Pilgrim Global buys Sable Offshore (SOC) shares worth $14.7m

Introduction & Market Context

Kinder Morgan Inc (NYSE:KMI) released its second quarter 2025 investor presentation, showcasing the company’s strategic focus on natural gas infrastructure amid growing demand for U.S. natural gas exports. The presentation follows the company’s Q1 2025 earnings report, which saw revenue of $4.24 billion exceeding forecasts while EPS of $0.34 slightly missed expectations.

The midstream energy giant continues to position itself as a critical player in U.S. energy infrastructure, transporting approximately 40% of U.S. natural gas production through its extensive network of approximately 66,000 miles of natural gas pipelines. This strategic positioning comes as the company’s stock trades at $27.04, down 2.1% in the most recent session but well above its 52-week low of $18.83.

Strategic Focus on Natural Gas

Kinder Morgan has strategically shifted its business mix toward natural gas over the past decade, with natural gas now representing 65% of its business, up from 49% in 2014. This pivot aligns with growing domestic and international demand for U.S. natural gas, particularly for LNG exports, power generation, and industrial use.

As shown in the following infrastructure portfolio overview, the company’s natural gas focus is complemented by refined products (26%) and CO2 (9%) segments:

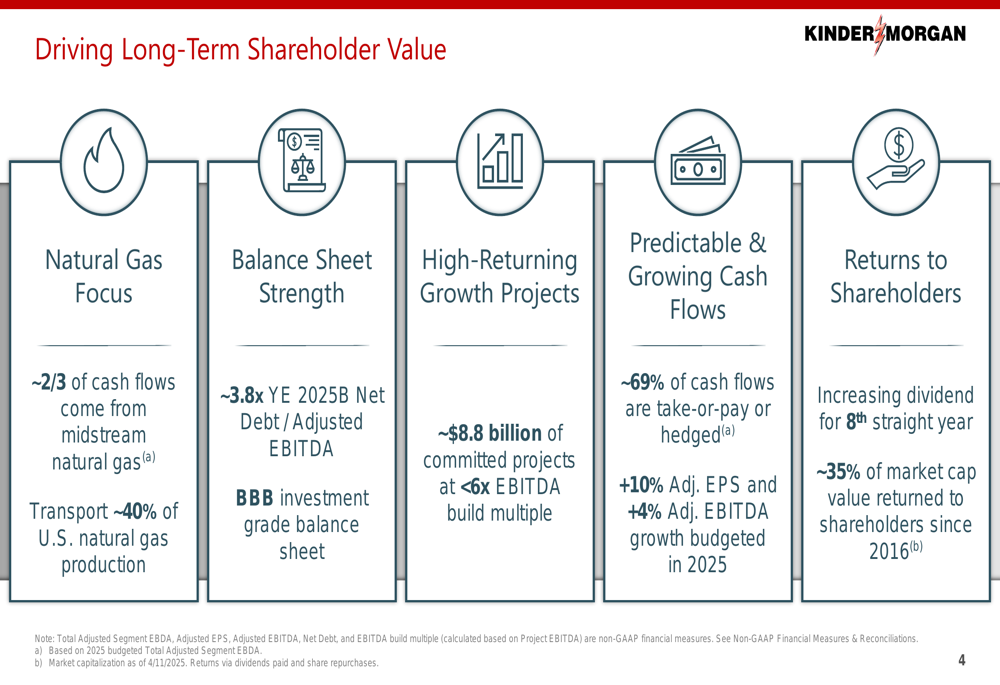

The company’s strategic focus on five key areas is designed to drive long-term shareholder value, emphasizing its natural gas-centric business model, balance sheet strength, high-returning growth projects, predictable cash flows, and shareholder returns:

