BigBear.ai appoints Sean Ricker as chief financial officer

Introduction & Market Context

Koppers Holdings Inc (NYSE:KOP) released its Q2 2025 earnings presentation on August 8, 2025, revealing mixed results as the company navigated challenging market conditions. Despite achieving improved EBITDA margins, the wood treatment and carbon chemicals company reported declining sales across all segments and lowered its full-year guidance. The market reacted negatively to the news, with Koppers stock falling 13.95% to $28.48 in morning trading.

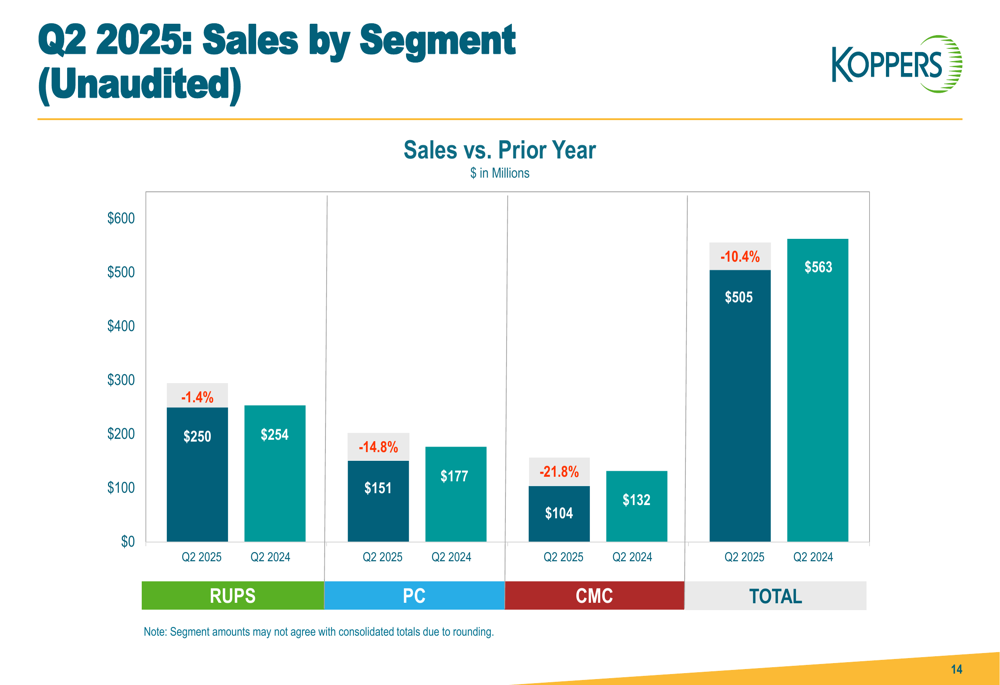

The company reported Q2 sales of $504.8 million, down 10.4% from $563.2 million in Q2 2024, while maintaining adjusted EBITDA at $77.1 million (15.3% margin) compared to $77.5 million (13.8% margin) in the year-ago quarter. This margin improvement, achieved despite revenue pressure, highlights the company’s focus on operational efficiency and cost management.

Quarterly Performance Highlights

Koppers’ Q2 performance showed significant variations across its three business segments. As shown in the following sales breakdown by segment, all business units experienced year-over-year declines:

The Railroad and Utility Products and Services (RUPS) segment saw the smallest decline at 1.4%, while Performance Chemicals (PC) and Carbon Materials and Chemicals (CMC) experienced more substantial drops of 14.8% and 21.8%, respectively. The company attributed these declines to lower volumes in the Class I crosstie business, market share shifts in the U.S. preservative market, and the planned discontinuation of phthalic anhydride production.

