Street Calls of the Week

Kinetik Holdings Inc. (NASDAQ:KNTK) reported modest growth in its second quarter 2025 results on August 6, while simultaneously lowering its full-year guidance due to project delays. The midstream energy company, which focuses exclusively on the Permian Basin, saw its stock decline 1.42% on the day of the announcement.

Quarterly Performance Highlights

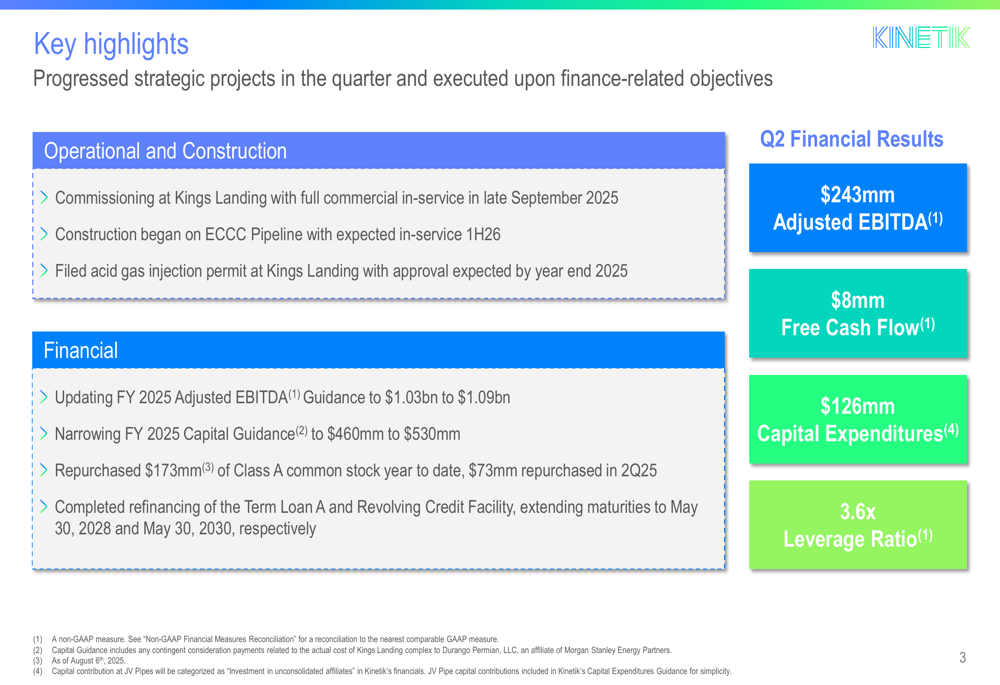

Kinetik reported Adjusted EBITDA of $243 million for Q2 2025, with Free Cash Flow of $8 million and Capital Expenditures of $126 million. The company maintained a leverage ratio of 3.6x, slightly above its long-term target of 3.5x.

"Our second quarter results demonstrate the resilience of our business model, with both of our operating segments delivering year-over-year growth despite challenging market conditions," the company stated in its presentation.

