Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Introduction & Market Context

Kearny Financial Corp (NASDAQ:KRNY) released its fourth-quarter fiscal 2025 investor presentation on July 24, 2025, highlighting steady earnings and improved net interest margin despite a challenging interest rate environment. The New Jersey-based bank, which operates 43 branches across 12 counties in New Jersey and New York City, reported stable net income while achieving notable expansion in pre-tax, pre-provision earnings.

Shares of Kearny Financial were trading down 3.21% at $6.54 following the presentation, as investors digested the results against the backdrop of the company’s 52-week range of $5.45 to $8.59.

Quarterly Performance Highlights

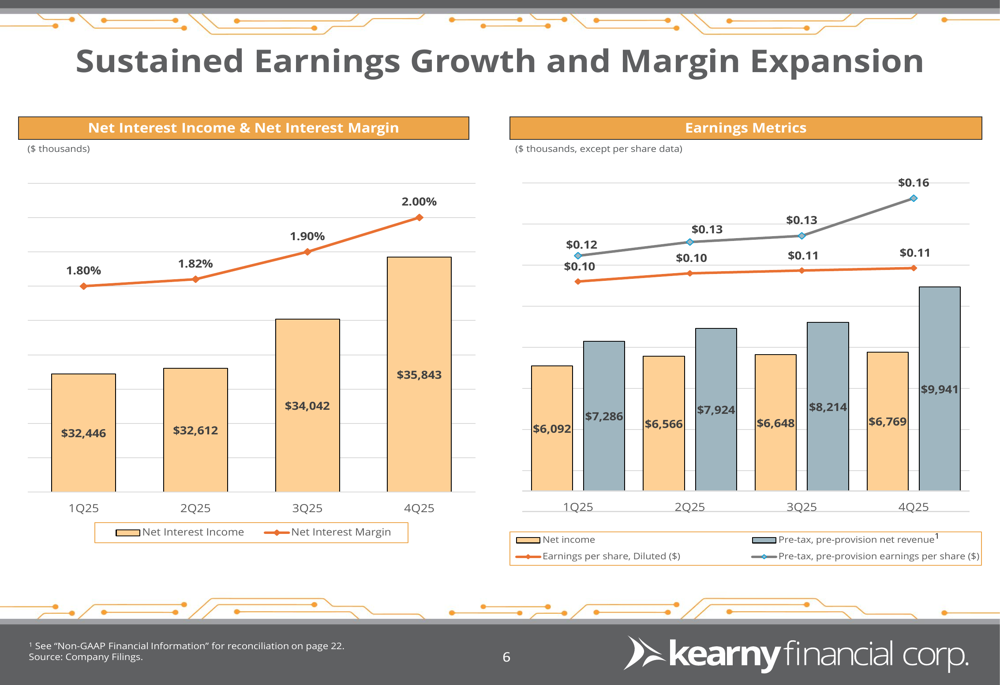

Kearny Financial reported net income of $6.8 million for Q4 FY2025, with earnings per share holding steady at $0.11. More notably, pre-tax, pre-provision earnings per share increased by 23% to $0.16, signaling underlying operational improvements.

The bank’s net interest income grew 5.3% as its net interest margin (NIM) improved by 10 basis points to 2.00%, continuing a positive trend throughout the fiscal year. Non-interest income also showed strength, rising 9.4% during the quarter.

As shown in the following chart of quarterly earnings metrics and margin expansion:

The company maintained strong capital levels, with a Common Equity Tier 1 (CET-1) ratio of 14.49%, well above regulatory requirements. Total (EPA:TTEF) assets stood at $7.7 billion, with loans at $5.8 billion and deposits at $5.7 billion as of quarter-end.

