Five things to watch in markets in the week ahead

Introduction & Market Context

Limbach Holdings Inc (NASDAQ:LMB) delivered strong second-quarter results for 2025, with revenue increasing 16.4% year-over-year to $142.2 million, according to the company’s latest investor presentation. The building systems solutions firm, which specializes in revitalizing and maintaining mission-critical systems in existing facilities, continues to benefit from its strategic shift toward higher-margin Owner Direct Relationships (ODR).

The company’s stock has performed exceptionally well over the past year, delivering a 122.36% return according to recent data. Following the Q2 earnings announcement, Limbach’s stock traded at $134.84, near its 52-week high of $154.05, reflecting strong investor confidence in the company’s strategic direction.

As shown in the following overview of Limbach’s business model and market positioning:

Quarterly Performance Highlights

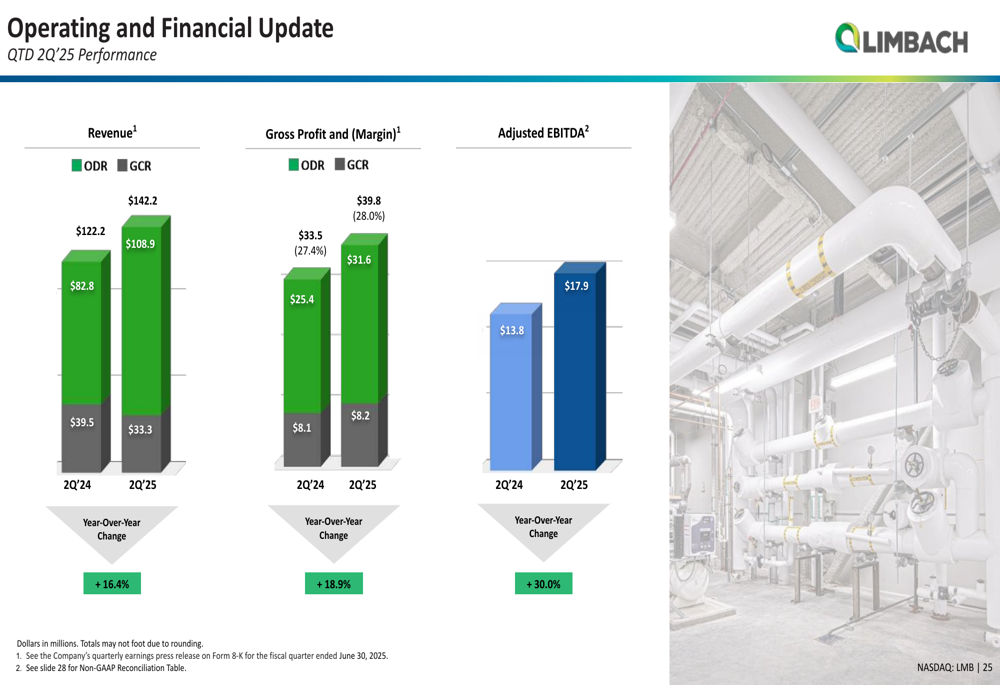

Limbach reported impressive financial results for Q2 2025, with revenue reaching $142.2 million, representing a 16.4% increase compared to the same period last year. The company’s ODR segment, which focuses on direct relationships with building owners, contributed $108.9 million (76.6% of total revenue), while the General Contractor Relationships (GCR) segment accounted for $33.3 million (23.4%).

Gross profit for the quarter was $39.8 million, representing a margin of 28.0% and an 18.9% year-over-year increase. Adjusted EBITDA grew by 30.0% to $17.9 million, demonstrating the company’s improving operational efficiency and the success of its strategic initiatives.

