Street Calls of the Week

Lifecore Biomedical Inc. (NASDAQ:LFCR) recently presented its corporate strategy and financial performance, highlighting its transformation into a specialized contract development and manufacturing organization (CDMO) focused on sterile injectables. While the company reported a slight revenue decline for Q3 2025, management emphasized an ambitious growth strategy targeting significant revenue expansion and margin improvement in the coming years.

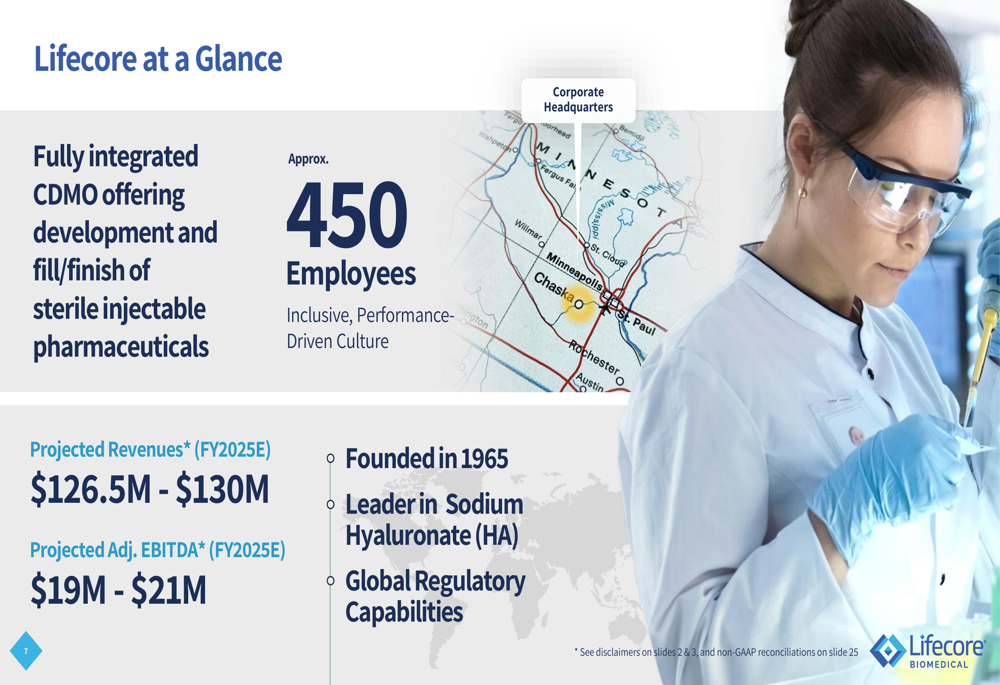

Introduction & Market Context

Lifecore has completed its transformation from a low-margin agricultural business to a standalone CDMO specializing in sterile injectable pharmaceuticals. The company operates in several high-growth markets, including the global CDMO market ($120B, +8% CAGR), hyaluronic acid market ($9.8B, +7% CAGR), and the injectable CDMO market ($10B, +10% CAGR).

As shown in the following market overview, the company is positioning itself to capitalize on strong industry tailwinds:

The injectable pharmaceutical segment represents a significant opportunity, with more than 50% of annual US drug approvals being injectables. Additionally, the company noted increasing momentum for Western manufacturing, a trend that could benefit domestic CDMOs like Lifecore.

Quarterly Performance Highlights

For Q3 fiscal 2025, Lifecore reported revenue of $35.2 million, representing a 2% decrease from the same period in fiscal 2024. The company posted a net loss of $14.8 million and adjusted EBITDA of $5.7 million, down $0.7 million year-over-year. Following the earnings announcement, Lifecore’s stock fell by 5.56% during regular trading hours and an additional 2.35% in aftermarket trading.

Despite these short-term challenges, management maintained its full-year fiscal 2025 guidance:

The company highlighted several positive developments during the quarter, including signing multiple new project agreements with both new and existing customers. Lifecore also strengthened its balance sheet by selling a 10-head filler, raising approximately $17.0 million.