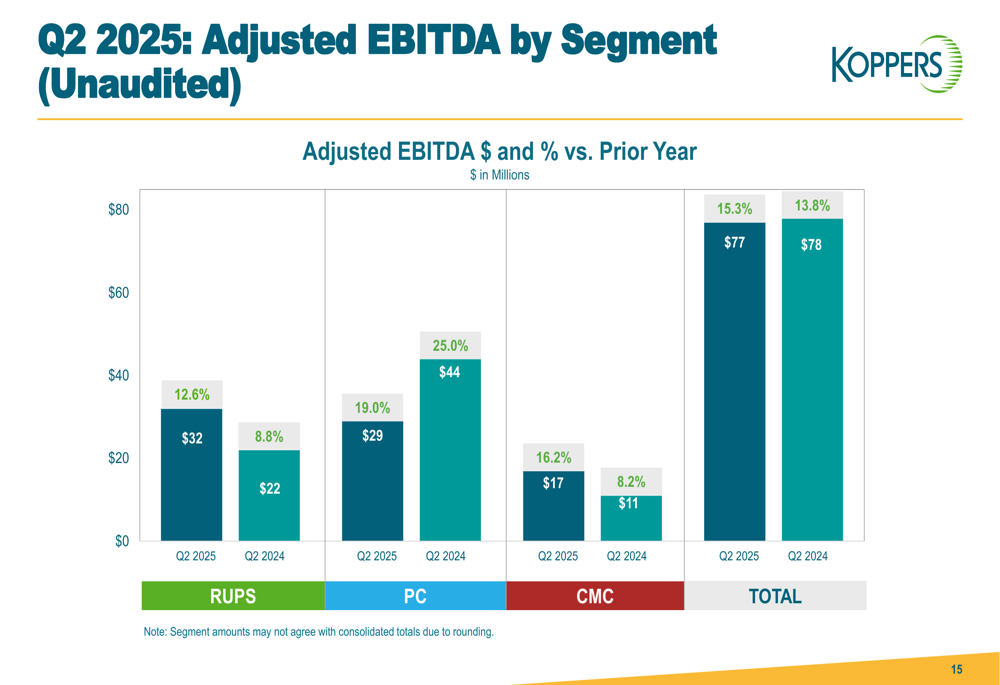

Despite the sales challenges, Koppers achieved notable improvement in profitability metrics, particularly in the RUPS and CMC segments:

The RUPS segment’s adjusted EBITDA increased by 45% to $32 million, driven by lower costs, reduced SG&A expenses, and net sales price increases. Similarly, the CMC segment’s adjusted EBITDA rose by 55.6% to $17 million, benefiting from lower raw material costs and operating expenses. However, the PC segment’s adjusted EBITDA declined by 35.2% to $29 million due to higher raw material costs and lower sales volumes.

