United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

LandBridge Co LLC (NYSE:LB) released its second quarter 2025 earnings presentation on August 7, 2025, showcasing strong financial performance and strategic initiatives. The company’s stock closed at $59.35 on August 6, with premarket trading indicating a slight increase of 0.44% to $59.61. LandBridge continues to leverage its extensive surface acreage in the Permian Basin to generate diversified revenue streams, with a notable shift toward non-oil and gas royalties.

The company, which owns approximately 277,000 surface acres in the heart of the Permian Basin, has positioned itself as a critical player in energy and broader industrial development. This quarter’s results demonstrate LandBridge’s continued execution of its strategy to maximize commercial activity on its surface by actively seeking collaboration opportunities with operating companies and developers.

Quarterly Performance Highlights

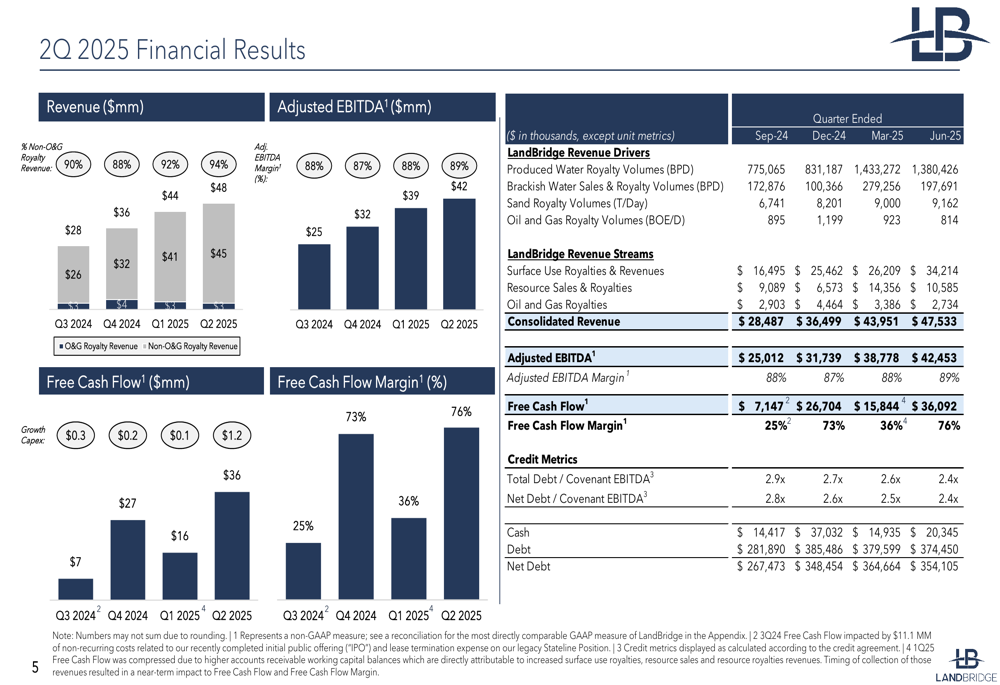

LandBridge reported substantial year-over-year growth in Q2 2025, with revenue increasing 83% to $47.5 million and Adjusted EBITDA rising 81% to $42.5 million. The company achieved a record $34.2 million in Surface Use Royalties and Revenues, driven by recent acquisitions and strong organic growth. Non-oil and gas royalty revenue represented approximately 94% of total revenue in the quarter, highlighting the company’s successful diversification strategy.

As shown in the following comprehensive financial results chart, LandBridge has maintained strong sequential growth across key metrics:

The company’s high-margin business model continues to deliver impressive results, with an Adjusted EBITDA margin of 89% and a Free Cash Flow margin of 76% in Q2 2025. Free Cash Flow reached $36.1 million, more than doubling from the previous quarter’s $15.8 million. This improvement reflects the company’s limited operating expenses and minimal capital expenditure requirements.

