United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Kearny Financial Corp (NASDAQ:KRNY) presented its third quarter fiscal year 2025 results on April 24, 2025, highlighting stable financial performance amid a challenging banking environment. The New Jersey-based financial institution, founded in 1884, operates 43 full-service branches across New Jersey and New York City and ranks among the top 10 financial institutions in New Jersey with $7.7 billion in assets.

The stock closed at $6.16 on the presentation day, up 3% following the release, reflecting positive market reception to the quarterly results.

Quarterly Performance Highlights

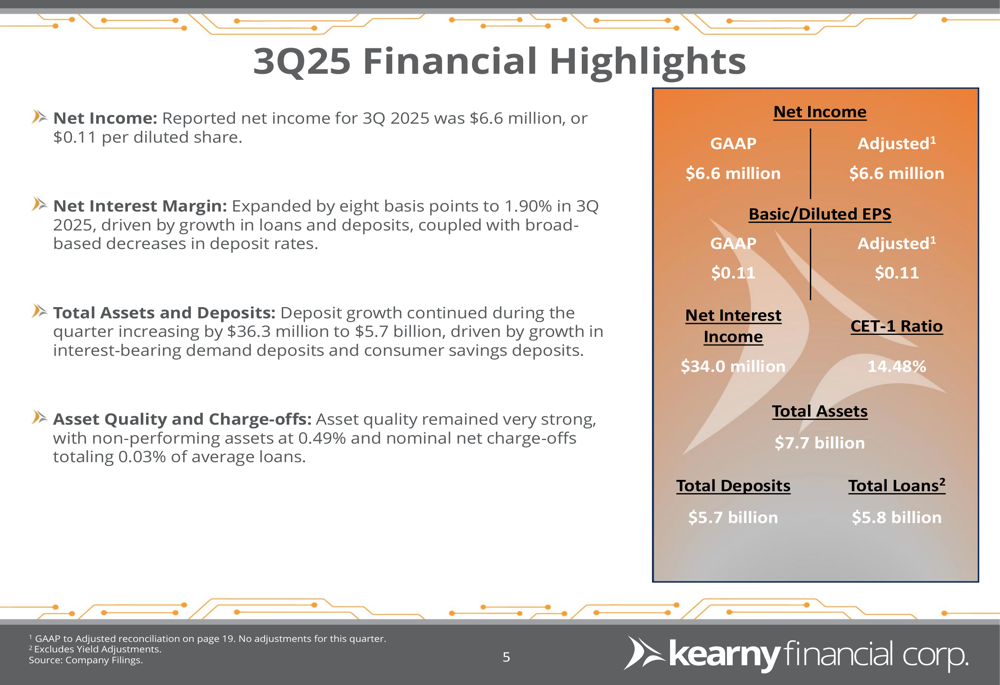

For the third quarter of fiscal year 2025, Kearny Financial reported net income of $6.6 million, translating to earnings per share of $0.11 on both a GAAP and adjusted basis. The company’s net interest income stood at $34.0 million, with the net interest margin expanding by 8 basis points to 1.90% compared to the previous quarter.

As shown in the following quarterly financial highlights:

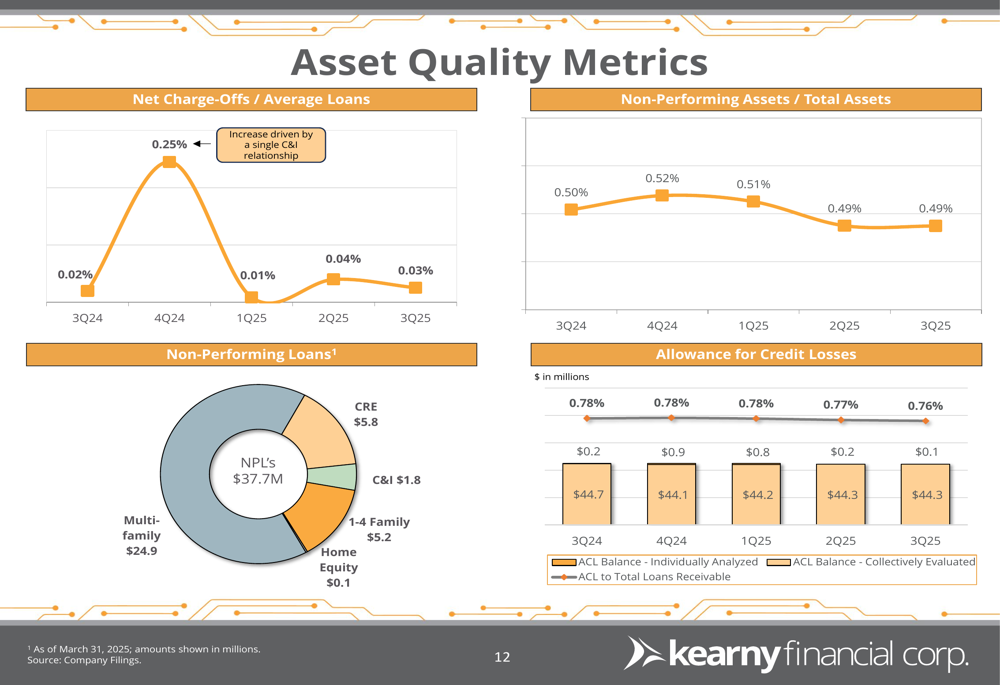

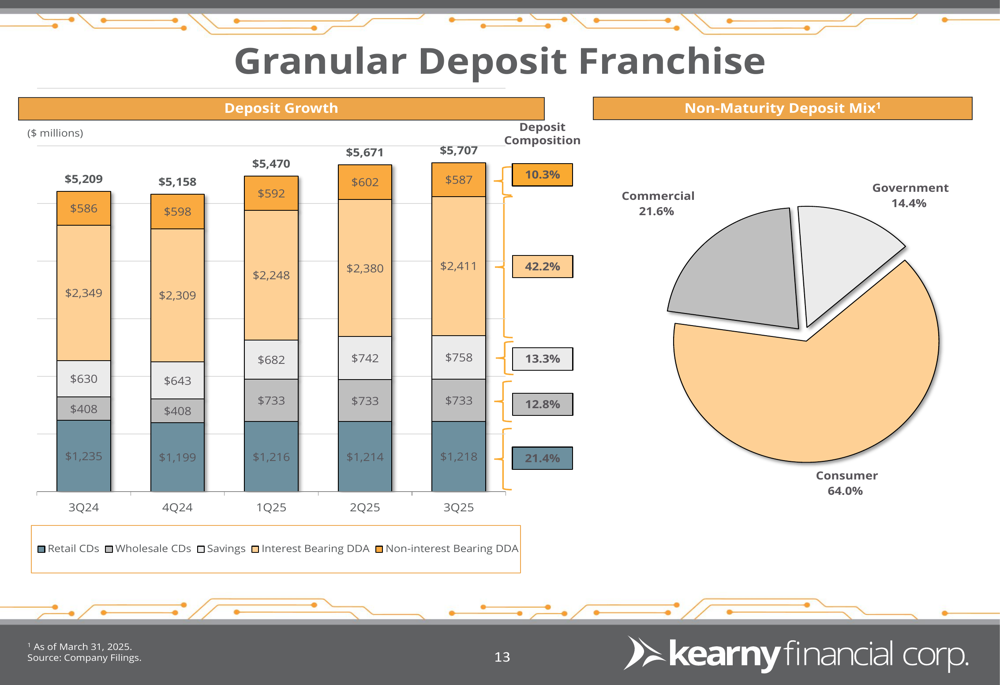

The bank maintained strong asset quality metrics with non-performing assets at 0.49% of total assets and nominal net charge-offs at just 0.03% of average loans. Total (EPA:TTEF) assets reached $7.7 billion, with total deposits of $5.7 billion and total loans of $5.8 billion. The company also reported continued deposit growth, with an increase of $36.3 million during the quarter.

