Powell speech takes center stage in Tuesday’s economic events

Introduction & Market Context

JPMorgan Chase & Co. (NYSE:JPM) released its first quarter 2025 financial results on April 11, showcasing strong performance across all business segments while simultaneously preparing for potential economic headwinds. The banking giant reported earnings per share of $5.07, significantly exceeding analyst expectations of $4.62, and revenue of $46 billion, surpassing the forecasted $43.9 billion.

Following the earnings release, JPMorgan's stock rose 2.76%, adding $6.26 to reach $233.37, reflecting positive investor sentiment despite management's cautious commentary about economic uncertainty. The results demonstrate the bank's continued resilience and market leadership position in an increasingly complex global economic environment.

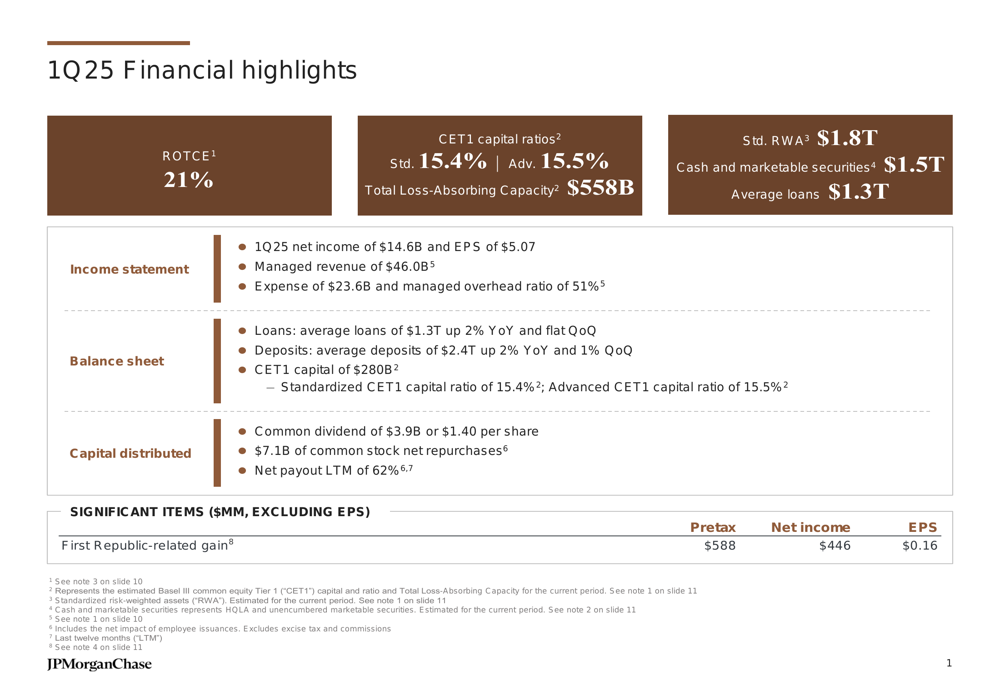

As shown in the following comprehensive financial highlights slide, JPMorgan delivered strong returns while maintaining robust capital and liquidity positions:

Quarterly Performance Highlights

JPMorgan reported net income of $14.6 billion for Q1 2025, translating to earnings per share of $5.07. The bank achieved a return on tangible common equity (ROTCE) of 21%, reflecting its ability to generate substantial returns for shareholders. Total (EPA:TTEF) managed revenue reached $46.0 billion, with expenses of $23.6 billion resulting in a managed overhead ratio of 51%.

