Microsoft’s data-center shortages to persist longer than expected - Bloomberg

Introduction & Market Context

Kyndryl Holdings Inc (NYSE:KD) presented its first-quarter fiscal 2026 earnings on August 5, 2025, highlighting continued margin improvement despite flat revenue performance. The IT services provider’s stock fell 11.44% in premarket trading to $32.50, suggesting investors may be concerned about the company’s 2.6% constant-currency revenue decline, despite improvements in profitability metrics.

The presentation comes as Kyndryl continues its post-IBM spinoff transformation, focusing on higher-margin business while navigating a challenging macroeconomic environment. The company’s strategic initiatives in cloud services, AI implementation, and consulting appear to be gaining traction, though revenue growth remains elusive.

Quarterly Performance Highlights

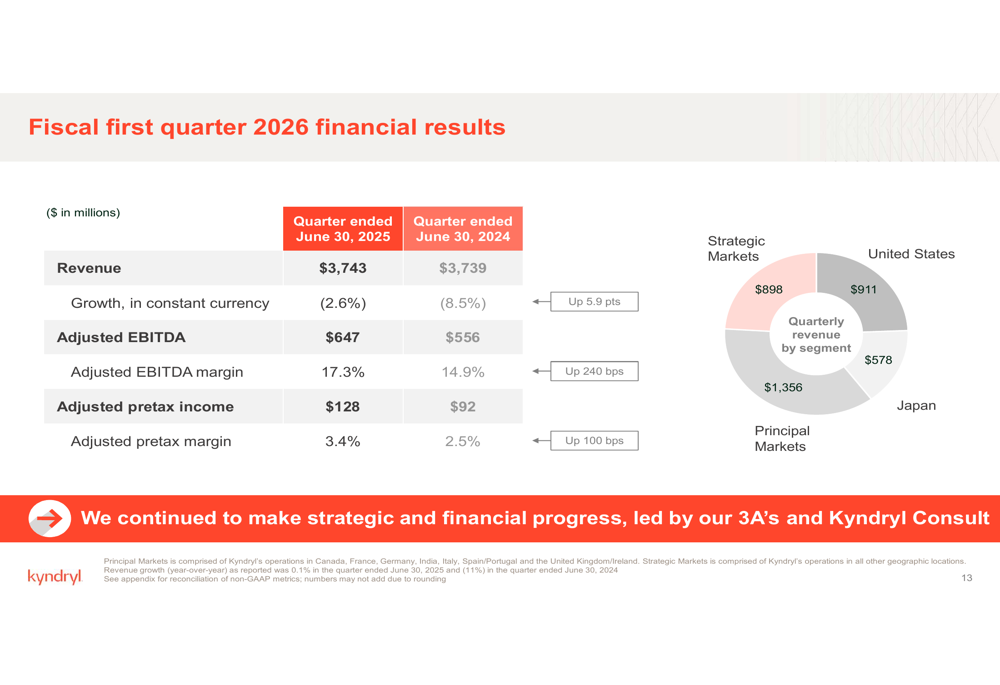

Kyndryl reported Q1 2026 revenue of $3,743 million, essentially flat compared to $3,739 million in the same quarter last year. However, in constant currency terms, revenue declined by 2.6%, though this represents an improvement from the 8.5% decline in the prior year period.

Despite revenue challenges, profitability metrics showed notable improvement. Adjusted EBITDA reached $647 million with a 17.3% margin, up from $556 million and 14.9% margin in Q1 2025. Adjusted pretax income increased to $128 million (3.4% margin) from $92 million (2.5% margin) a year ago.

As shown in the following quarterly financial results chart, revenue was distributed across Kyndryl’s geographic segments, with Principal Markets contributing $1,356 million, Japan $578 million, Strategic Markets $898 million, and the United States $911 million:

