Michigan survey ahead; Applied Digital surges; gold dips - what’s moving markets

Introduction & Market Context

Jamieson Wellness Inc. (TSX:JWEL), a leading global health and wellness company, released its investor presentation on May 8, 2025, showcasing strong first-quarter results and an optimistic outlook for the full year. The company, which recently celebrated its 100-year anniversary, continues to leverage its established Canadian market position to drive international expansion, particularly in high-growth markets like China.

The health and wellness sector continues to benefit from several megatrends highlighted in the presentation, including an aging population, increasing focus on health consciousness (including GLP-1 trends), rising disposable income in emerging markets, and more informed consumers with greater access to information.

Executive Summary

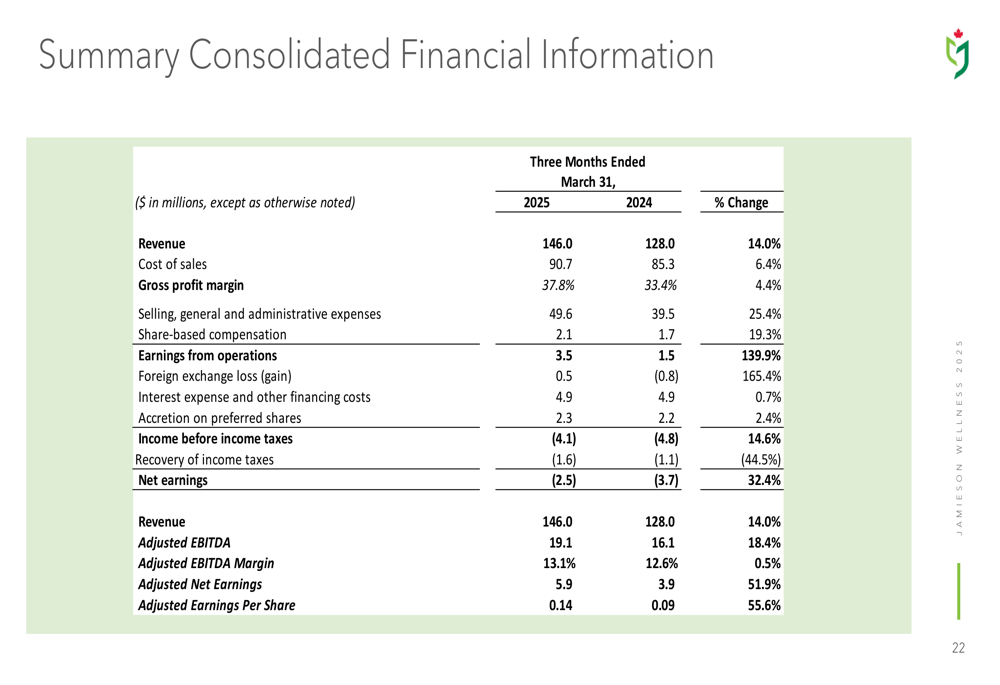

Jamieson reported Q1 2025 revenue of $146.0 million, representing a 14.0% increase compared to the same period last year. Adjusted EBITDA rose 18.4% to $19.1 million, with margins improving to 13.1% from 12.6% in Q1 2024. Adjusted earnings per share jumped 55.6% to $0.14.