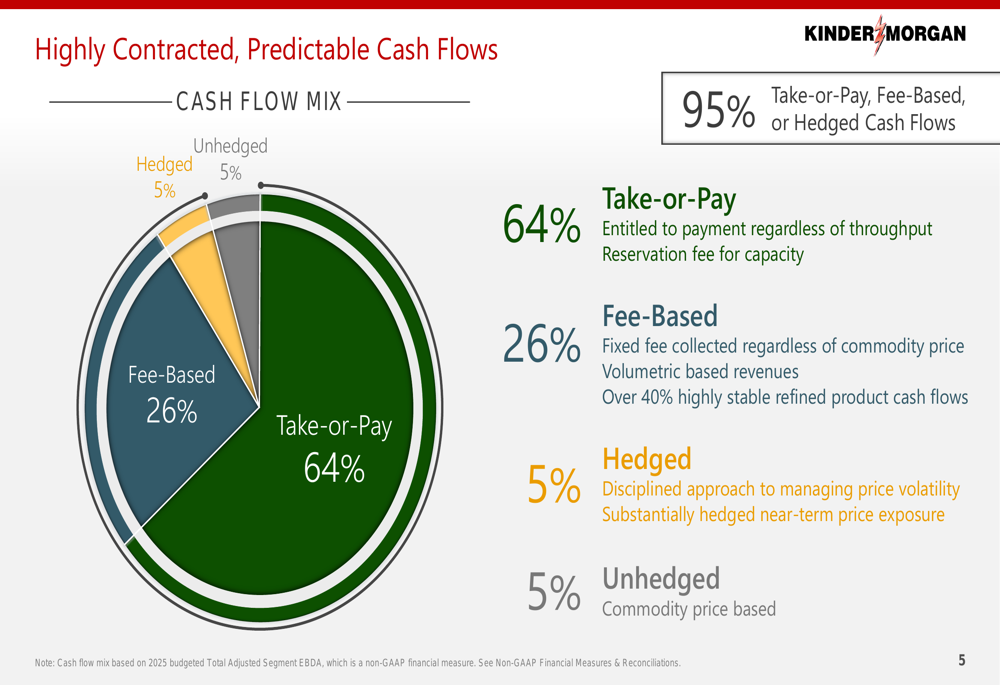

A key strength of Kinder Morgan’s business model is its highly contracted, predictable cash flows, with 95% of cash flows being take-or-pay, fee-based, or hedged. This structure provides significant revenue stability regardless of commodity price fluctuations:

Financial Outlook & Project Growth

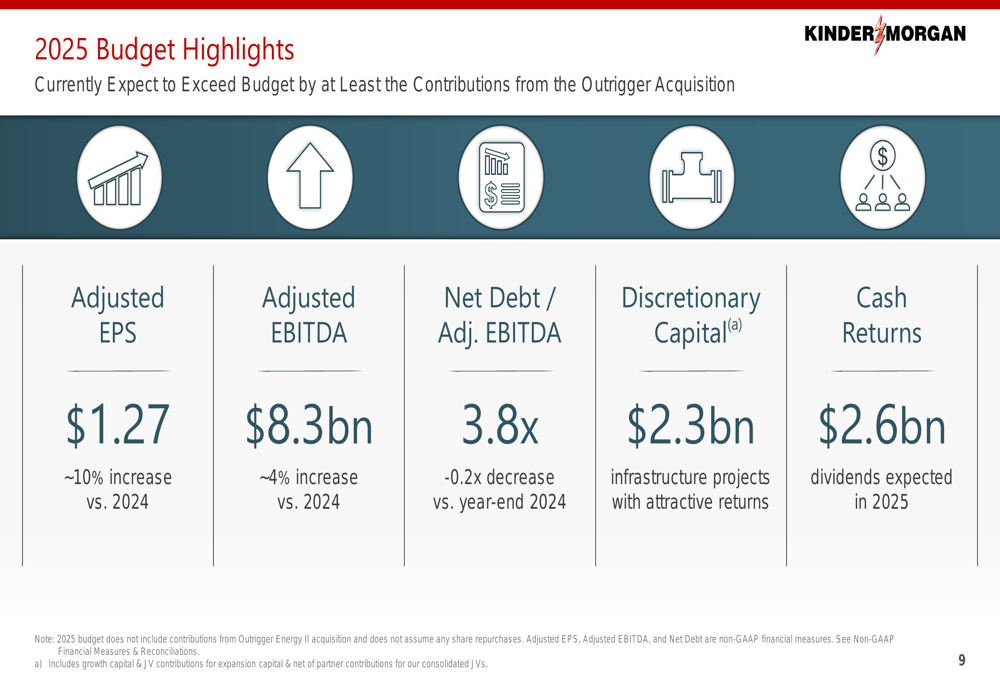

Kinder Morgan’s 2025 budget highlights project continued growth, with adjusted EPS expected to reach $1.27, representing approximately 10% growth compared to 2024. The company forecasts adjusted EBITDA of $8.3 billion, a 4% increase from 2024, while maintaining balance sheet strength with a net debt to adjusted EBITDA ratio of 3.8x.

The following slide details these key financial metrics for 2025:

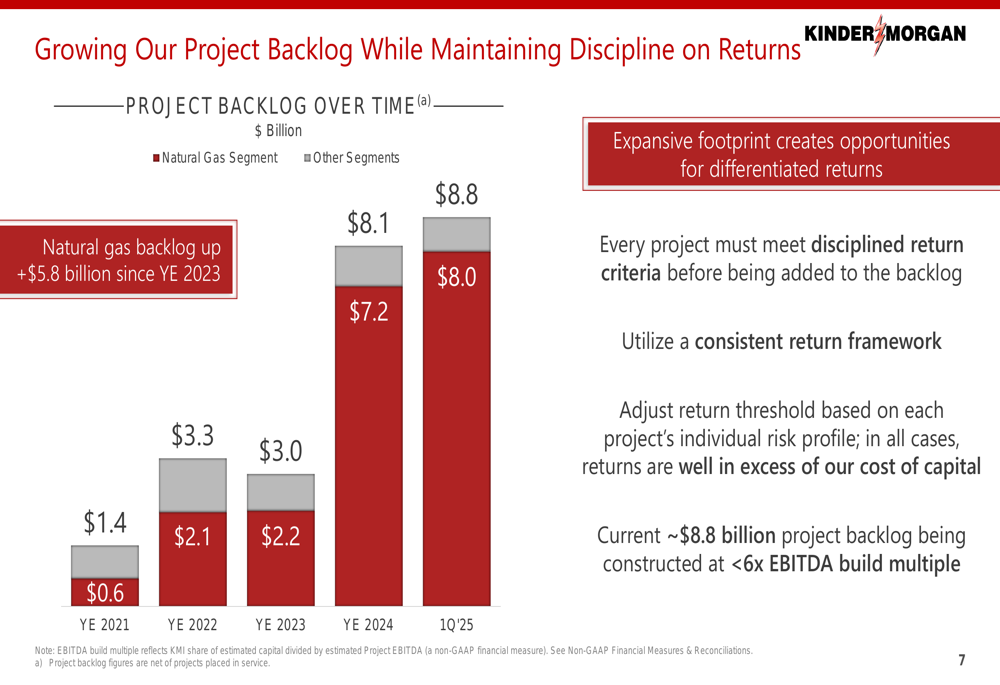

One of the most significant developments has been the substantial growth in Kinder Morgan’s project backlog, which has expanded from $1.4 billion at year-end 2021 to $8.8 billion as of Q1 2025. This growth aligns with the company’s Q1 earnings report, which noted a $900 million expansion in the project backlog, primarily focused on meeting power demand.

The following chart illustrates this dramatic growth in the company’s project backlog:

These projects are expected to generate attractive returns, with the backlog being constructed at less than 6x EBITDA build multiple, well above the company’s cost of capital.

