Street Calls of the Week

Introduction & Market Context

Kimbell Royalty Partners (NYSE:KRP) showcased record Q1 2025 performance in its latest investor presentation, marking a significant turnaround from the disappointing Q4 2024 results that saw the company miss earnings expectations by a wide margin. The mineral royalty company, which offers a 15.2% annualized distribution yield, has positioned itself as a unique investment opportunity in the energy sector with tax advantages and a strong balance sheet.

The presentation comes as Kimbell’s stock has been trading near its 52-week low, with the fundamentals showing a current price of $11.88, down 1.25% in the most recent session, though premarket trading on May 8, 2025, showed signs of recovery with the stock up 5.39% to $12.52.

Quarterly Performance Highlights

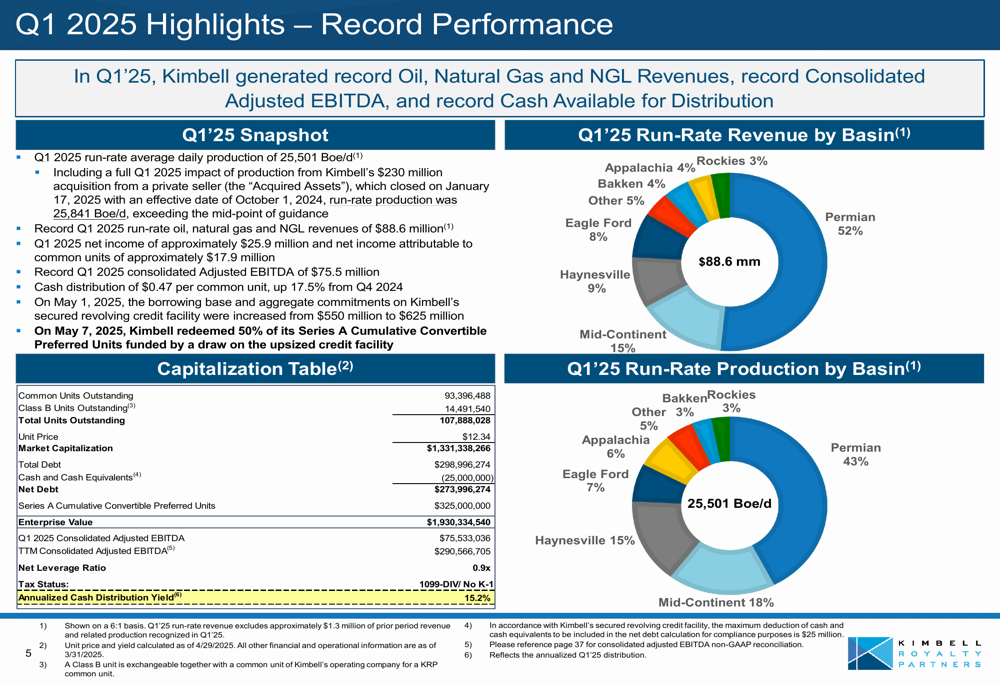

Kimbell reported record performance across key metrics for Q1 2025, including record oil, natural gas, and NGL revenues, record consolidated adjusted EBITDA, and record cash available for distribution. This represents a significant improvement from Q4 2024, when the company reported an EPS of -$0.48 against a forecast of $0.19 and revenue of $66.71 million versus expectations of $76.42 million.

As shown in the following chart detailing Q1 2025 highlights, the company maintains a strong balance sheet with a net leverage ratio of 0.9x and an attractive distribution yield of 15.2%:

The company’s production reached 25,501 Boe/d in Q1 2025, with the Permian Basin representing 43% of total production, followed by Mid-Continent (18%), Haynesville (15%), and Eagle Ford (7%). Revenue distribution follows a similar pattern, with the Permian Basin accounting for 52% of Q1 2025 run-rate revenue.

Strategic Positioning

Kimbell has positioned itself as a unique investment opportunity in the energy sector, offering a combination of high yield, tax advantages, and a strong balance sheet that the company claims is unmatched in the public markets. According to the presentation, Kimbell is the only publicly traded company (out of approximately 6,100) that offers a dividend yield above 15%, has a market capitalization exceeding $1.3 billion, and maintains a debt-to-enterprise value ratio below 20%.