Loan Portfolio and Asset Quality

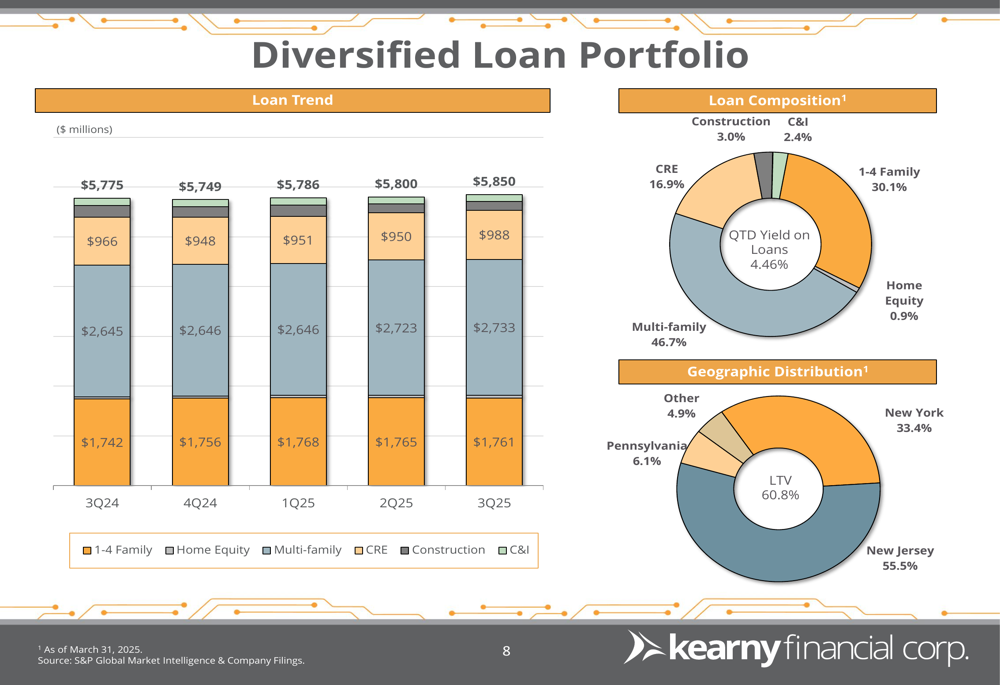

Kearny Financial maintains a diversified loan portfolio with a strategic focus on multi-family and residential lending. As of Q3 FY2025, multi-family loans represented 46.7% of the total portfolio, followed by 1-4 family residential loans at 30.1%, commercial real estate at 16.9%, construction loans at 3.0%, and commercial and industrial loans at 2.4%.

The company’s loan portfolio composition and geographic distribution is illustrated here:

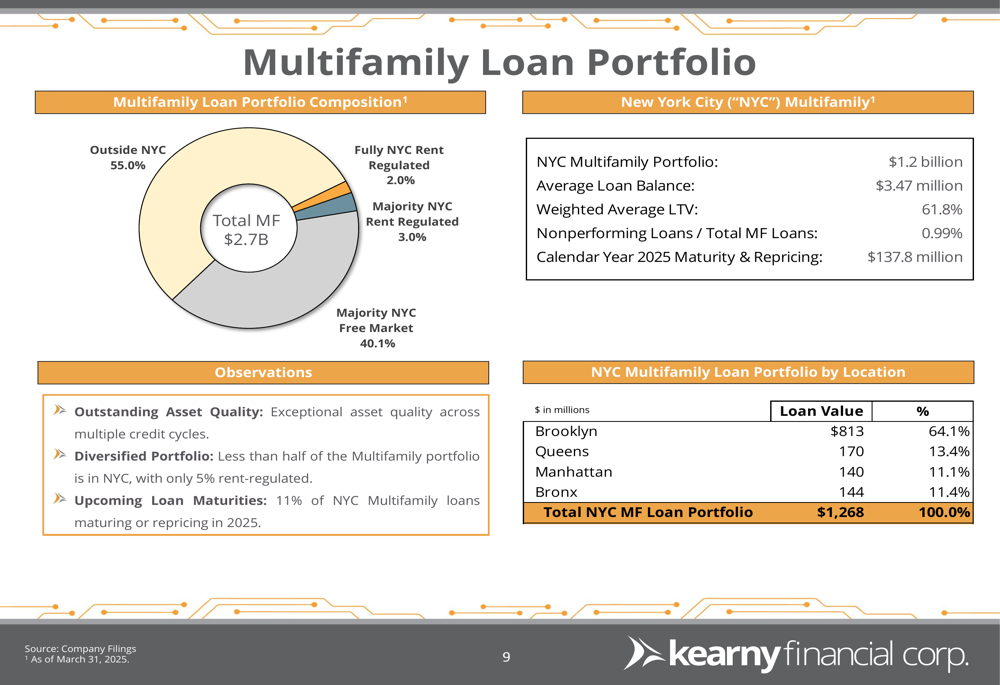

The bank’s multifamily loan portfolio, which constitutes the largest segment, is well-diversified with 55% outside of New York City. Within the NYC portfolio, the majority (40.1%) consists of free market properties rather than rent-regulated units, which helps mitigate regulatory risk.

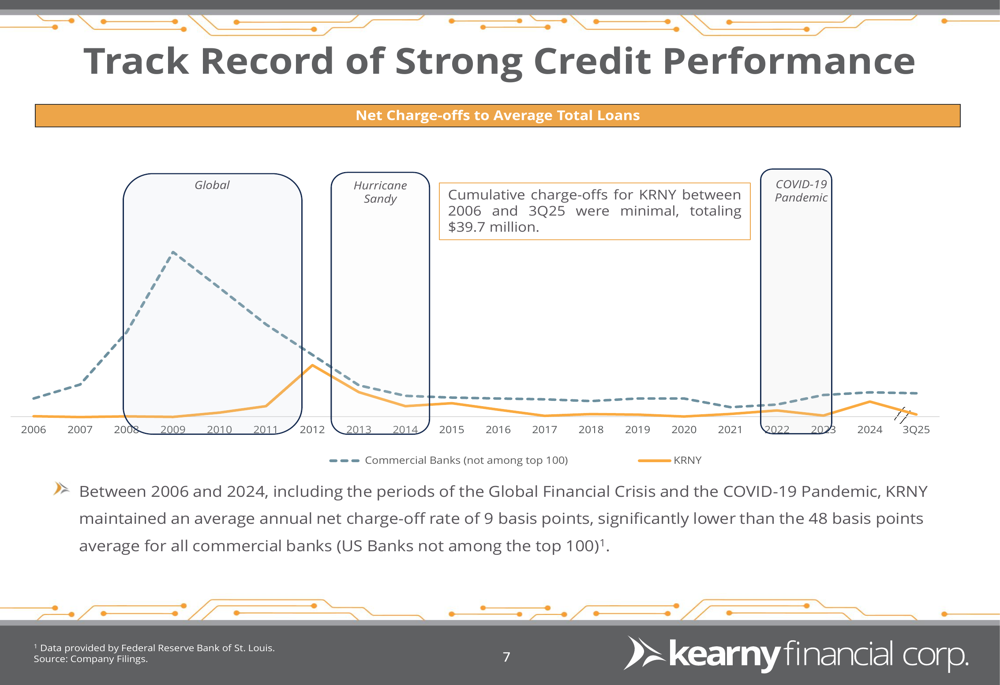

Kearny Financial has maintained an impressive track record of credit performance through various economic cycles. The company’s average annual net charge-off rate of 9 basis points significantly outperforms the industry average of 48 basis points for all commercial banks, demonstrating its conservative underwriting approach.

