Trump in Japan; UnitedHealth raises outlook; gold drops - what’s moving markets

Introduction & Market Context

Kenvue Inc (NYSE:KVUE) released its second quarter 2025 financial results on August 7, revealing a 4.2% year-over-year decline in organic sales and the initiation of a comprehensive strategic review. The consumer health company, which houses brands like Tylenol, Neutrogena, and Listerine, also announced that its board is exploring a "broad range of strategic alternatives" to unlock shareholder value.

The results come amid leadership changes, with Kirk Perry stepping in as Interim Chief Executive Officer. Despite the challenging quarter, Kenvue’s stock showed resilience, rising 2.15% in premarket trading to $21.90, building on the previous day’s 0.82% gain.

Quarterly Performance Highlights

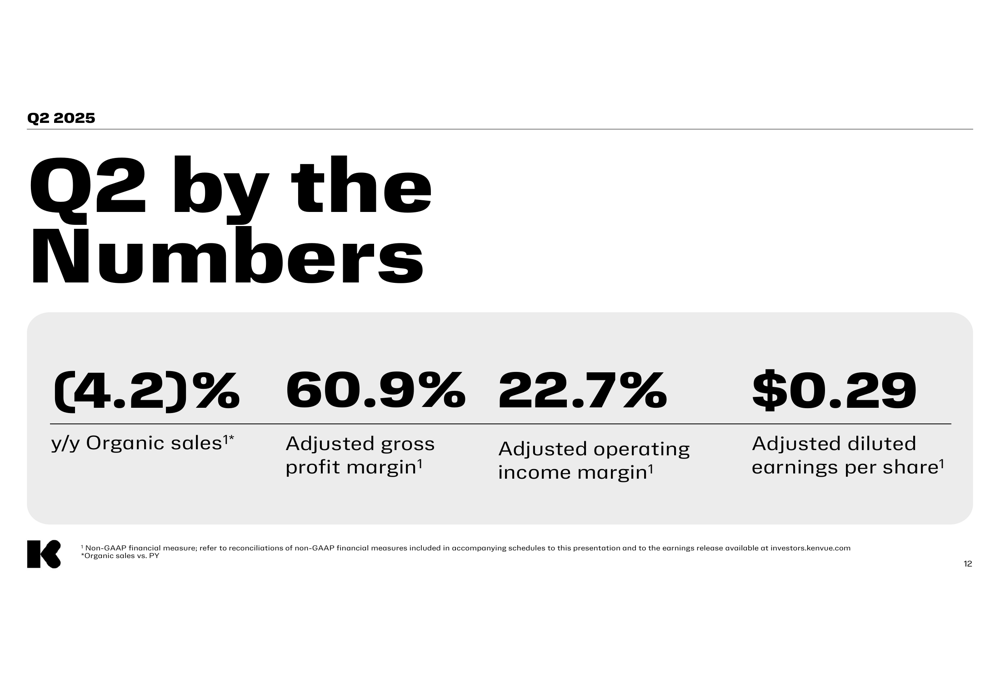

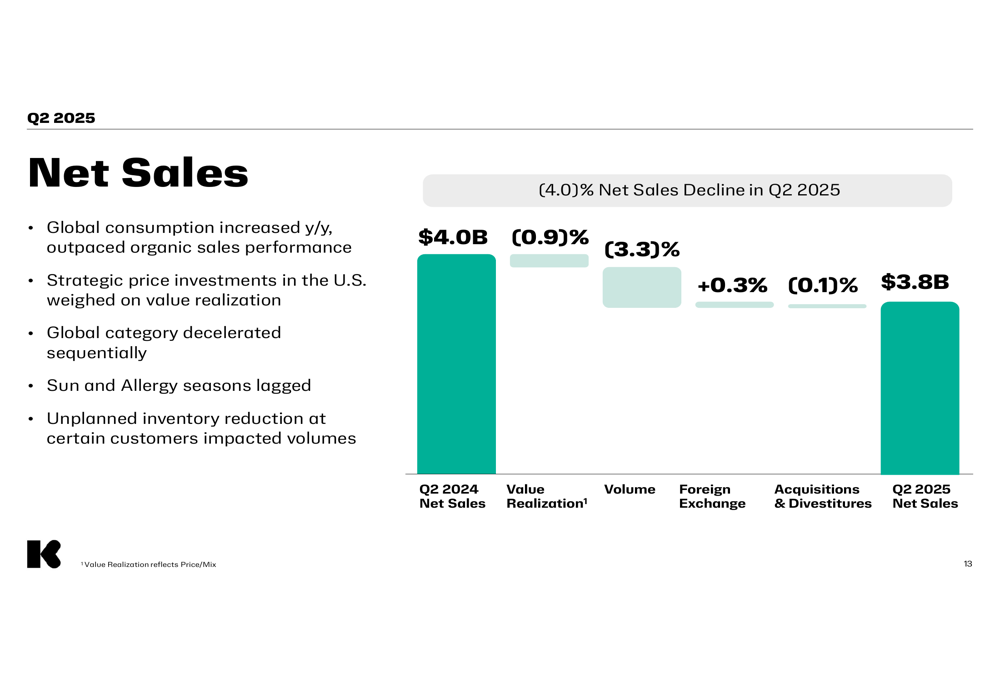

Kenvue reported net sales of $3.8 billion for Q2 2025, down from $4.0 billion in the same period last year. The 4.2% organic sales decline was driven by volume decreases of 3.3% and negative value realization of 0.9%.

As shown in the following chart of quarterly financial metrics:

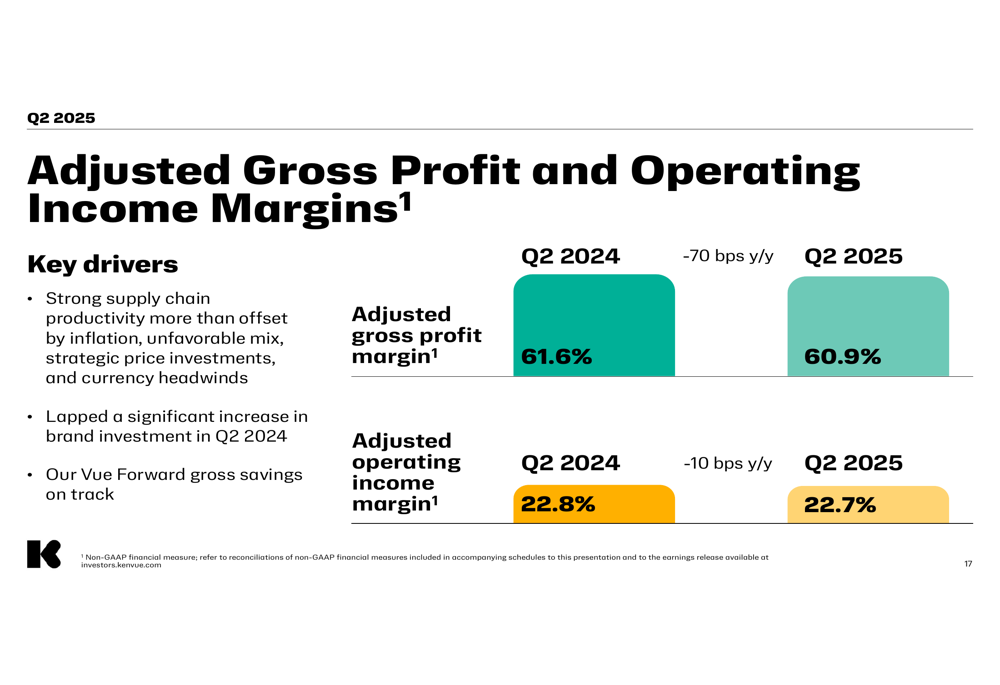

The company maintained an adjusted gross profit margin of 60.9%, down 70 basis points year-over-year, while adjusted operating income margin held relatively steady at 22.7%, just 10 basis points below Q2 2024. Adjusted diluted earnings per share came in at $0.29, compared to $0.32 in the prior-year period.