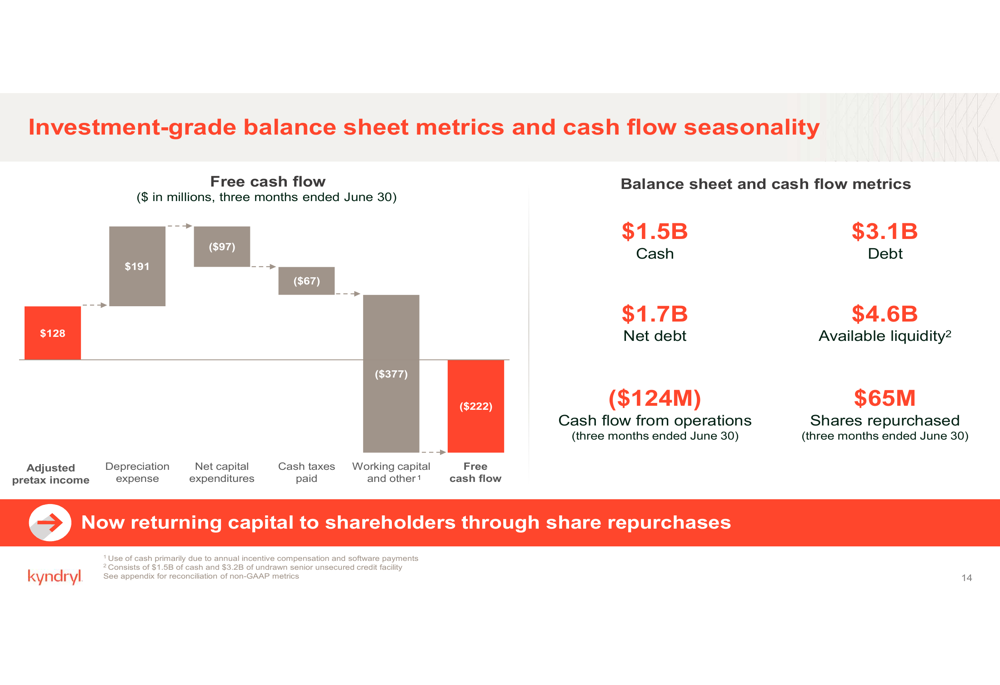

The company’s balance sheet showed $1.5 billion in cash and $3.1 billion in debt, resulting in net debt of $1.7 billion. Available liquidity stood at $4.6 billion. Kyndryl repurchased $65 million in shares during the quarter, though free cash flow was negative at ($222) million, reflecting typical seasonal patterns in the company’s business.

The following chart illustrates Kyndryl’s balance sheet metrics and cash flow seasonality:

Strategic Initiatives

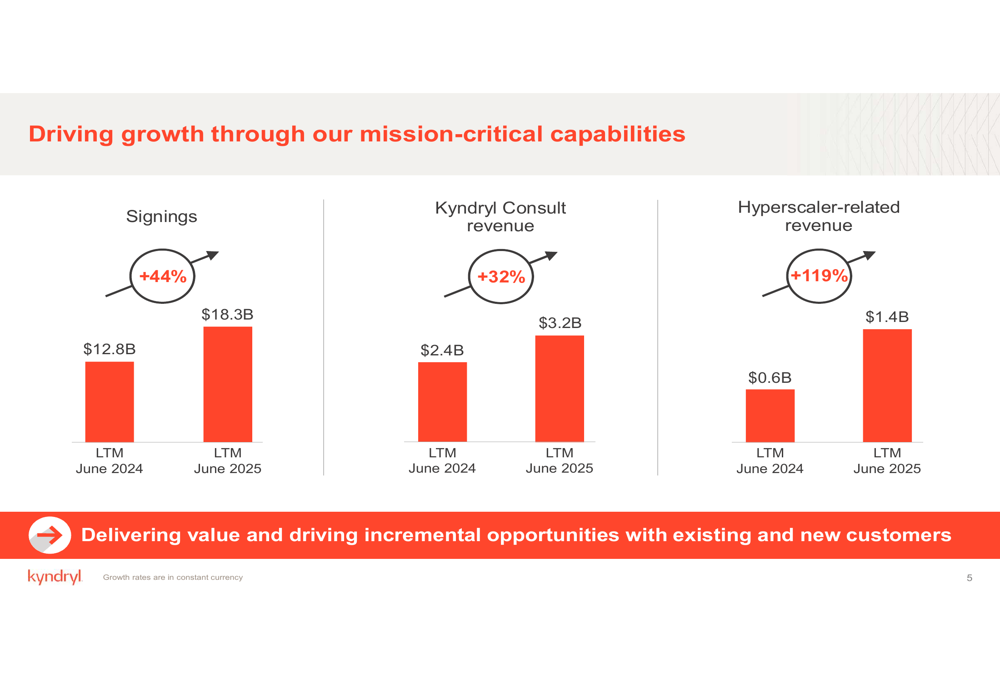

Kyndryl’s presentation emphasized three key growth areas showing significant momentum. Signings increased 44% to $18.3 billion, Kyndryl Consult revenue grew 32% to $3.2 billion, and Hyperscaler-related revenue surged 119% to $1.4 billion (all figures in constant currency, comparing LTM June 2025 to LTM June 2024).

