Novo Nordisk, Eli Lilly fall after Trump comments on weight loss drug pricing

Introduction & Market Context

Jyske Bank (CPH:JYSK) presented its Q2 2025 results on August 19, 2025, highlighting an improved outlook for the full year despite challenges from lower interest rates. The Danish bank now expects net profit to reach the upper end of its previously announced DKK 3.8-4.6 billion range for 2025, supported by strong fee income growth, improving customer satisfaction, and solid credit quality.

The presentation comes after Jyske Bank’s stock closed at DKK 682.50 on August 18, representing a 1.16% decline. Despite this recent dip, the bank’s shares remain closer to their 52-week high of DKK 696 than their low of DKK 450, reflecting overall positive market sentiment toward the company’s performance.

Quarterly Performance Highlights

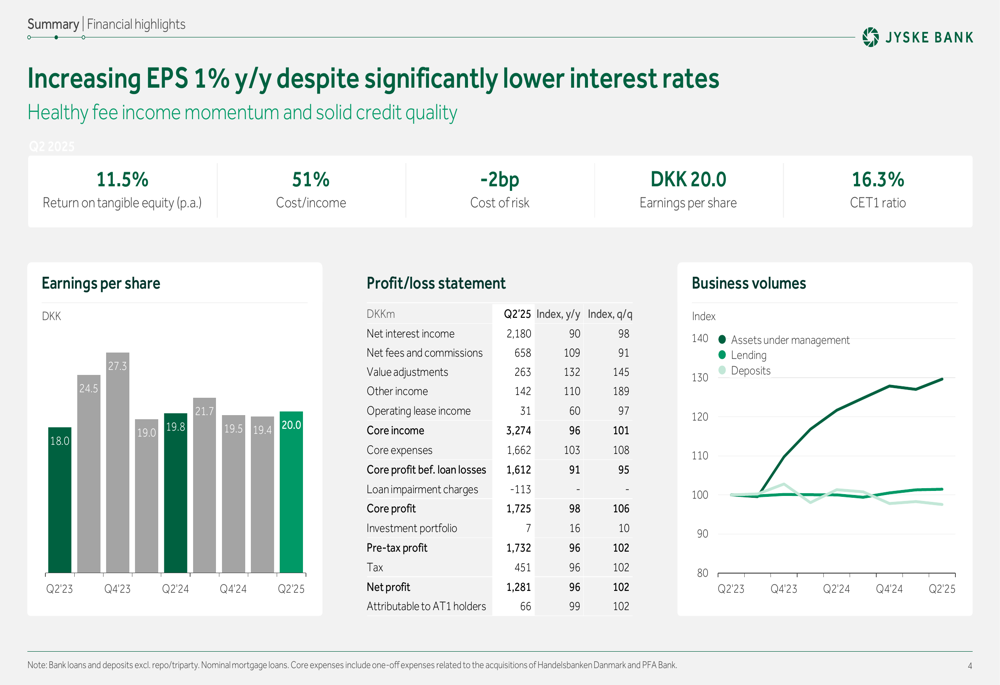

Jyske Bank reported earnings per share of DKK 20.0 in Q2 2025, up 1% year-over-year despite significantly lower policy rates. The bank achieved a return on tangible equity of 11.5% and maintained a cost/income ratio of 51%. Net profit for the quarter reached DKK 1,281 million, supported by strong fee income and negative loan impairment charges.

As shown in the following comprehensive financial summary:

Net interest income totaled DKK 2,180 million in Q2 2025, down 2% quarter-over-quarter due to lower policy rates and funding costs related to new issuances. However, this was partially offset by higher lending margins and resilient deposit margins. The bank’s ability to maintain relatively stable interest income despite the challenging rate environment demonstrates effective balance sheet management.

