Nvidia and TSMC to unveil first domestic wafer for Blackwell chips, Axios reports

Introduction & Market Context

KION Group AG (ETR:KGX) presented its Q2 2025 financial results on July 30, 2025, revealing a mixed performance characterized by record order intake but declining revenue. Following the announcement, the company’s stock fell 4.42%, closing at €56.6, despite several positive metrics. The presentation, delivered by CEO Rob Smith and CFO Christian Harm, highlighted the company’s resilience in a challenging economic environment marked by trade conflicts and geopolitical uncertainties.

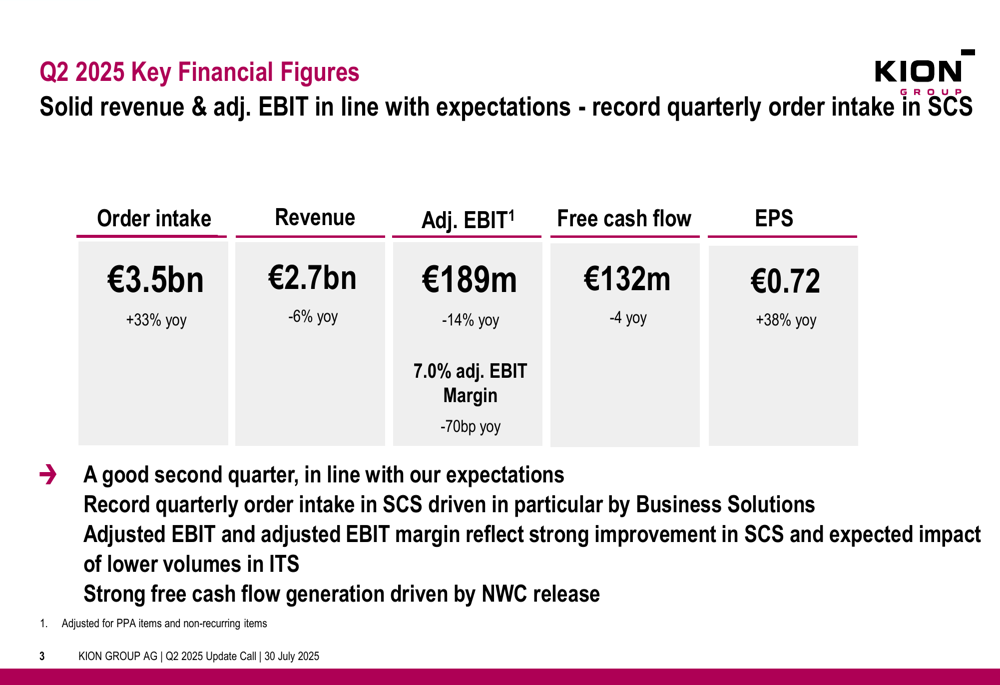

The industrial truck and warehouse automation provider reported a substantial 33% year-over-year increase in order intake, reaching €3.5 billion, while revenue declined 6% to €2.7 billion compared to the same period last year.

Quarterly Performance Highlights

KION’s Q2 2025 performance showed significant variance between its two main business segments. The company reported adjusted EBIT of €189 million, representing a 14% year-over-year decline, with the margin contracting 70 basis points to 7.0%. Despite these challenges, earnings per share increased 38% to €0.72, and the company maintained strong free cash flow of €132 million.

As shown in the following key financial figures:

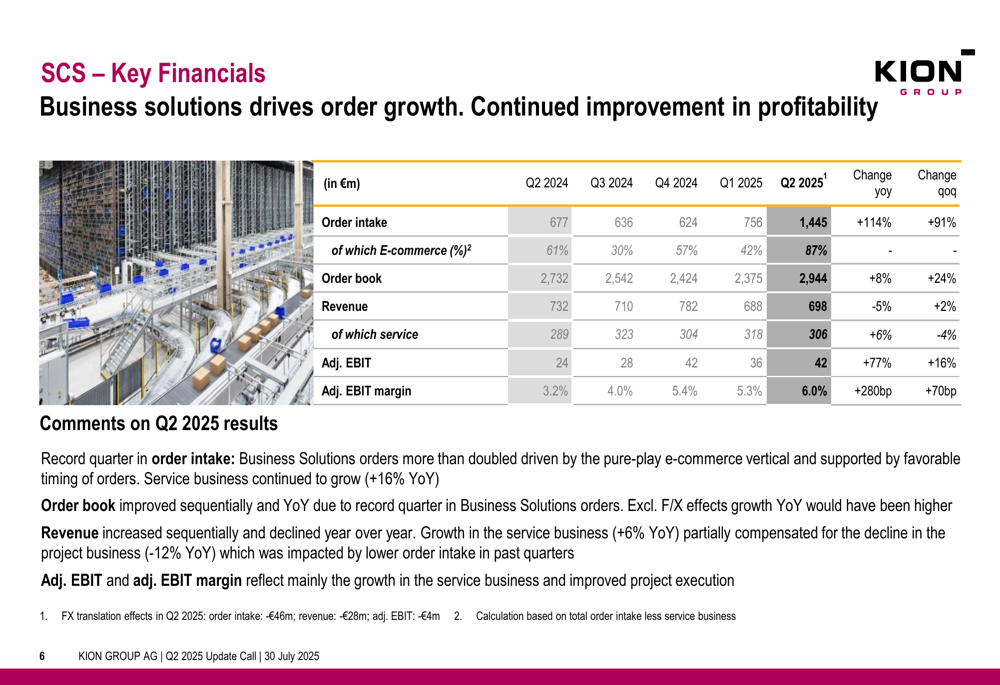

The Supply Chain Solutions (SCS) segment was the standout performer, achieving a record quarterly order intake of €1.445 billion, representing a remarkable 114% year-over-year increase. This growth was primarily driven by the e-commerce sector, which accounted for 87% of SCS orders. The segment’s adjusted EBIT increased 77% year-over-year to €42 million, with the margin expanding 280 basis points to 6.0%.

The detailed SCS segment performance demonstrates this strong improvement:

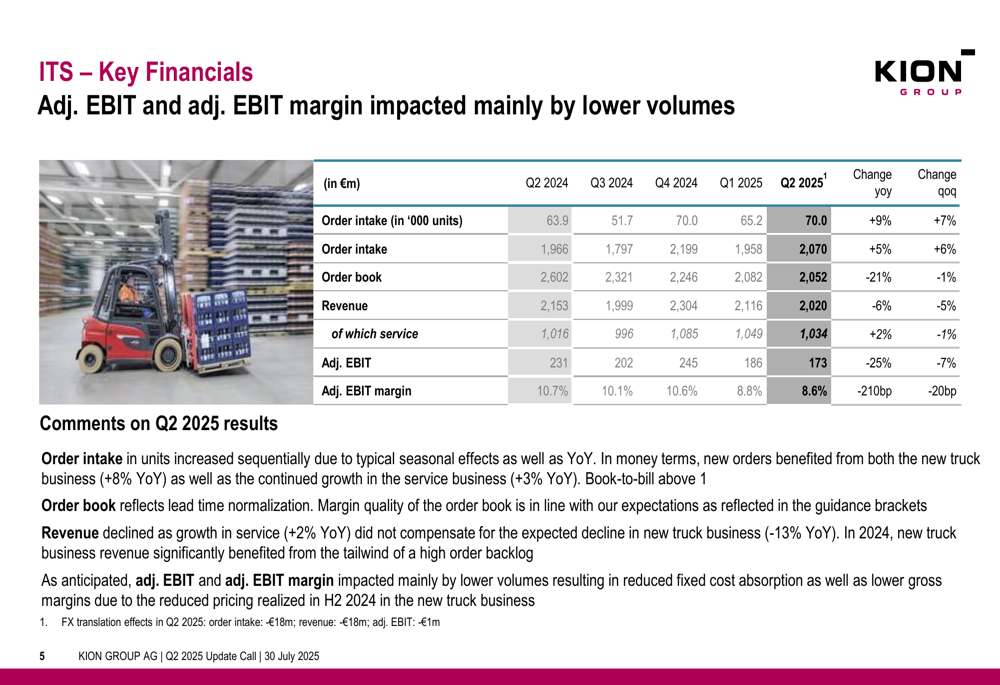

Meanwhile, the Industrial Trucks & Services (ITS) segment faced more significant challenges. While order intake in units increased 9% year-over-year to 70,000 units, revenue declined 6% to €2.02 billion. The segment’s adjusted EBIT fell 25% to €173 million, with the margin contracting 210 basis points to 8.6%.