The quarterly performance data is illustrated in the following chart:

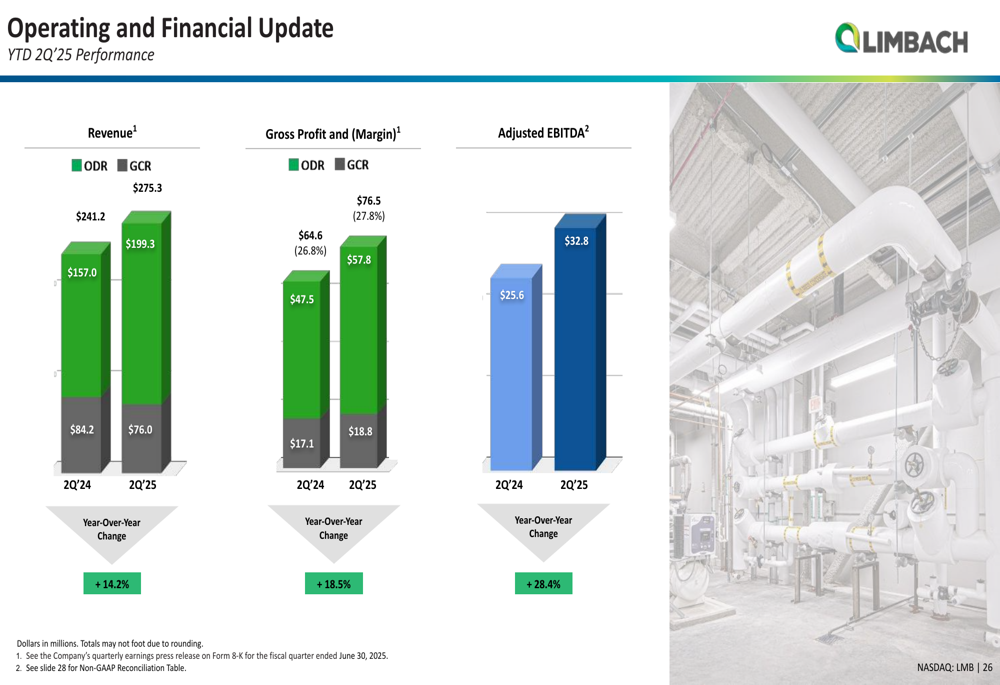

Year-to-date results through Q2 2025 show similar strength, with revenue of $275.3 million (up 14.2% year-over-year), gross profit of $76.5 million (27.8% margin), and adjusted EBITDA of $32.8 million (up 28.4%). The consistent performance across both quarters indicates sustainable momentum in Limbach’s business model.

Strategic Initiatives

Limbach’s presentation highlighted its three-pillar approach to scaling the business: shifting revenue mix toward higher-margin ODR business, expanding margins through evolved offerings, and growing through strategic acquisitions.