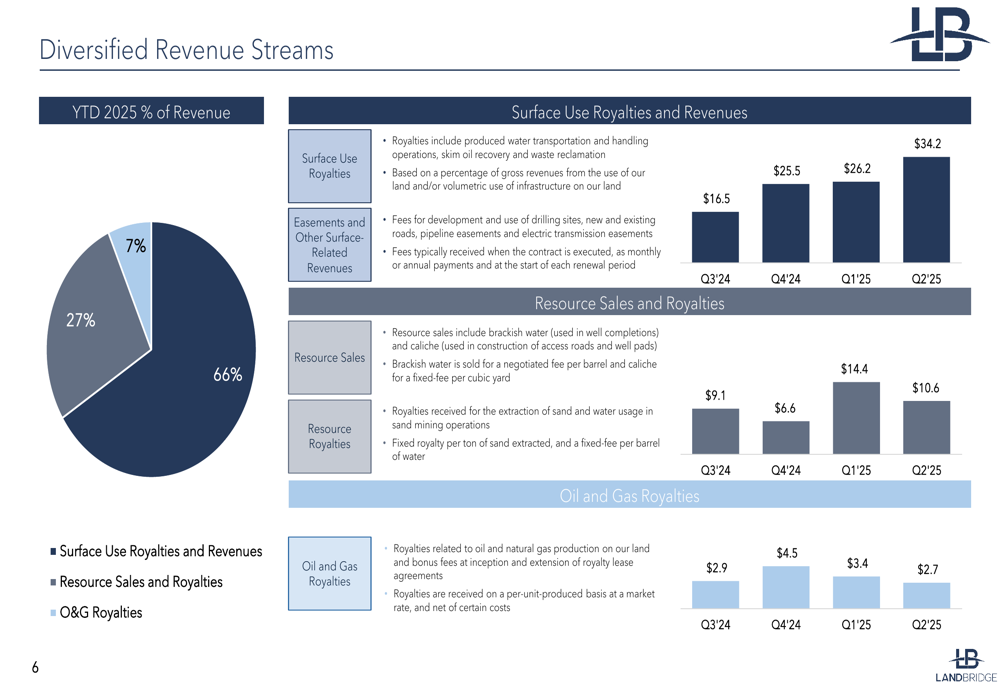

LandBridge’s revenue streams remain well-diversified, as illustrated in the following breakdown:

Surface Use Royalties and Revenues accounted for 66% of year-to-date 2025 revenue, followed by Resource Sales and Royalties at 27% and Oil and Gas Royalties at 7%. This diversification provides stability while allowing the company to benefit from increased activity across multiple sectors.

Strategic Initiatives

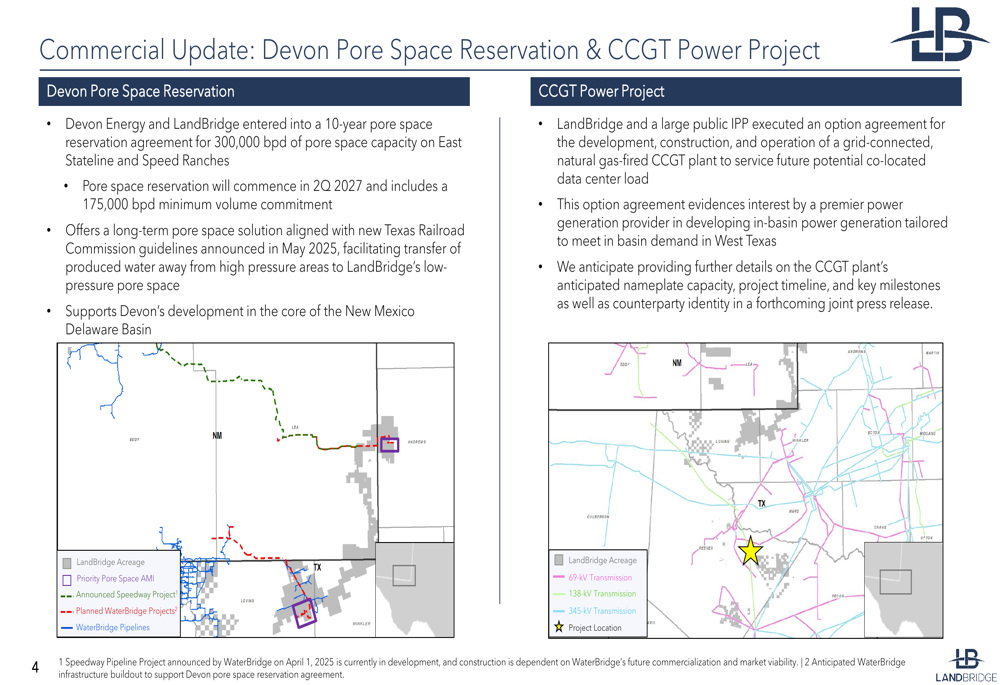

A key highlight from the quarter was LandBridge’s 10-year surface use and pore space reservation agreement with Devon Energy (NYSE:DVN). This agreement secures 300,000 barrels per day of pore space capacity with an obligation to deliver a minimum of 175,000 barrels per day on East Stateline and Speed Ranches. The pore space reservation will commence in Q2 2027 and aligns with new Texas Railroad Commission guidelines announced in May 2025.

The following slide details this strategic agreement and its significance:

Additionally, LandBridge executed a lease option agreement with a large public independent power producer (IPP) for the development, construction, and operation of a natural gas-fired advanced combined cycle gas turbine (CCGT) plant. This agreement further demonstrates the company’s ability to attract commercial development beyond traditional oil and gas activities.

