Micron to exit server chips business in China after 2023 ban- Reuters

Introduction & Market Context

Kvika banki hf (ICE:KVIKA) reported strong second-quarter 2025 results on August 13, with pre-tax profit soaring 70.3% year-over-year to ISK 2,025 million. The bank’s shares closed at ISK 18.25, up 1.37% following the announcement, as investors responded positively to the robust financial performance and ongoing merger discussions with Arion banki.

The Q2 results reflect Kvika’s successful execution across its commercial banking, investment banking, and asset management segments, alongside strong performance in its UK operations. The bank also made significant strategic advances, including the successful launch of its mortgage product and its first EUR-denominated bond issuance.

Quarterly Performance Highlights

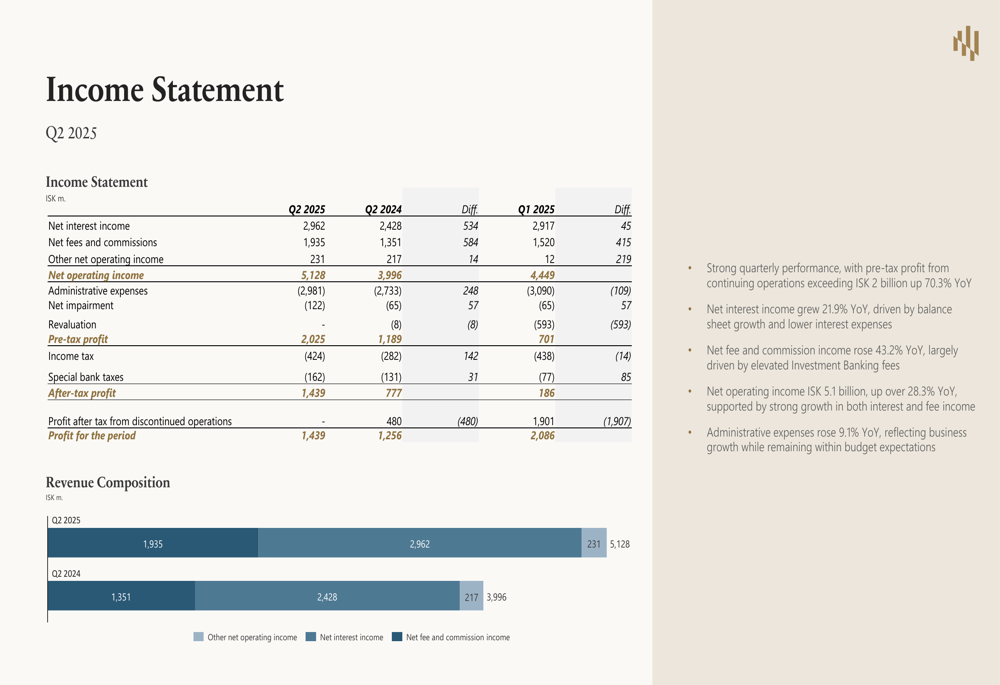

Kvika’s financial performance showed substantial improvement across key metrics in Q2 2025. Net interest income grew 21.9% year-over-year to ISK 2,962 million, while net fee and commission income surged 43.2% to ISK 1,935 million. Administrative expenses increased at a more modest pace of 9.1% to ISK 2,981 million, reflecting improved operational efficiency.

As shown in the following comprehensive income statement:

The bank’s pre-tax Return on Tangible Equity (RoTE) reached 18.5%, approaching its target of over 20%. The cost-to-core income ratio improved significantly to 60.3%, down from 70.5% in Q2 2024, demonstrating enhanced operational efficiency despite ongoing investments in growth initiatives.