The following chart demonstrates this growth across these strategic initiatives:

The company is placing particular emphasis on expanding Kyndryl Consult, its high-margin advisory business, which it aims to grow from 10% of revenue at the time of its 2021 spin-off to more than 25% in the coming years. This consulting arm leverages Kyndryl’s infrastructure expertise and AI capabilities to help clients modernize their IT environments.

Kyndryl highlighted two customer examples demonstrating its strategy in action. In one case, the company expanded services with a travel sector client, resulting in projected annual revenue growth exceeding 30% in a new $50 million+ contract. In another example, Kyndryl won a new industrial customer and expanded the relationship to achieve 3x projected revenue growth within twelve months of the original contract.

Forward-Looking Statements

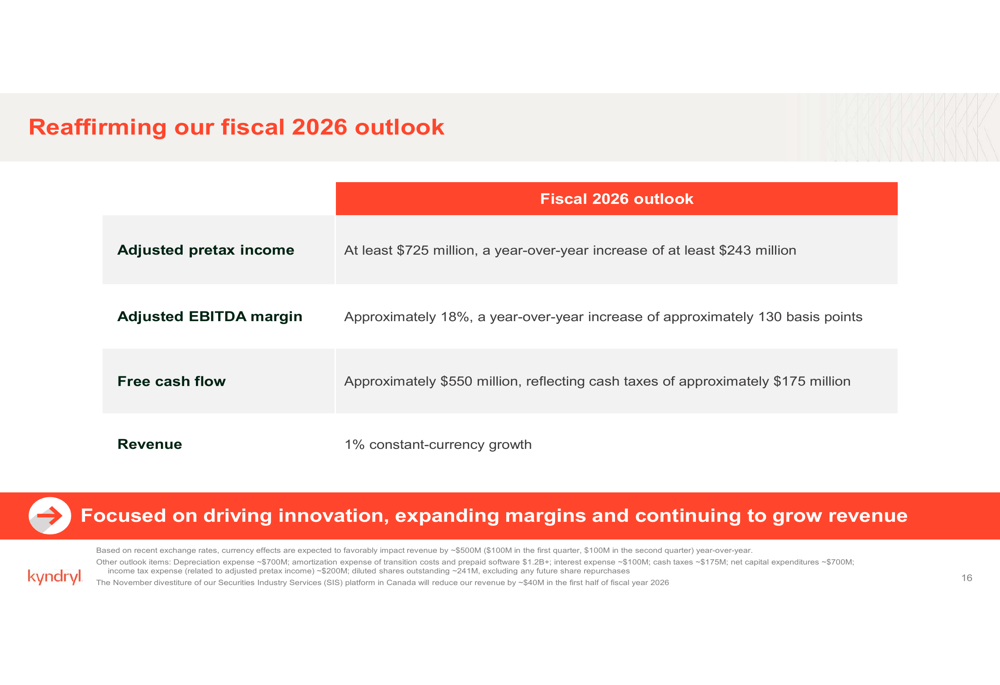

Kyndryl reaffirmed its fiscal 2026 outlook, projecting adjusted pretax income of at least $725 million (a year-over-year increase of at least $243 million), adjusted EBITDA margin of approximately 18% (up approximately 130 basis points), free cash flow of approximately $550 million, and 1% constant-currency revenue growth.

The detailed fiscal 2026 outlook is presented in the following chart:

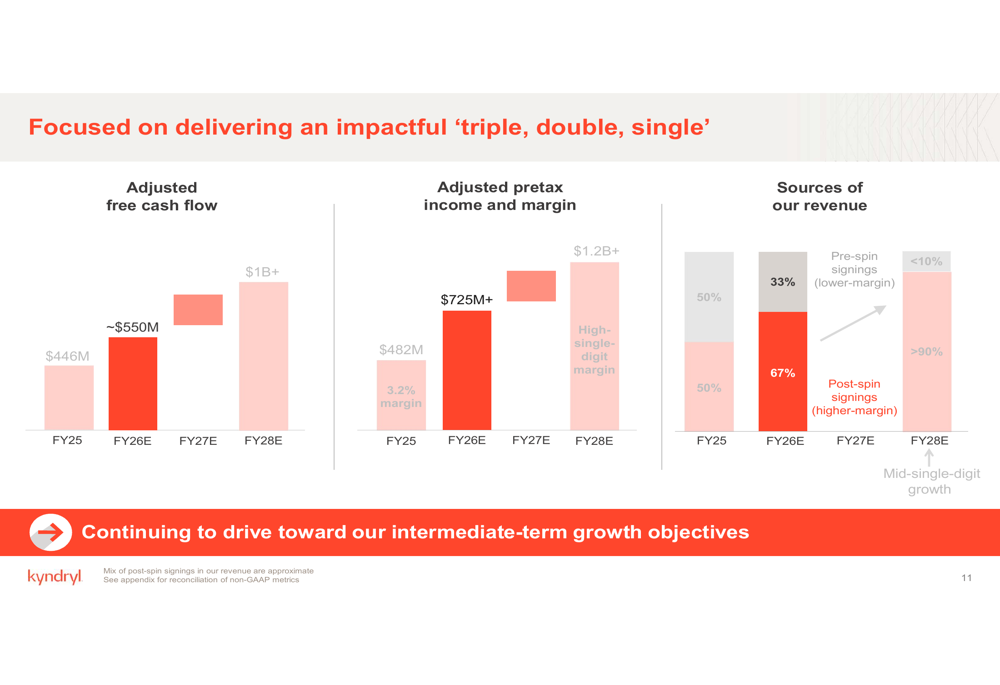

Looking further ahead, Kyndryl outlined ambitious medium-term targets through fiscal 2028, characterized by what the company calls a "triple, double, single" strategy:

1. Triple: Increasing adjusted free cash flow from $446 million in FY25 to over $1 billion by FY28

2. Double: Growing adjusted pretax income from $482 million in FY25 to over $1.2 billion by FY28

3. Single: Achieving high-single-digit adjusted pretax margin by FY28

This strategy is illustrated in the following chart showing the progression of these key metrics:

A key driver of this projected improvement is the ongoing shift in Kyndryl’s revenue mix. Post-spin signings, which carry higher margins, are expected to represent 67% of revenue in FY26 and grow to more than 90% by FY28, replacing lower-margin pre-spin business.

The following chart shows the consistent 26% gross margin and 9% pretax margin expected on post-spin signings:

Detailed Financial Analysis

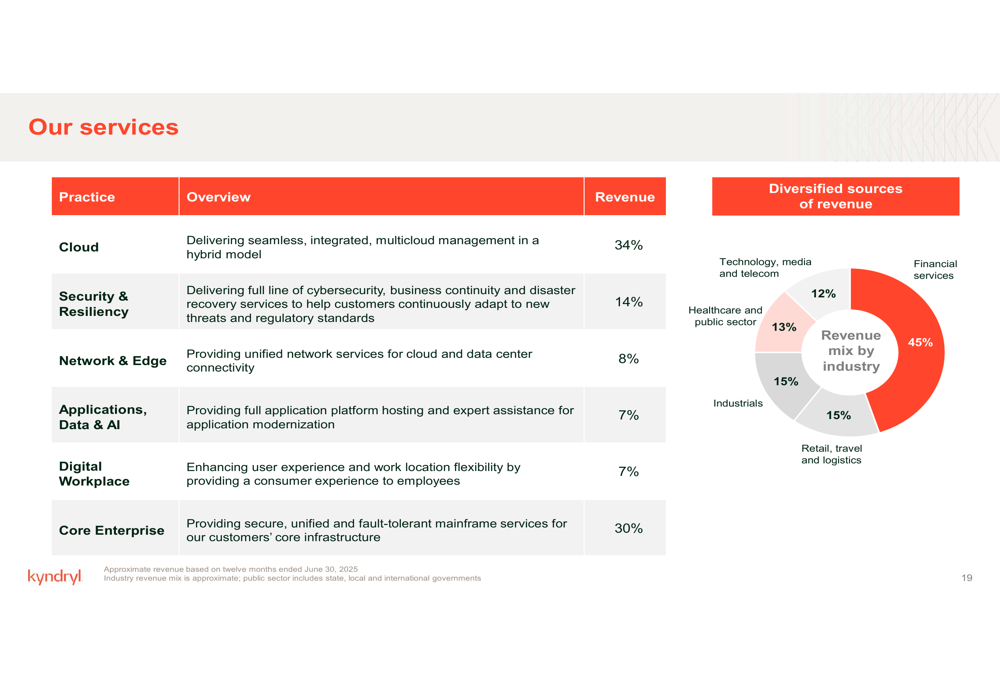

Kyndryl’s service portfolio spans multiple technology domains, with Cloud services representing 34% of revenue, followed by Core Enterprise at 30%, Security & Resiliency at 14%, Network & Edge at 8%, Applications, Data & AI at 7%, and Digital Workplace at 7%. The company serves diverse industries, with Financial services representing its largest sector at 45% of revenue.

The breakdown of Kyndryl’s services and industry exposure is shown in the following chart:

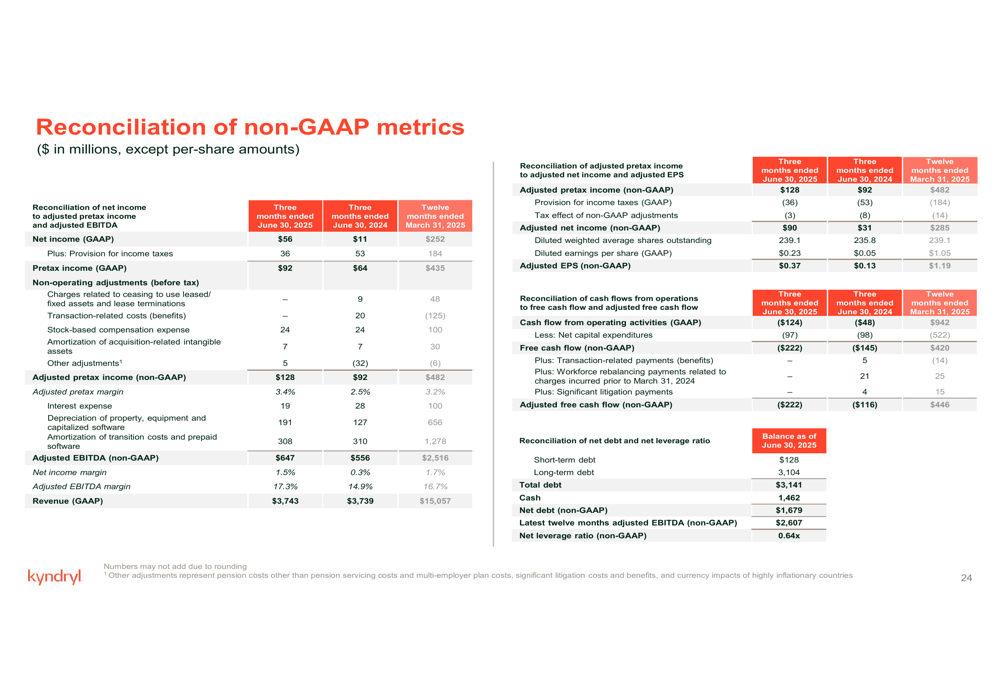

The reconciliation between GAAP and non-GAAP metrics provides additional insight into Kyndryl’s financial performance. For Q1 2026, the company reported GAAP net income of $56 million, which adjusts to $128 million in adjusted pretax income and $647 million in adjusted EBITDA after accounting for various non-cash items and special charges.

The detailed reconciliation is presented in the following chart:

Competitive Industry Position

Kyndryl highlighted several recent accolades and industry recognitions, including the 2025 Google (NASDAQ:GOOGL) Cloud Global Partner of the Year Award for Infrastructure Modernization and the 2025 Dell (NYSE:DELL) Global Alliances Partner of the Year for Marketing, Americas Innovation, and Asia Pacific and Japan Expansion.

The company was also recognized as a Leader in the March 2025 Gartner (NYSE:IT) Magic Quadrant for Outsourced Digital Workplace Services and ranked No.1 in Infrastructure Implementation and Managed Services Providers by Revenue in Gartner’s Market Share Analysis.

These recognitions underscore Kyndryl’s position as a leader in mission-critical enterprise technology services, though the market’s negative reaction to the earnings presentation suggests investors may be looking for more tangible evidence of revenue growth to complement the margin improvements the company has achieved.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.