Strategic Initiatives

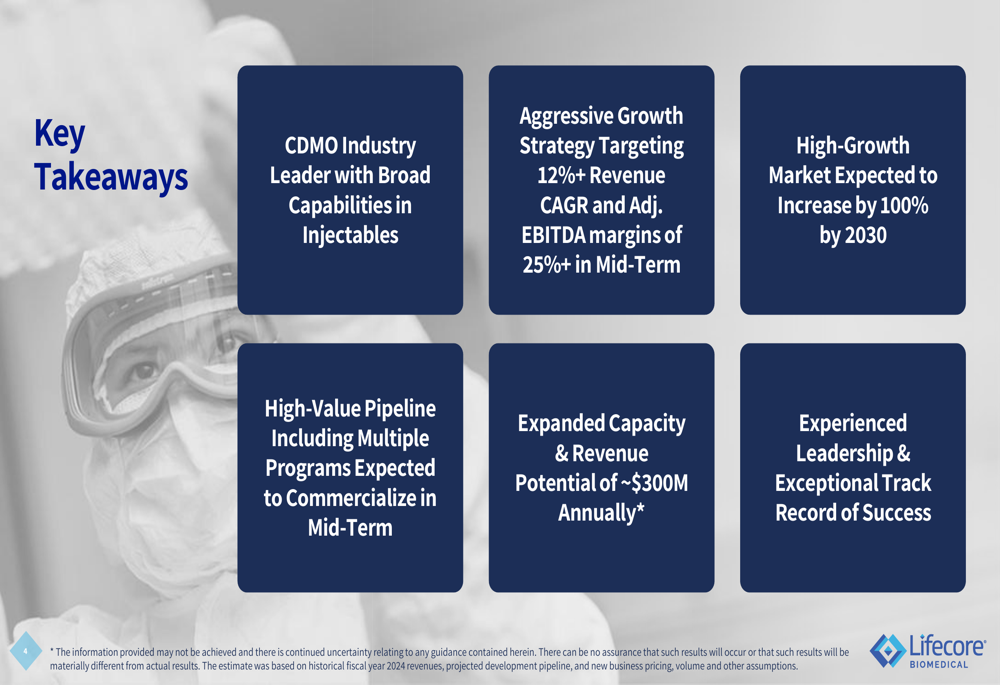

Lifecore’s corporate presentation outlined a three-pronged growth strategy focused on maximizing existing customer business, advancing programs toward commercialization, and driving new business development.

The company’s key strategic initiatives are summarized in the following slide:

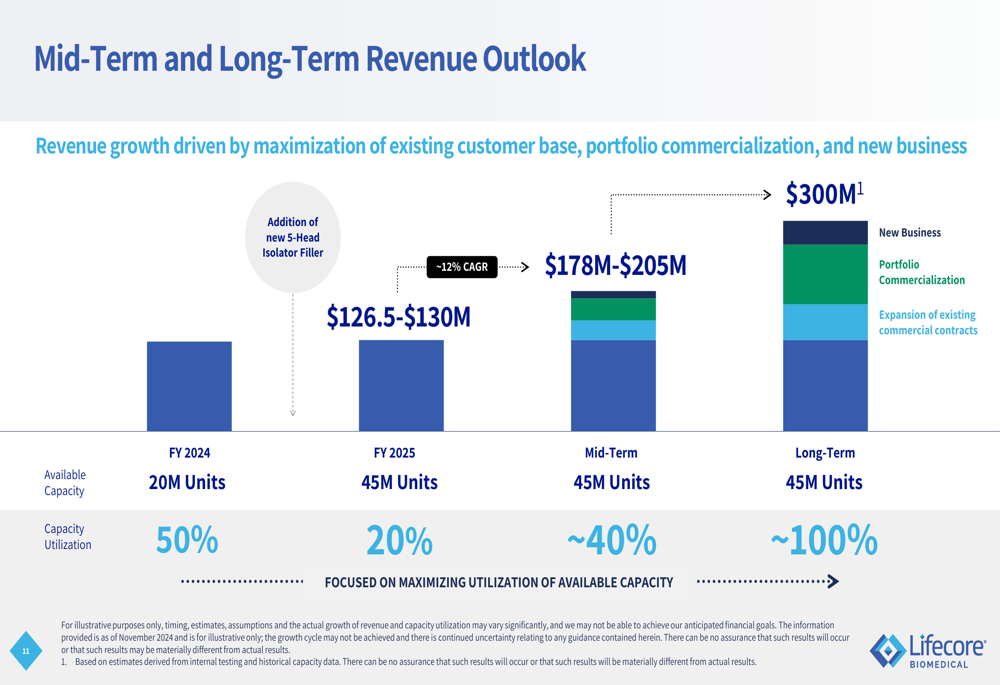

A central element of Lifecore’s growth strategy involves expanding capacity to meet future demand. The company recently installed a state-of-the-art 5-head isolator filler, which has approximately doubled its annual production capacity. This investment positions Lifecore to pursue new business opportunities while supporting the growth of existing customer relationships.

The revenue growth trajectory is illustrated in this forward-looking projection:

Management expects to grow from current revenue levels of approximately $126.5-$130 million to $178-205 million in the mid-term and potentially over $300 million in the long term. This growth is anticipated to come from expansion of commercial contracts, portfolio commercialization, and new business development.

Detailed Financial Analysis

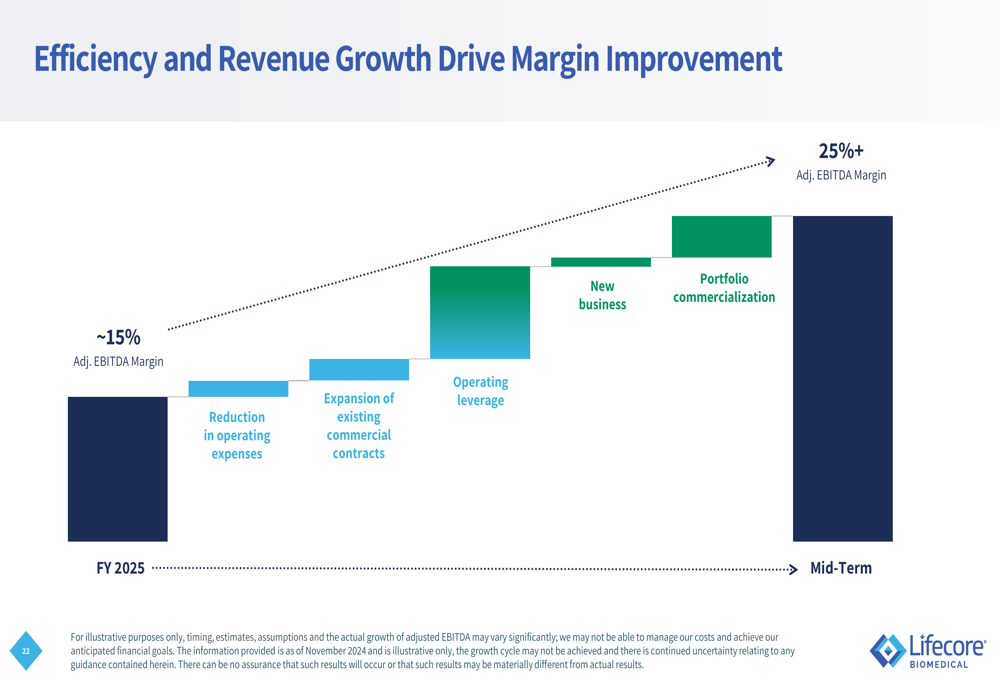

Lifecore’s financial performance reflects a company in transition. While Q3 revenue declined 2% year-over-year, the company reported a 2% increase in nine-month revenues to $92.4 million. Current adjusted EBITDA margins are around 15%, but management is targeting improvement to over 25% in the mid-term through operational efficiencies and revenue growth.