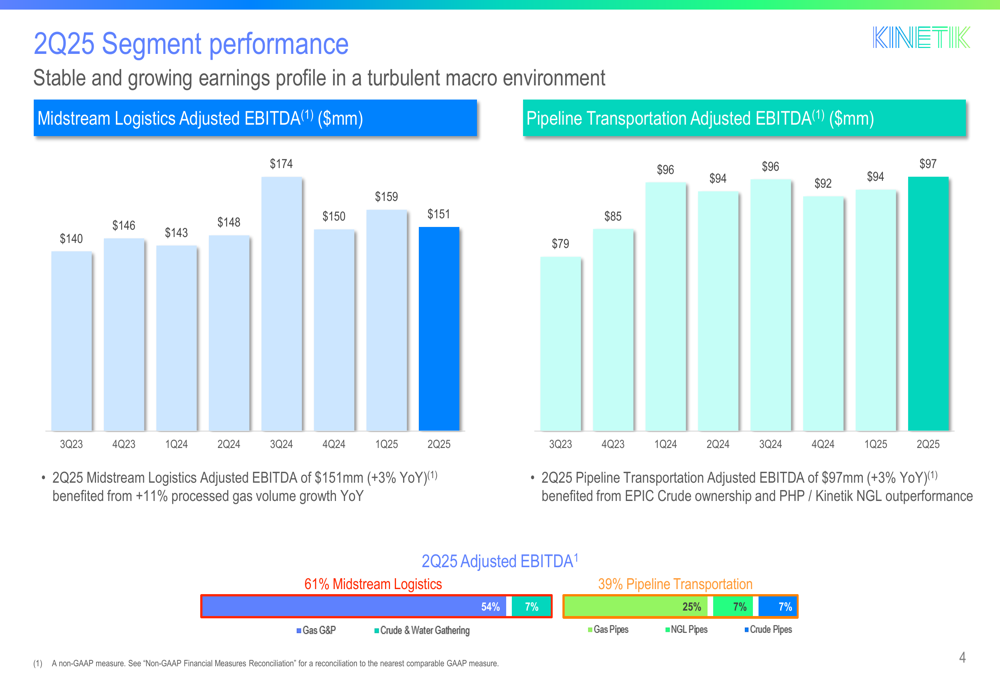

The quarterly performance breakdown shows balanced growth across Kinetik’s business segments. Midstream Logistics delivered Adjusted EBITDA of $151 million, representing a 3% year-over-year increase, driven by 11% growth in processed gas volumes. Similarly, the Pipeline Transportation segment generated $97 million in Adjusted EBITDA, also up 3% year-over-year, benefiting from EPIC Crude ownership and outperformance in PHP/Kinetik NGL operations.

As shown in the following segment performance breakdown:

Guidance Revision and Operational Challenges

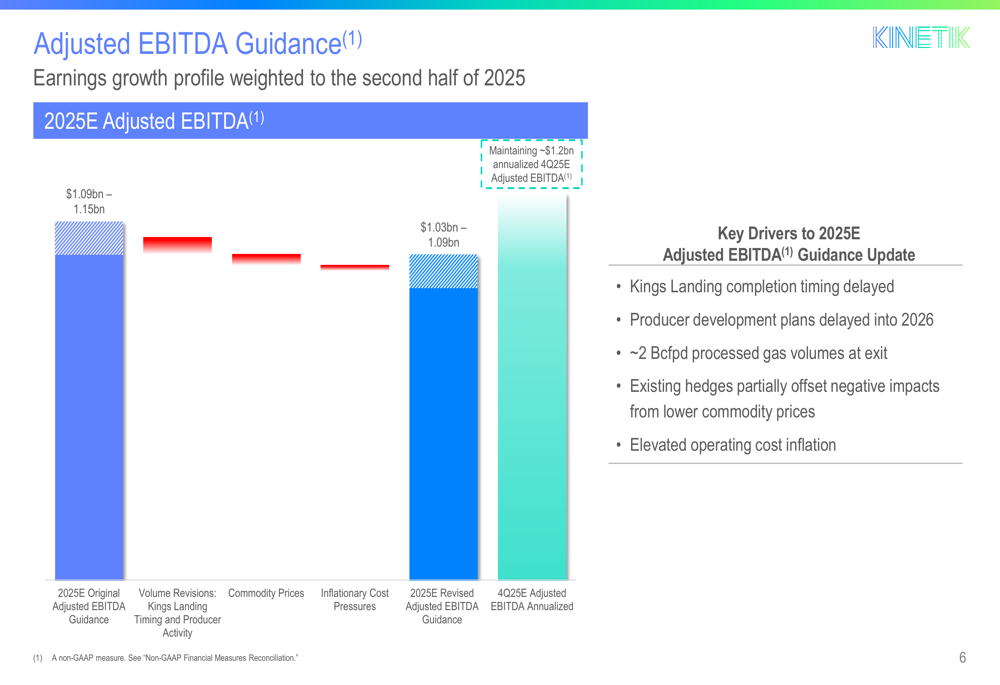

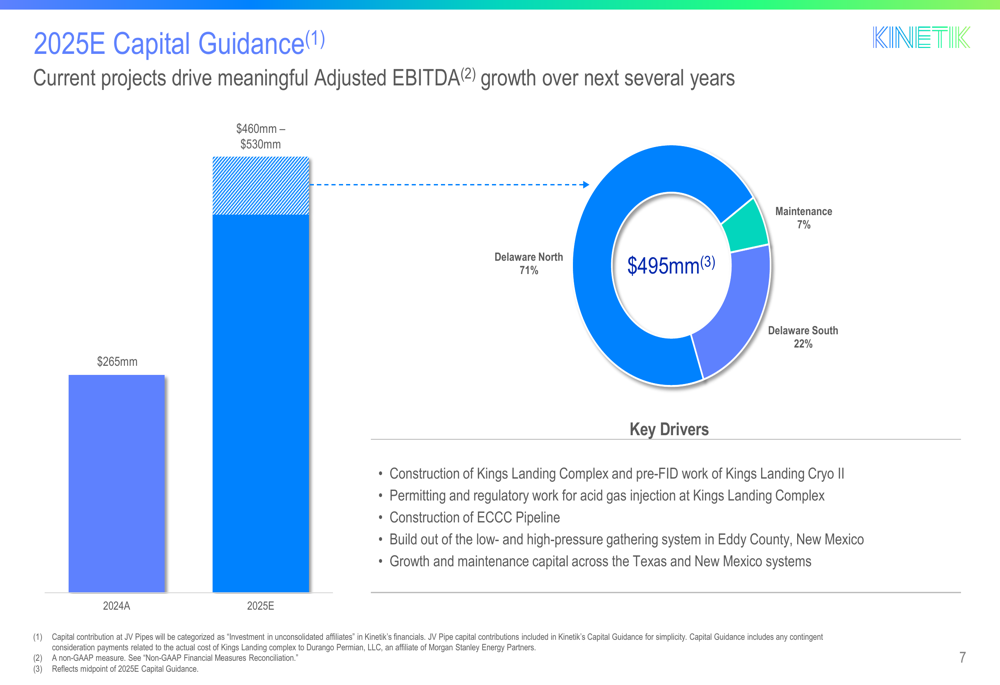

In a significant development, Kinetik lowered its full-year 2025 Adjusted EBITDA guidance to $1.03-1.09 billion, down from the previous range of $1.09-1.15 billion. The company also narrowed its capital expenditure guidance to $460-530 million.

The downward revision stems primarily from delays in the Kings Landing complex completion and postponed producer development plans. Despite these setbacks, Kinetik projects annualized fourth-quarter 2025 Adjusted EBITDA of approximately $1.2 billion, suggesting stronger performance toward year-end.

The following chart illustrates the factors affecting the guidance revision:

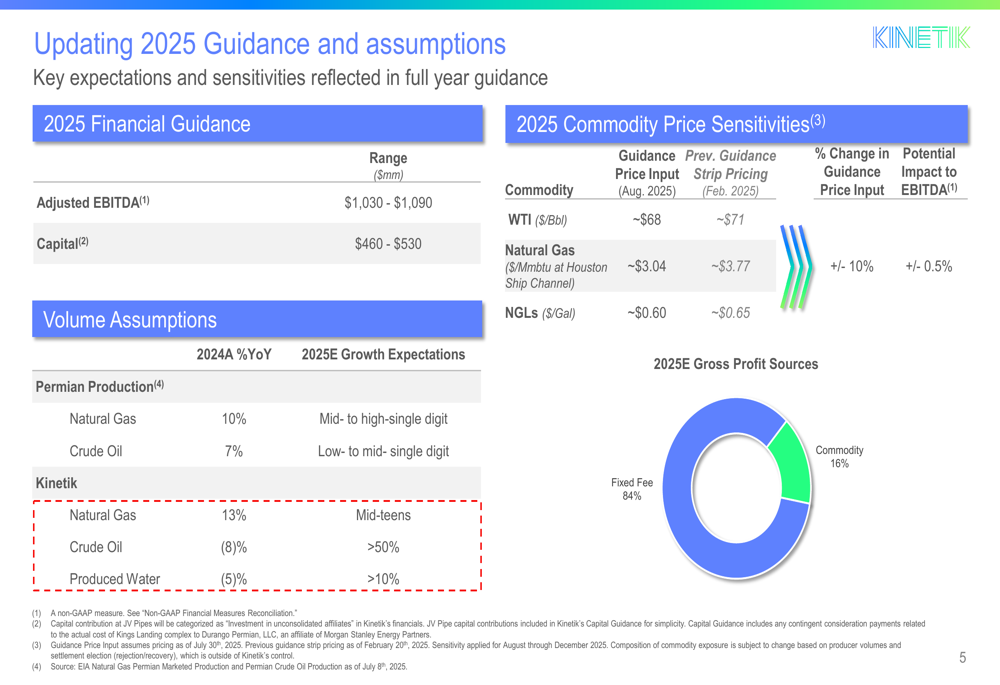

Kinetik’s commodity price assumptions include WTI at approximately $68/Bbl, Natural Gas at $3.04/Mmbtu, and NGLs at $0.60/Gal. The company noted that its existing hedges partially offset negative impacts from lower commodity prices and elevated operating cost inflation.

A key strength of Kinetik’s business model is its revenue stability, with 84% of 2025 estimated gross profit coming from fixed-fee sources and only 16% from commodity-sensitive revenue streams.

Strategic Capital Investments

Despite near-term challenges, Kinetik continues to advance several strategic growth initiatives. The company has allocated its 2025 capital expenditures primarily to Delaware North (71%), Delaware South (22%), and maintenance (7%).

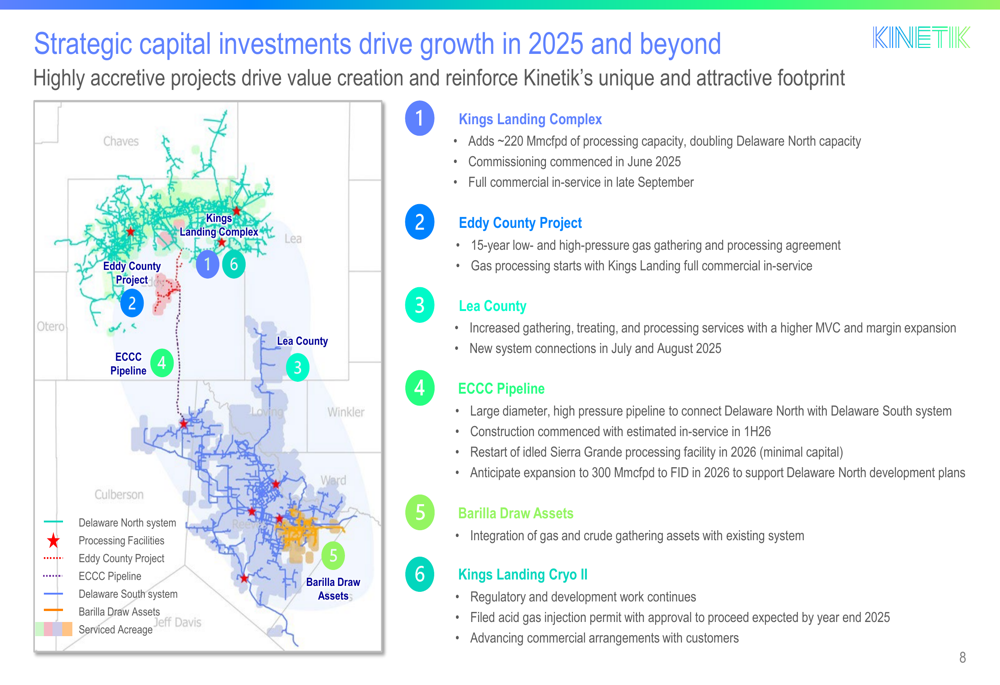

The Kings Landing Complex, which will add approximately 220 Mmcfpd of processing capacity, remains a centerpiece of Kinetik’s growth strategy, effectively doubling Delaware North capacity. Though delayed, the facility is now scheduled for full commercial in-service in late September 2025.

