Goldman Sachs chief credit strategist Lotfi Karoui departs after 18 years - Bloomberg

Introduction & Market Context

Lam Research Corporation (NASDAQ:LRCX) presented its June quarter (Q2) 2025 financial results on July 30, 2025, showcasing strong performance with revenue and profitability at the upper end of guided ranges. The semiconductor equipment manufacturer reported significant growth compared to the previous quarter, with its stock rising 0.65% in after-hours trading to $99.58, continuing its upward trajectory from its 52-week low of $56.32.

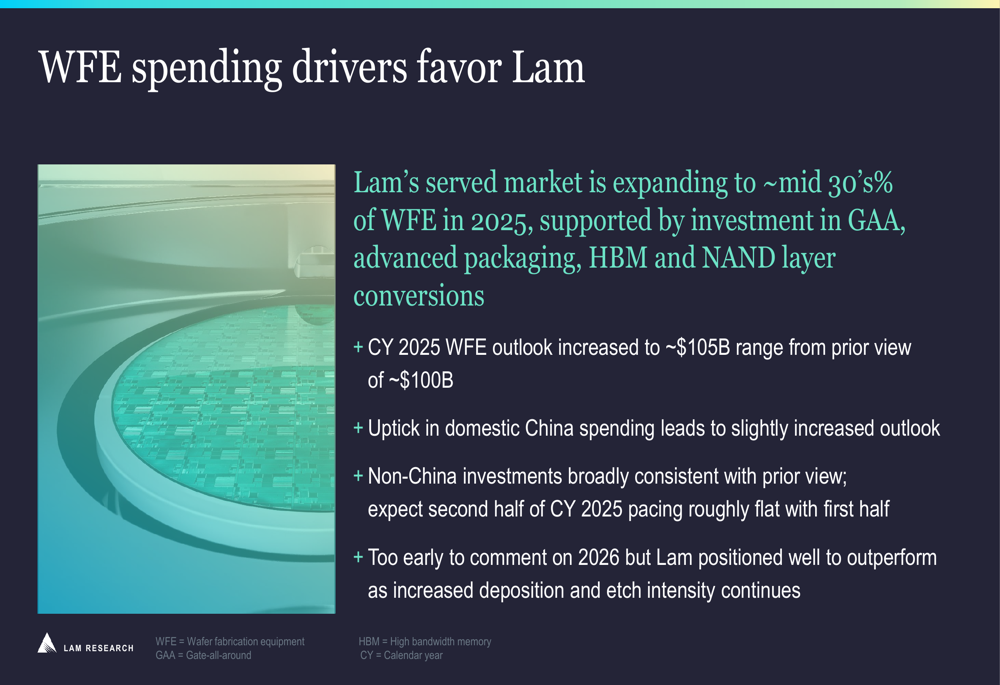

The company’s presentation highlighted an improved outlook for Wafer Fabrication Equipment (WFE) spending, increasing its 2025 forecast to approximately $105 billion from the previous estimate of $100 billion. This positive revision reflects growing industry demand, particularly from domestic Chinese customers, while non-China investments remained broadly consistent with previous projections.

As shown in the following slide detailing WFE spending drivers, Lam’s served market is expanding to approximately mid-30s percentage of WFE in 2025, supported by investments in Gate-All-Around (GAA) technology, advanced packaging, High Bandwidth (NASDAQ:BAND) Memory (HBM), and NAND layer conversions:

Quarterly Performance Highlights

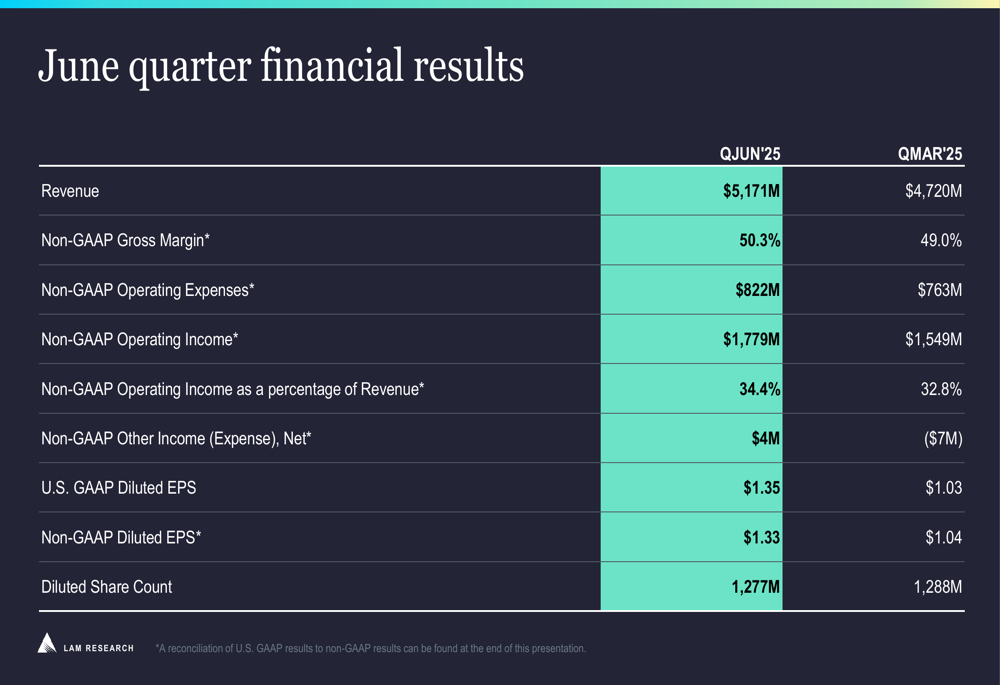

Lam Research reported Q2 2025 revenue of $5.17 billion, up from $4.72 billion in the March quarter, representing a 9.5% sequential increase. The company achieved a record non-GAAP earnings per share of $1.33, compared to $1.04 in the previous quarter. Notably, gross margin exceeded 50% for the first time in recent quarters, reaching 50.3%, up from 49.0% in Q1.

The following slide summarizes these key financial highlights for the June quarter:

For the full fiscal year 2025, Lam Research generated $18.44 billion in revenue, a substantial 23.7% increase from $14.91 billion in fiscal year 2024, demonstrating strong year-over-year growth momentum.

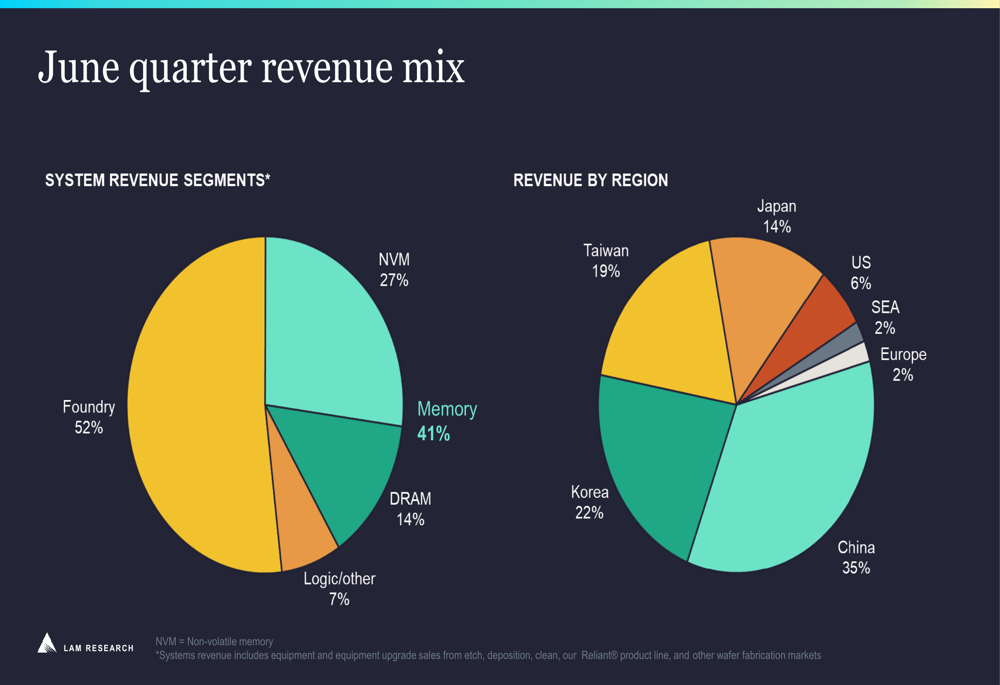

The company’s revenue mix for the June quarter shows a balanced portfolio across different semiconductor segments, with foundry representing 52% of system revenue, followed by memory at 41% (split between NVM at 27% and DRAM at 14%), and logic/other at 7%. Geographically, China accounted for 35% of revenue, followed by Korea (22%), Taiwan (19%), and Japan (14%), highlighting Lam’s global market presence:

Strategic Initiatives & Product Momentum

Lam Research emphasized its strong positioning in key technology inflections, with several product innovations gaining market traction. The company is ramping its ALTUS Halo ALD Mo (Atomic Layer Deposition Molybdenum) technology at multiple NAND customers in 2025, with adoption expected to increase as more customers convert capacity to 200+ layers. This technology is also gaining momentum in Foundry/Logic applications as performance requirements accelerate the transition to Gate-All-Around architecture.

