Gold scales new record high; nears $4,200/oz on Fed easing bets, trade tensions

Introduction & Market Context

Koppers Holdings Inc . (NYSE:KOP) reported its first quarter 2025 results on May 9, showing improved profitability metrics despite an overall revenue decline. The market responded positively to the results, with the stock rising 3.44% to close at $27.06, reflecting investor confidence in the company’s cost management capabilities and strategic direction.

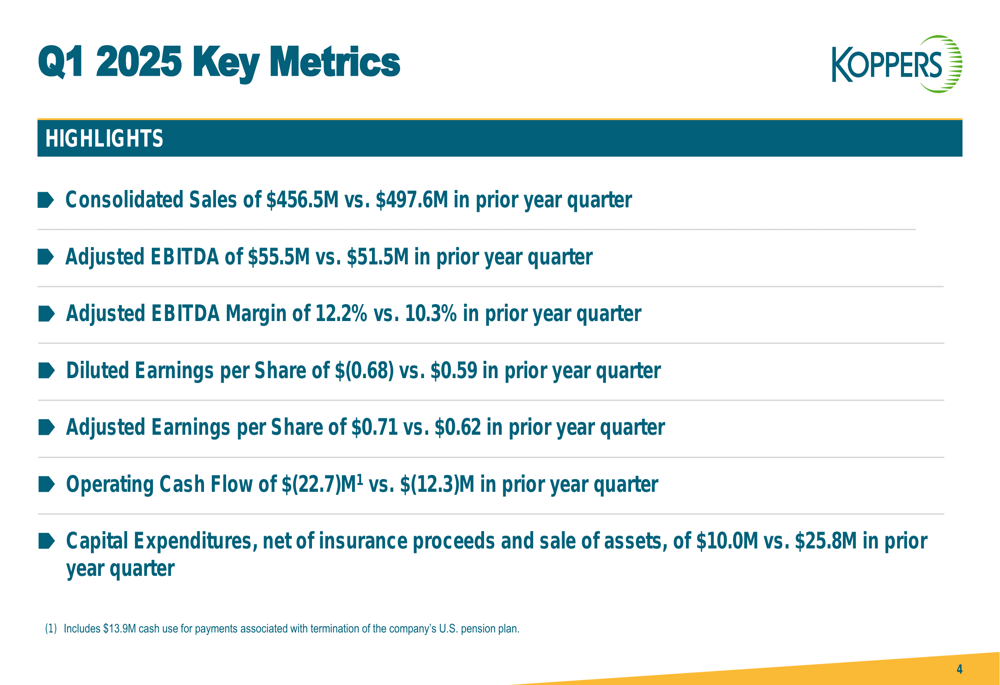

The infrastructure products and services provider demonstrated resilience in a challenging economic environment, with adjusted earnings per share exceeding analyst expectations. According to the earnings call transcript, Koppers reported adjusted EPS of $0.71, significantly outperforming the forecasted $0.56, while revenue fell short of expectations at $456.5 million versus an anticipated $488 million.

As shown in the following summary of key financial metrics, Koppers managed to improve profitability despite the revenue decline:

Quarterly Performance Highlights

Koppers’ first quarter results revealed a mixed performance across its three business segments. While consolidated sales decreased by 8.3% year-over-year to $456.5 million, the company successfully improved its adjusted EBITDA by 7.8% to $55.5 million, resulting in an adjusted EBITDA margin expansion from 10.3% to 12.2%.