The ITS segment’s performance reflects ongoing market pressures:

Detailed Financial Analysis

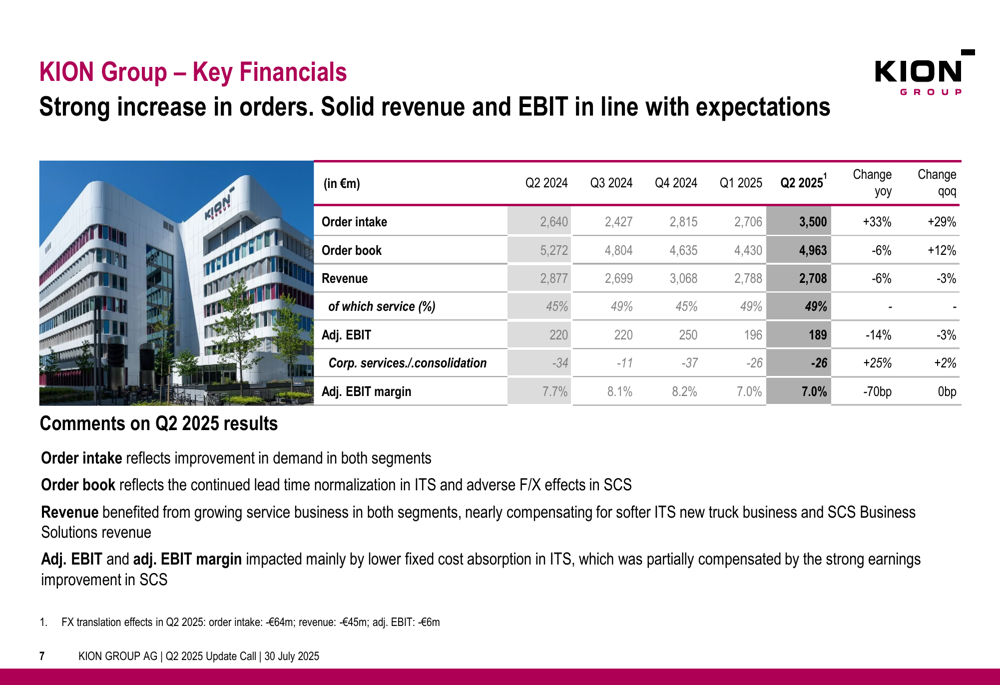

The consolidated financial performance of KION Group shows the contrasting results between segments, with the overall company maintaining stable performance despite headwinds:

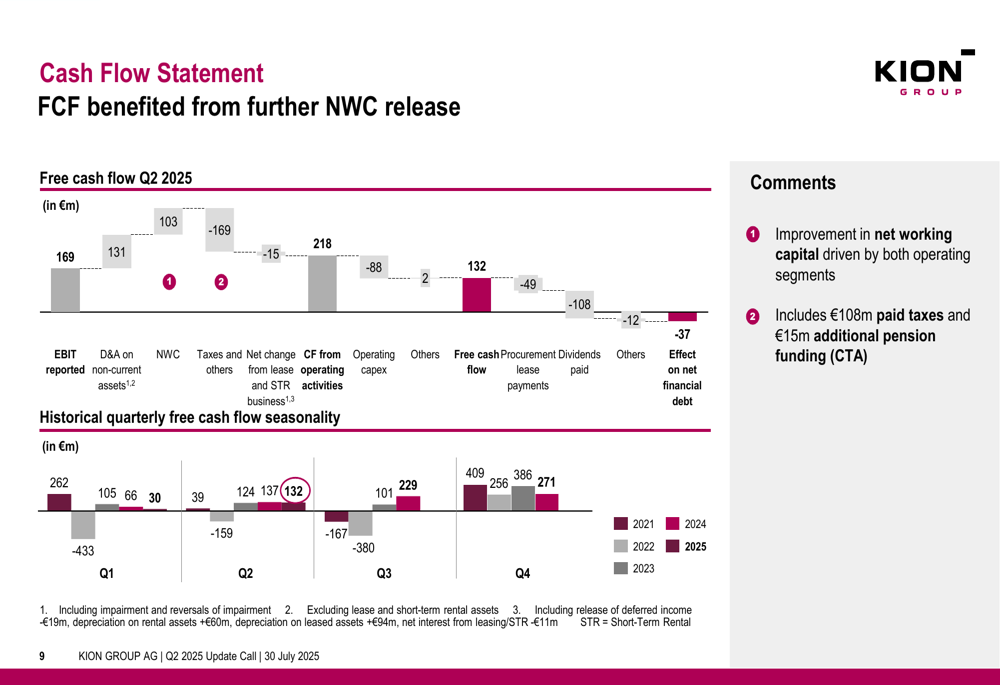

KION’s net income increased year-over-year to €95 million, primarily due to lower PPA and tax expenses, despite the decline in adjusted EBIT. The company’s free cash flow remained strong at €132 million, benefiting from net working capital release.