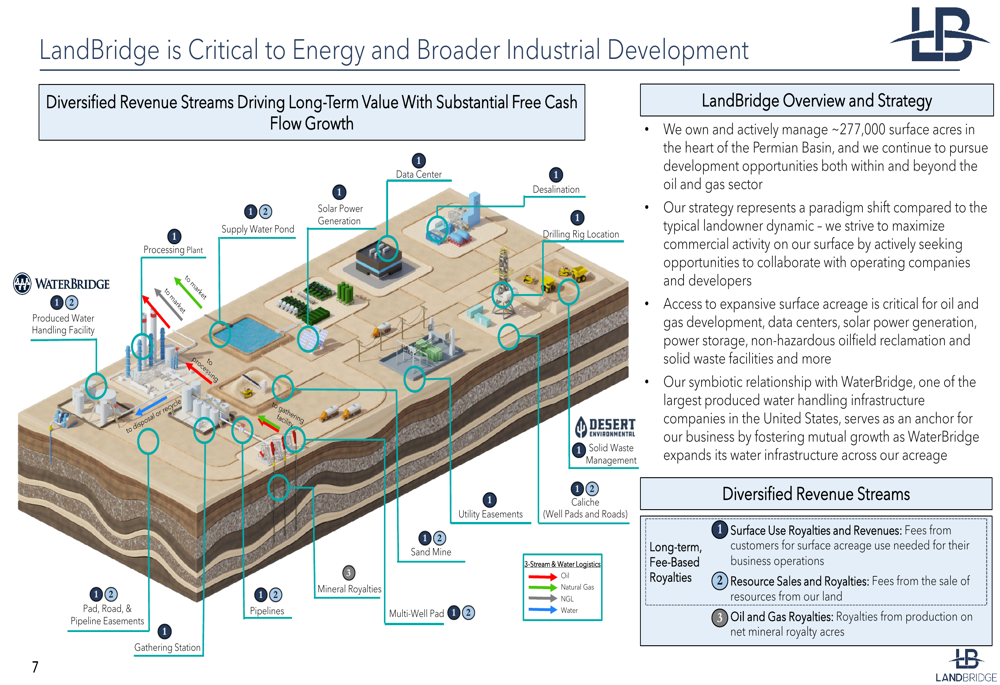

LandBridge’s business model leverages its extensive surface acreage for multiple revenue-generating activities, as illustrated in this cross-sectional view:

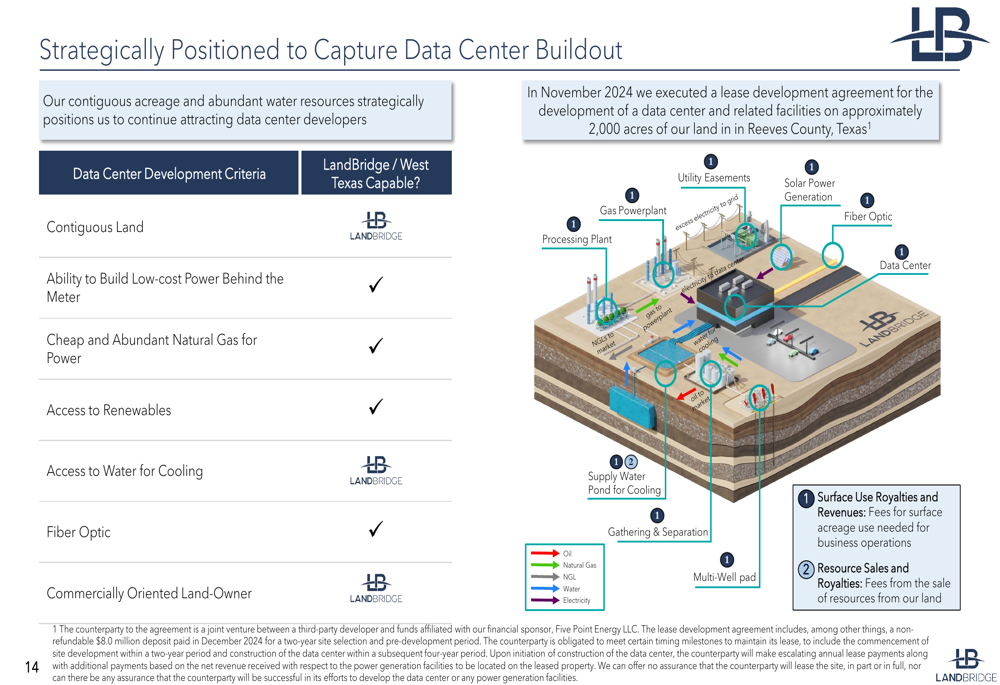

The company has also positioned itself to capitalize on the growing demand for data center infrastructure. In November 2024, LandBridge executed a lease development agreement for a data center and related facilities on approximately 2,000 acres. The company’s land meets all critical data center development criteria, including contiguous land availability, access to low-cost power, abundant natural gas, renewables, water for cooling, and fiber optic connectivity.