Other key projects include the Eddy County Project, featuring a 15-year low- and high-pressure gas gathering and processing agreement, and the ECCC Pipeline, which has begun construction with expected in-service in the first half of 2026.

The following map highlights Kinetik’s strategic capital investments:

The capital allocation breakdown for 2025 demonstrates the company’s investment priorities:

Long-Term Financial Objectives

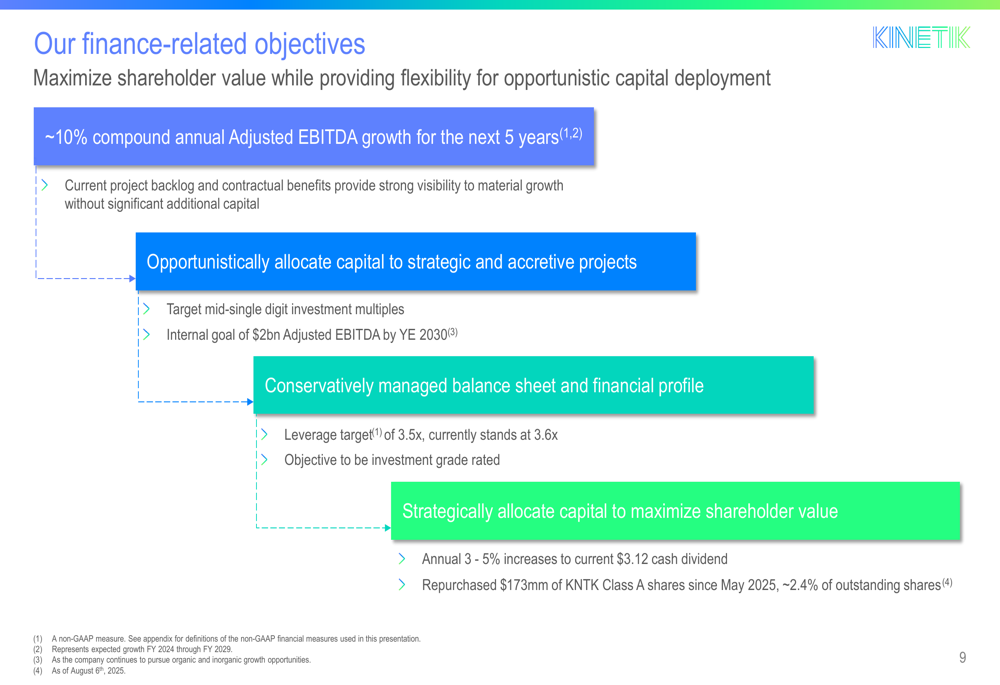

Looking beyond current challenges, Kinetik outlined ambitious long-term financial goals, targeting approximately 10% compound annual Adjusted EBITDA growth over the next five years. The company aims to reach $2 billion in Adjusted EBITDA by year-end 2030, nearly double its current level.

"We remain committed to conservatively managing our balance sheet while strategically allocating capital to maximize shareholder value," the company stated in its presentation.

Kinetik has been active in returning capital to shareholders, repurchasing $173 million of Class A common stock year-to-date, including $73 million in the second quarter alone. The company also plans annual 3-5% increases to its current $3.12 cash dividend.

Market Context and Outlook

Kinetik’s Q2 results and guidance revision come after a mixed first quarter. In Q1 2025, the company reported Adjusted EBITDA of $250 million, suggesting a sequential decline in Q2. Despite missing earnings expectations in Q1, with EPS of $0.05 versus a forecast of $0.36, the stock had risen 3.99% following that announcement.

The company’s current trading price of $41.54 remains closer to its 52-week low of $39.33 than its high of $67.60, reflecting ongoing investor concerns about project delays and reduced guidance. However, Kinetik’s high percentage of fixed-fee revenue provides stability in a volatile commodity environment, potentially supporting the stock as delayed projects come online later this year and into 2026.

With its exclusive focus on the Permian Basin, one of North America’s most productive oil and gas regions, Kinetik remains well-positioned to capitalize on continued production growth in the area, which the company expects to be in the mid- to high-single digits for natural gas and low- to mid-single digits for crude oil in 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.