Asset quality metrics remained strong in Q3 FY2025, with non-performing assets stable at 0.49% of total assets and minimal net charge-offs:

Deposit Growth and Liquidity

The bank reported continued deposit growth with total deposits reaching $5.7 billion, an increase of $36.3 million during the quarter. Kearny maintains a granular deposit base with 64.0% of deposits coming from consumer accounts, 21.6% from commercial accounts, and 14.4% from government accounts.

The company’s deposit franchise is well-positioned with a diversified mix of retail and wholesale funding sources. Retail deposits totaled $4.42 billion across 106,827 accounts, with an average balance per account of $41,372, indicating a stable and granular deposit base.

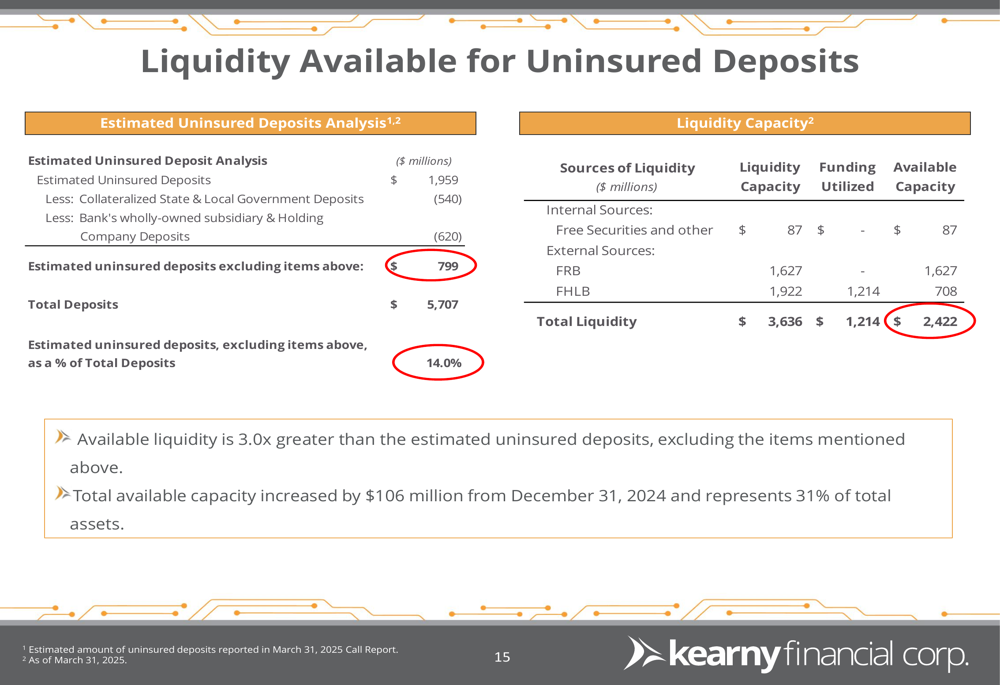

Kearny Financial maintains strong liquidity to cover uninsured deposits, with total available liquidity of $3.64 billion against estimated uninsured deposits (excluding collateralized and related-party deposits) of $799 million, representing just 14.0% of total deposits.