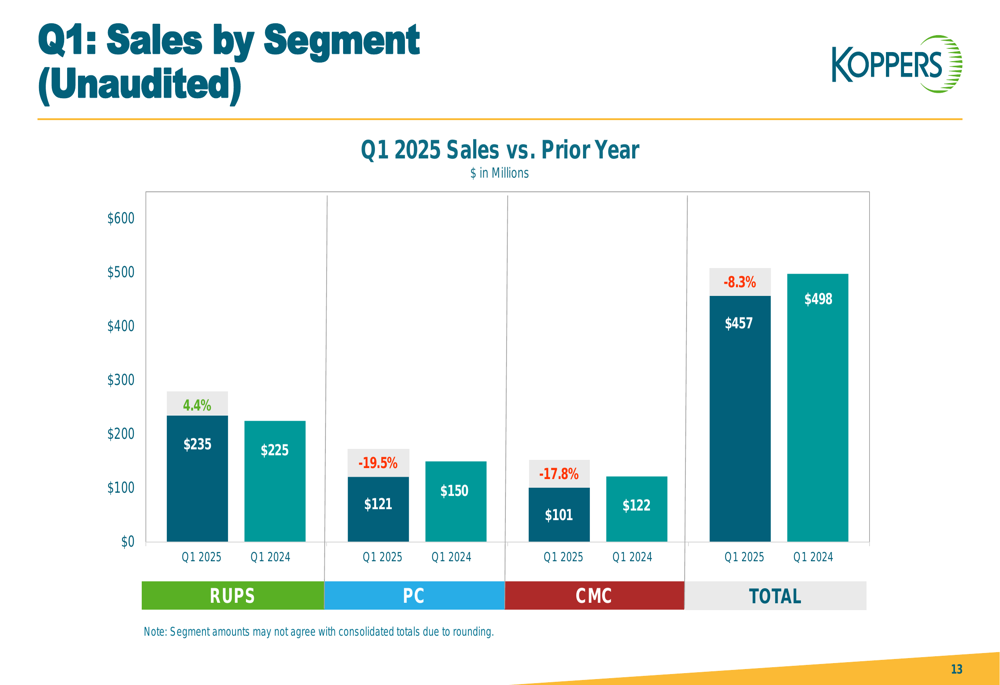

The segment breakdown shows divergent performance, with the Railroad and Utility Products and Services (RUPS) segment delivering strong results while the Performance Chemicals (PC) and Carbon Materials and Chemicals (CMC) segments experienced significant sales declines:

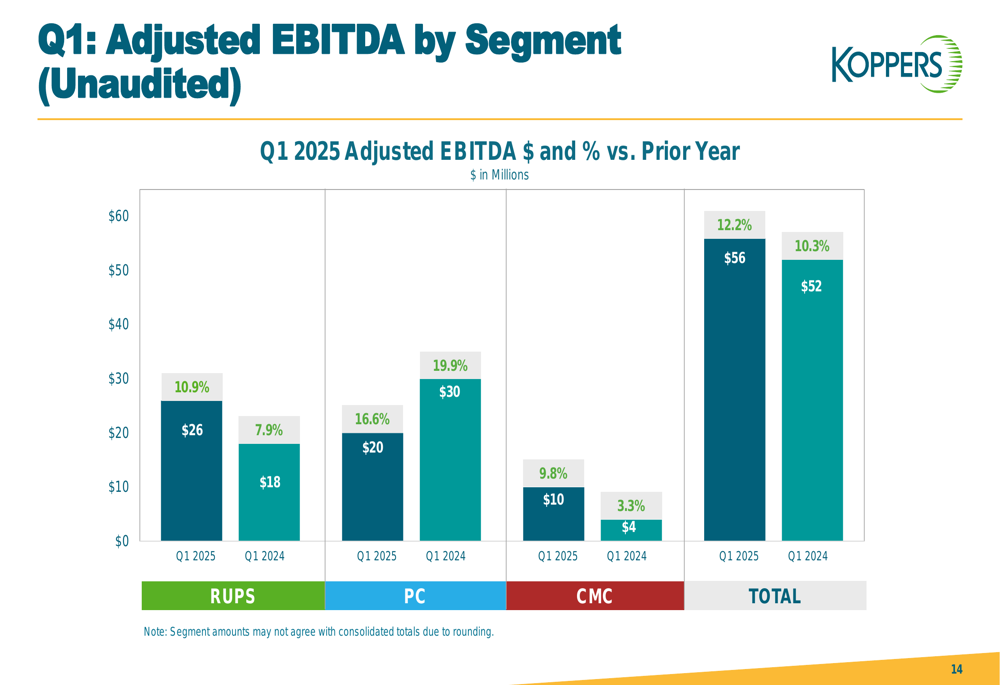

Despite the sales challenges in two segments, Koppers managed to improve profitability in both the RUPS and CMC segments, with only the PC segment showing a decline in adjusted EBITDA:

Detailed Financial Analysis

The RUPS segment emerged as the strongest performer in Q1 2025, with sales increasing by 4.4% to $235 million and adjusted EBITDA surging by 44.4% to $26 million. This improvement was primarily driven by higher volumes in the Class I crosstie business, price increases of $4.6 million, and a 9% increase in domestic utility poles volumes following the Brown Wood acquisition. The segment also benefited from increased activity in railroad bridge services and lower operating expenses in the crossties business.