Strategic Initiatives

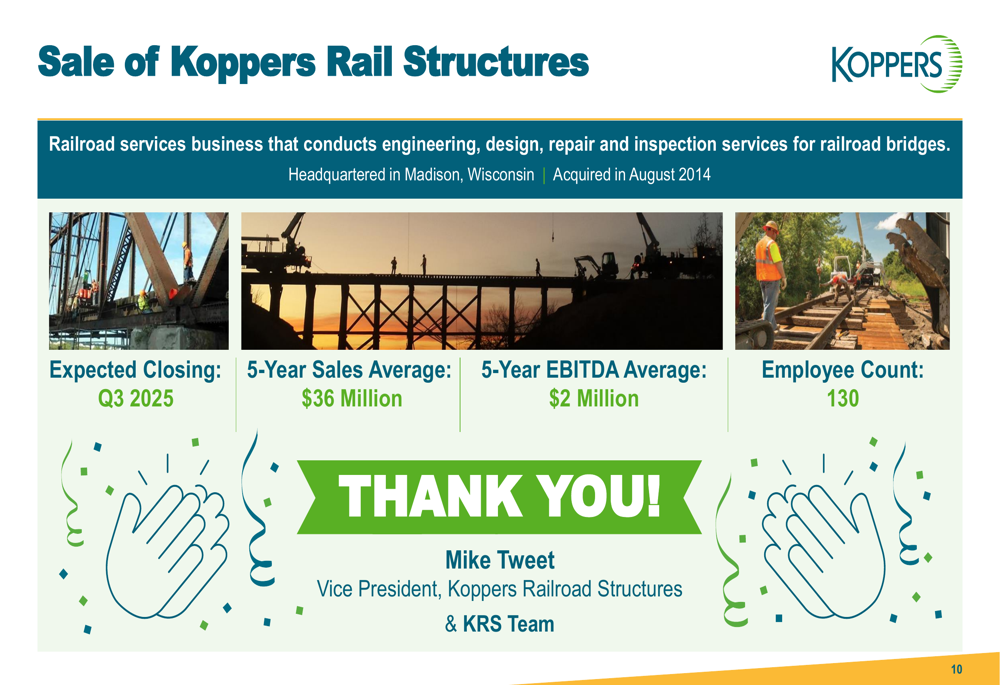

Koppers highlighted several strategic initiatives aimed at improving profitability and operational efficiency. The company announced the expected sale of its Railroad Structures business, which conducts engineering, design, repair, and inspection services for railroad bridges. The divestiture, expected to close in Q3 2025, aligns with Koppers’ focus on its core operations.

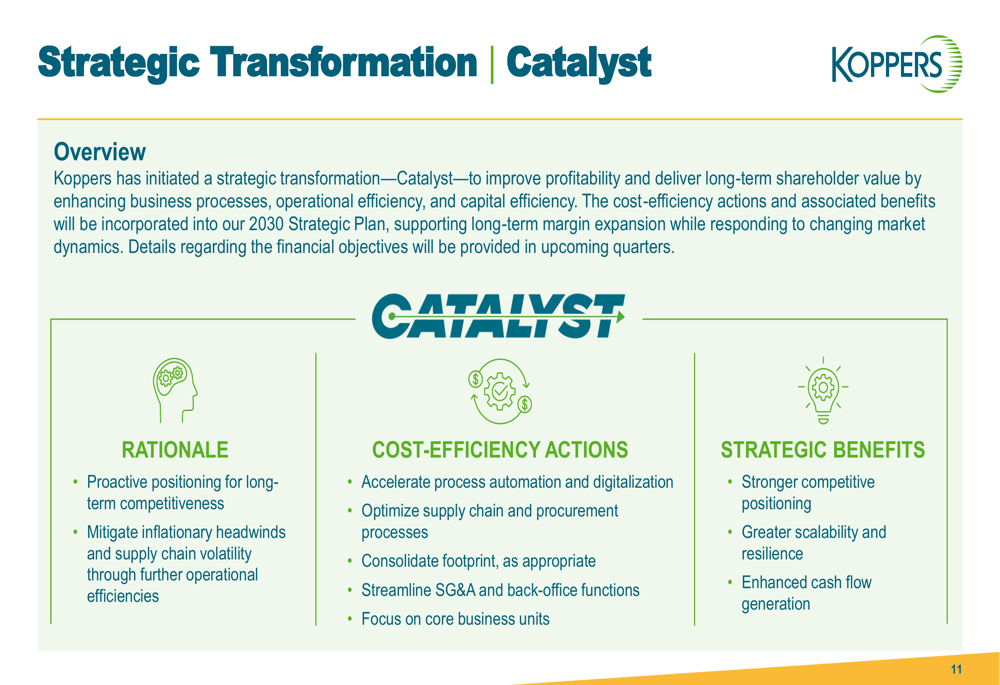

Additionally, Koppers launched its "Catalyst" transformation initiative, designed to enhance business processes, operational efficiency, and capital efficiency. This strategic program aims to position the company for long-term competitiveness and mitigate inflationary headwinds and supply chain volatility.

The company also reported significant progress in its cost-reduction efforts, including a 13% reduction in SG&A expenses year-to-date compared to the prior year, a 14-month consecutive reduction in headcount (11% lower than April 2024), and the early cessation of phthalic anhydride production.