Capital Position and Efficiency

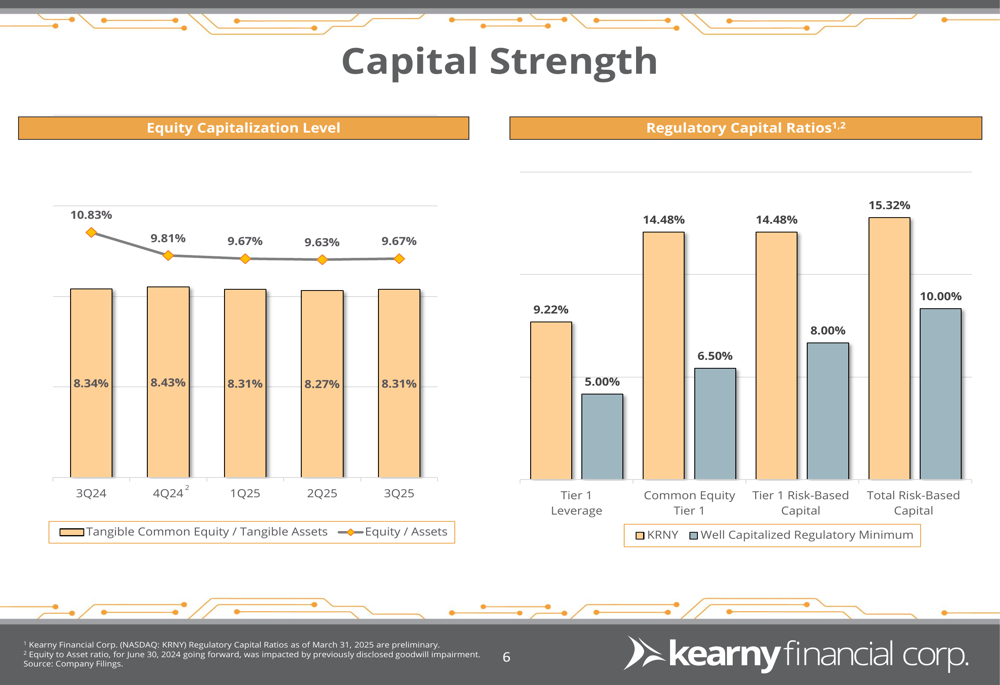

Kearny Financial maintains robust capital levels well above regulatory requirements. As of March 31, 2025, the Common Equity Tier 1 (CET-1) ratio stood at 14.48%, while the Total Risk-Based Capital ratio was 15.32%, significantly exceeding the well-capitalized regulatory minimums of 6.50% and 10.00%, respectively.

