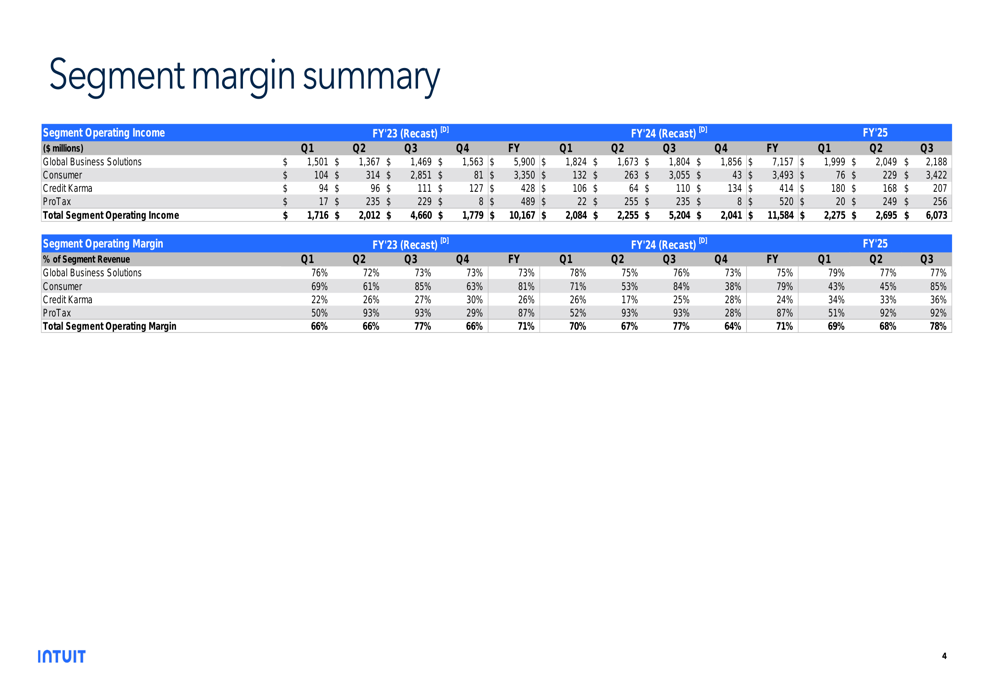

Intuit’s profitability metrics remain robust across all business segments. The Consumer segment, which includes TurboTax, achieved an impressive 85% margin in Q3 FY25, up from 79% for the full FY24. This demonstrates the company’s ability to leverage its scale during the critical tax season.

ProTax maintained exceptional margins of 92% in both Q2 and Q3 of FY25, while Global Business Solutions consistently delivered margins in the high 70% range. Credit Karma showed margin improvement to 36% in Q3 FY25, up from the 24% reported for full-year FY24.

The following segment margin summary illustrates these trends:

For the first three quarters of FY25, Intuit has already generated $15 billion in revenue, positioning the company well to achieve its full-year guidance of $18.723-$18.760 billion. This represents a significant acceleration from the $16.285 billion reported for FY24.

The company’s earnings trajectory also remains strong, with guidance for GAAP diluted EPS of $13.19-$13.24 and non-GAAP diluted EPS of $20.07-$20.12 for FY25, compared to $10.43 and $16.94 respectively for FY24.

Forward-Looking Statements

Intuit’s presentation includes guidance that aligns with CEO Sasan Gudarzi’s recent statement that the company is "confident in delivering double-digit revenue growth and expanding margin this year." The projected 17-18% revenue growth for FY25 supports this outlook.

The company faces potential risks from competition, technological changes, and economic conditions affecting small businesses. However, Intuit’s strong performance across segments suggests it is successfully navigating these challenges while capitalizing on opportunities in artificial intelligence and mid-market expansion.

Intuit’s continued investment in AI-driven solutions appears to be paying dividends, as reflected in the strong margins and revenue growth across its product portfolio. The company’s focus on the mid-market segment, which CEO Gudarzi suggested "one day will be bigger than the entire business group," represents a significant growth opportunity.

With three quarters of FY25 now reported, Intuit appears well-positioned to meet or exceed its full-year financial targets, continuing its trajectory of strong revenue growth and margin expansion across its diversified business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.