The path to margin improvement is outlined in the following slide:

During the earnings call, CFO Ryan Lake expressed optimism about cash flow improvements, stating, "We expect to see a pretty dramatic improvement in free cash flow." The company aims to achieve cash flow-positive operations in the second half of the year.

Competitive Industry Position

Lifecore positions itself as a specialized CDMO with particular expertise in high-viscosity and complex formulations. The company has a 40+ year track record with global regulatory bodies and has manufactured more than 150 million doses of its premium sodium hyaluronate worldwide.

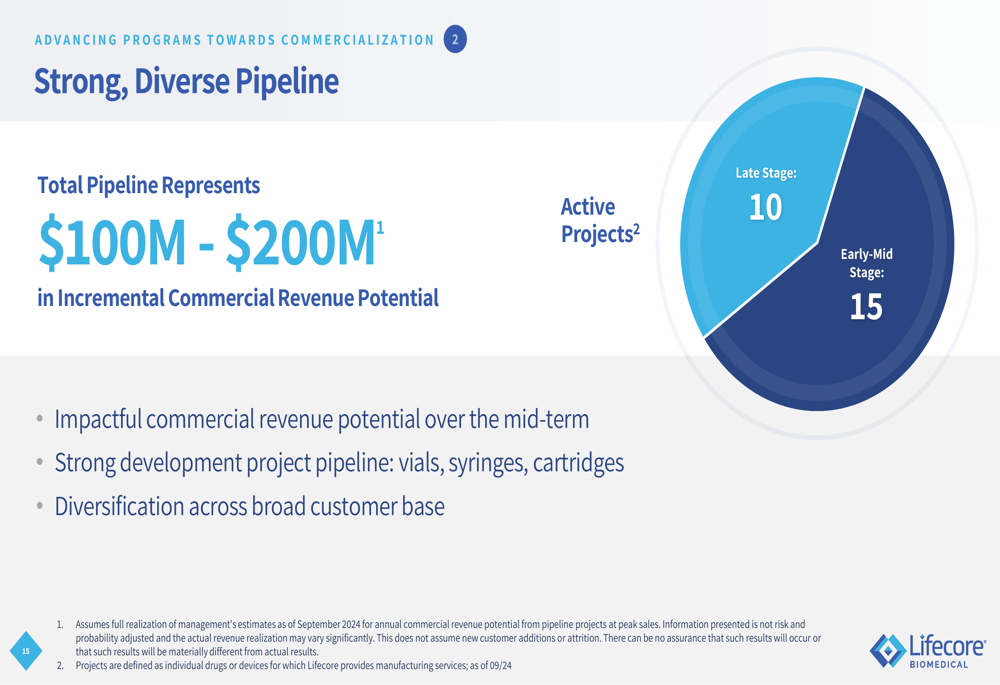

The company’s pipeline represents significant growth potential:

With 10 late-stage and 15 early-to-mid-stage development projects, Lifecore estimates its pipeline represents $100-200 million in incremental commercial revenue potential. These projects span various delivery formats including vials, syringes, and cartridges, and involve both specialty and large pharmaceutical companies.

Forward-Looking Statements

CEO Paul Josephs emphasized the company’s strategic focus during the earnings call, stating, "We are executing aggressively against the plan we articulated last November." He also highlighted growing interest in domestic drug manufacturing, noting, "We’ve never heard as much discussion around Western manufacturing."

Despite management’s optimism, investors should consider several risk factors:

- The current revenue decline and net losses

- Execution risks in achieving projected growth

- Competitive pressures in the CDMO space

- Regulatory hurdles that could impact pipeline progression

- Macroeconomic pressures affecting customer spending

Lifecore’s current stock price of $6.67 is closer to its 52-week low of $3.68 than its high of $7.99, suggesting investor caution regarding the company’s near-term prospects despite its ambitious growth strategy.

The company’s snapshot provides additional context for evaluating its current position and future potential:

As Lifecore continues its transformation journey, investors will be watching closely to see if management can execute on its growth strategy while improving financial performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.