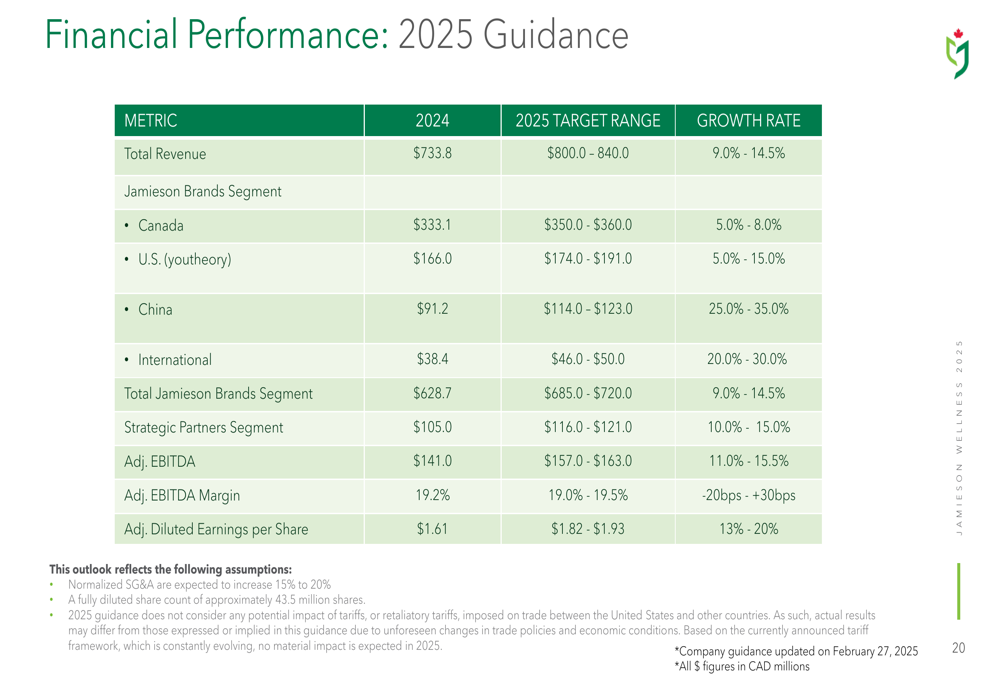

For the full year 2025, Jamieson is guiding for revenue between $800-$840 million, representing growth of 9.0-14.5% from 2024’s $733.8 million. The company expects adjusted EBITDA to reach $157.0-$163.0 million, up 11.0-15.5% from $141.0 million in 2024.

As shown in the following detailed financial guidance for 2025:

Detailed Financial Analysis

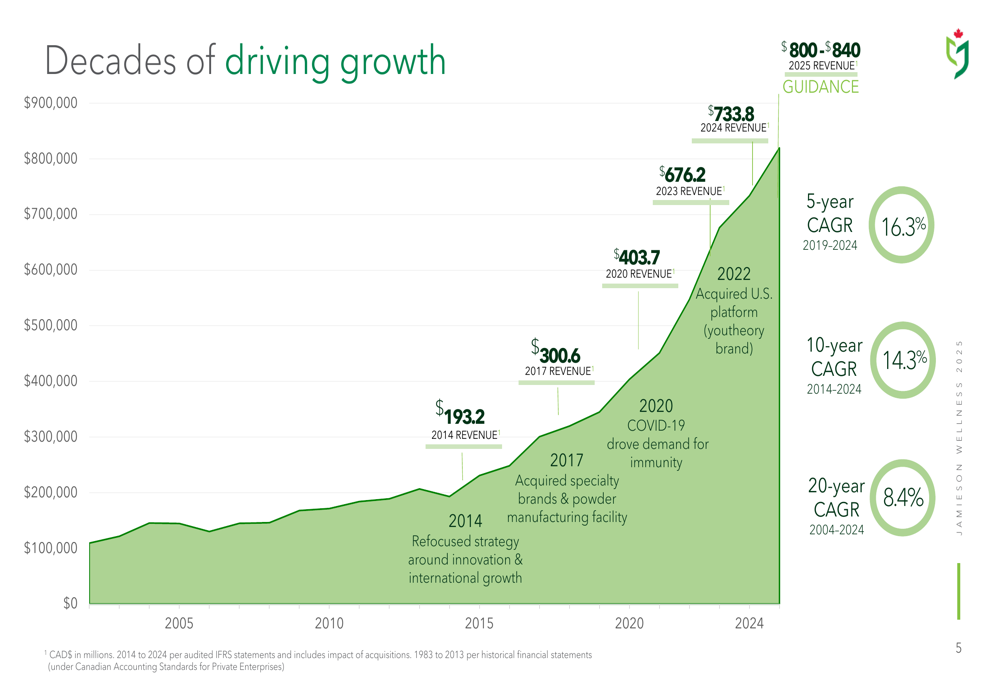

Jamieson has demonstrated consistent financial growth over multiple time horizons. The company achieved a 5-year CAGR (2019-2024) of 16.3% and a 10-year CAGR (2014-2024) of 14.3%, illustrating its ability to sustain long-term growth. The acquisition of youtheory in 2022 provided an additional growth catalyst.