Demand Drivers

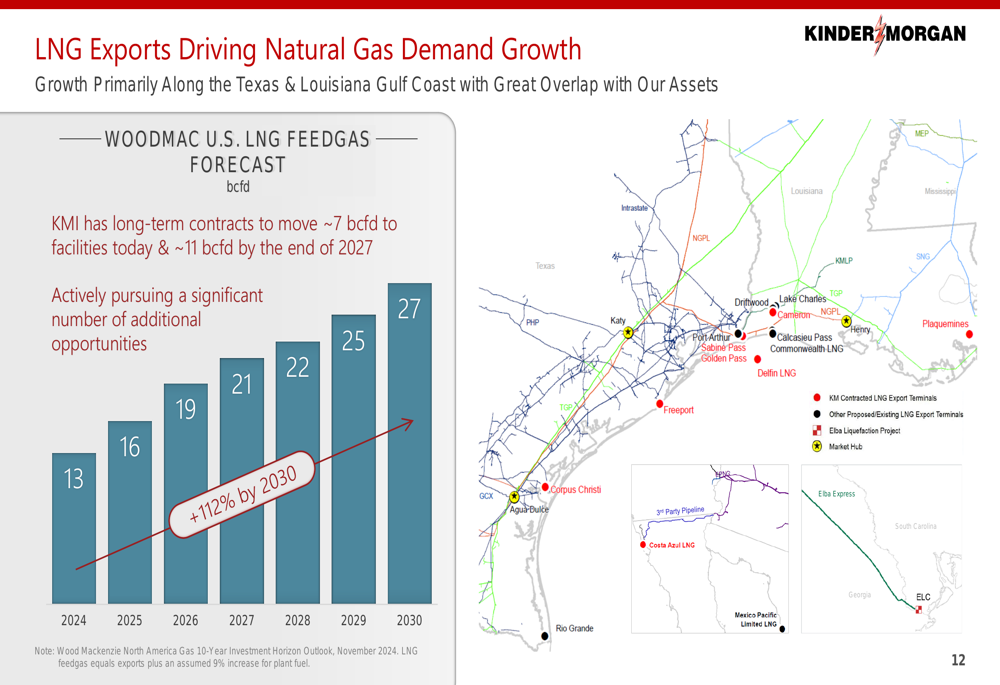

LNG exports represent a primary growth driver for Kinder Morgan’s natural gas business. According to Wood Mackenzie forecasts highlighted in the presentation, U.S. LNG feedgas demand is projected to more than double from 13 bcfd in 2024 to 27 bcfd by 2030, representing 112% growth.

The following chart illustrates this projected growth in LNG feedgas demand:

Kinder Morgan is well-positioned to capitalize on this trend, with long-term contracts to move approximately 7 bcfd to LNG facilities today, growing to approximately 11 bcfd by the end of 2027.

