Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Jamieson Wellness Inc. (TSX:JWEL) reported strong fourth-quarter results for 2024, demonstrating continued momentum across its key markets and setting an optimistic tone for 2025. The Canadian health and wellness company, known for its vitamins and supplements, delivered double-digit revenue growth in Q4, with particularly impressive performance in its China operations.

The company’s shares have been trading between $27.42 and $38.20 over the past 52 weeks, with a recent closing price of $35.47 as of June 23, 2025, reflecting investor confidence in its growth trajectory and international expansion strategy.

Q4 2024 Performance Highlights

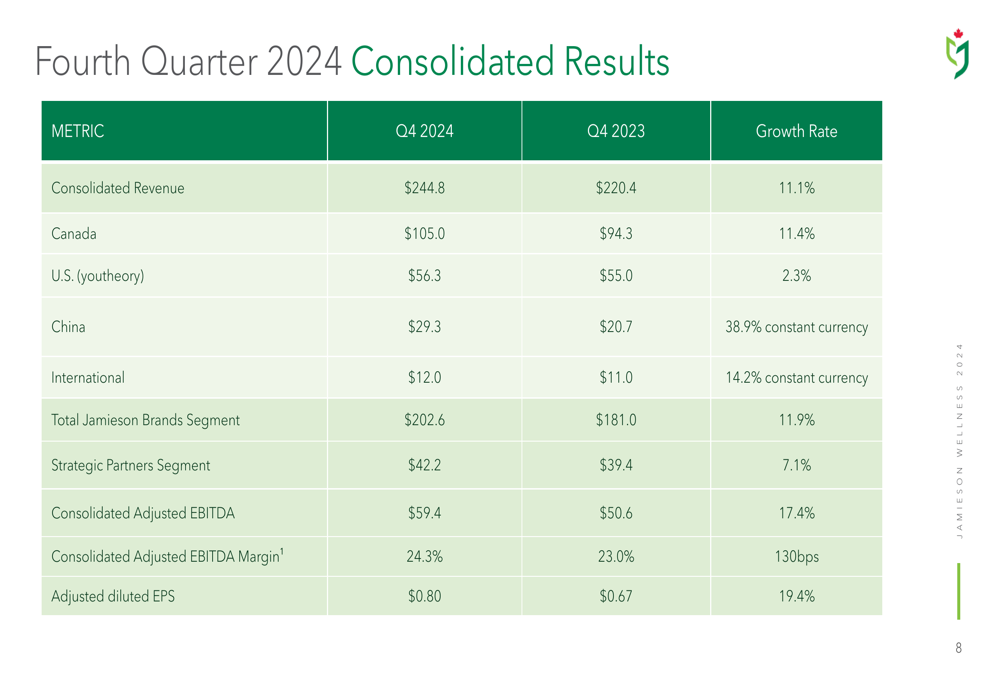

Jamieson Wellness reported consolidated revenue of $244.8 million for the fourth quarter of 2024, representing an 11.1% increase compared to the same period in 2023. The company’s adjusted EBITDA rose by 17.4% to $59.4 million, with the adjusted EBITDA margin expanding by 130 basis points to 24.3%. Adjusted diluted earnings per share increased by 19.4% to $0.80.

As shown in the following comprehensive financial summary:

The company’s cash generation also showed significant improvement, with cash from operating activities before working capital considerations reaching $41.3 million in Q4 2024, an increase of $20.9 million compared to Q4 2023. This strong cash flow performance underscores the company’s improved operating leverage and strategic management of SG&A investments.

Segment Analysis

Jamieson’s performance varied across its different geographical segments, with particularly strong results in Canada and China.

