Five things to watch in markets in the week ahead

Introduction & Market Context

ISS A/S (CPH:ISS) reported its H1 2025 interim results on August 12, 2025, highlighting steady performance in line with management expectations. The facility services provider saw its stock rise 0.65% to DKK 186.4 following the presentation, approaching its 52-week high of DKK 191.2.

The company continues to navigate a challenging global business environment with varying regional performance, while maintaining its focus on key industry segments and sustainability initiatives. ISS’s presentation emphasized its resilience through economic cycles and its strategy of maximizing shareholder returns.

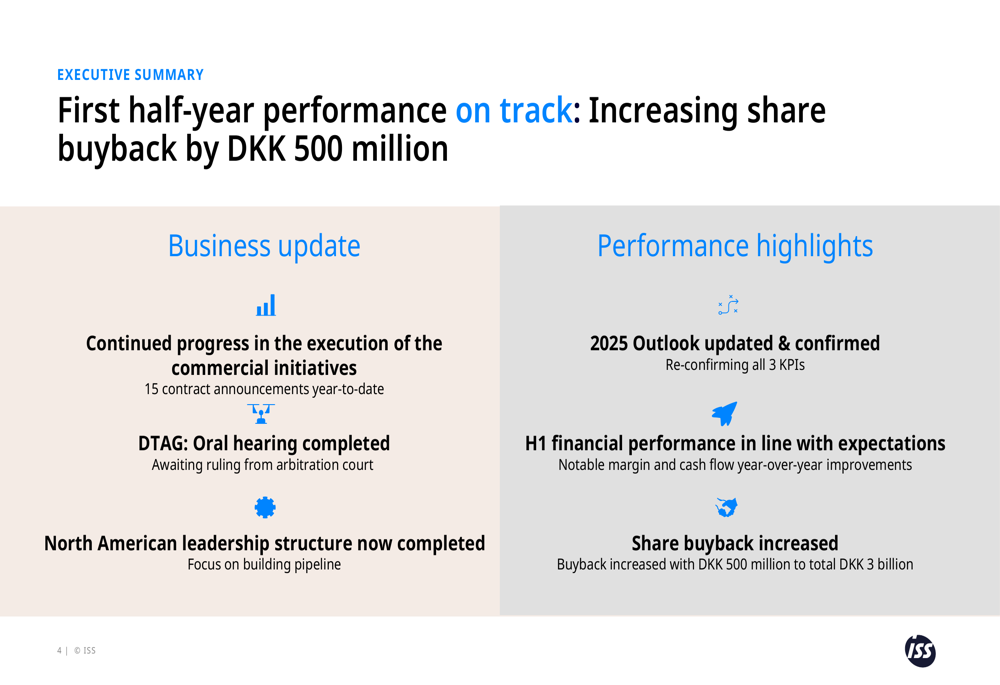

Executive Summary

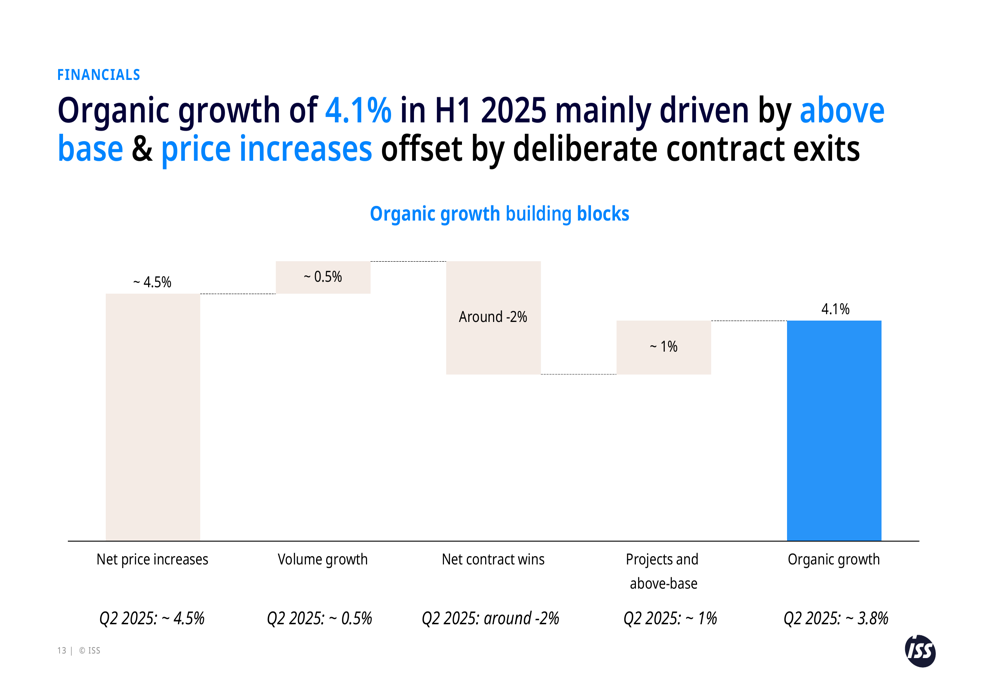

ISS described its H1 2025 performance as "on track" and announced an increase to its share buyback program by DKK 500 million, bringing the total to DKK 3 billion. The company reported organic growth of 4.1% for the first half of 2025, down from 5.9% in the same period last year, but still within its full-year guidance range of 4-6%.

