Pilgrim Global buys Sable Offshore (SOC) shares worth $14.7m

Introduction & Market Context

Kitron ASA (OB:KIT) presented its first quarter 2025 results on April 24, showing mixed performance with a slight year-over-year revenue decline but improved profitability and strong order backlog growth. The stock reacted negatively, dropping 4.56% to 48.96 NOK following the announcement, despite the company trading near its 52-week high of 53.90 NOK.

The electronics manufacturing services provider highlighted its strategic focus on the defence and aerospace sector, which has become a cornerstone of its growth strategy amid increasing NATO investments and global security concerns. While overall revenue declined slightly year-over-year, the company’s profitability metrics and order backlog showed significant improvement.

Quarterly Performance Highlights

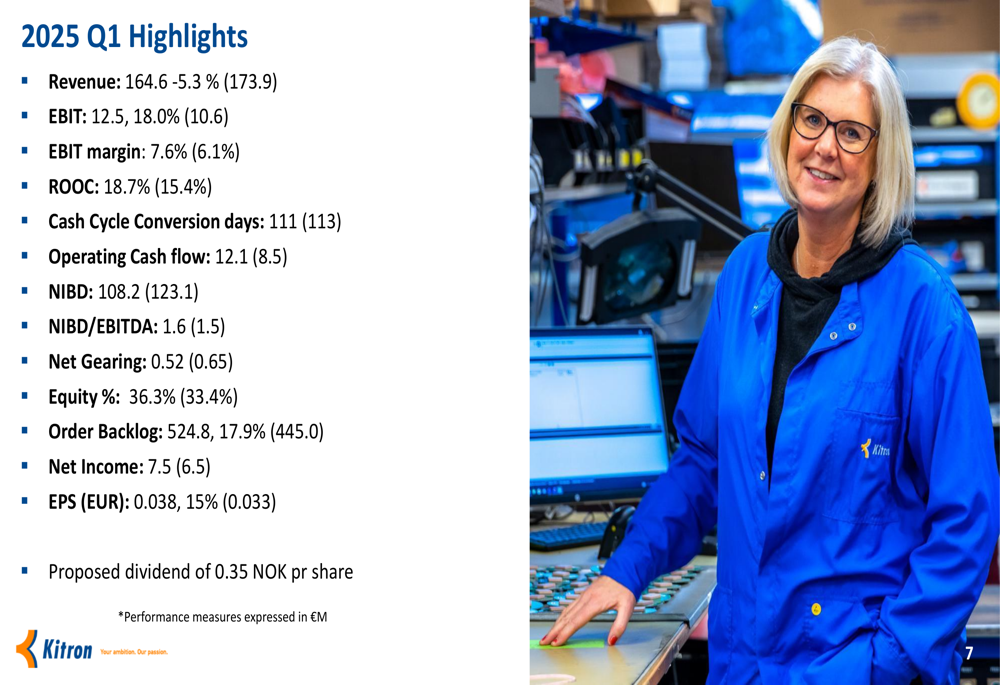

Kitron reported Q1 2025 revenue of €164.6 million, representing a 5.3% decrease compared to the same period last year but a 2% sequential increase from Q4 2024. Despite the revenue decline, the company achieved substantial improvement in profitability with EBIT reaching €12.5 million, an 18% increase year-over-year, resulting in an EBIT margin of 7.6% compared to 6.1% in Q1 2024.

As shown in the following financial highlights slide, Kitron demonstrated strong cash flow generation and improved financial ratios:

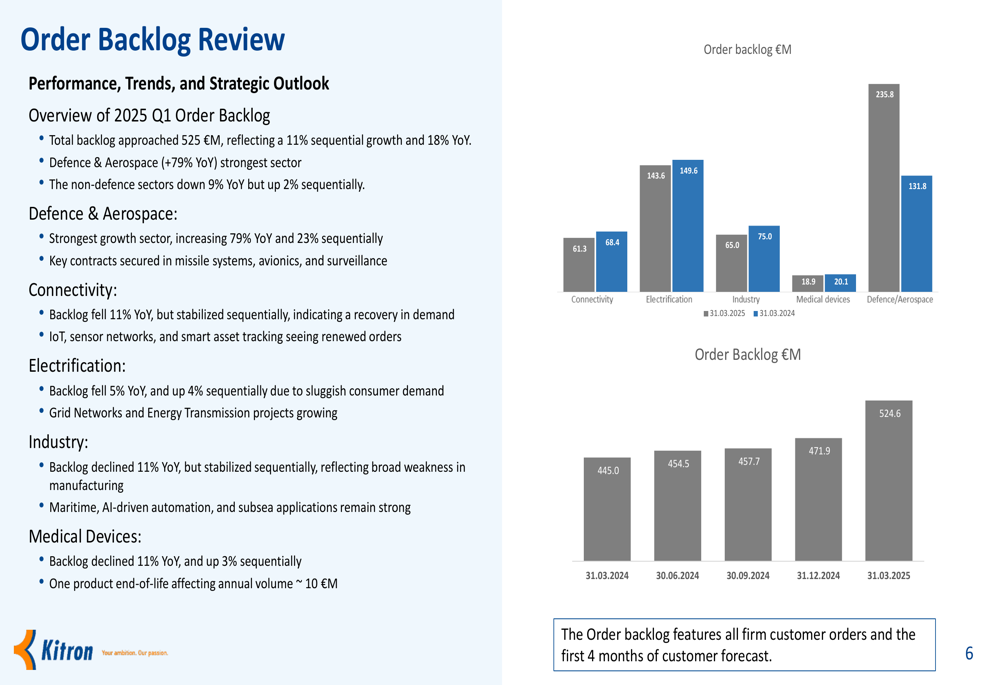

The company’s order backlog grew to €524.8 million, representing an 11% sequential increase and a robust 17.9% year-over-year growth. This strong backlog provides visibility for future revenue and supports the company’s 2025 outlook.

CEO Peter Nelson emphasized during the earnings call that "Defence and aerospace continues to be a strategic cornerstone for us," noting that the company is seeing "early signs of momentum rebuilding" across its business segments.

Sector Performance Analysis

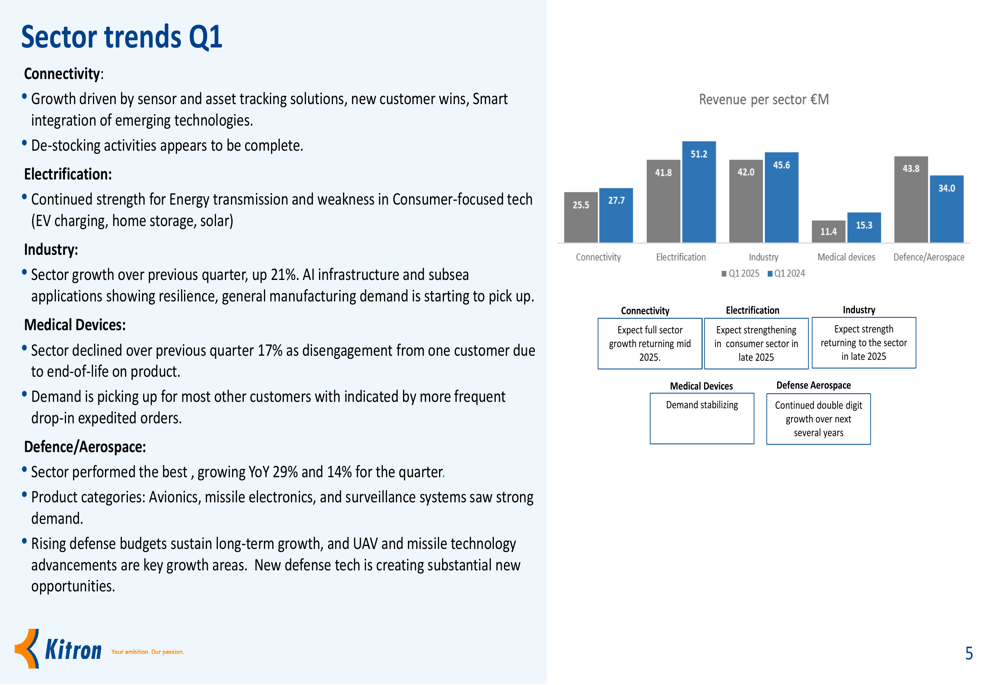

Kitron’s performance varied significantly across its business sectors, with Defence & Aerospace emerging as the clear standout. This sector grew 29% year-over-year and 14% quarter-over-quarter, driven by increased NATO investments and significant contract wins.

The following chart illustrates the revenue breakdown by sector, comparing Q1 2025 with Q1 2024:

While Defence & Aerospace showed strong growth, other sectors displayed mixed results. The Connectivity sector showed modest growth driven by sensor and asset tracking solutions. Electrification continued to demonstrate strength in energy transmission applications but weakness in consumer-focused technologies. The Industry sector grew 21% over the previous quarter, while Medical (TASE:BLWV) Devices declined 17% sequentially due to end-of-life products, though demand is now stabilizing.