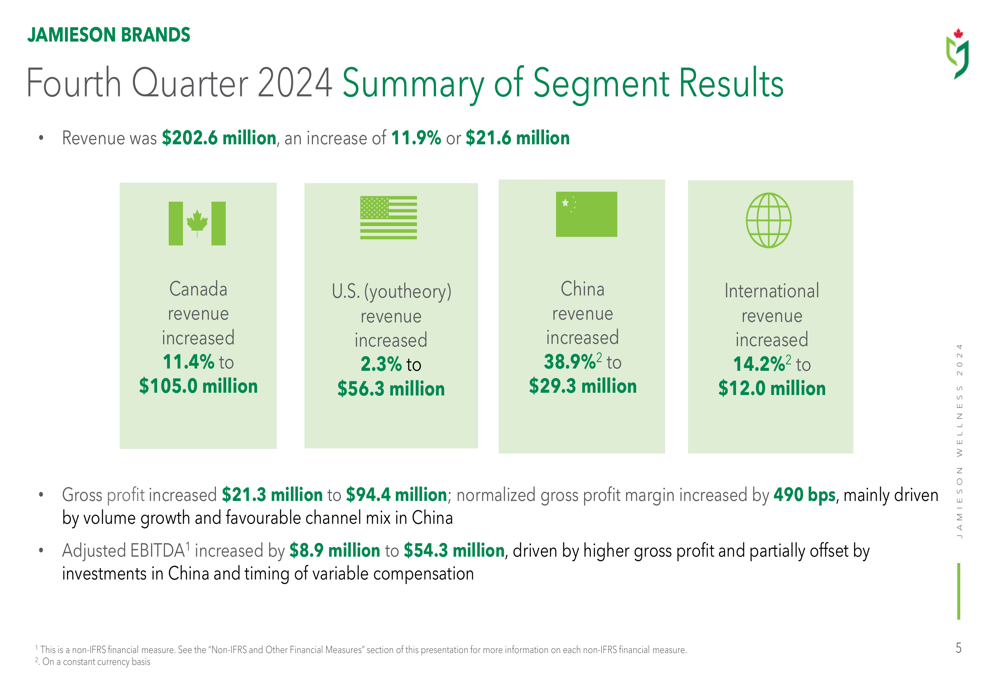

The Jamieson Brands segment, which includes operations in Canada, the United States (youtheory), China, and other international markets, saw revenue increase by 11.9% to $202.6 million in Q4 2024. Within this segment, Canada revenue grew by 11.4% to $105.0 million, driven by strong consumer demand for immune health products during the cold and flu season.

The following segment breakdown illustrates the company’s performance across its key markets:

China emerged as a standout performer with revenue growth of 38.9% in Q4 2024, reaching $29.3 million. This exceptional growth was attributed to successful 11/11 promotional campaigns that outpaced industry and channel growth among the company’s peers. For the full year 2024, China revenue grew by an impressive 77.9%, demonstrating the effectiveness of the company’s investment strategy in this key market.

The U.S. (youtheory) business showed more modest growth of 2.3% in Q4, reaching $56.3 million. While international expansion and new distribution channels for the youtheory brand grew by 20% and 37% respectively, these gains were partially offset by the timing of promotional purchases within its traditional distribution base.

The Strategic Partners segment, which represents Jamieson’s contract manufacturing business, reported revenue of $42.2 million in Q4 2024, an increase of 7.1% compared to the same period in 2023. This growth was driven by customer ordering patterns and initial shipments of new business.