The Performance Chemicals segment faced significant headwinds, with sales declining by 19.5% to $121 million and adjusted EBITDA falling by 33.3% to $20 million. This decline was attributed to a 21.5% reduction in volumes of residential and industrial preservatives in the Americas, market share shifts in the U.S., lower activity due to winter weather, and a $2.4 million unfavorable impact from foreign currency. The segment’s profitability was further impacted by higher raw material costs, though partially offset by $3.7 million in lower logistics and SG&A expenses.

The Carbon Materials and Chemicals segment showed remarkable profitability improvement despite a 17.8% sales decline to $101 million. Adjusted EBITDA for the segment increased by 150% to $10 million, driven by $7.0 million in lower raw material and allocated SG&A expenses, favorable sales mix, and the absence of a plant outage that affected the prior year period. The sales decrease was primarily due to $10.8 million in volume decreases for phthalic anhydride as production was ramped down, lower sales prices for carbon pitch globally, and a $2.3 million unfavorable impact from foreign currency.

Strategic Initiatives

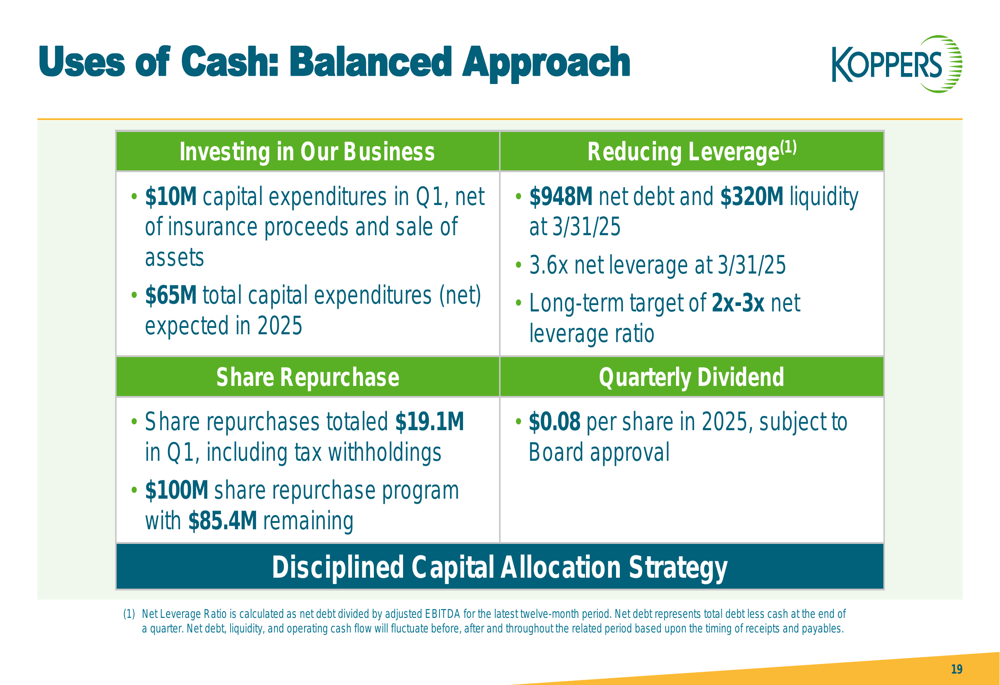

Koppers continued to execute its balanced capital allocation strategy in Q1 2025, focusing on business investment, share repurchases, debt reduction, and shareholder returns:

The company’s commitment to sustainability was highlighted by its recognition on USA Today’s Climate Leaders list for the third consecutive year and the CSX (NASDAQ:CSX) Chemical Safety Excellence Award for zero non-accidental releases in 2024. These achievements underscore Koppers’ focus on environmental stewardship and operational excellence.

Safety performance also showed improvement, with 31 out of 41 facilities remaining accident-free during the quarter. The company reported a 16% increase in leading safety activities, a 10% decrease in recordable injury rate, and a 50% decrease in serious safety incidents compared to the previous year.