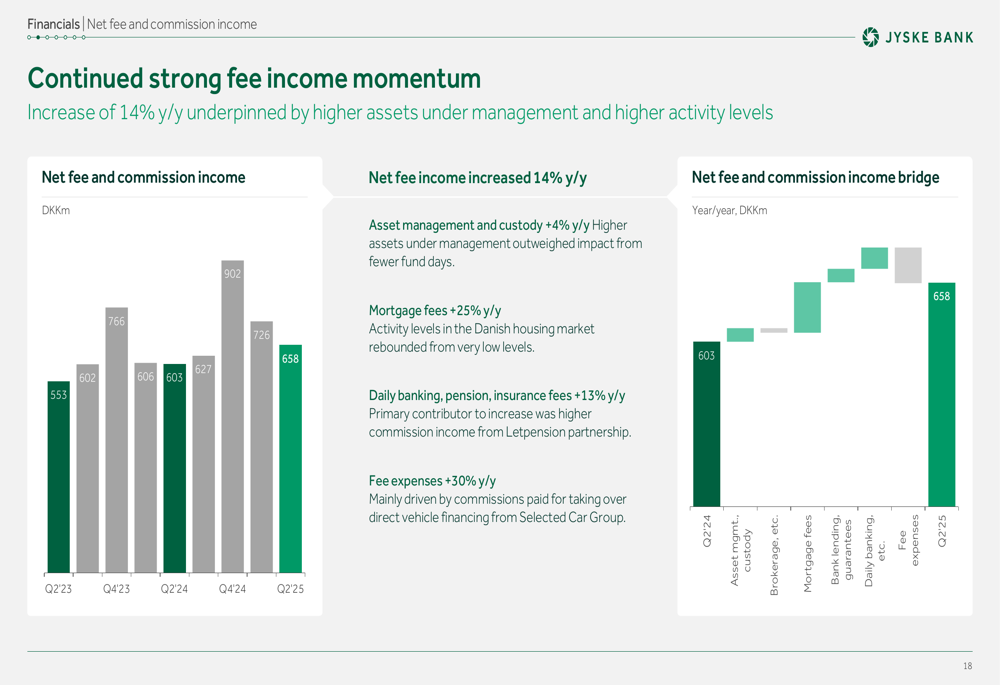

Net fee and commission income showed particularly strong performance, increasing 14% year-over-year to DKK 658 million. This growth was underpinned by higher assets under management and increased activity levels across various business segments.

As illustrated in the following fee income breakdown:

The bank’s core income totaled DKK 3,274 million for the quarter, while core expenses amounted to DKK 1,662 million. Notably, credit quality remained solid with loan impairment reversals of DKK 113 million (-2bp cost of risk), reflecting the bank’s conservative risk management approach.

Customer Satisfaction & Business Growth

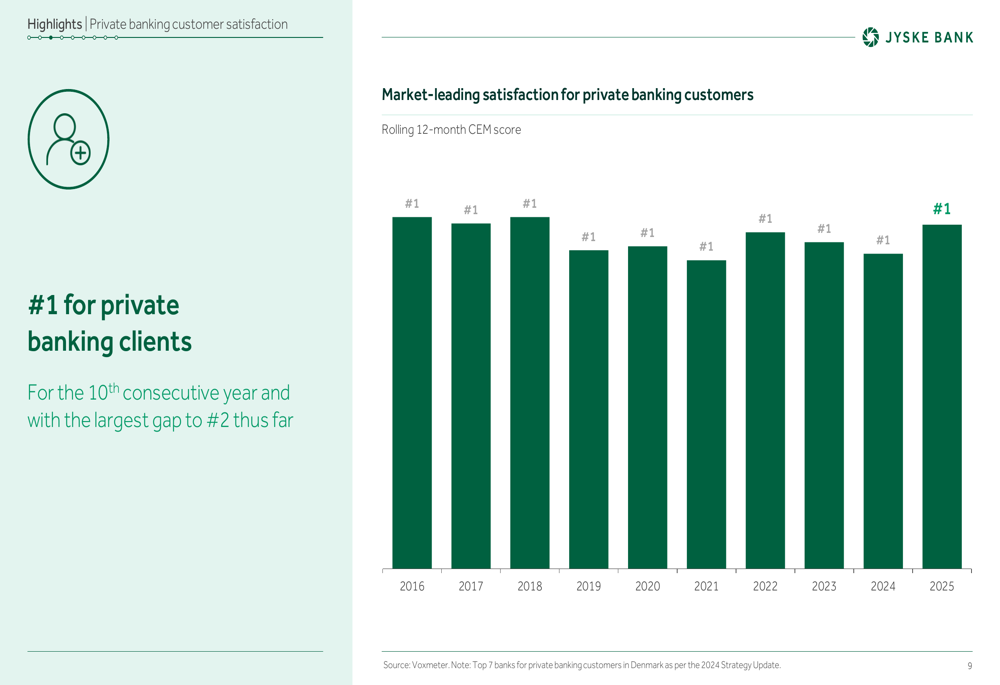

Jyske Bank reported significant improvements in customer satisfaction across multiple segments. The bank achieved market-leading satisfaction for corporate clients with 20+ employees and maintained its #1 position for private banking clients for the tenth consecutive year. Personal customer satisfaction also showed strong improvement.