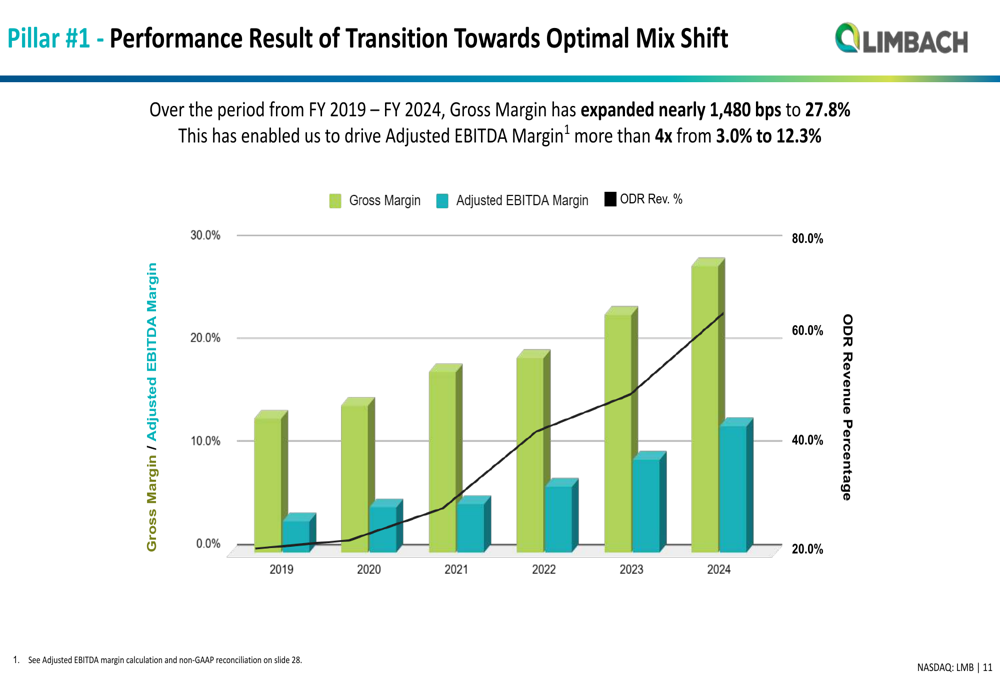

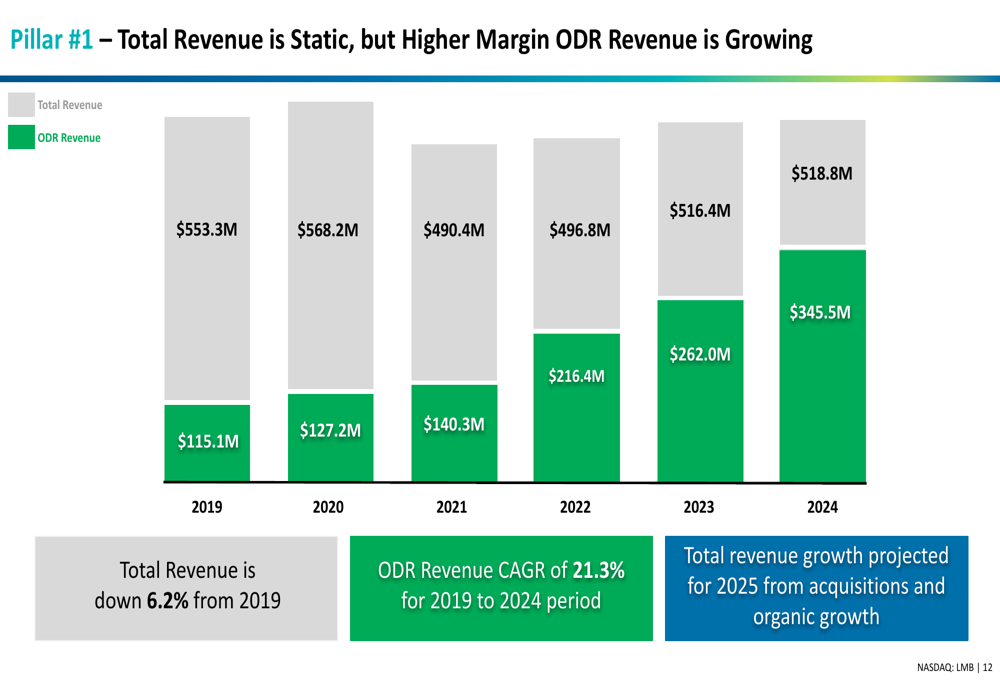

The company has made significant progress in its first pillar, transforming from a traditional contractor to a building systems solutions provider. From 2019 to 2024, Limbach expanded its gross margin by nearly 1,480 basis points to 27.8% while increasing its adjusted EBITDA margin more than fourfold from 3.0% to 12.3%. This improvement directly correlates with the increasing proportion of ODR revenue, as shown in the following chart:

While total revenue has remained relatively stable from 2019 to 2024 (actually decreasing 6.2% from $553.3M to $518.8M), the composition has shifted dramatically. ODR revenue grew at a CAGR of 21.3% during this period, increasing from $115.1M in 2019 to $345.5M in 2024. This strategic pivot has been the primary driver of Limbach’s margin expansion.