The following slide details this strategic product and its market momentum:

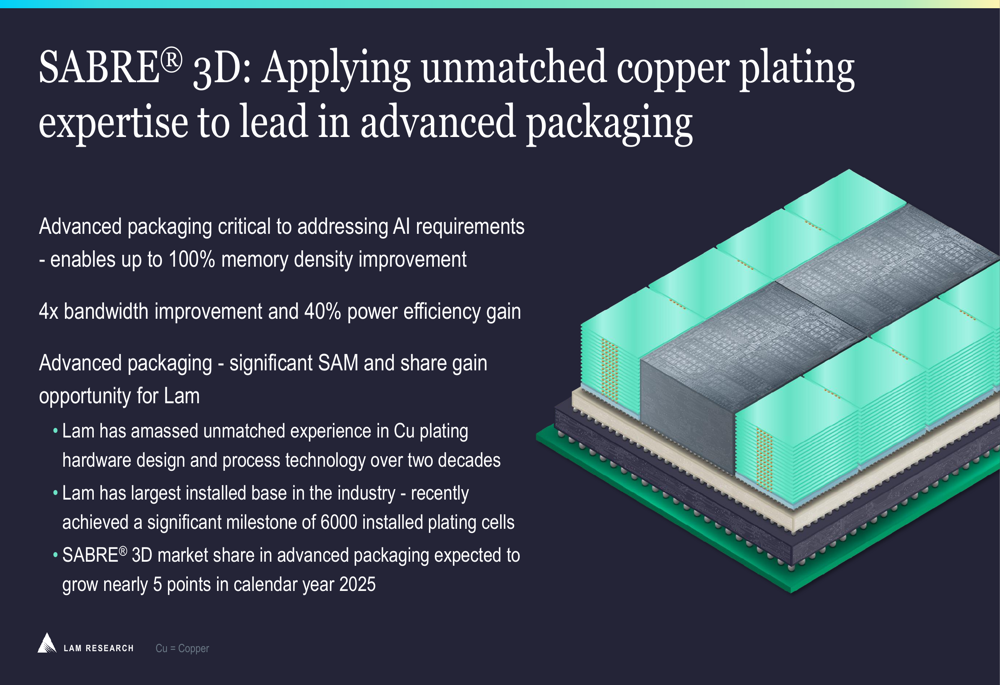

In advanced packaging, Lam is leveraging its copper plating expertise with the SABRE 3D system, which is critical for addressing AI requirements. The company highlighted that it has achieved a significant milestone of 6,000 installed plating cells, the largest installed base in the industry, and expects its market share in advanced packaging to grow by nearly 5 percentage points in calendar year 2025:

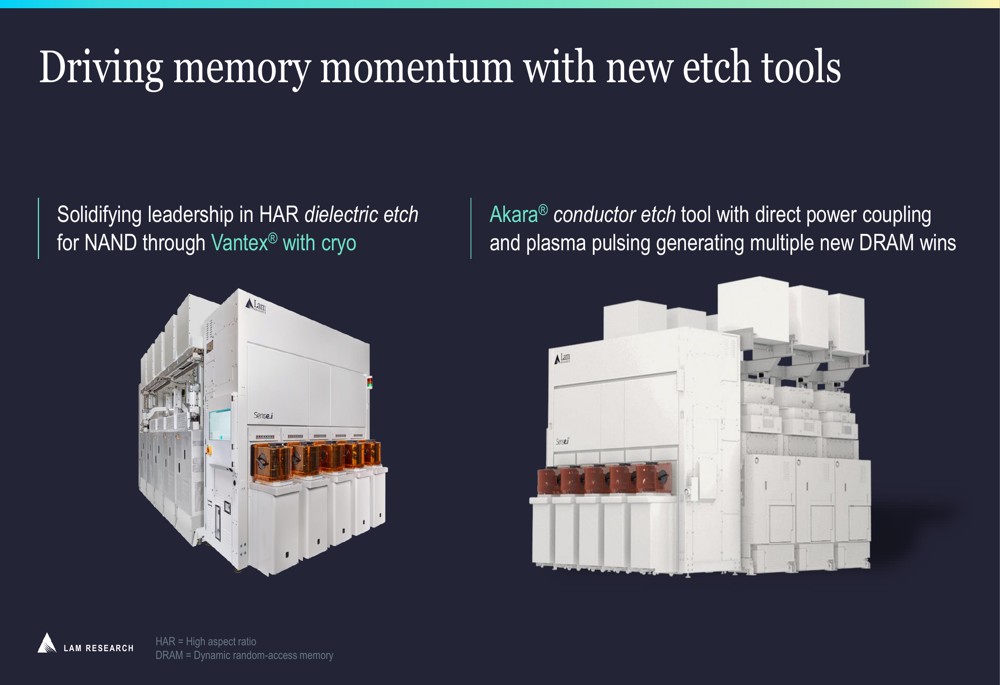

Additionally, Lam is strengthening its position in memory with new etch tools, including the Vantex with cryo technology for high aspect ratio dielectric etch in NAND and the Akara conductor etch tool, which has generated multiple new DRAM wins:

Forward-Looking Statements & Guidance

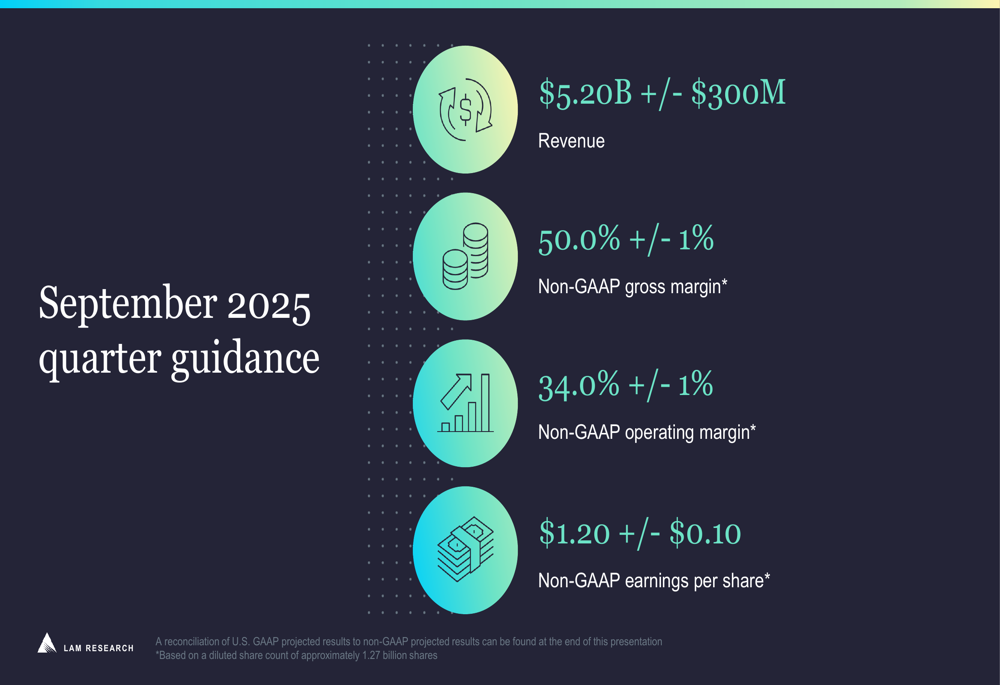

For the September 2025 quarter, Lam Research provided guidance of $5.20 billion in revenue (±$300 million), with a non-GAAP gross margin of 50.0% (±1%) and non-GAAP earnings per share of $1.20 (±$0.10). The company expects operating margins to remain strong at 34.0% (±1%).

The following slide presents the detailed guidance for the upcoming quarter:

Management expressed confidence in Lam’s ability to outperform as deposition and etch intensity continues to increase, noting that while it’s too early to comment specifically on 2026, the company is well-positioned for continued growth. The company highlighted three key strategic focus areas: strong product positioning in key technology inflections, growth in etch and deposition intensity with 3D scaling, and potential to expand its served available market and increase share at successive nodes.

Detailed Financial Analysis

Lam Research’s June quarter financial results showed improvement across multiple metrics compared to the March quarter. Non-GAAP operating income increased to $1.78 billion (34.4% of revenue) from $1.55 billion (32.8% of revenue) in the previous quarter. The company’s cash position strengthened significantly, with total consolidated gross cash balance rising to $6.41 billion from $5.46 billion.

The following comprehensive financial results table provides a detailed comparison between the June and March quarters:

The company significantly accelerated its share repurchase program, buying back $1.31 billion worth of shares in the June quarter compared to $347 million in the March quarter, while maintaining its dividend payments at $295 million. Inventory management improved, with inventory turns increasing to 2.4 from 2.2 in the previous quarter, and days sales outstanding decreased to 59 days from 62 days.

Lam’s Customer Support Business Group (CSBG) generated $1.73 billion in revenue for the June quarter, up from $1.68 billion in the March quarter, demonstrating continued growth in the company’s services and aftermarket business.

The company’s strong financial performance in the June quarter builds upon the momentum seen in the previous quarter, where it had exceeded analyst expectations. With gross margins now exceeding 50% and continued revenue growth, Lam Research appears well-positioned to capitalize on the expanding semiconductor equipment market, particularly as demand for advanced technologies continues to drive industry investment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.