The following chart illustrates Jyske Bank’s leadership in private banking customer satisfaction:

Assets under management reached a new all-time high, exceeding DKK 300 billion and representing 10% annual growth over the past decade. This resilient performance in asset management has been a key driver of fee income growth and helps diversify the bank’s revenue streams beyond interest income.

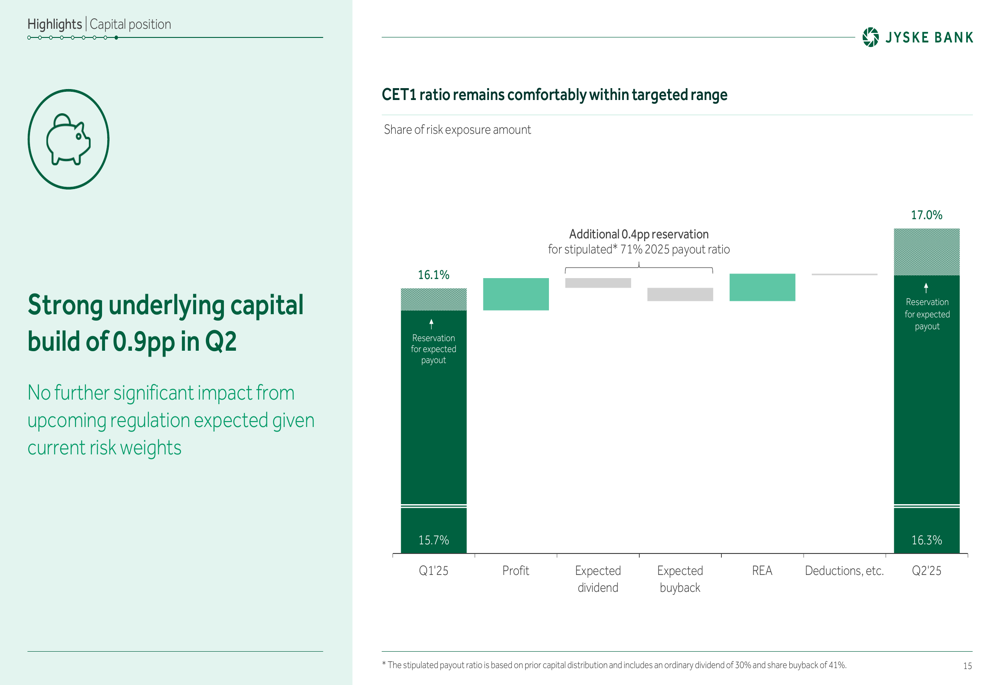

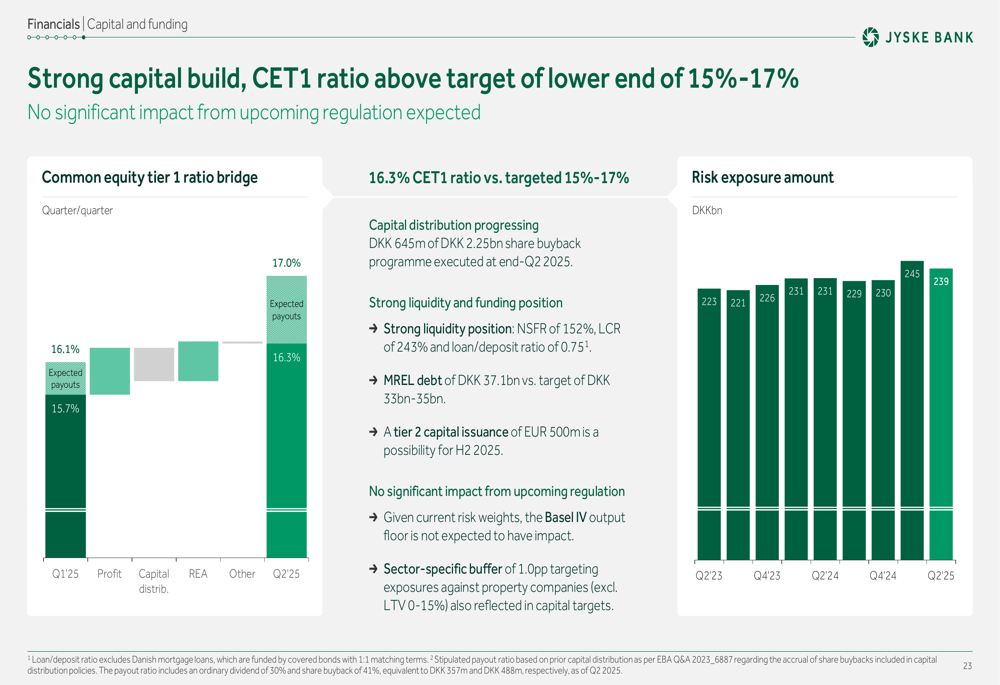

As shown in the following capital position analysis, Jyske Bank maintained a strong capital build of 0.9 percentage points in Q2:

The bank’s CET1 ratio stood at 16.3%, comfortably within its target range of 15-17%. This strong capital position supports the bank’s commitment to shareholder returns through both dividends and share buybacks, with a stated dividend payout ratio of 30%.

Detailed Financial Analysis

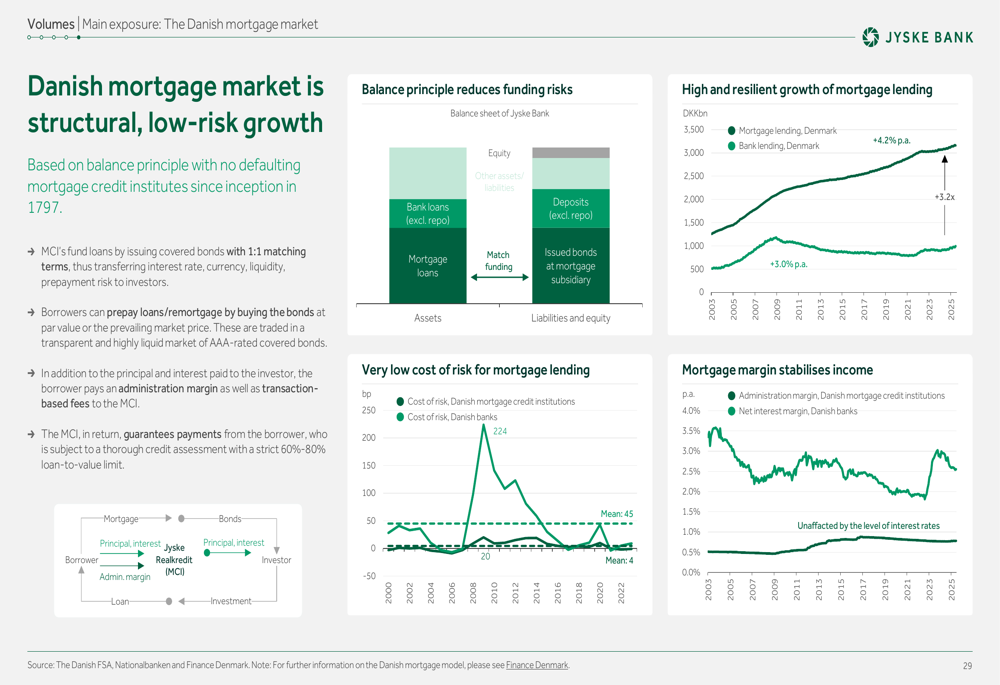

Jyske Bank’s lending portfolio remains heavily weighted toward low-risk mortgage exposures, which constitute 75% of total lending. The bank emphasized the structural advantages of the Danish mortgage market, which has not experienced any defaulting mortgage credit institutes since its inception in 1797.