Capital Allocation Strategy

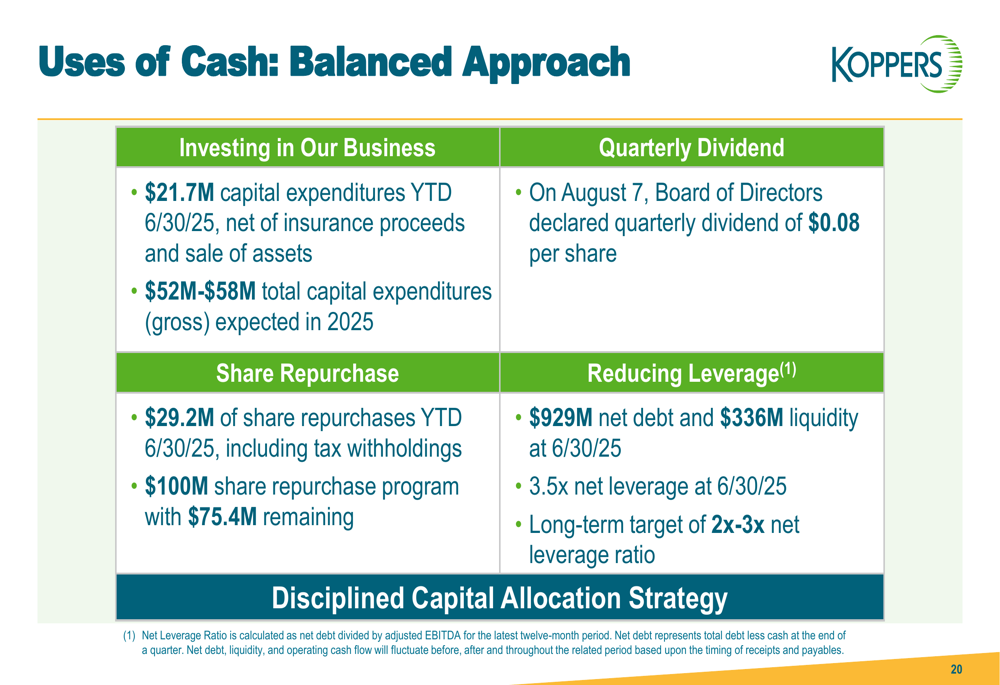

Koppers presented a balanced approach to capital allocation, focusing on business investment, shareholder returns, and debt reduction. The company generated over $50 million in cash flow during Q2 and deployed $24 million to dividends, share repurchases, and debt reduction.

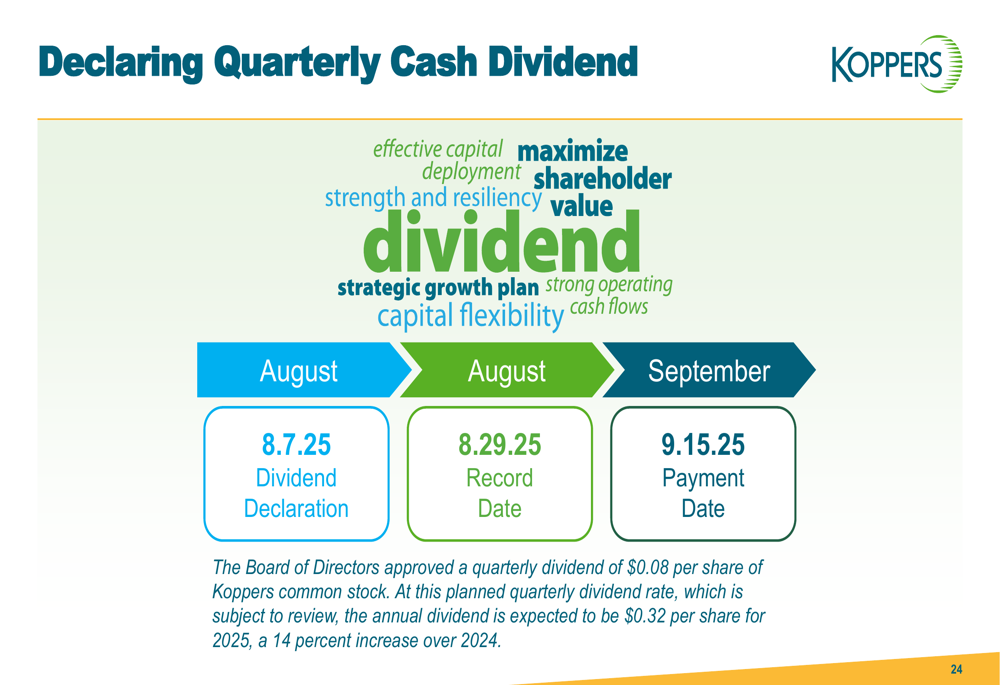

On August 7, Koppers’ Board of Directors declared a quarterly dividend of $0.08 per share, payable on September 15, 2025. At this rate, the annual dividend is expected to be $0.32 per share for 2025, representing a 14% increase over 2024.