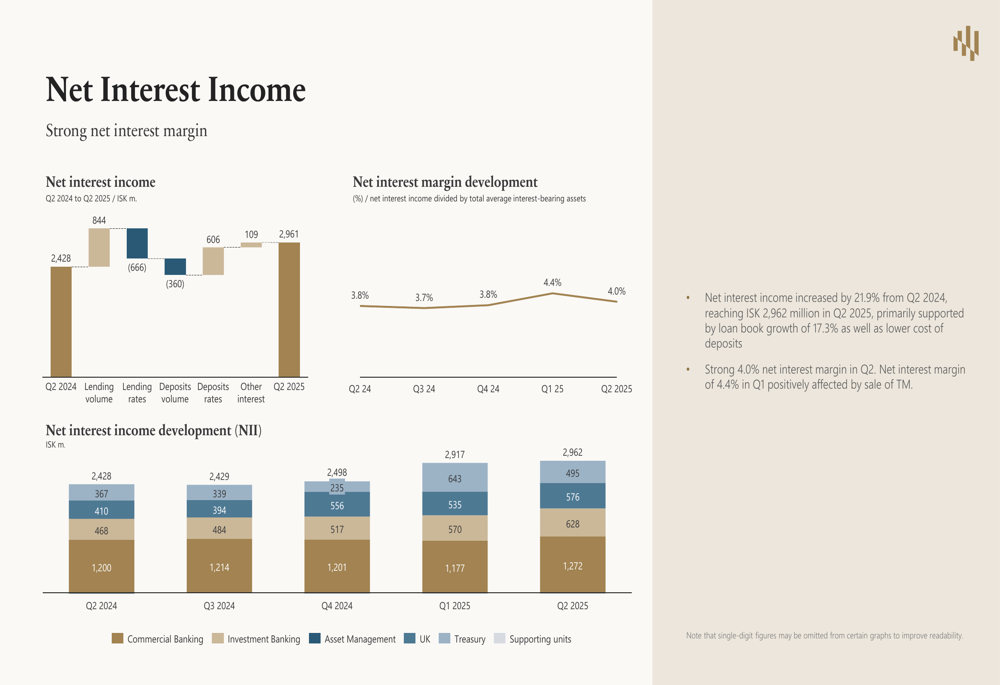

Net interest margin improved to 4.0% in Q2 2025 from 3.8% in the same period last year, driven by favorable changes in lending volumes and rates, as illustrated in this breakdown:

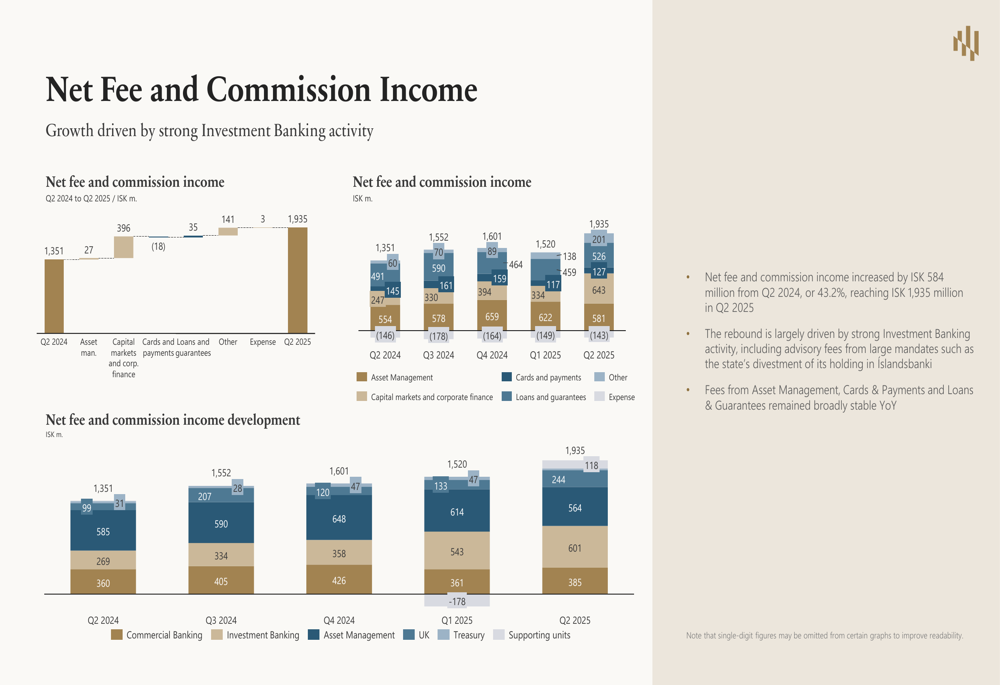

The strong growth in fee and commission income was primarily driven by increased investment banking activity, particularly in capital markets and corporate finance:

Balance Sheet Strength and Credit Quality

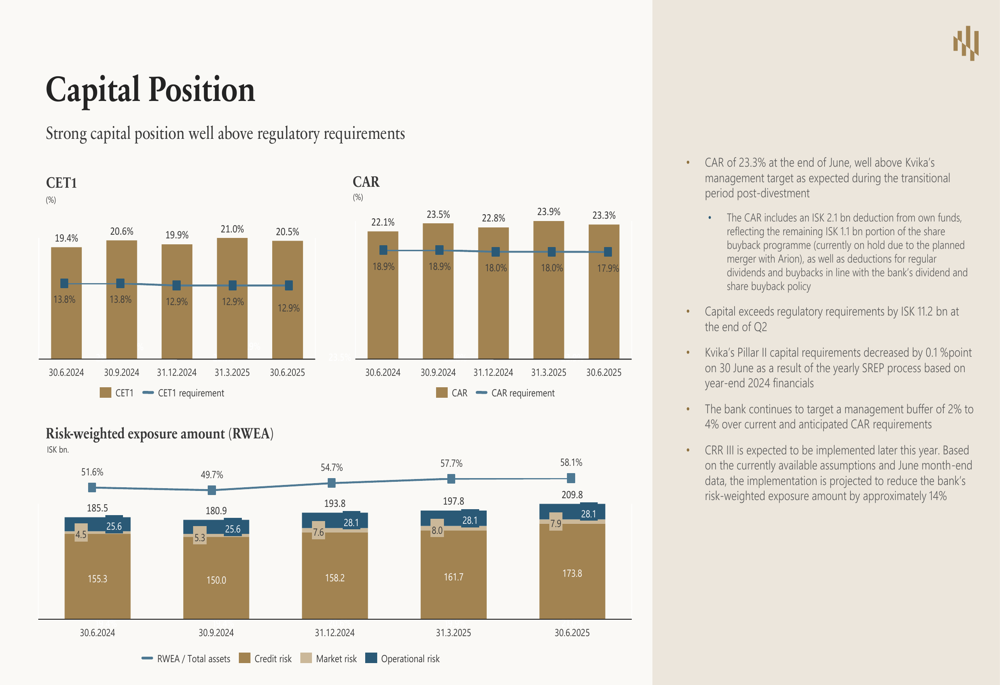

Kvika maintained a strong capital position with a Capital Adequacy Ratio (CAR) of 23.3%, well above regulatory requirements. The bank’s capital exceeds regulatory requirements by ISK 11.2 billion, providing substantial flexibility for continued growth and potential acquisitions.

The bank’s capital position remains robust as shown in this analysis:

Total assets reached ISK 361.2 billion, with 37.8% (ISK 136.6 billion) consisting of cash, non-maturing bank balances, and liquid financial instruments. This strong liquidity position supports the bank’s loan book growth strategy while maintaining risk control.

Credit quality remained solid, with Stage 3 loans declining from 2.5% to 2.3% on a net loan book basis during the quarter. The bank’s liquidity coverage ratio (LCR) stood at an impressive 910%, while the net stable funding ratio (NSFR) was strong at 160%.

Strategic Initiatives

Kvika launched its Auður Heima mortgage product in late May, which quickly gained significant traction. By quarter-end, mortgage applications totaled approximately ISK 18 billion, with ISK 3 billion already disbursed in Q2 and a pipeline of ISK 15 billion being processed. This successful entry into the mortgage market represents a strategic expansion of Kvika’s retail banking operations.