Detailed Financial Analysis

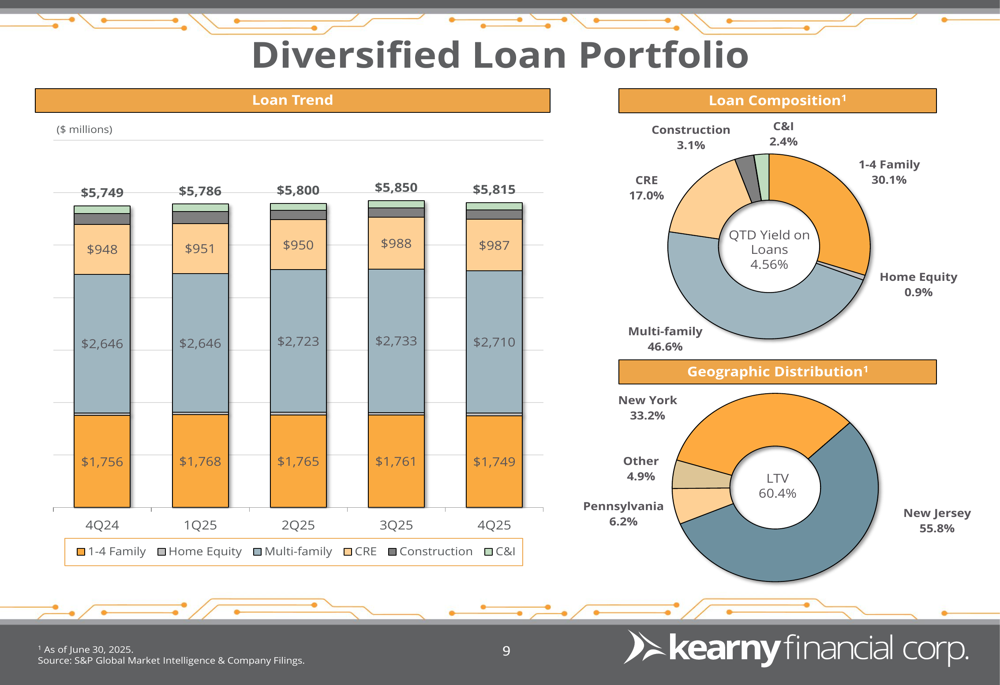

Kearny’s loan portfolio showed modest growth, increasing from $5.75 billion in Q4 FY2024 to $5.82 billion in Q4 FY2025. The portfolio remains diversified, with a significant concentration in multifamily loans (46.6%), followed by 1-4 family residential loans (30.1%), commercial real estate (17.0%), and smaller allocations to commercial and industrial loans and home equity lines.

The geographic distribution of the loan portfolio is illustrated below:

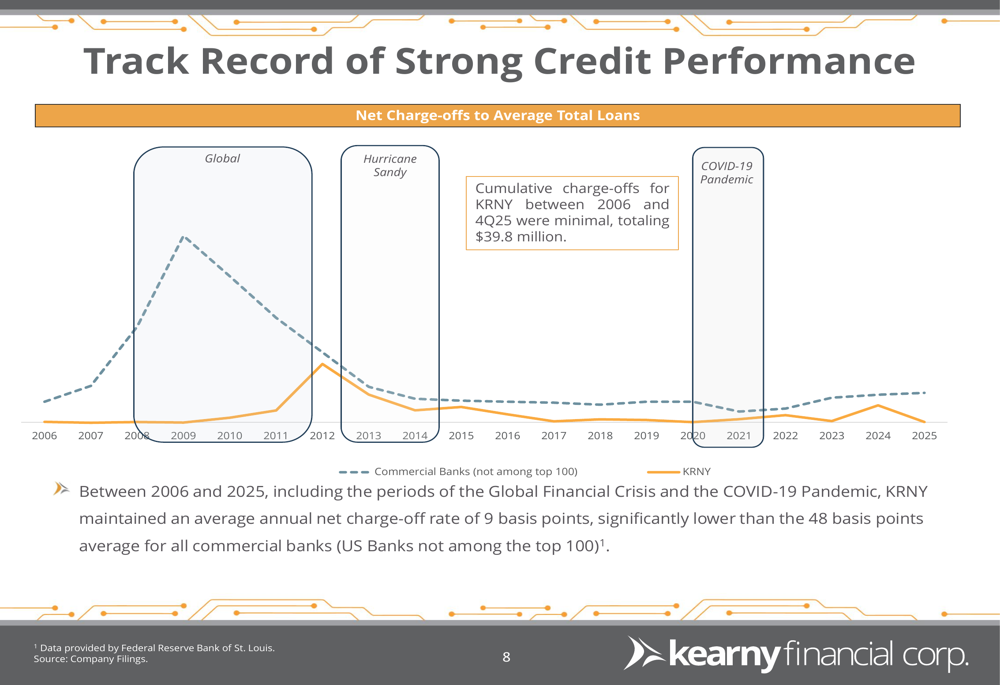

Asset quality remained strong, with net charge-offs less than 0.01% of average loans for the quarter. This continues Kearny’s historical trend of exceptional credit performance, with the bank maintaining an average annual net charge-off rate of just 9 basis points since 2006, significantly outperforming the 48 basis point average for comparable commercial banks.