The company also announced the extension of its $800 million revolving credit facility to January 9, 2030, providing additional financial flexibility. As of June 30, 2025, Koppers reported net debt of $929 million and liquidity of $336 million, with a net leverage ratio of 3.5x (compared to its long-term target of 2-3x).

Forward-Looking Statements

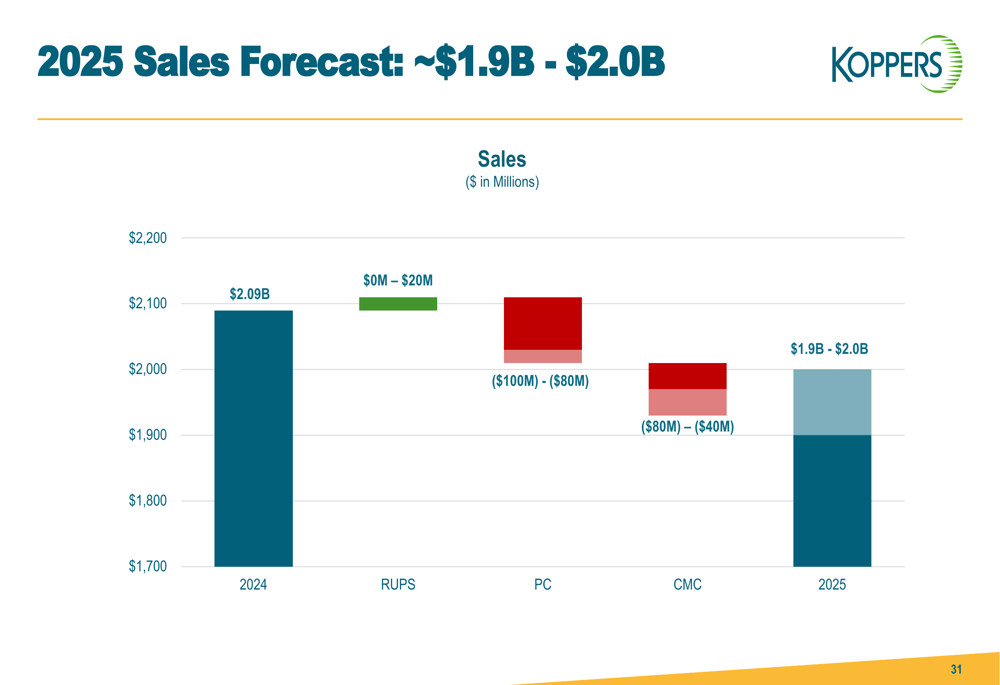

In response to challenging market conditions, Koppers revised its full-year 2025 guidance downward. The company now projects sales of approximately $1.9-2.0 billion, down from its previous forecast of $2.0-2.2 billion provided in Q1 2025.