As part of its strategic evolution, Koppers ceased primary phthalic anhydride production in April 2025, a move that aligns with its focus on core businesses and operational efficiency. The company also extended a long-term raw material supply agreement in Australia, securing important supply chain stability.

Forward-Looking Statements

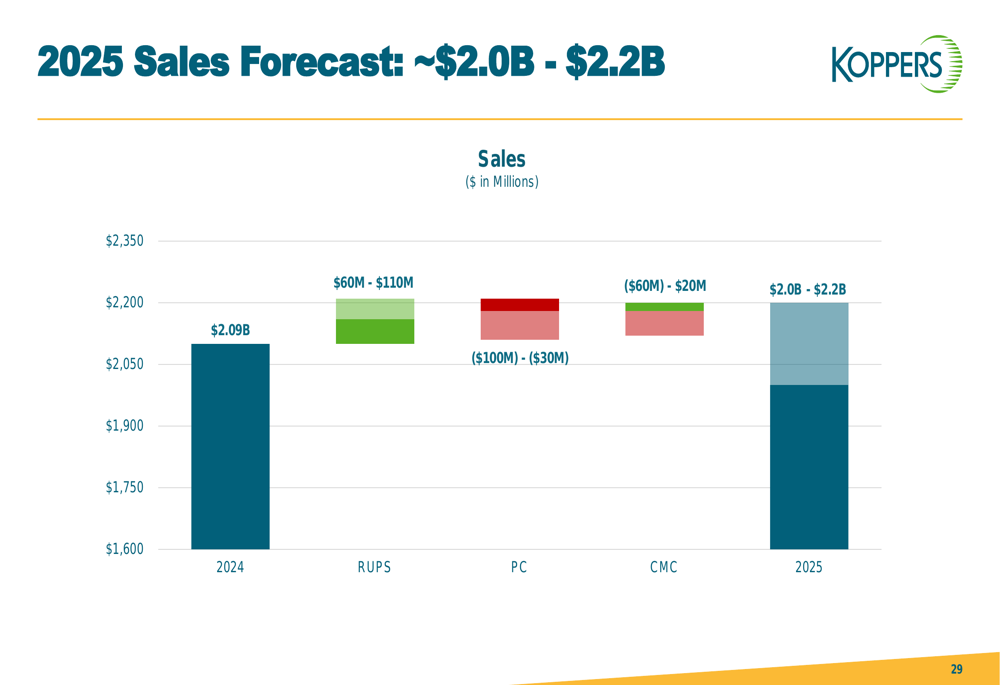

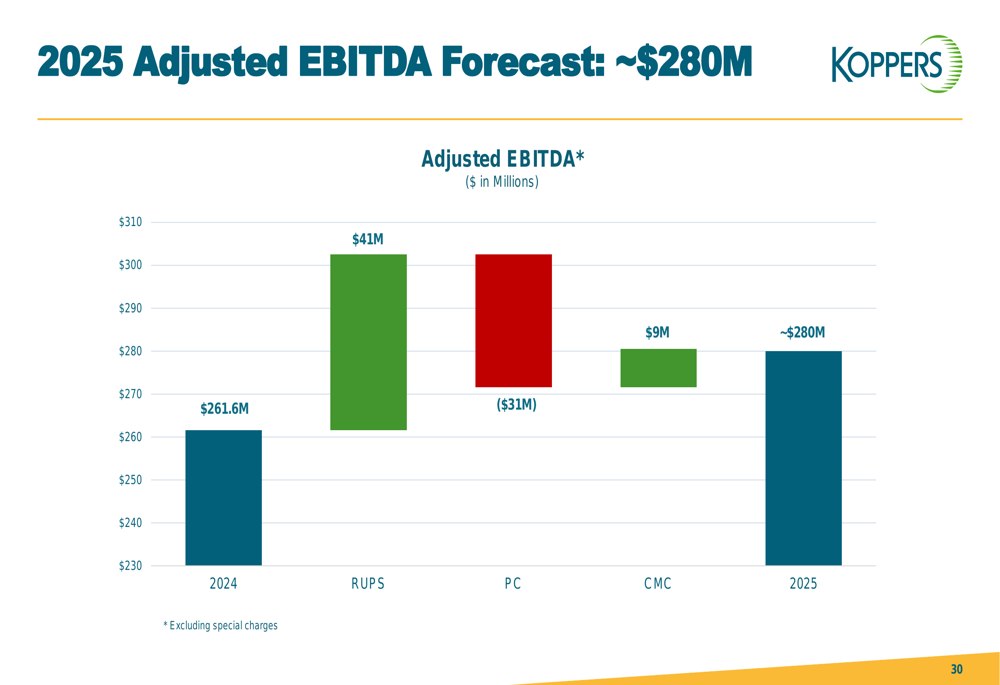

Despite the mixed Q1 results, Koppers maintained its full-year 2025 guidance, projecting consolidated sales of $2.0-2.2 billion and adjusted EBITDA of approximately $280 million. The company’s sales forecast by segment shows expected growth in RUPS offset by declines in the PC and CMC segments:

The adjusted EBITDA forecast indicates that the anticipated RUPS segment improvement will more than offset the expected decline in the PC segment, while the CMC segment is also projected to contribute positively to overall profitability:

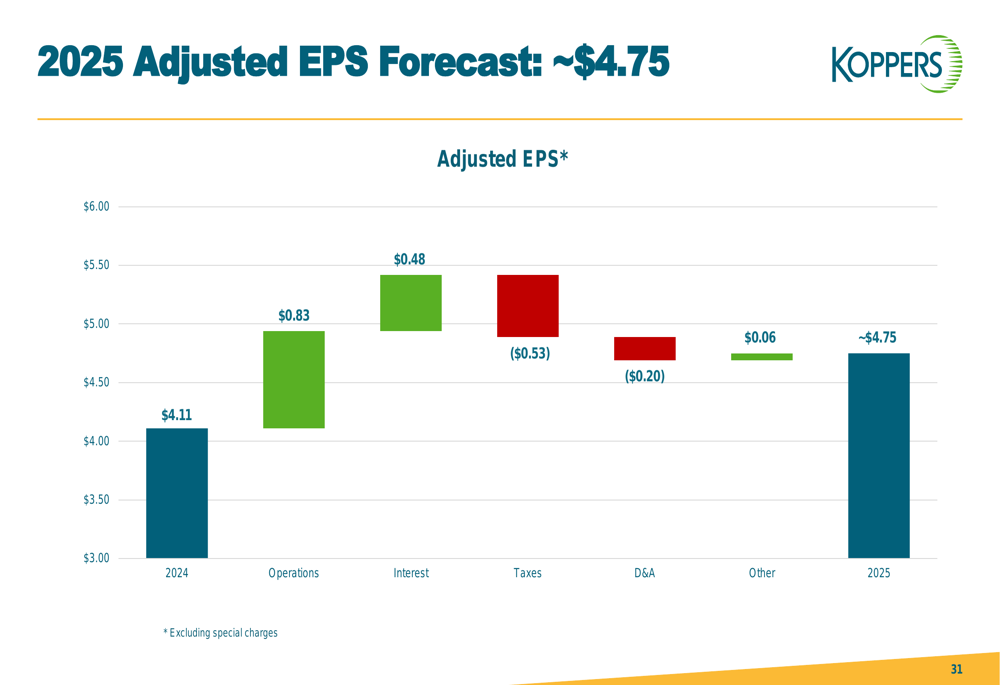

Koppers expects adjusted earnings per share of approximately $4.75 for 2025, representing a significant improvement from $4.11 in 2024:

Management expressed cautious optimism about the business outlook, noting that while demand started the year solid for the PC segment, it lost momentum as the quarter progressed. The company acknowledged concerns that economic uncertainty could dampen demand throughout 2025, with the PC segment being most exposed to tariff activity.

For the RUPS segment, Koppers expects Q2 to look similar to Q1, with a pickup anticipated in the second half of the year. The company remains bullish on long-term demand dynamics due to increasing demand for power. Meanwhile, most CMC end markets are expected to remain challenging throughout 2025, with profit improvement primarily coming from lower operating costs.

CEO Leroy Ball (NYSE:BALL) expressed confidence despite market challenges, stating, "Despite the extreme uncertainty that exists in the markets right now, we are fighting our way through it and we’ll come out the other side in an even stronger position." This sentiment, combined with the company’s maintained guidance and improved profitability metrics, suggests management’s belief in Koppers’ resilience and strategic positioning for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.