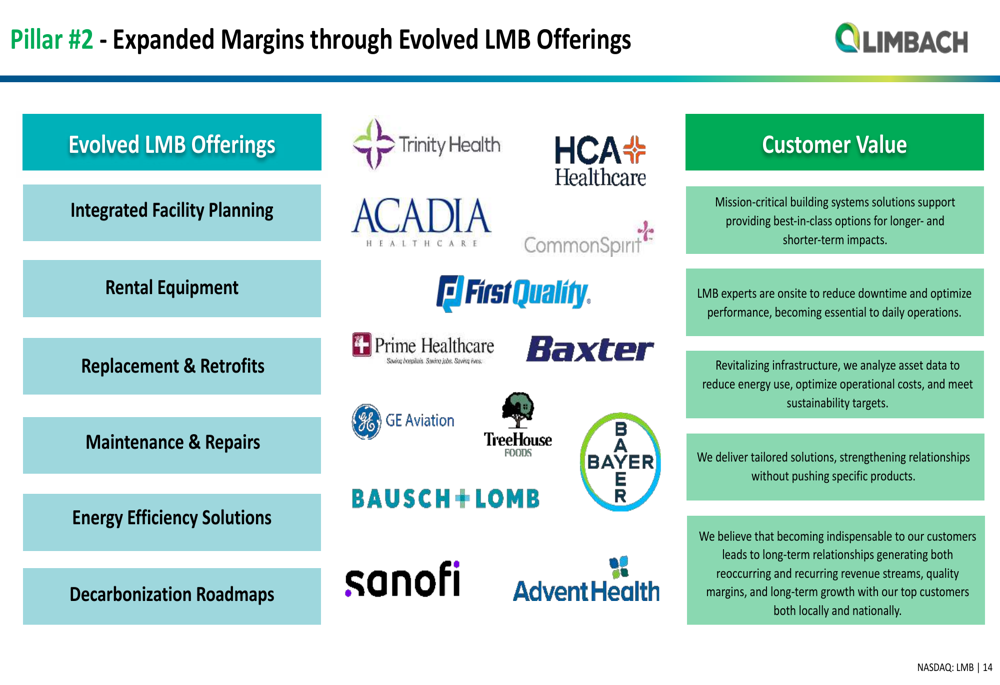

The second pillar of Limbach’s strategy involves expanding margins through evolved offerings. The company has developed specialized services including integrated facility planning, rental equipment, replacement and retrofits, maintenance and repairs, energy efficiency solutions, and decarbonization roadmaps. These services cater to national clients such as Trinity Health, HCA Healthcare (NYSE:HCA), GE Aviation, and Sanofi (NASDAQ:SNY).

Acquisition Strategy

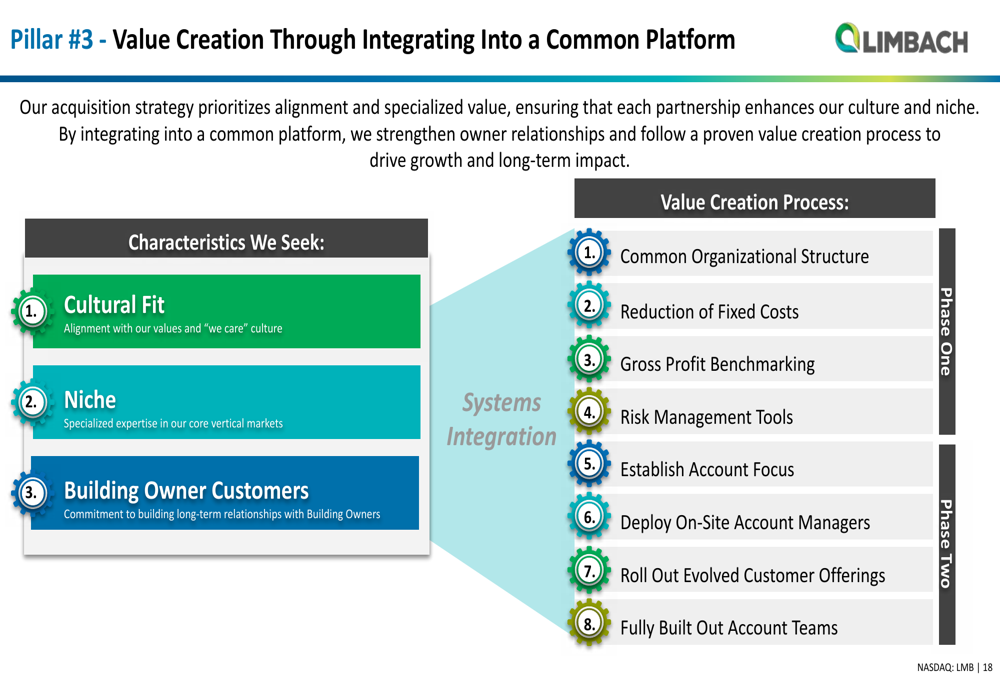

The third pillar of Limbach’s growth strategy focuses on strategic acquisitions to expand its geographic footprint and service capabilities. The company has established clear criteria for both "tuck-in" acquisitions in existing markets and expansion into new geographies.