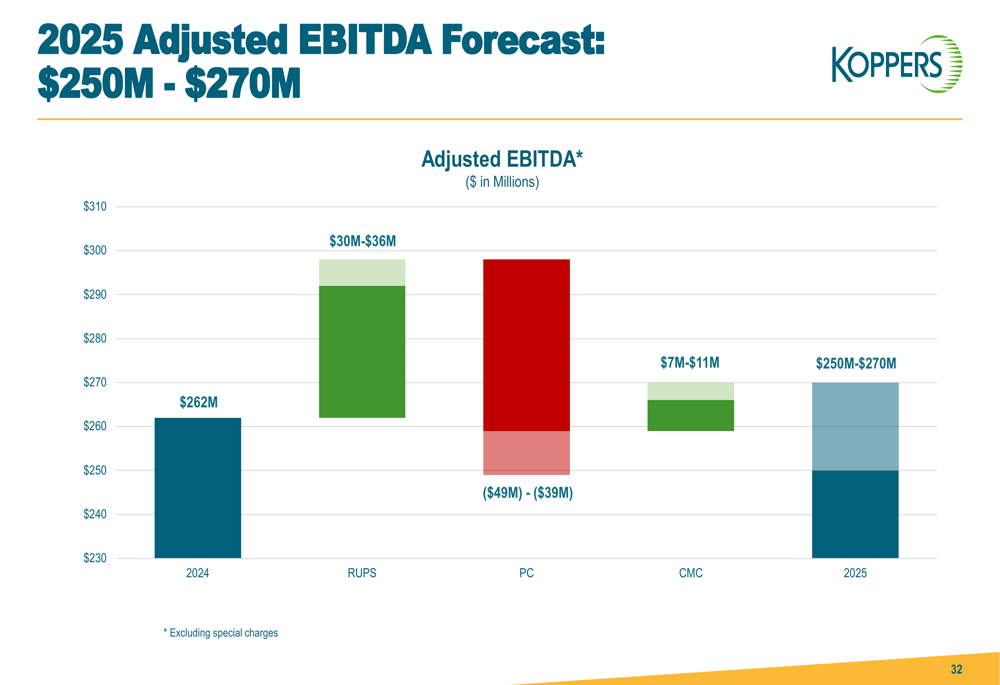

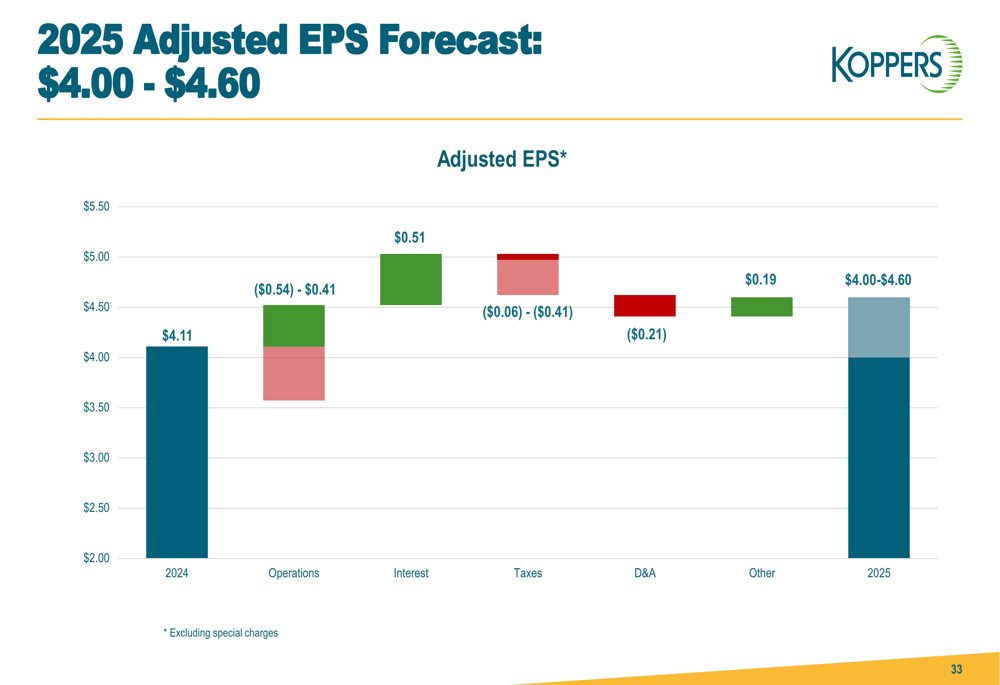

Similarly, the adjusted EBITDA forecast was lowered to $250-270 million from the previous guidance of $280 million, and the adjusted EPS forecast was reduced to $4.00-4.60 from $4.75.

The revised guidance reflects softer demand across all business segments, with the Performance Chemicals segment particularly affected by tariff impacts (approximately $2 million in Q2) and market share shifts in the U.S. The company noted that while utility pole volumes showed improvement, the pace was slower than expected, and Class I railroad demand is anticipated to be lower in the second half of the year than previously indicated.

Despite these challenges, Koppers highlighted several positive developments, including its recognition as one of "America’s Best Companies 2025" by TIME magazine, based on employee satisfaction, revenue growth, and sustainability transparency. The company also reported improvements in safety metrics, with recordable injury rates down 3% and serious safety incidents down 71.5% compared to 2024.

Looking ahead, Koppers’ management remains focused on operational efficiency and cost management to navigate the challenging market environment. The company’s "Catalyst" transformation initiative, combined with its balanced capital allocation approach, underscores its commitment to delivering long-term shareholder value despite near-term headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.