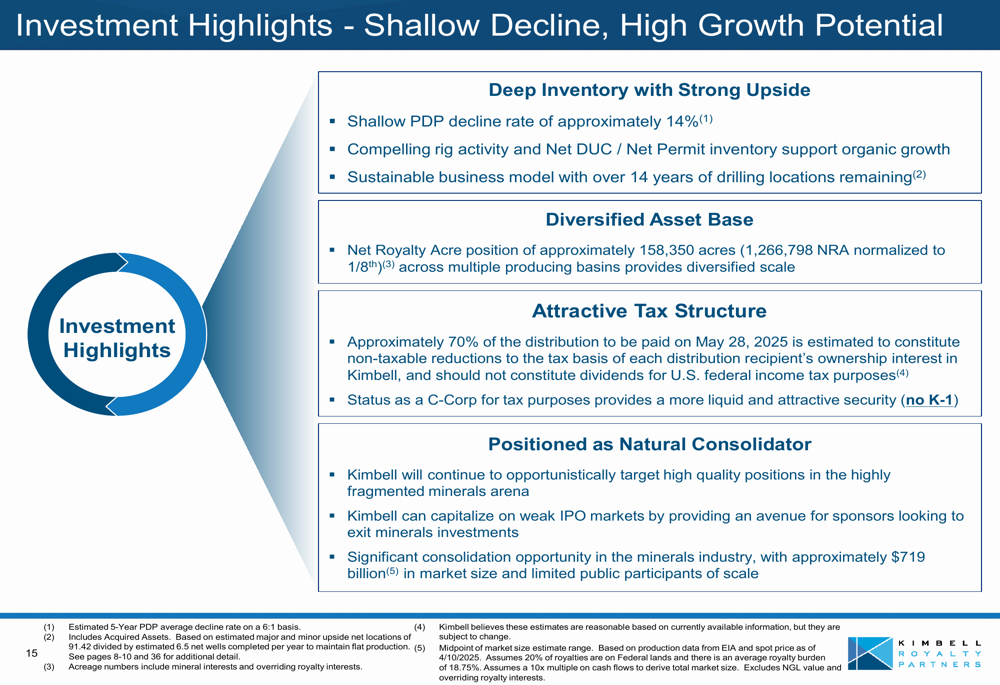

The company’s investment highlights are summarized in the following slide, emphasizing its shallow decline rate, diversified asset base, tax advantages, and position as a natural consolidator in the minerals industry:

A key differentiator for Kimbell is the tax treatment of its distributions. Approximately 70% of the distribution to be paid on May 28, 2025, is estimated to constitute non-taxable reductions to the tax basis of each distribution recipient’s ownership interest, providing tax advantages to investors while maintaining C-Corp status for tax purposes (no K-1).

Asset Portfolio & Growth Strategy

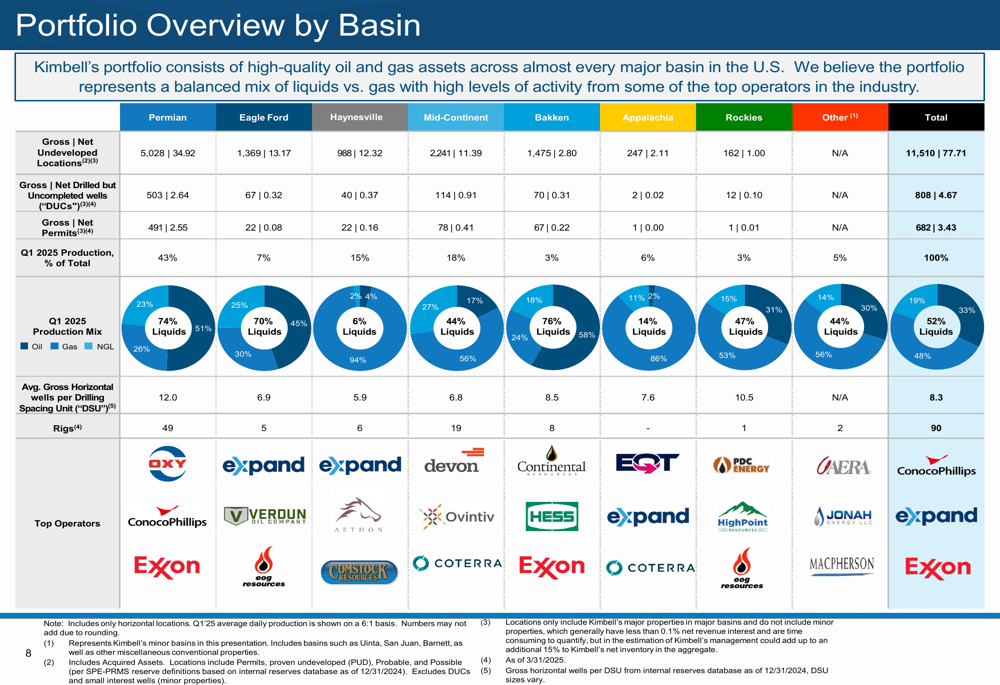

Kimbell’s portfolio is diversified across all major U.S. basins, with interests in over 131,000 gross wells across more than 17 million gross acres. The company has exposure to nearly all active drilling regions in the Lower 48 states, with approximately 98% of all onshore rigs operating in counties where Kimbell holds mineral interest positions.