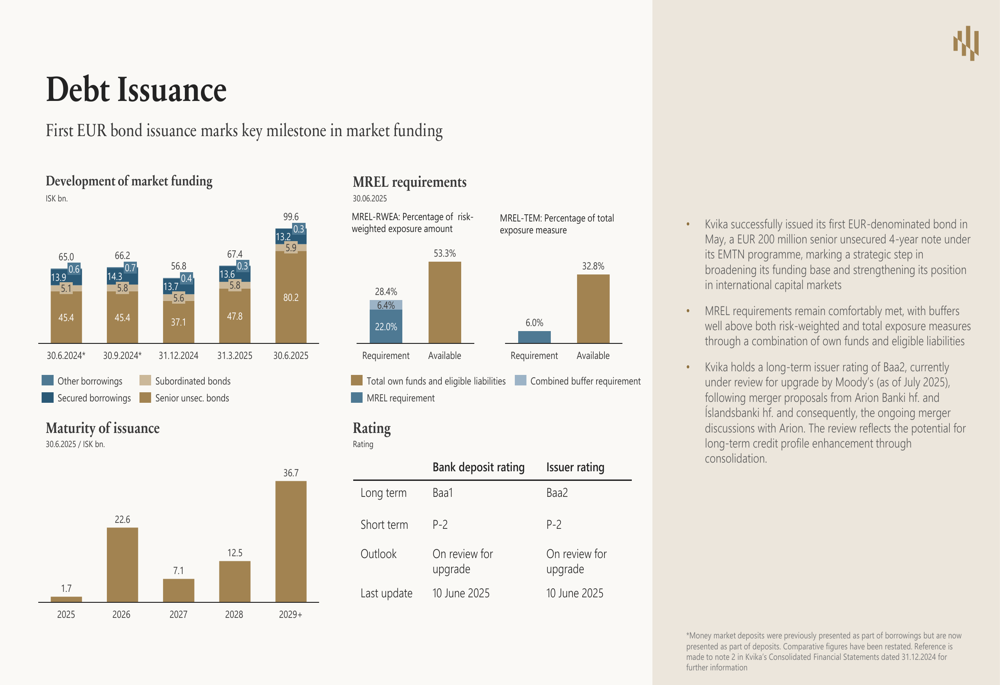

In a significant funding milestone, Kvika successfully issued its first EUR-denominated bond in May, a EUR 200 million senior unsecured 4-year note. This issuance strengthens and diversifies the bank’s funding mix, as illustrated in the following chart:

The bank’s asset management division established a new ISK 8.5 billion credit fund, ACF V slhf., with ISK 6 billion already committed to new loans by the end of July. Assets under management increased by ISK 11 billion from the end of the first quarter, reaching ISK 453 billion at the end of June 2025.