The company’s revenue trajectory is clearly illustrated in this historical growth chart:

Beyond top-line growth, Jamieson has shown steady improvement in profitability metrics. Adjusted EBITDA has grown from $88.0 million in 2020 to $141.0 million in 2024, representing a CAGR of 12.5%. Similarly, adjusted earnings per share increased from $1.16 in 2020 to $1.61 in 2024, with a CAGR of 8.5%.

Cash flow generation has also been strong, with cash flow from operations reaching $81.5 million in 2024 and projected to grow to $100.0-$110.0 million in 2025. This has supported consistent dividend growth, with the annual dividend increasing at a CAGR of 17.0% from 2020 to 2024, reaching $0.80 in 2024 and projected at $0.88 for 2025.

The Q1 2025 results show acceleration across key metrics compared to previous quarters, suggesting momentum is building in the company’s growth strategy:

Strategic Growth Initiatives

Jamieson’s growth strategy centers around four key pillars: expansion in the USA, China, Canada, and International markets, with an aspiration to surpass $1 billion in net revenue.

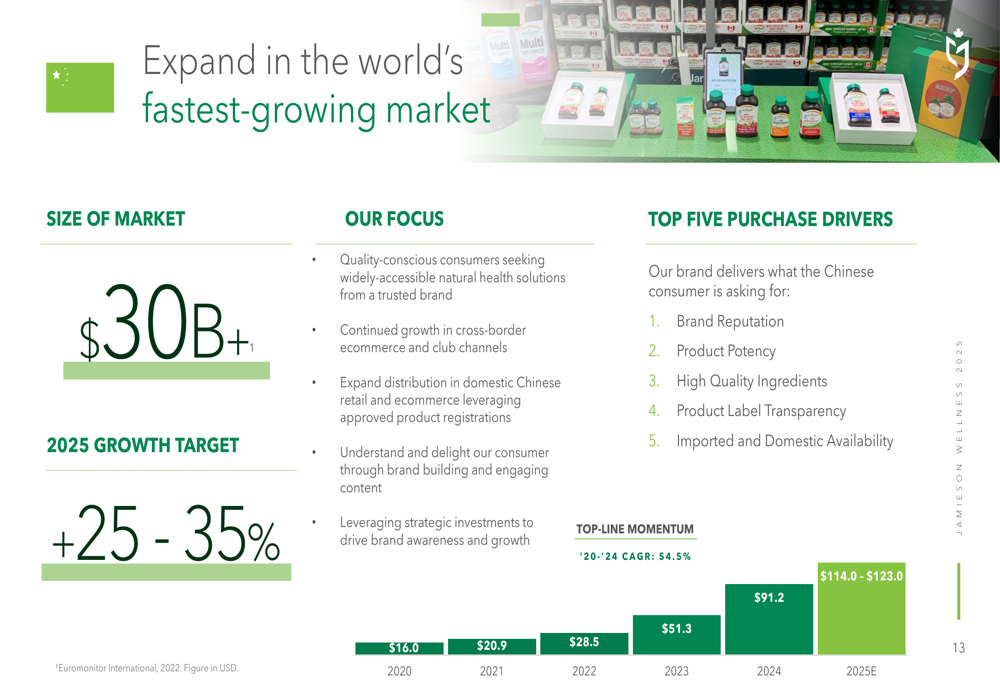

China represents the company’s fastest-growing market, with 2024 revenue of $91.2 million expected to increase by 25.0-35.0% to $114.0-$123.0 million in 2025. The company is focusing on cross-border e-commerce and club channels while expanding distribution in domestic Chinese retail and e-commerce leveraging approved product registrations.