A detailed breakdown of the net sales decline reveals multiple challenges:

Management noted that while global consumption increased year-over-year and outpaced organic sales performance, strategic price investments in the U.S. weighed on value realization. Additionally, seasonal categories like sun care and allergy products underperformed, and unplanned inventory reductions at certain retail customers negatively impacted volumes.

Segment Performance

All three of Kenvue’s business segments experienced sales declines in the second quarter:

Self Care, which includes brands like Tylenol and Zyrtec, saw the steepest decline with organic sales falling 5.9%. The company attributed this primarily to soft seasonal business performance, though it highlighted strong market share gains.

Skin Health & Beauty, featuring brands such as Neutrogena and Aveeno, reported a 3.7% organic sales decline, with management noting that global consumption had stabilized with sequential improvement in the U.S. market.

Essential Health, home to brands like Listerine and Johnson’s, experienced a 2.4% organic sales decline, which the company attributed to tough year-ago comparisons.

The following chart illustrates the company’s profitability metrics:

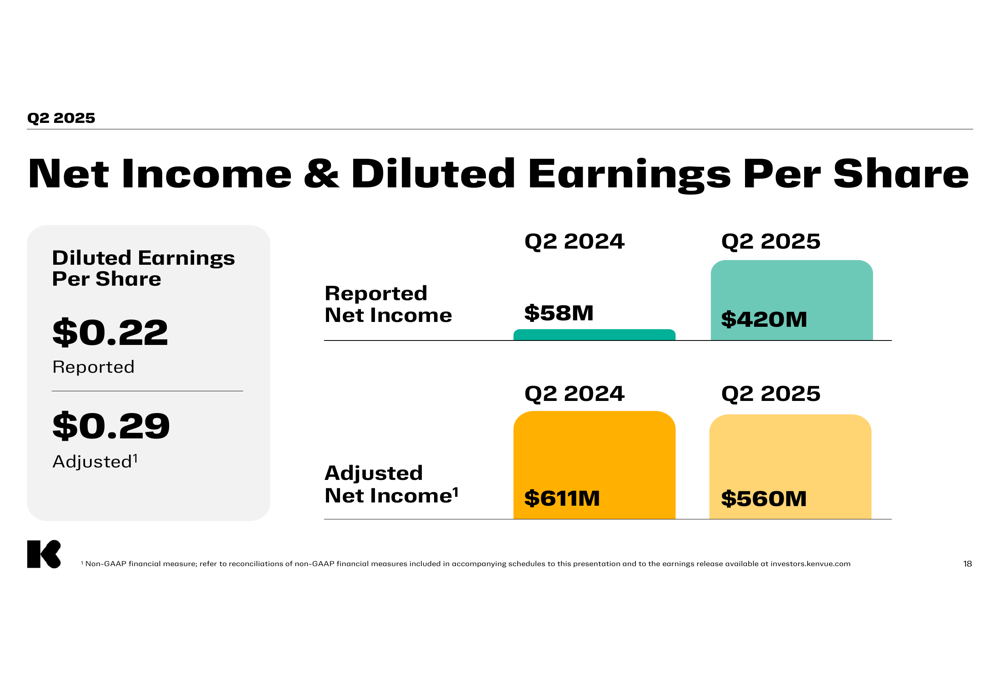

Kenvue’s adjusted net income decreased from $611 million in Q2 2024 to $560 million in Q2 2025, as shown in this earnings summary:

Strategic Initiatives

In response to the challenging quarter, Kenvue’s board has initiated what it describes as a "comprehensive review of a broad range of strategic alternatives" to enhance shareholder value. While specific options weren’t detailed, such language typically signals potential major corporate actions including business restructuring, divestitures, or even exploring a sale.