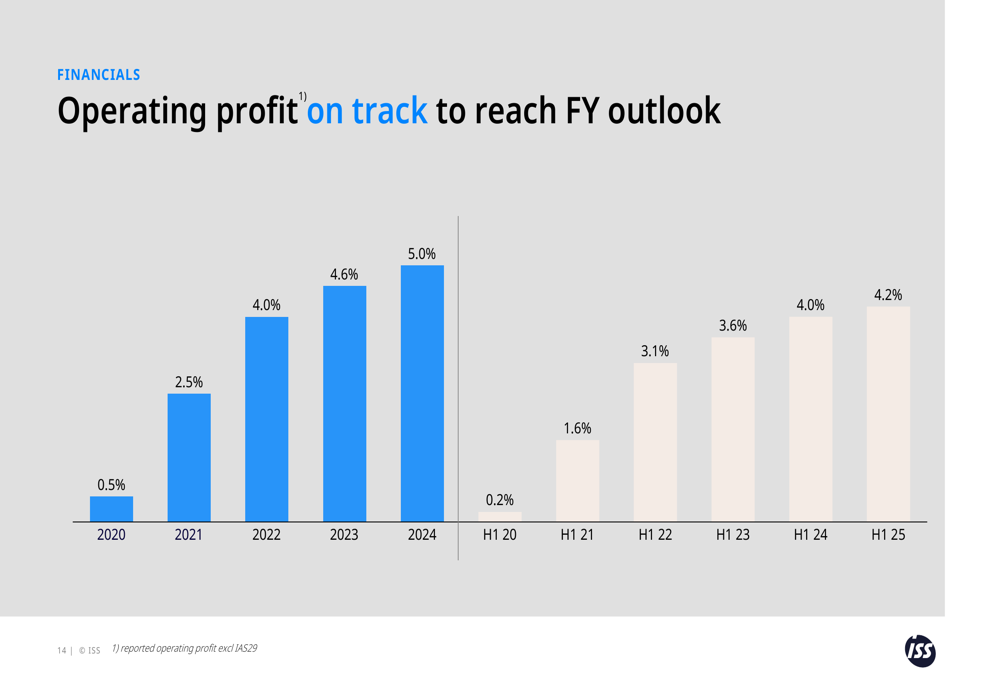

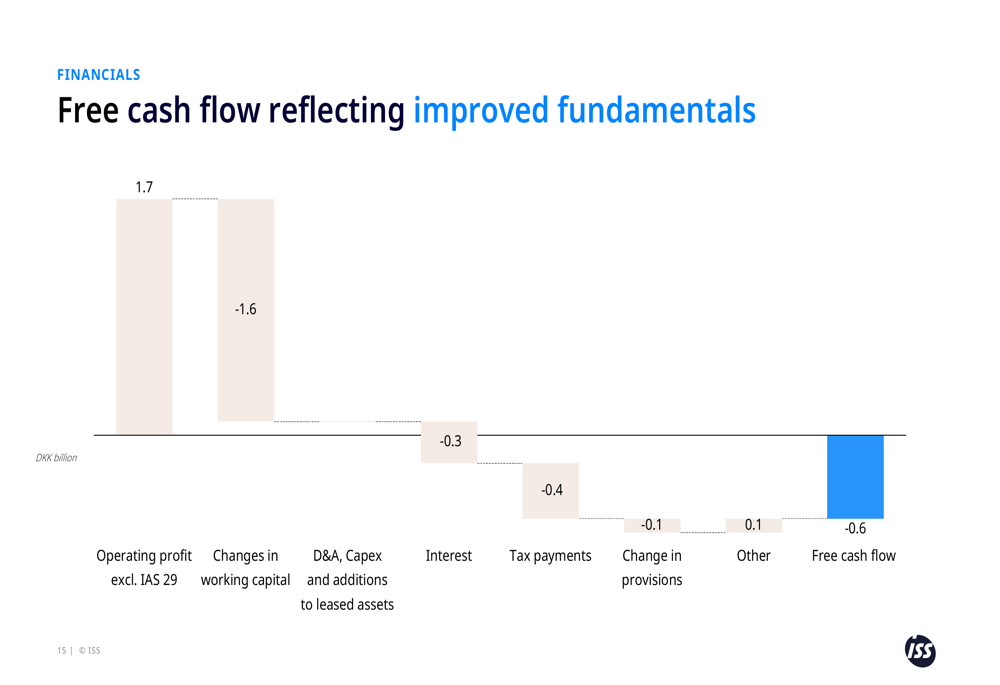

Operating margin improved to 4.2% in H1 2025, up from 4.0% in H1 2024, continuing a positive trend that began in 2020. Free cash flow also showed improvement at DKK -0.6 billion compared to DKK -1.1 billion in H1 2024.

As shown in the following performance highlights slide, the company made continued progress in executing its commercial initiatives with 15 contract announcements year-to-date:

Quarterly Performance Highlights

ISS reported varied performance across its regions for H1 2025. Central & Southern Europe led with strong 9% organic growth and a margin of 5.6%, while Asia & Pacific delivered 6% growth with the highest regional margin at 6.7%. Northern Europe, which represents 38% of group revenue, showed modest 2% growth with a margin of 4.9%.

The Americas region continued to face challenges, posting a 9% decline in organic growth and a reduced margin of 2.8%, down from 4.6% in H1 2024. This aligns with the trend observed in Q1 2025, where the region also reported a 9% decline.

The following slide illustrates the regional performance breakdown:

ISS’s organic growth of 4.1% in H1 2025 was primarily driven by net price increases of approximately 4.5%, with modest volume growth of 0.5% and projects and above-base work contributing about 1%. These positive factors were partially offset by net contract losses of around 2%.

The breakdown of organic growth components is clearly visualized in this chart:

Detailed Financial Analysis

ISS’s operating margin continued its steady improvement trajectory, reaching 4.2% in H1 2025 compared to 4.0% in H1 2024. This represents significant progress from the 0.5% margin recorded in 2020, demonstrating the company’s successful margin recovery strategy.

The following chart shows the consistent margin improvement over time:

Free cash flow showed notable improvement at DKK -0.6 billion in H1 2025 compared to DKK -1.1 billion in H1 2024. While still negative, which is typical for the first half of the year in ISS’s business model, the improvement reflects better operational execution and working capital management.

The components of free cash flow are broken down in this waterfall chart:

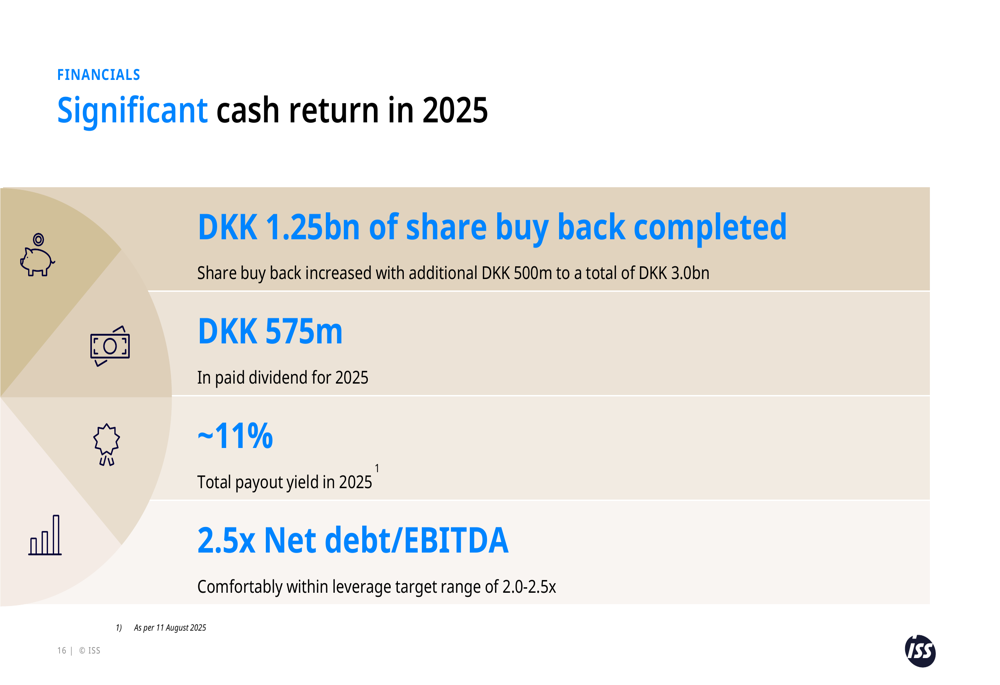

ISS highlighted its significant cash return to shareholders in 2025, with DKK 1.25 billion of share buybacks completed to date and the program now increased by an additional DKK 500 million to a total of DKK 3.0 billion. Combined with DKK 575 million in paid dividends, this represents approximately 11% total payout yield for 2025.

The company’s net debt to EBITDA ratio stands at 2.5x, which is within its target range of 2.0-2.5x, indicating a balanced approach to leverage:

Strategic Initiatives

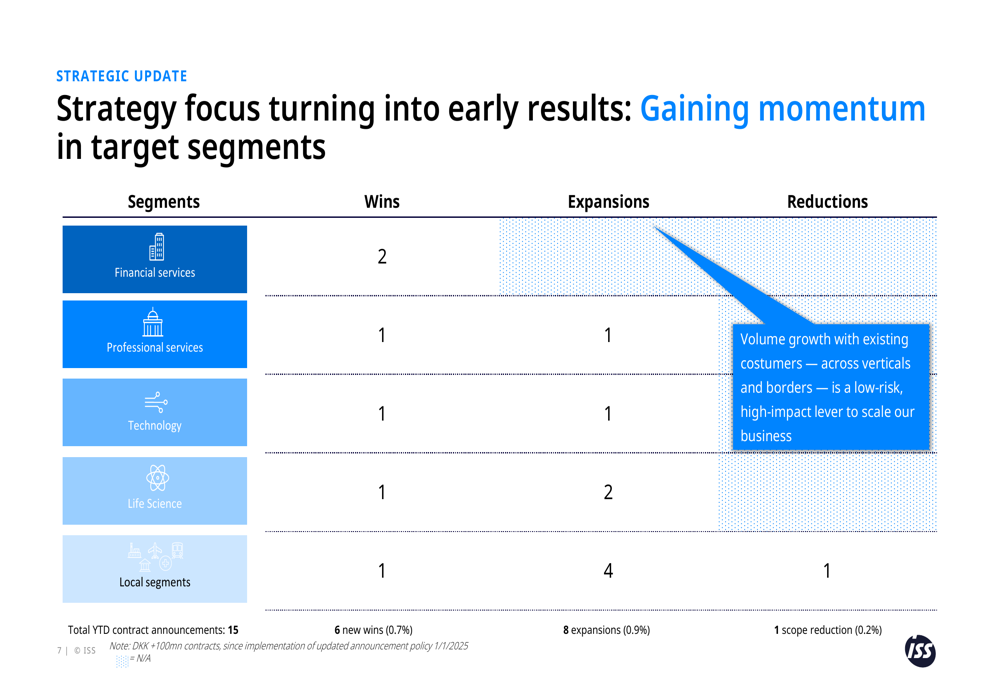

ISS reported continued progress in executing its commercial strategy, with a focus on target segments including financial services, professional services, technology, and life sciences. The company secured 6 new contract wins and 8 expansions with existing customers, each valued above DKK 100 million.