Merger Progress with Arion Banki

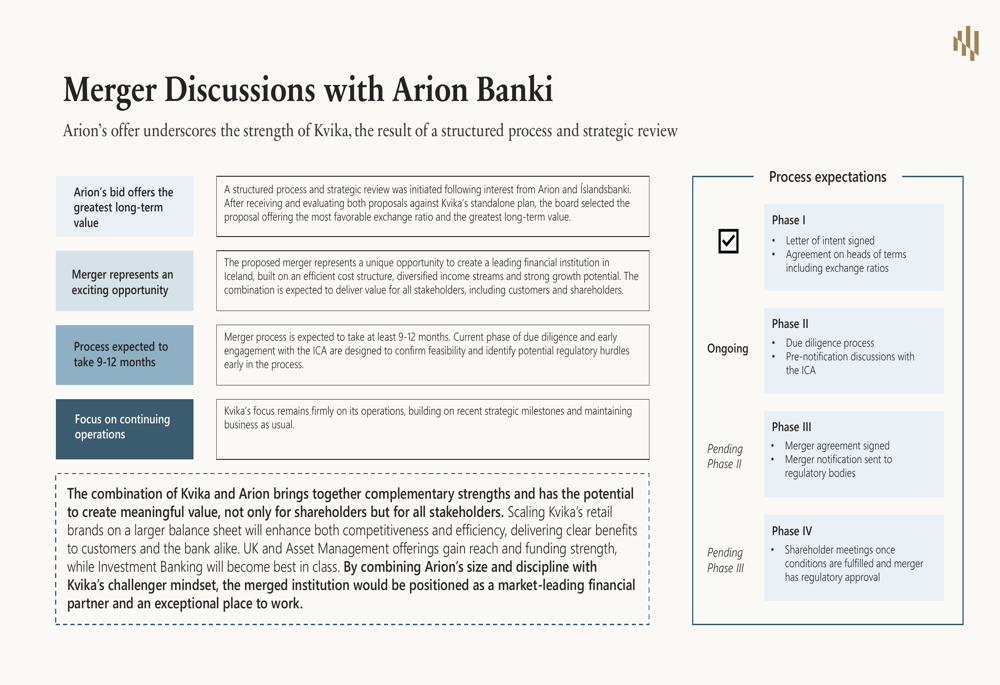

A key strategic development is the ongoing merger discussions with Arion banki hf. According to the presentation, Kvika’s board believes Arion’s bid offers the greatest long-term value, and the merger represents an exciting opportunity for the bank. The overall process is expected to take 9-12 months, with significant milestones anticipated before the end of the year.

The following slide outlines the merger process and timeline:

Forward-Looking Statements

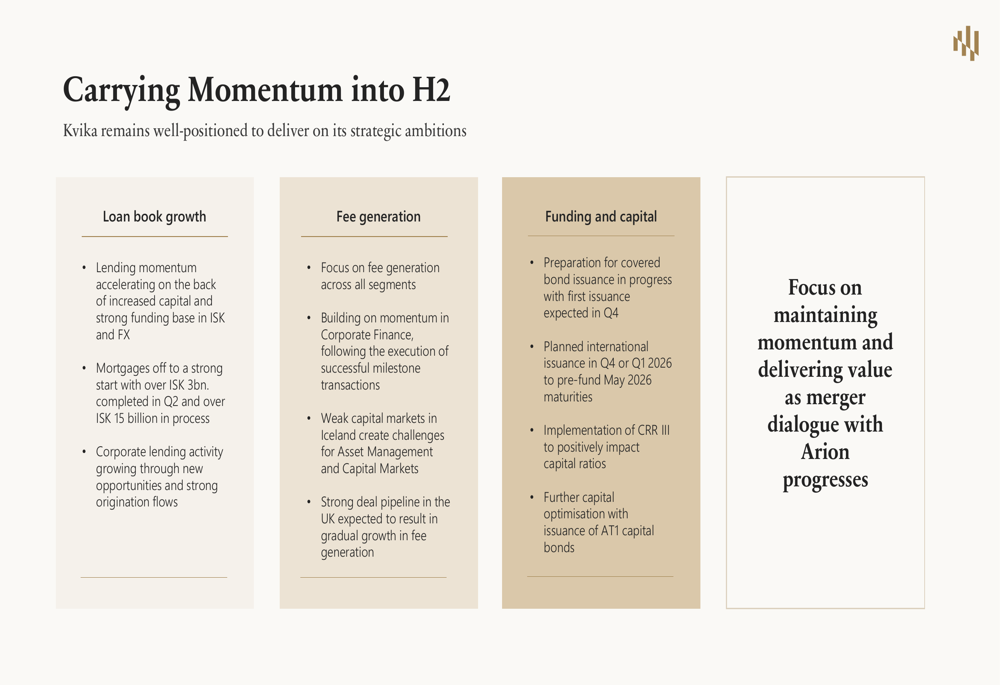

Looking ahead to the second half of 2025, Kvika plans to build on its momentum across several key areas. The bank expects accelerating lending growth, particularly in mortgages, and will focus on fee generation across all segments while building on momentum in corporate finance.

On the funding side, Kvika is preparing for covered bond issuance and planning additional international issuance. The bank outlined its strategic priorities for H2 2025 as follows:

Kvika remains committed to its financial targets, including a Return on Tangible Equity above 20% (currently at 18.5% for Q2 2025), maintaining a Capital Adequacy Ratio 200-400 basis points above regulatory requirements (currently at 540 bps), and a dividend payout ratio of 25%.

Management emphasized that while the merger dialogue with Arion progresses, the bank remains focused on maintaining momentum and delivering value to shareholders through continued execution of its growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.