This long-term credit performance is demonstrated in the following chart:

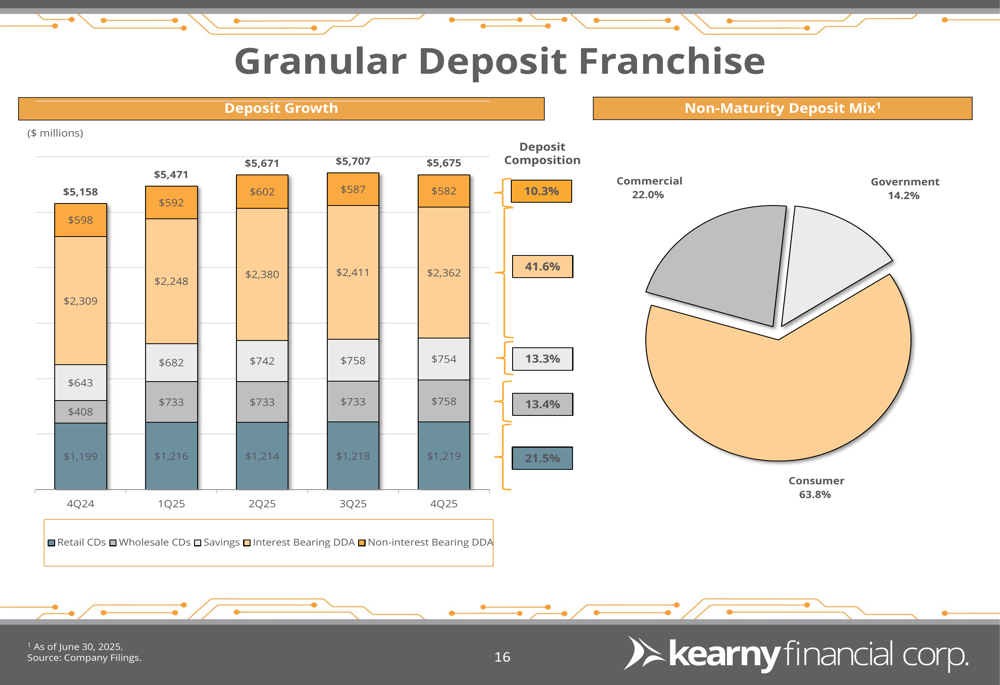

The company’s deposit base grew from $5.16 billion in Q4 FY2024 to $5.68 billion in Q4 FY2025, reflecting a healthy funding environment. The deposit mix remains granular and well-diversified, with consumer deposits representing 63.8% of non-maturity deposits.

Strategic Initiatives

Kearny highlighted several strategic initiatives aimed at improving efficiency and profitability. The company received regulatory approval to consolidate three branches, continuing its focus on optimizing its physical footprint while maintaining strong deposits per branch, which have increased from $68 million in 2017 to $132 million in Q4 2025.