The order backlog analysis further highlights the dominance of the Defence & Aerospace sector, which saw a remarkable 79% year-over-year increase:

Strategic Initiatives & Outlook

Kitron secured significant contract wins in the Defence & Aerospace sector during Q1, totaling €76 million with key customers including Kongsberg Defence & Aerospace and Thales (EPA:TCFP). These contracts cover Joint Strike Missile (JSM), Naval Strike Missile (NSM), communications and air defence systems, and optical assemblies for UAVs and drones.

The company is strategically expanding its defence production capabilities with five sites focused on this sector and an additional EU site undergoing accreditation. Kitron highlighted its flexible and rapid scalability in production, with capability to triple output across EU and U.S. operations. The Norway operations ramp-up is progressing well, targeting a 50% increase in defence volumes compared to last year.

The following slide summarizes the key takeaways from Q1 2025 and provides the outlook for the full year:

For the full year 2025, Kitron expects revenue between €640-710 million and EBIT between €47-65 million. The company anticipates higher margins in upcoming quarters, driven by a recovery in the electrification sector and continued growth in defence revenue.

Financial Position & Dividend

Kitron maintained a solid financial position with improved ratios compared to the previous year. Net interest-bearing debt (NIBD) decreased to €108.2 million from €123.1 million in Q1 2024, resulting in a net gearing ratio of 0.52 compared to 0.65 last year. The equity ratio improved to 36.3% from 33.4% in the same period last year.

The company’s cash flow performance was particularly strong, with operating cash flow of €12.1 million compared to €8.5 million in Q1 2024. This represents approximately 70% of EBITDA, demonstrating efficient cash conversion.

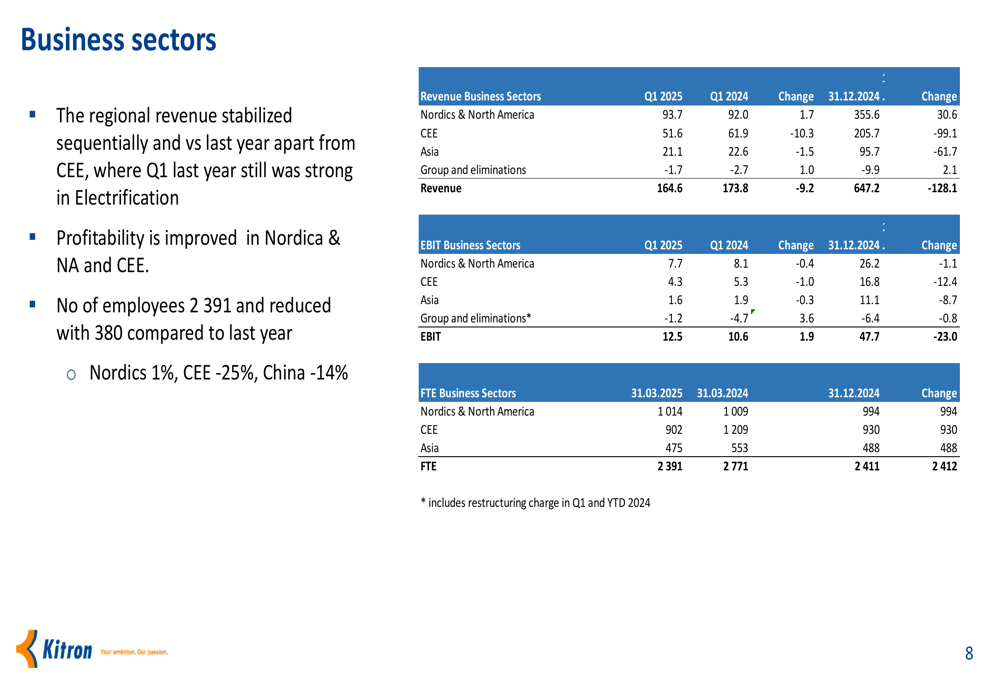

Kitron’s regional performance showed variations, with the Nordics & North America segment generating the highest revenue at €93.7 million, followed by Central and Eastern Europe (CEE) at €51.6 million and Asia at €21.1 million:

The company proposed a dividend of 0.35 NOK per share, reflecting confidence in its financial stability and commitment to shareholder returns despite the mixed quarterly results.

While Kitron faces challenges including global economic uncertainties, trade wars, and potential market saturation in non-defence sectors, its strategic focus on the defence and aerospace sector appears to be paying dividends. The company’s improved profitability metrics and strong order backlog provide a solid foundation for growth in the coming quarters, particularly as the semiconductor oversupply issues resolve and customer demand normalizes across sectors.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.