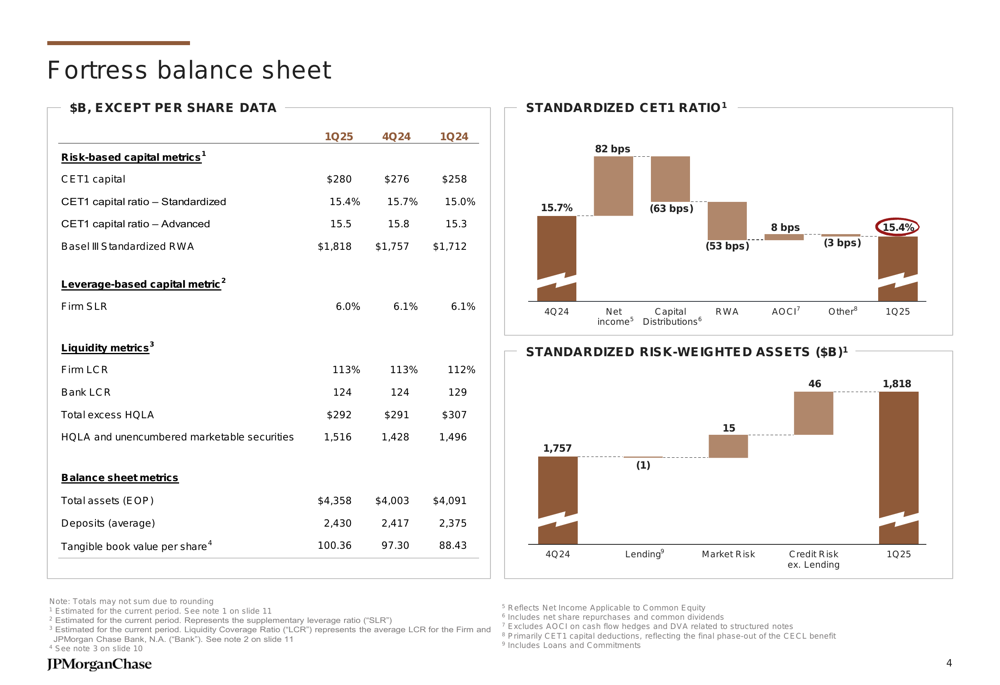

The bank's balance sheet remains strong with average loans of $1.3 trillion, up 2% year-over-year but flat quarter-over-quarter, while average deposits increased to $2.4 trillion, up 2% year-over-year and 1% sequentially. Capital levels remain well above regulatory requirements with a Standardized CET1 capital ratio of 15.4% and Advanced CET1 capital ratio of 15.5%.

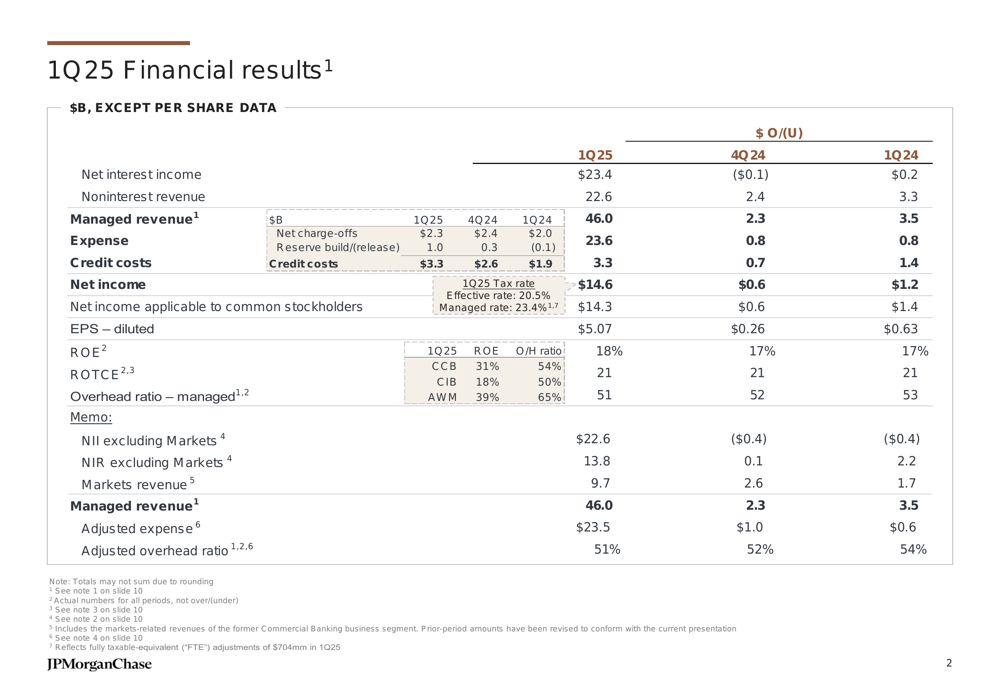

The detailed breakdown of JPMorgan's first quarter financial results shows consistent performance across key metrics:

Credit Position and Reserve Build

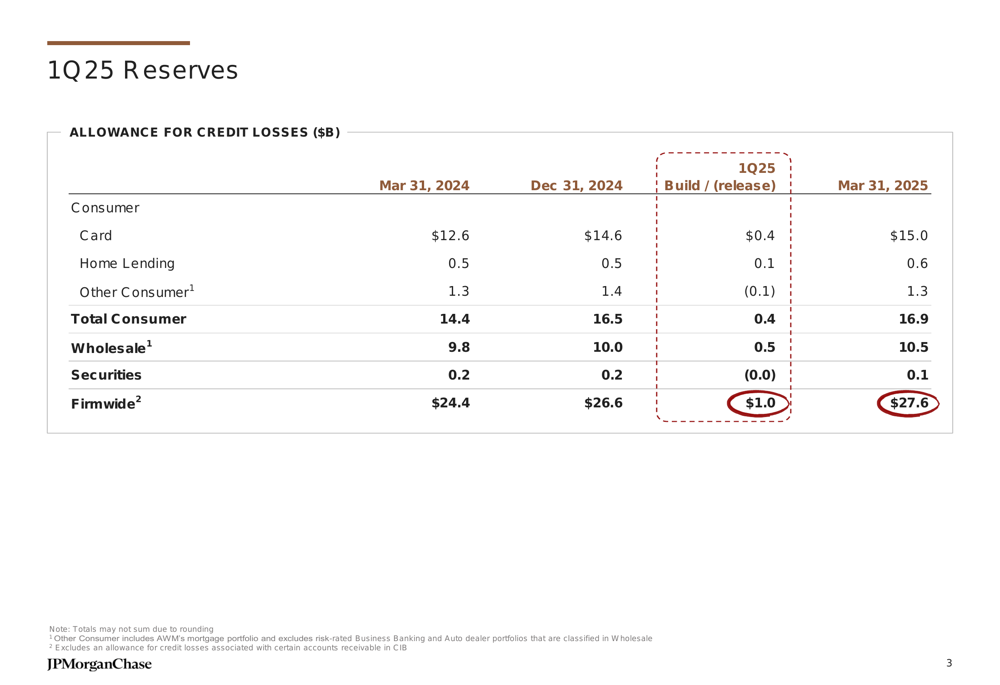

A notable aspect of JPMorgan's Q1 results was the $973 million net reserve build, bringing total allowance for credit losses to $27.6 billion. This conservative approach reflects management's assessment of elevated economic risks, with the weighted average unemployment rate embedded in their allowance increasing to 5.8% from 5.5% in the previous quarter.

Credit costs for the quarter totaled $3.3 billion, with net charge-offs of $2.3 billion. The reserve build was distributed across both consumer and wholesale portfolios, with consumer reserves increasing by $441 million and wholesale reserves by $549 million. Management emphasized that the increase in allowance was not driven by deterioration in actual credit performance, which remains largely in line with expectations.

The following slide details the composition of JPMorgan's reserves across different segments:

Segment Performance Analysis

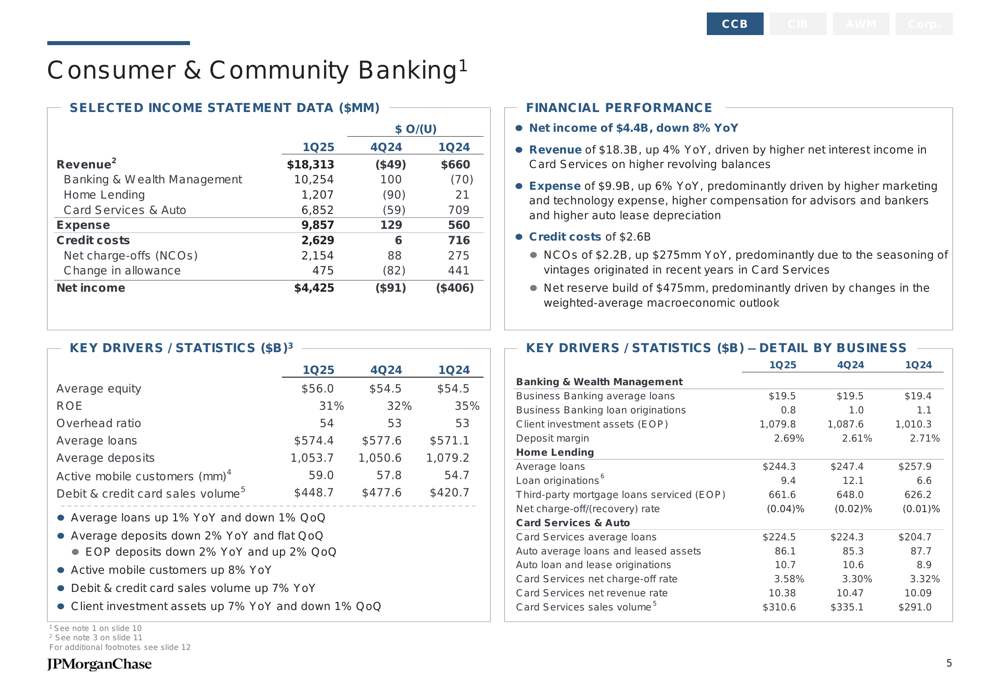

JPMorgan's Consumer & Community Banking (CCB) segment delivered strong results with revenue of $18.3 billion, up 4% year-over-year, and net income of $4.4 billion. Card Services & Auto was a standout performer with revenue up 12% year-over-year, driven by higher revolving balances in cards and increased operating lease income in auto. Card outstandings grew 10% due to strong account acquisition, while auto originations increased 20% to $10.7 billion.

The bank continues to see growth in its digital capabilities, with active mobile customers up 8% year-over-year. However, average deposits in CCB were down 2% year-over-year and flat quarter-over-quarter, reflecting competitive pressures in the deposit market.

The detailed performance metrics for the Consumer & Community Banking segment show resilience across multiple business lines:

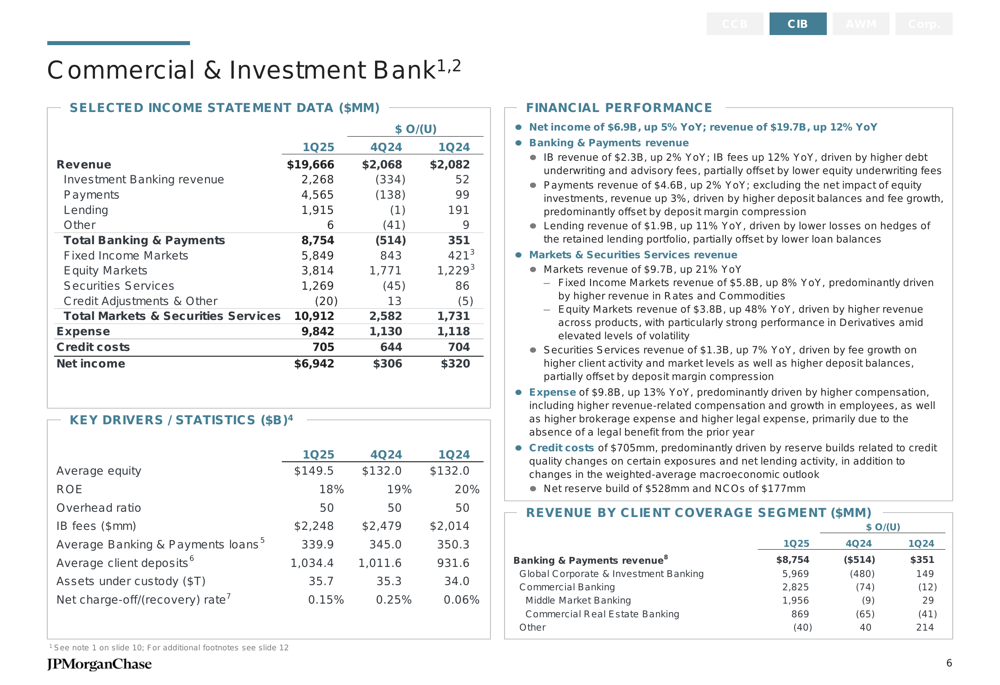

The Commercial & Investment Bank (CIB) segment reported impressive results with revenue of $19.7 billion, up 12% year-over-year, and net income of $6.9 billion. Markets revenue was particularly strong, up 21% year-over-year, with equities showing exceptional performance with a 48% increase. Investment banking fees rose 12% year-over-year, with JPMorgan maintaining its #1 ranking with a 9% wallet share.

Securities services revenue increased 7% year-over-year, driven by fee growth and higher deposit balances. Average client deposits in the CIB segment were up 11% year-over-year and 2% sequentially, reflecting increased activity across payments and securities services.

The following slide provides a comprehensive view of the Commercial & Investment Bank's performance:

Asset & Wealth Management (AWM) continued its strong trajectory with revenue of $5.7 billion, up 12% year-over-year, and net income of $1.6 billion. The segment achieved a pretax margin of 35% and saw significant growth in assets under management, which reached $4.1 trillion, up 15% year-over-year. Client assets totaled $6.0 trillion, also up 15% year-over-year, driven by continued net inflows and higher market levels.

Long-term net inflows were $54 billion for the quarter, primarily driven by equity and fixed income investments. Liquidity products saw net inflows of $36 billion, reflecting clients' preference for cash-like investments in the current environment.

Forward Outlook and Guidance

Despite the strong quarterly performance, JPMorgan's management maintained a cautious outlook for the remainder of 2025. The bank expects full-year net interest income of approximately $94.5 billion, with net interest income excluding Markets of around $90 billion. Adjusted expenses are projected to be approximately $95 billion, excluding firmwide legal expenses. The Card Services net charge-off rate is expected to be around 3.6%.

During the earnings call, Chairman and CEO Jamie Dimon emphasized the bank's preparedness for various economic scenarios, stating, "We are prepared for any environment." He highlighted concerns about economic uncertainty, particularly related to trade policy changes and potential tariff increases. CFO Jeremy Barnum noted that the "banking system being a source of strength means what it says," underscoring JPMorgan's commitment to supporting clients through economic challenges.

The outlook slide provides a concise summary of JPMorgan's financial guidance for the remainder of 2025:

Capital Position and Shareholder Returns

JPMorgan continues to deliver strong returns to shareholders while maintaining robust capital levels. During the quarter, the bank distributed $11 billion to shareholders, comprising $7.1 billion in net common share repurchases and $3.9 billion in common dividends. The quarterly dividend was increased to $1.40 per share, and the bank's net payout over the last twelve months stands at 62%.

The CET1 ratio of 15.4% remains well above regulatory requirements, providing JPMorgan with significant flexibility to navigate economic uncertainty while continuing to invest in growth opportunities and return capital to shareholders. Total loss-absorbing capacity reached $558 billion, further strengthening the bank's resilience.

Conclusion

JPMorgan's Q1 2025 financial results demonstrate the bank's ability to generate strong returns across diverse business segments while prudently preparing for potential economic challenges. The significant reserve build reflects management's cautious approach to an uncertain economic environment, particularly regarding trade policies and inflation concerns.

With robust capital and liquidity positions, JPMorgan remains well-positioned to weather economic headwinds while continuing to support clients and deliver value to shareholders. However, investors should monitor the evolving economic situation, particularly regarding trade policies and their potential impact on corporate activity and consumer spending patterns.

The bank's performance continues to set the standard for the financial services industry, with its diversified business model providing resilience against various economic scenarios. As economic uncertainty persists, JPMorgan's conservative approach to reserves and capital management may prove to be a significant competitive advantage in navigating the challenges ahead.

Full Presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.