2025 Guidance and Strategic Outlook

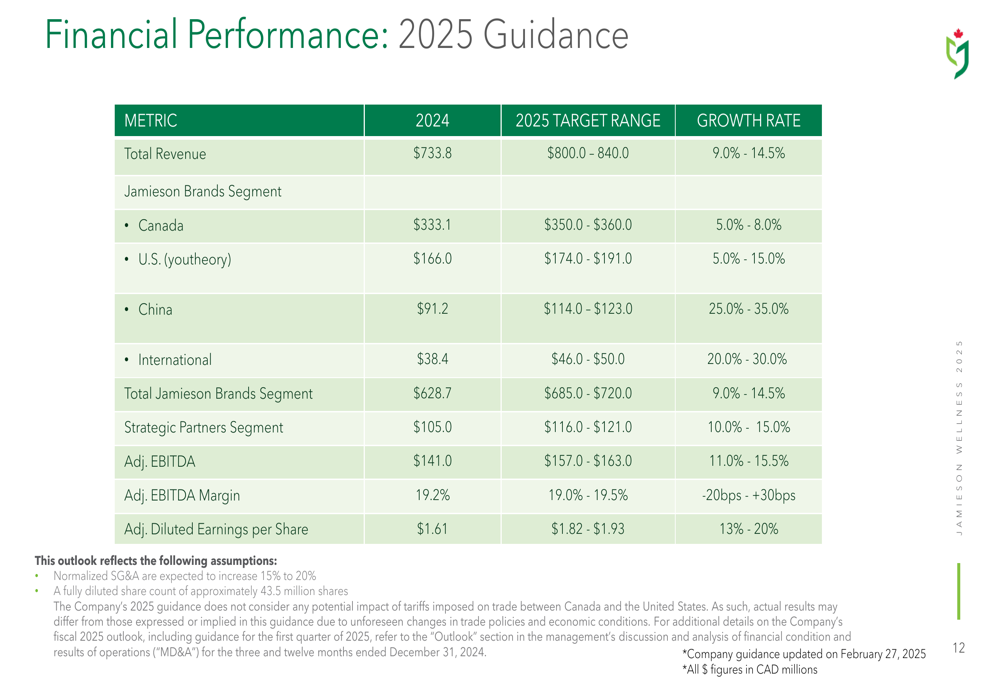

Looking ahead to 2025, Jamieson Wellness provided an optimistic outlook with growth expected across all segments. The company’s detailed guidance is presented in the following chart:

Total (EPA:TTEF) revenue for 2025 is projected to be between $800.0 million and $840.0 million, representing growth of 9.0% to 14.5% compared to 2024. China is expected to continue its strong performance with projected revenue growth of 25.0% to 35.0%, while International markets are forecast to grow by 20.0% to 30.0%.

The company anticipates adjusted EBITDA to reach between $157.0 million and $163.0 million in 2025, an increase of 11.0% to 15.5% compared to 2024. Adjusted diluted earnings per share are expected to be in the range of $1.82 to $1.93, representing growth of 13% to 20%.

It’s worth noting that the company’s 2025 guidance does not consider any potential impact of tariffs imposed on trade between Canada and the United States, which could represent a risk factor for the business.

Recent Q1 2025 Performance

The company’s recent Q1 2025 results, released after the period covered in the presentation, confirm that Jamieson’s positive momentum has continued into the new fiscal year. Q1 2025 revenue reached $146 million, a 14% increase year-over-year, exceeding the forecast of $142.44 million.

Both the Branded and Strategic Partners segments showed strong double-digit growth in Q1 2025, with increases of 13.9% and 14.9% respectively. China continued its exceptional performance, growing over 50% in the quarter, while online platforms and e-commerce channels nearly doubled their performance.

Adjusted EBITDA for Q1 2025 was $19.1 million, representing an increase of 18.6% compared to the same period in 2024. Adjusted Net Earnings reached $5.9 million, up by $2 million from the previous year.

For Q2 2025, Jamieson has forecast consolidated revenue between $185 million and $195 million, suggesting up to 5% growth, with adjusted EBITDA expected to be between $32 million and $34 million, indicating up to a 7.5% increase.

Conclusion and Market Position

Jamieson Wellness demonstrated strong performance in Q4 2024, with double-digit revenue growth and significant expansion in key international markets, particularly China. The company’s full-year 2024 results show a business with growing global reach and increasing operational efficiency.

The company’s 2025 guidance suggests continued confidence in its growth strategy, with particular emphasis on international expansion. The strong start to 2025, as evidenced by the Q1 results, validates this optimistic outlook.

Jamieson’s focus on foundational health products and innovative natural solutions appears to be resonating with consumers globally, while its strategic investments in China and other international markets are yielding significant returns. As the company continues to execute its growth strategy, investors will be watching closely to see if it can maintain this momentum throughout 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.