Interim CEO Kirk Perry outlined his initial observations and priorities, focusing on four key areas:

1. Reducing organizational complexity

2. Reinforcing a consumer-centric mindset

3. Refocusing on household penetration

4. Executing flawless go-to-market strategies

"The only strategy your consumers and customers will ever see is execution," Perry stated in the presentation, emphasizing his 30 years of global consumer products experience.

The company’s immediate operational priorities include:

Similarly, new CFO Amit Banati highlighted opportunities to "drive reliability and consistency in results through operating discipline" and "unlock efficiencies across the P&L."

Forward-Looking Statements

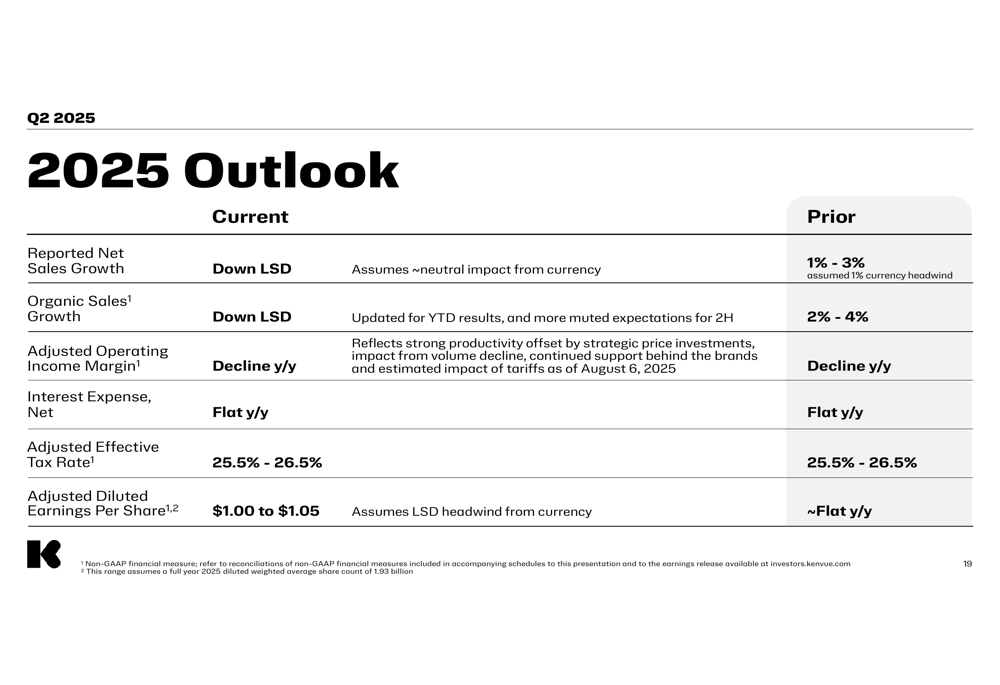

Kenvue has significantly revised its outlook for 2025, as shown in the following guidance summary:

The company now expects organic sales to decline in the low-single-digits for the full year, a marked change from the 2-4% growth projected after Q1 results. Adjusted operating income margin is expected to decline year-over-year, reflecting the impact of strategic price investments despite strong productivity measures. Adjusted diluted earnings per share is now projected to be between $1.00 and $1.05, with a low-single-digit headwind from currency.

This updated guidance represents a substantial shift from the company’s more optimistic outlook following Q1 2025, when Kenvue anticipated 2-4% organic sales growth for the remainder of the year.

Market Reaction

Despite the disappointing results and lowered guidance, Kenvue’s stock showed resilience, trading up 2.15% in premarket to $21.90. This follows a 0.82% gain in the previous session, suggesting investors may be responding positively to the strategic review announcement and new leadership’s focus on operational improvements.

The stock remains within its 52-week range of $19.75 to $25.17, though well below the high mark set earlier in the year. The market’s relatively positive reaction may indicate that investors see potential in the strategic alternatives being explored by the board and the new leadership team’s focus on execution and efficiency.

In summary, while Kenvue faces significant challenges across its business segments, the company’s board and new leadership are taking decisive action to address operational issues and explore strategic options to enhance shareholder value:

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.