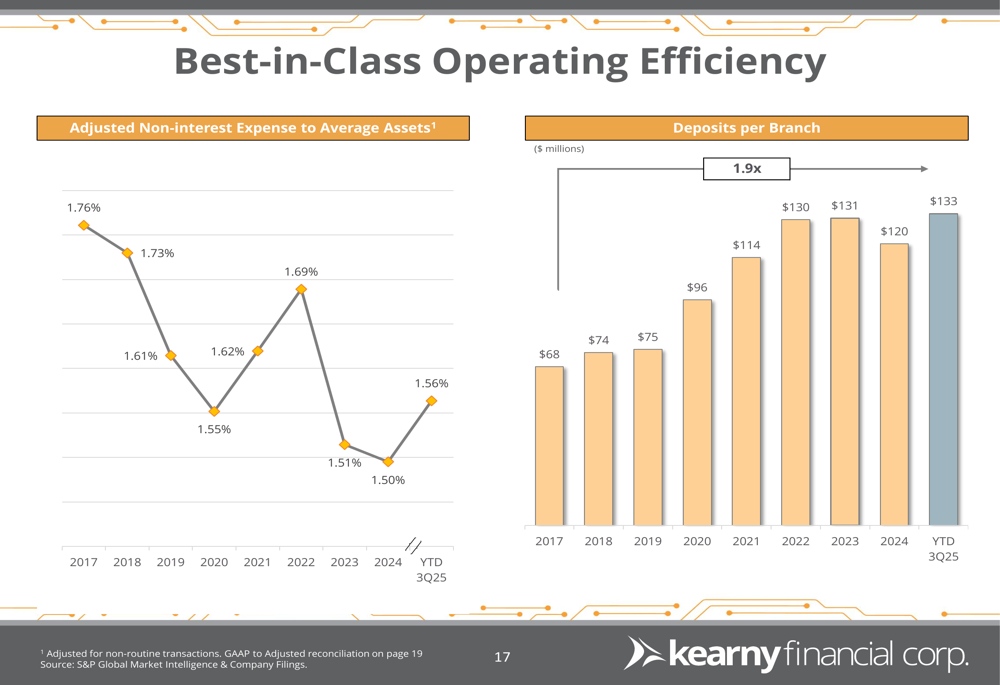

The company continues to demonstrate strong operational efficiency with adjusted non-interest expense to average assets at 1.56% for YTD Q3 FY2025, comparing favorably to historical levels. Deposits per branch have increased to $133 million, representing a 1.9x increase from previous years, highlighting improved operational leverage.

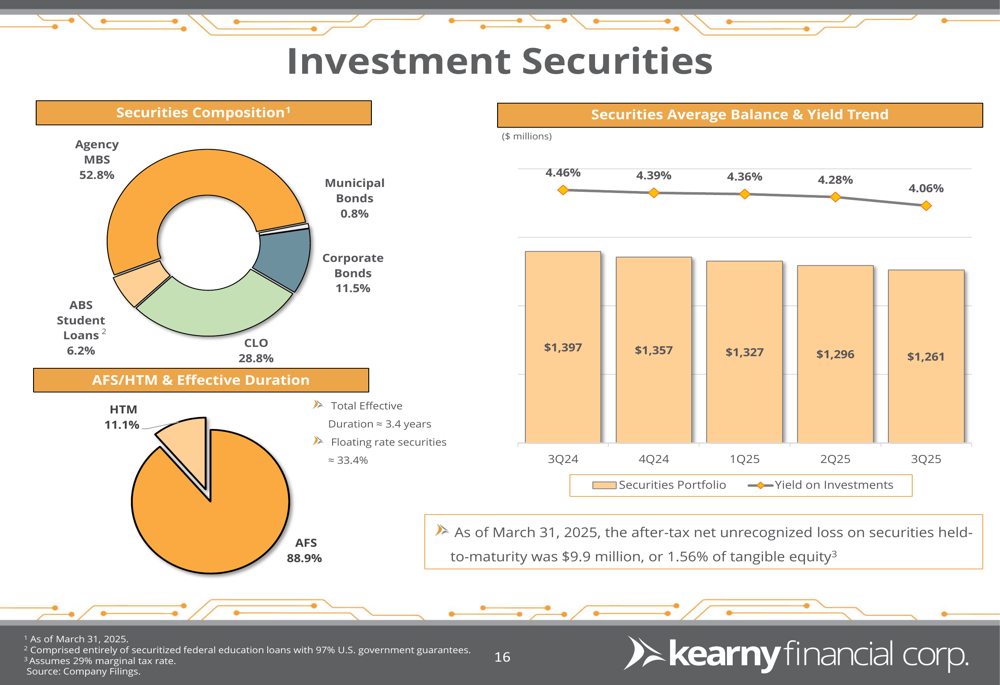

The investment securities portfolio, totaling $1.26 billion, is well-diversified with Agency MBS accounting for 52.8%, CLOs at 28.8%, corporate bonds at 11.5%, and other securities making up the remainder. The portfolio has an effective duration of approximately 3.4 years with 33.4% in floating rate securities, providing some protection against interest rate volatility.

Forward-Looking Statements

Looking ahead, Kearny Financial is positioned to navigate the current banking environment with its strong capital base, diversified loan portfolio, and granular deposit franchise. The company’s conservative underwriting culture, which includes comprehensive CRE and multifamily underwriting standards with disciplined loan-to-value ratios and debt service coverage requirements, should continue to support asset quality.

The bank’s historical performance through economic cycles, including the Global Financial Crisis and COVID-19 pandemic, demonstrates resilience and effective risk management. With capital ratios well above regulatory requirements and ample liquidity, Kearny Financial appears well-positioned to manage potential economic headwinds while pursuing strategic growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.