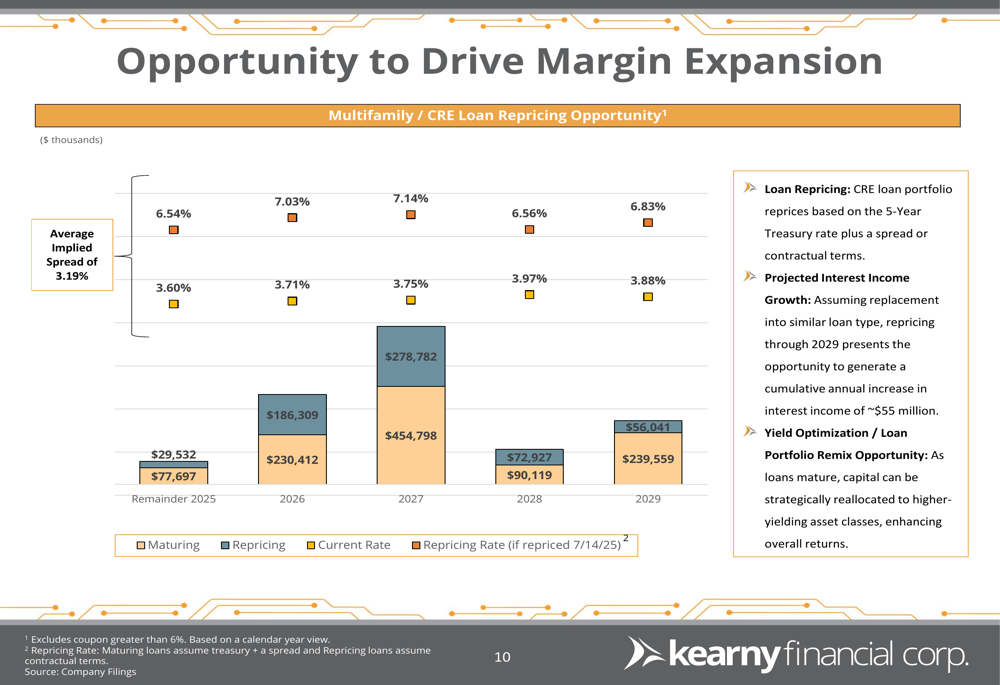

Perhaps most significantly, the presentation emphasized substantial opportunities for margin expansion through loan repricing. With a large portion of the multifamily and commercial real estate portfolio scheduled to reprice in the coming years, management projects a potential cumulative annual increase in interest income of approximately $55 million.

The loan repricing opportunity is illustrated in the following chart:

The company also highlighted its conservative underwriting culture, which includes comprehensive stress testing, stringent loan-to-value and debt service coverage ratio standards, and a proactive workout process for troubled assets.

Forward-Looking Statements

Looking ahead, Kearny is positioned to benefit from its strong capital position and the upcoming repricing of its loan portfolio. The bank’s tangible book value per share stands at $9.77, compared to its current trading price of $6.54, suggesting potential value for investors.

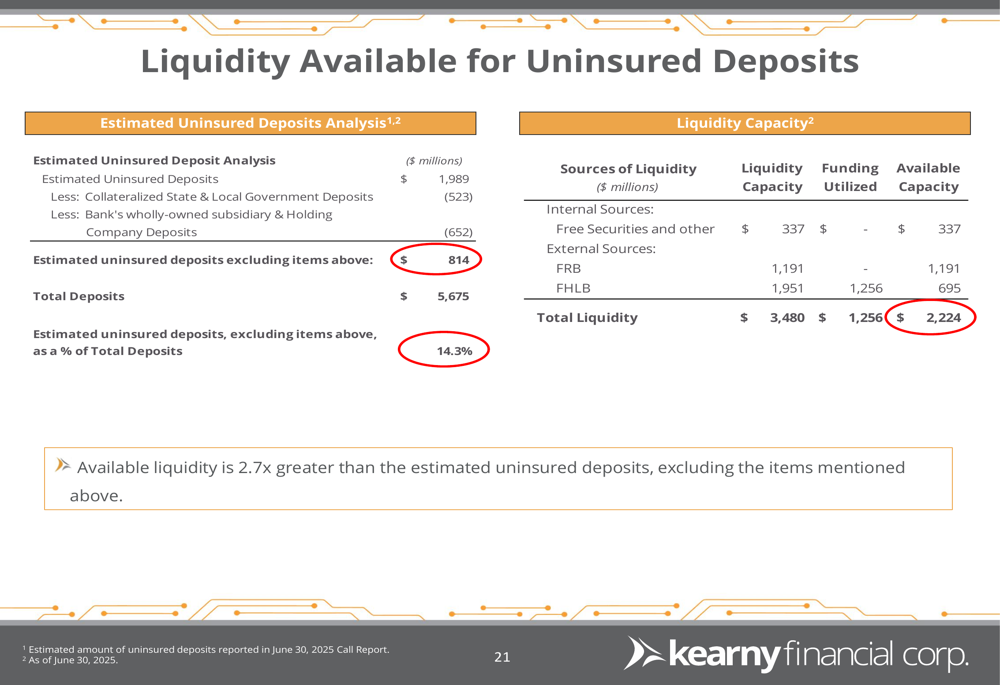

The company’s liquidity position remains robust, with available liquidity 2.7 times greater than estimated uninsured deposits, providing a substantial buffer against potential funding challenges.

Management emphasized the bank’s historical resilience through economic cycles, including the Global Financial Crisis and COVID-19 pandemic, attributing this to its conservative credit culture and disciplined growth strategy. With its strong capital position and upcoming loan repricing opportunities, Kearny appears well-positioned to navigate the current economic environment while pursuing sustainable growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.