The following slide highlights the key characteristics of the Danish mortgage market:

The bank’s deposit margin showed strong resilience despite the lower interest rate environment, supported by targeted initiatives including lowered deposit rates for transaction/savings accounts, normalized share of time deposits, and reduced preferential deposit rates.

Loan impairment charges remained at very low levels, with post-model adjustments of DKK 1,877 million (35bp), which is more than four times normalized loan losses. Stage 3 exposures declined 0.1 percentage points quarter-over-quarter to 1.0% of total exposures, further underscoring the bank’s solid credit quality.

The bank’s capital and funding analysis reveals a strong liquidity position and continued capital distribution to shareholders:

Forward-Looking Statements

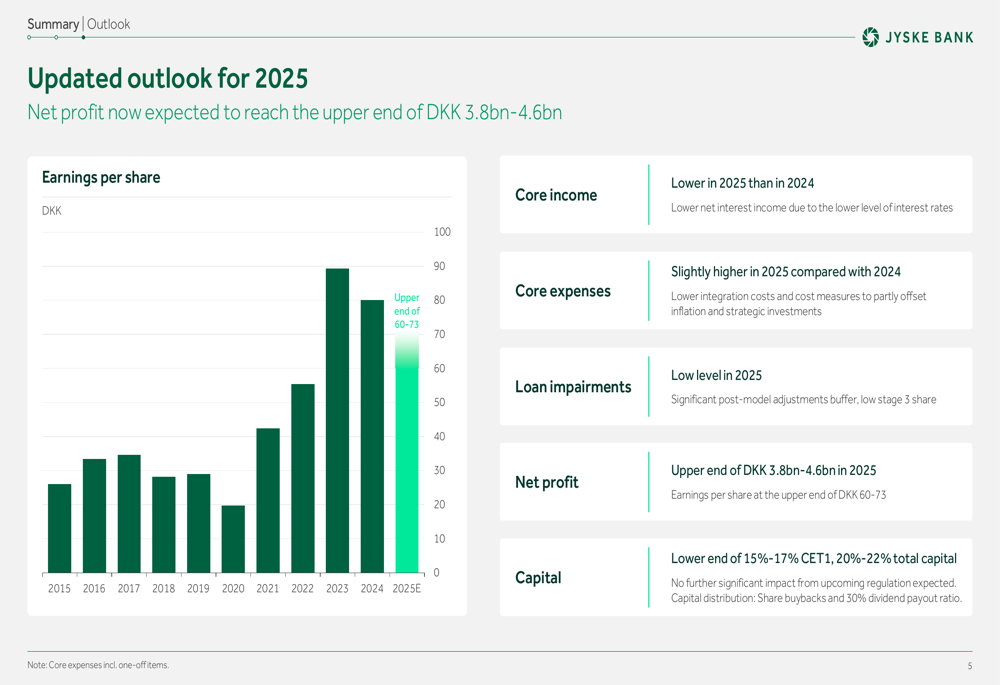

Jyske Bank updated its outlook for 2025, now expecting net profit to reach the upper end of the previously announced DKK 3.8-4.6 billion range. This corresponds to earnings per share at the upper end of DKK 60-73 for the full year.

The improved outlook comes despite expectations for lower core income in 2025 compared to 2024 due to the lower level of interest rates. Core expenses are projected to be slightly higher in 2025 compared to 2024, with lower integration costs and cost measures partly offsetting inflation and strategic investments.

As illustrated in the updated outlook slide:

The bank expects loan impairments to remain at low levels in 2025, supported by a significant post-model adjustments buffer and low stage 3 share. Capital targets remain unchanged at the lower end of 15%-17% for CET1 ratio and 20%-22% for total capital.

Regarding external factors, Jyske Bank noted that Denmark is well-positioned to handle the implications of a potential trade war, with US tariffs of 15% having a direct impact on only 3% of Danish exports. The bank cited estimates from Nationalbanken that a 25% tariff on all US exports, including services, would have a long-term Danish GNI impact of just 0.4%.

Jyske Bank’s Q2 2025 presentation demonstrates the bank’s ability to navigate a challenging interest rate environment while improving customer satisfaction and maintaining solid capital and credit positions. The raised outlook for 2025 reflects management’s confidence in the bank’s diversified revenue streams and operational efficiency.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.