The following slide provides a detailed breakdown of Kimbell’s portfolio by basin, including production mix, drilling inventory, and key operators:

Since its IPO in 2017, Kimbell has completed over $2.0 billion in acquisitions, growing its run-rate average daily production by more than 8x. The company’s most recent significant acquisition was a $230 million cash transaction in January 2025, continuing its strategy of consolidation in the fragmented minerals industry.

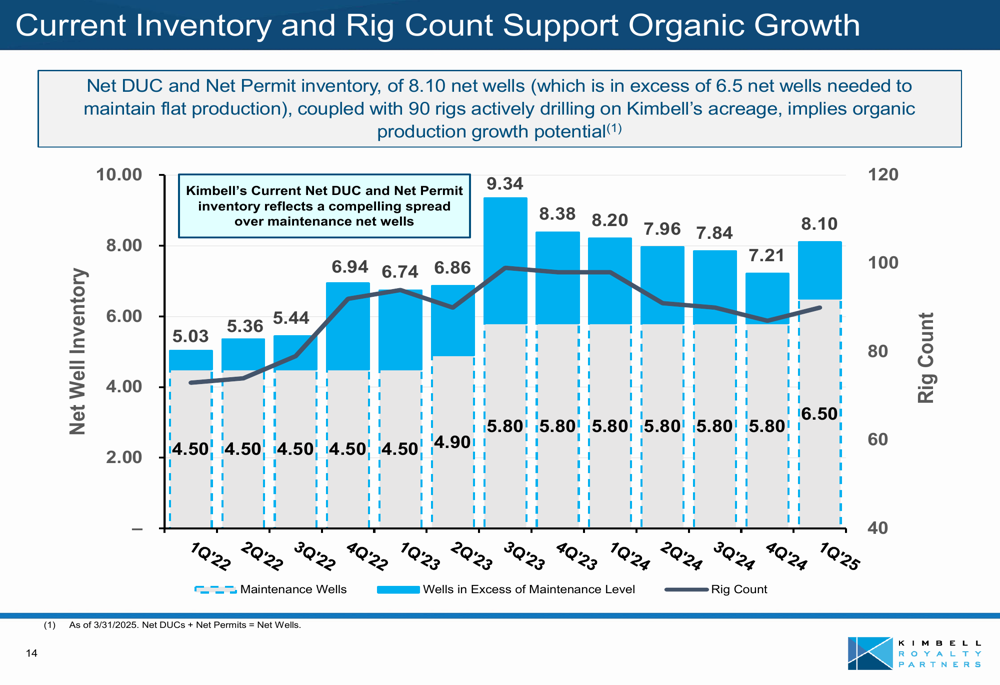

The company’s growth is supported by 90 active rigs (99% horizontal) drilling on its acreage at no cost to Kimbell, a key advantage of the royalty business model. This active drilling, combined with the company’s inventory of drilled but uncompleted wells (DUCs) and permits, supports organic production growth potential.

As illustrated in the following chart, Kimbell’s current inventory and rig count support organic growth beyond what’s needed to maintain flat production:

Forward-Looking Statements

Looking ahead, Kimbell is positioning itself to continue its growth trajectory through both acquisitions and organic development. The company has over 14 years of drilling inventory remaining and a shallow PDP decline rate of approximately 14%, providing a stable foundation for future growth.

Kimbell’s presentation highlights its position as a natural consolidator in the highly fragmented minerals industry, which it estimates has a market size of approximately $719 billion with limited public participants of scale. The company’s strong balance sheet and access to capital markets position it to capitalize on acquisition opportunities, particularly from sponsors looking to exit minerals investments in a weak IPO market.

However, investors should note the disconnect between the company’s optimistic presentation and its recent performance. The Q4 2024 earnings miss and subsequent stock price decline highlight potential risks, including market volatility in oil and gas prices, execution risks associated with acquisitions, and regulatory changes that could affect operational strategies.

Despite these challenges, Kimbell’s Q1 2025 results suggest a potential turnaround, with record performance across key metrics and a continued focus on its strategy of acquiring high-quality mineral and royalty assets across the United States. The company’s unique combination of high yield, tax advantages, and strong balance sheet continues to differentiate it in the energy sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.