The impressive growth trajectory in China is illustrated in the following chart:

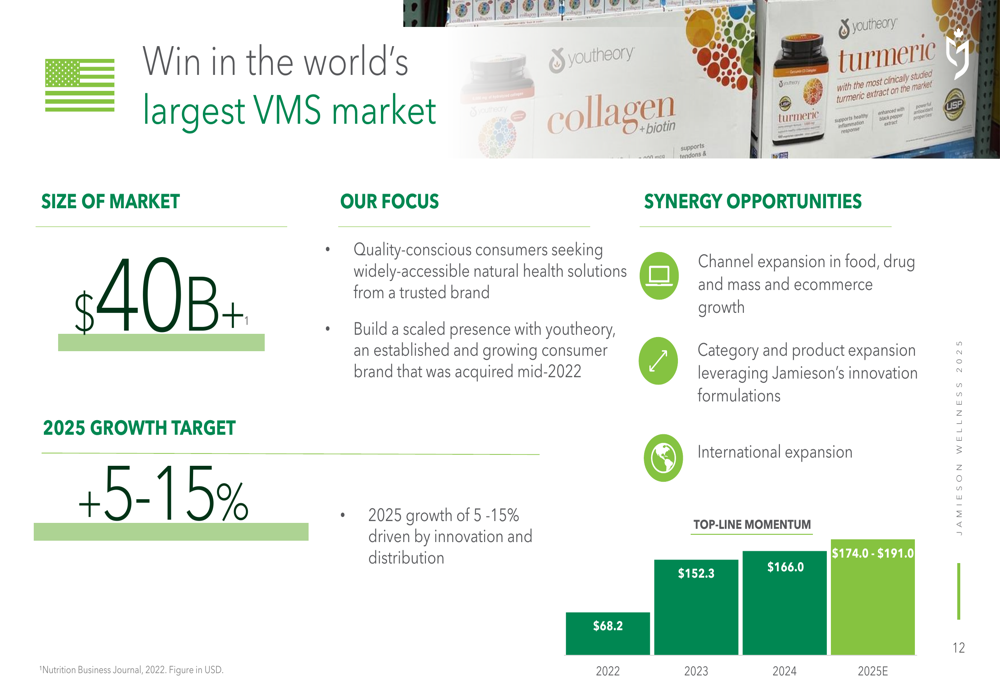

In the United States, Jamieson is building on its 2022 acquisition of youtheory, with 2025 revenue projected to reach $174.0-$191.0 million, representing growth of 5.0-15.0%. The company is targeting quality-conscious consumers seeking natural health solutions from trusted brands.

The U.S. growth strategy and performance is shown here:

Meanwhile, Jamieson continues to strengthen its leadership position in Canada, where it holds the #1 position in the VMS (vitamins, minerals, and supplements) market. Canadian revenue is projected to grow 5.0-8.0% to $350.0-$360.0 million in 2025.

International markets beyond the core regions are expected to deliver 20.0-30.0% growth in 2025, reaching $46.0-$50.0 million in revenue.

The company’s diverse brand portfolio, featuring the flagship Jamieson brand alongside youtheory and specialty Canadian brands, provides multiple growth avenues:

Forward-Looking Statements

Jamieson’s management has outlined ambitious but achievable targets for 2025, with overall revenue growth of 9.0-14.5% and adjusted EBITDA growth of 11.0-15.5%. The company expects adjusted EBITDA margins to remain stable at 19.0-19.5%, while adjusted EPS is projected to grow 13-20% to $1.82-$1.93.

The company’s commitment to quality remains a cornerstone of its strategy, with all products manufactured according to its "360 Quality" program and facilities operating at pharmaceutical standards. This focus on quality is particularly important as the company expands internationally, where trust in product integrity is crucial for premium positioning.

Sustainability initiatives are also gaining prominence in Jamieson’s strategy, with targets including a 50% reduction in Scope 1 & 2 emissions by 2030 and a path to Net Zero by 2050. The company has also set diversity and inclusion targets for leadership and board roles.

With a current stock price of $31.63, trading within its 52-week range of $25.60-$38.20, Jamieson Wellness appears well-positioned to execute its growth strategy across global markets, with China emerging as the most significant growth driver for the foreseeable future.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.