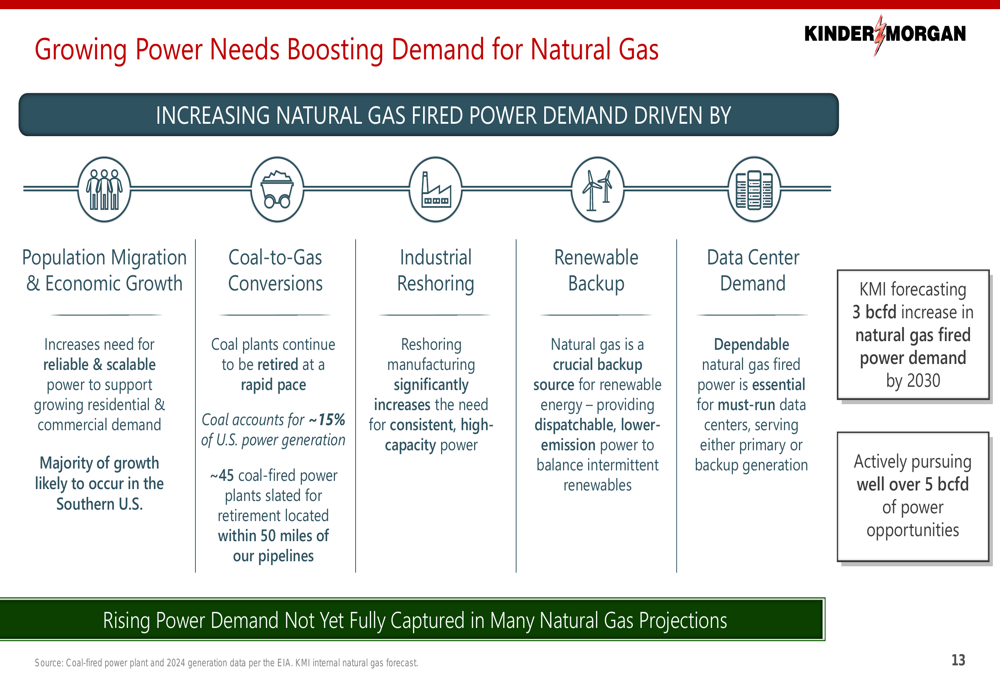

Power generation represents another significant growth opportunity, with Kinder Morgan forecasting a 3 bcfd increase in natural gas-fired power demand by 2030. This growth is driven by population migration, economic expansion, coal-to-gas conversions, industrial reshoring, renewable backup needs, and increasing data center demand.

Infrastructure Expansion & Project Pipeline

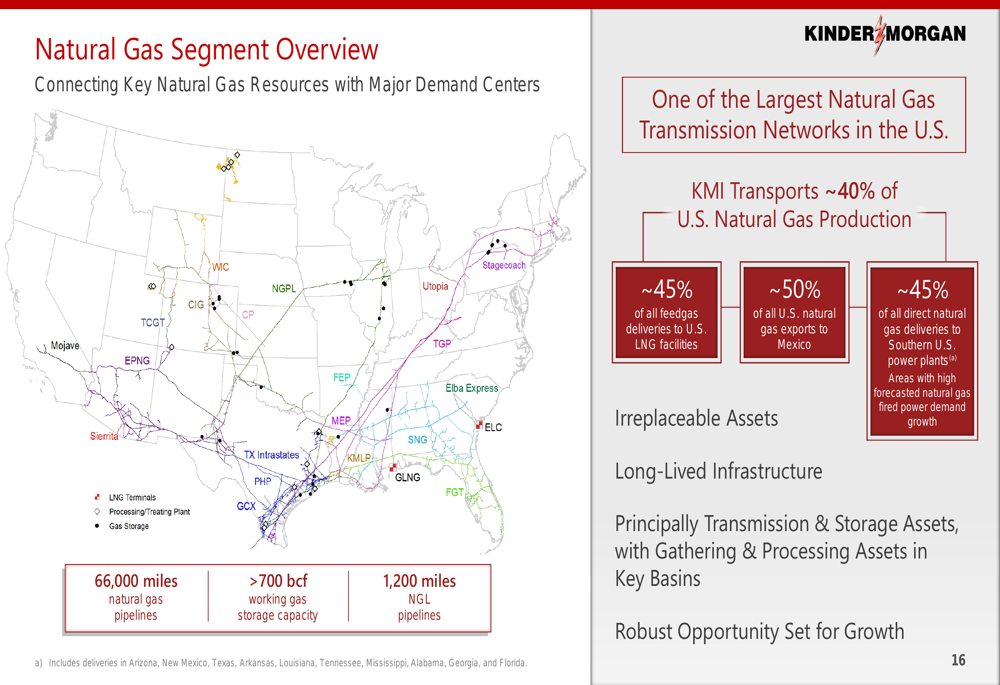

Kinder Morgan’s natural gas segment includes approximately 66,000 miles of natural gas pipelines, over 700 bcf of working gas storage capacity, and 1,200 miles of NGL pipelines. This extensive network positions the company to serve key demand centers across the United States:

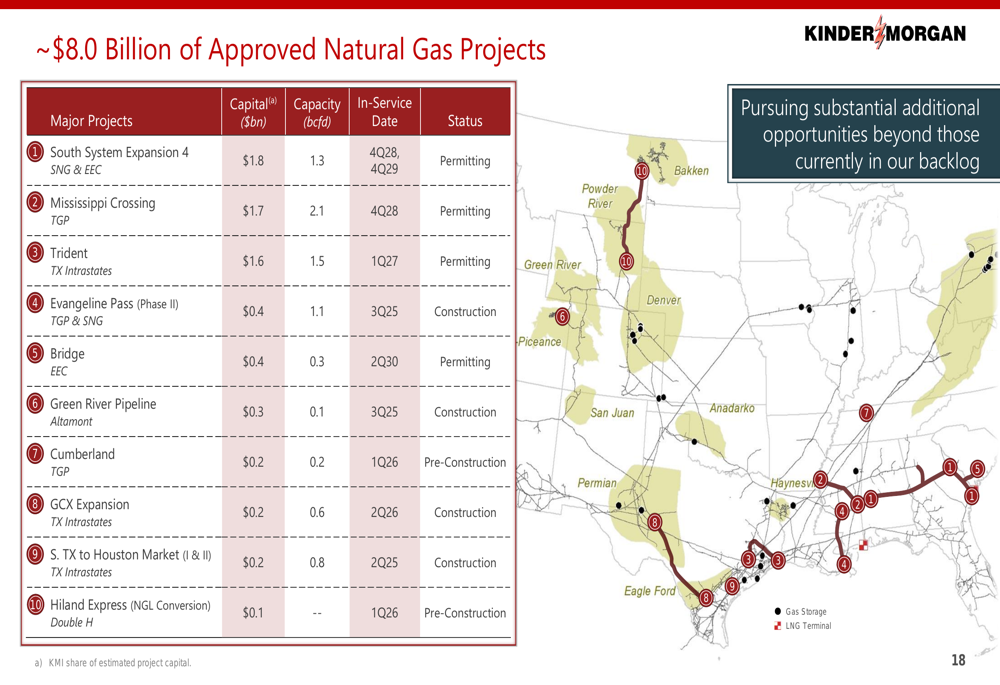

The company has approximately $8.0 billion of approved natural gas projects in its backlog, including major expansions such as the South System Expansion ($1.8 billion, 1.3 bcfd), Mississippi Crossing ($1.7 billion, 2.1 bcfd), and Trident (NSE:TRIE) ($1.6 billion, 1.5 bcfd). These projects are strategically located to serve growing demand centers:

Shareholder Returns & Financial Strength

Kinder Morgan continues to focus on returning value to shareholders, increasing its dividend for the eighth consecutive year. The company’s Q1 2025 earnings report confirmed a 2% year-over-year increase in the quarterly dividend to $0.295 per share. Since 2016, Kinder Morgan has returned approximately 35% of its market capitalization to shareholders.

The company maintains a strong balance sheet with a BBB investment grade rating and expects to achieve a net debt to adjusted EBITDA ratio of 3.8x by year-end 2025, an improvement from 4.0x at year-end 2024.

Forward-Looking Statements

Kinder Morgan’s outlook remains positive, driven by strong fundamentals in the natural gas market. The company expects U.S. natural gas demand to increase by 20-28 bcfd by the end of the decade, with particularly strong growth in the Gulf Coast region to support LNG exports and industrial demand.

While the presentation paints an optimistic picture, investors should note that the company’s Q1 2025 EPS slightly missed analyst expectations despite revenue outperformance. Additionally, the company faces potential challenges from economic slowdowns, regulatory changes, and competition in the natural gas sector.

Nevertheless, Kinder Morgan’s extensive infrastructure network, growing project backlog, and strong financial position appear to provide a solid foundation for continued growth in the evolving energy landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.