The following slide shows the distribution of wins, expansions, and reductions across key segments:

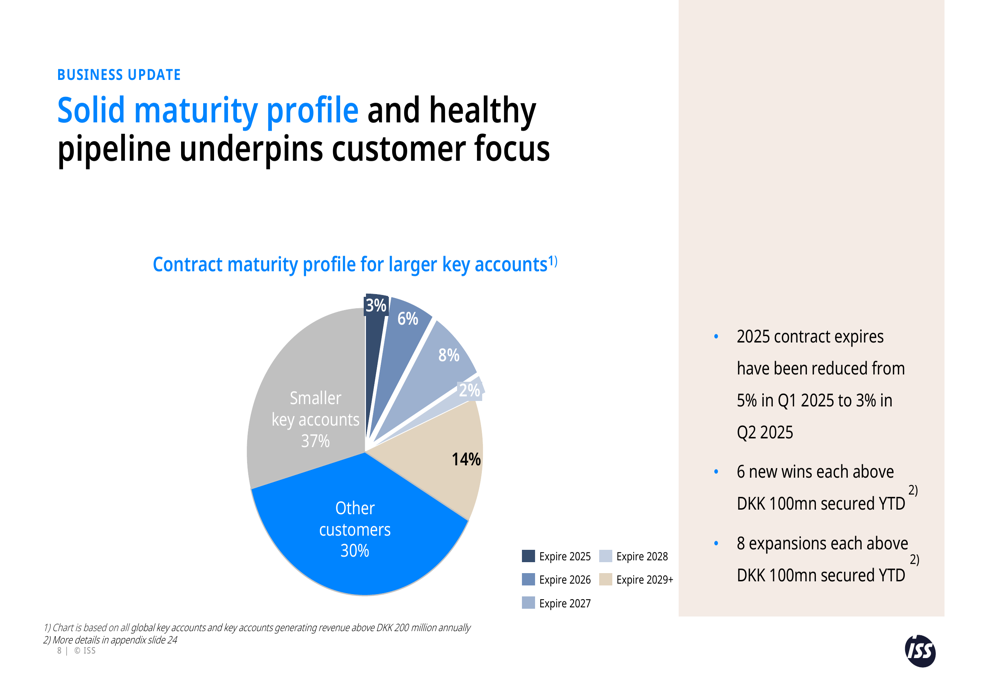

The company also highlighted its improved contract maturity profile, with only 3% of larger key account contracts expiring in 2025, down from 5% in Q1 2025. This reduction in near-term expirations provides greater revenue visibility and stability.

The contract maturity profile is illustrated in this pie chart:

ISS reported progress on its social sustainability commitments, with 13 countries achieving living wages for all placemakers and the company on track to exceed its target of providing 100,000 placemakers with recognized qualifications by the end of 2025. More than 12,000 placemakers received recognized qualifications in H1 2025 alone.

Forward-Looking Statements

ISS reconfirmed its full-year 2025 outlook with organic growth expected between 4-6%, operating margin above 5%, and free cash flow exceeding DKK 2.4 billion. The company noted that while net price increases and above-base work remain unchanged in their outlook, volume growth is slightly up and net new wins are slightly down compared to previous expectations.

The Department for Work and Pensions (DWP) contract mobilization in the UK is progressing as planned, with the contract valued at DKK 1.2 billion (£135 million) set to go live on October 1, 2025. This involves mobilizing 774 sites across the UK and transferring 2,325 employees from the previous supplier.

ISS’s capital allocation strategy remains focused on maintaining its leverage ratio within the target range of 2.0-2.5x while balancing dividends, investments in the existing business, and share buybacks. The company expects to continue delivering significant shareholder returns, with total shareholder returns projected to reach DKK 3.6 billion in 2025, up from DKK 3.0 billion in 2024.

Despite challenges in the Americas region, ISS appears well-positioned to achieve its full-year targets through continued focus on operational execution, strategic customer segments, and margin improvement initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.