As shown in the following slide, LandBridge is strategically positioned to capture opportunities in the data center sector:

Detailed Financial Analysis

LandBridge’s financial performance demonstrates strong momentum across key metrics. The company’s produced water royalty volumes reached 1,380,426 barrels per day in Q2 2025, slightly down from 1,433,272 in Q1 2025 but significantly higher than 775,065 in Q3 2024. Sand royalty volumes continued to increase, reaching 9,162 tons per day in Q2 2025 compared to 6,741 in Q3 2024.

The company’s balance sheet remains solid, with cash of $20.3 million and debt of $374.5 million as of Q2 2025, resulting in net debt of $354.1 million. The net leverage ratio improved to 2.4x from 2.9x in Q3 2024, within the company’s target range of 2.0-2.5x.

LandBridge announced a quarterly cash dividend of $0.10 per share, payable on September 18th to shareholders of record as of September 4th, maintaining the same dividend level as the previous quarter.

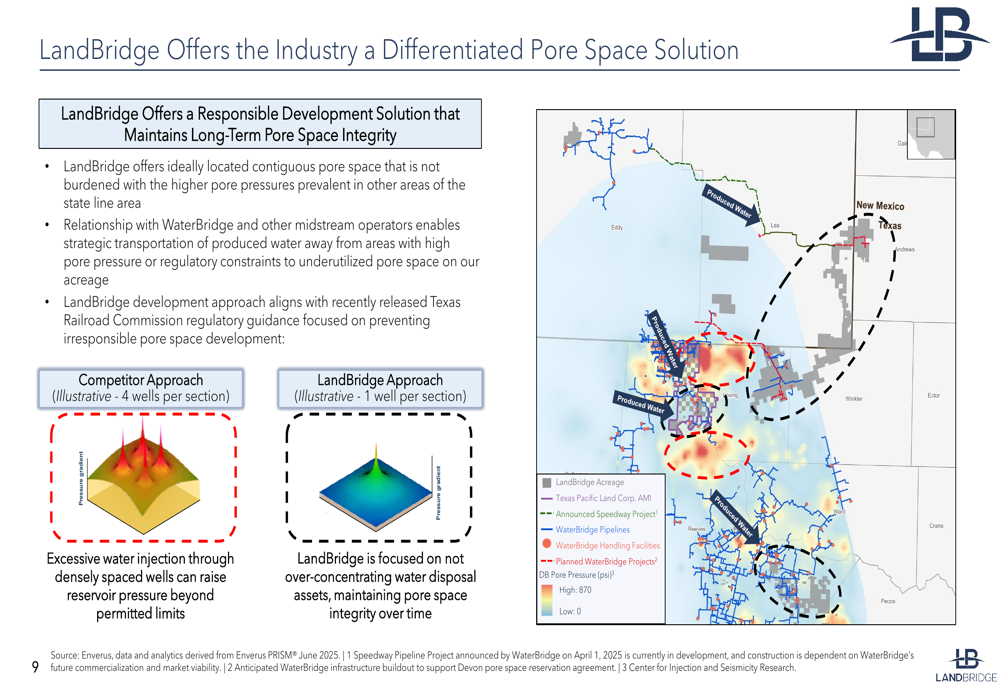

The company’s differentiated approach to pore space utilization provides a competitive advantage, as illustrated in the following comparison:

LandBridge’s approach focuses on maintaining pore space integrity over time by using fewer injection wells per section compared to competitors, aligning with recent Texas Railroad Commission regulatory guidance.

Forward-Looking Statements

LandBridge’s capital allocation strategy focuses on three key areas: maintaining an appropriate capital structure, returning capital to shareholders, and opportunistically pursuing value-enhancing acquisitions. The company aims to maintain its net leverage ratio between 2.0-2.5x while supporting financial flexibility for future growth initiatives.

The company’s relationship with WaterBridge, a leading water management solutions provider, continues to be a significant driver of growth. WaterBridge operates water infrastructure on LandBridge’s surface, providing fees and royalty streams to LandBridge while being responsible for all costs related to construction, maintenance, and operations.

Looking ahead, LandBridge is well-positioned to benefit from continued development in the Delaware Basin, where oil production has grown by 36% from 2021 to 2024, outpacing the broader Permian Basin’s 11% growth during the same period. The company’s strategic footprint in highly productive regions with favorable breakeven economics supports its long-term growth prospects.

With its diversified revenue streams, high-margin business model, and strategic positioning in the Permian Basin, LandBridge appears well-equipped to continue delivering strong financial results while expanding into new growth opportunities beyond traditional oil and gas activities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.