The cash flow statement illustrates the key drivers behind KION’s solid free cash flow generation:

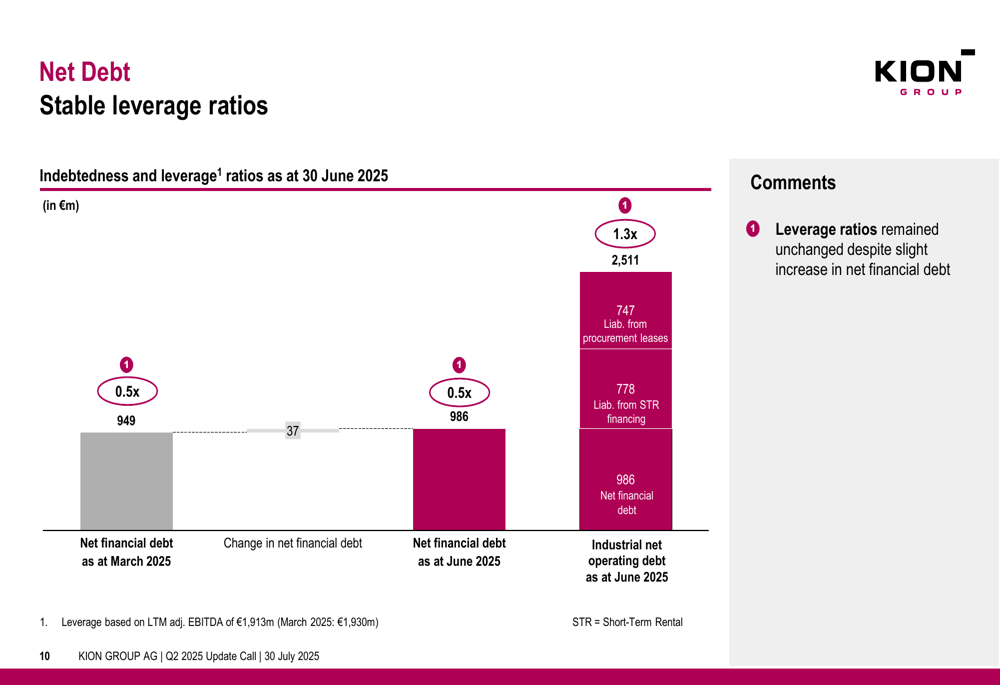

The company maintained a stable financial position, with net financial debt of €986 million and an unchanged leverage ratio of 0.5x. This stability provides KION with flexibility to navigate current market uncertainties while continuing to invest in strategic initiatives.

The net debt position and leverage ratios remain healthy:

Forward-Looking Statements

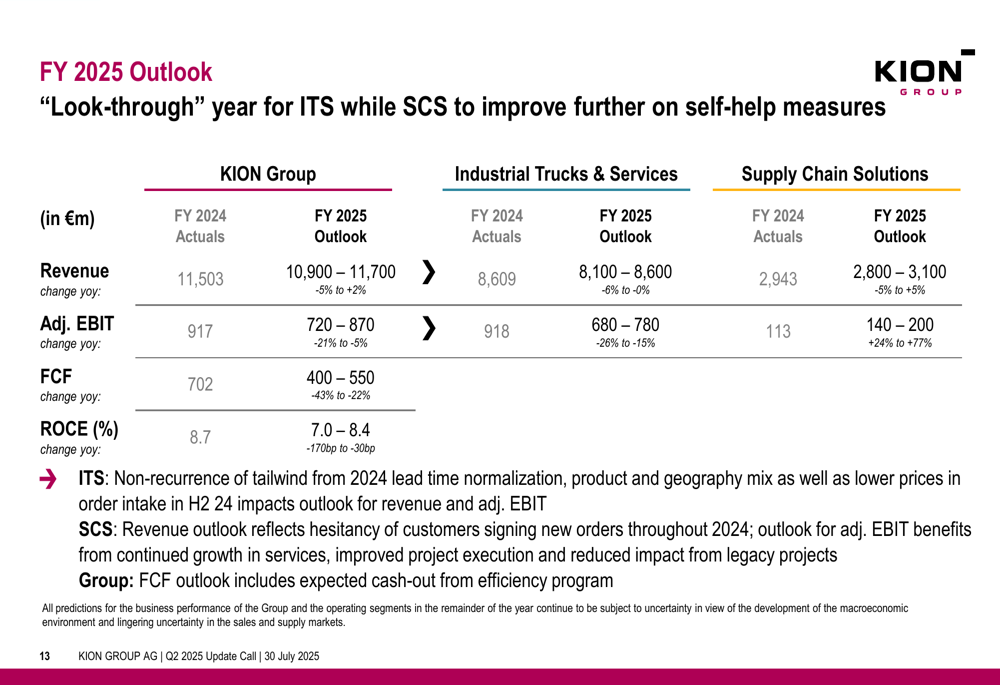

KION Group confirmed its outlook for fiscal year 2025, projecting revenue between €10.9 billion and €11.7 billion (representing a change of -5% to +2% year-over-year) and adjusted EBIT between €720 million and €870 million (-21% to -5% year-over-year). The company expects free cash flow to range from €400 million to €550 million.

The detailed outlook by segment provides further clarity on KION’s expectations:

The company noted that its outlook is contingent on there being no significant disruptions to supply chains as a result of trade barriers, especially tariffs and restrictions on access to critical commodities. KION has expanded its production, research and development, and sales and service networks in the APAC and Americas regions to prepare for shifting geopolitical scenarios.

CEO Rob Smith emphasized the company’s unique market position during the earnings call, stating: "We are the only western player in the China market at this point in time." He also reaffirmed the company’s profitability targets: "Our objective is to have both of our segments and our group above 10% by 2027."

Strategic Initiatives

KION highlighted several strategic initiatives aimed at improving long-term performance. The company is implementing an efficiency program announced in February 2025, which targets sustainable annual cost savings of €140-160 million from 2026 onwards. This program has already incurred non-recurring expenses of €197 million in the first half of 2025, with the remainder expected in the second half of the year.

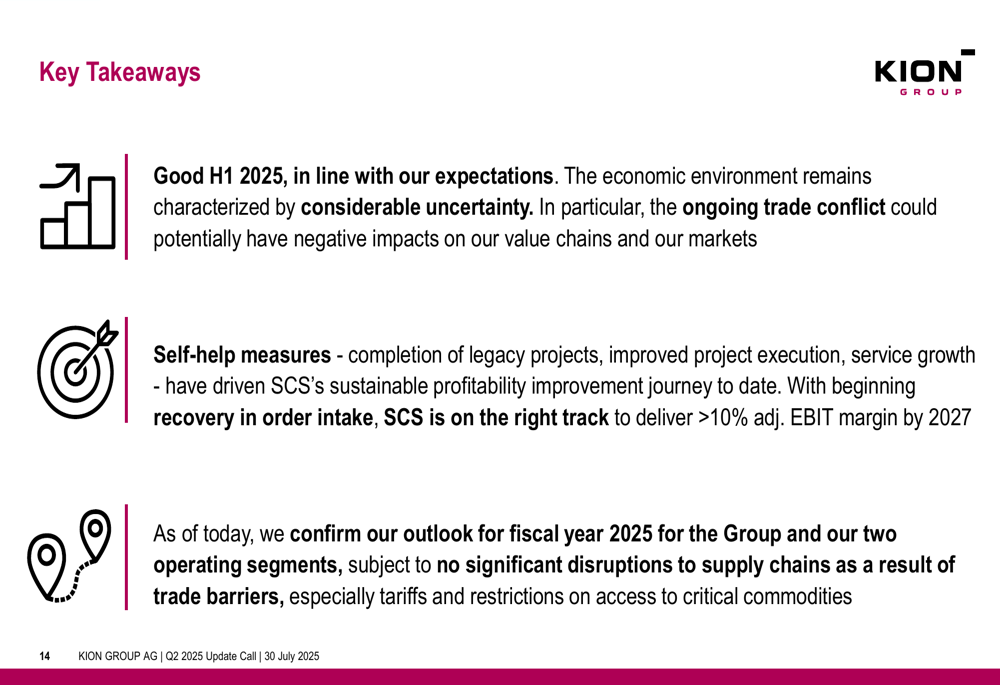

The key takeaways from the presentation underscore KION’s strategic focus:

The company also announced a partnership with NVIDIA for AI integration in industrial settings, according to the earnings article, signaling KION’s commitment to technological advancement in its product offerings.

KION’s service business continues to be a bright spot, growing to 49% of total revenue in Q2 2025, up from 45% in the prior year. This shift toward higher-margin service revenue is part of the company’s strategy to improve overall profitability and reduce cyclicality.

Despite the mixed quarterly results and subsequent stock decline, KION’s strong order intake and confirmed outlook suggest potential for improved performance in the coming quarters, particularly if the company can successfully execute its efficiency initiatives while capitalizing on the growing demand in its SCS segment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.