Limbach’s approach to integrating acquisitions follows a structured process designed to create value through common platforms and organizational structures. The integration process includes implementing common organizational structures, reducing fixed costs, benchmarking gross profit, deploying risk management tools, establishing account focus, and rolling out evolved customer offerings.

The company recently completed two significant acquisitions. Pioneer Power Inc. was acquired for $66.1 million, closing on July 1, 2025. This expansion transaction is expected to contribute approximately $120 million in annualized revenue and $10 million in adjusted EBITDA beginning in 2026. The acquisition expands Limbach’s footprint in the Midwest region.

Earlier, on December 2, 2024, Limbach acquired Consolidated Mechanical, which expanded the company’s reach into Kentucky, Illinois, and Michigan. This acquisition is expected to contribute approximately $23 million in annualized revenue and $4 million in EBITDA beginning in 2025, while enhancing Limbach’s offerings in power generation, food processing, manufacturing, and metals markets.

Financial Outlook

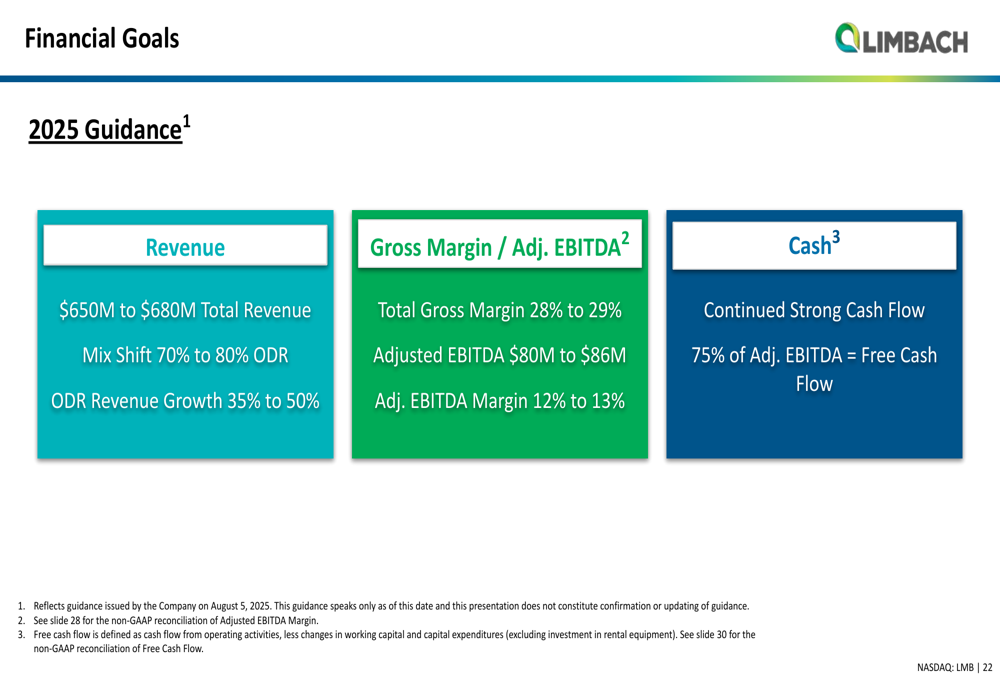

Limbach provided updated guidance for fiscal year 2025, projecting total revenue between $650 million and $680 million, with ODR revenue expected to represent 70% to 80% of the total. This represents a significant increase from the $610-$630 million guidance provided in the Q1 earnings report, reflecting the company’s growing confidence in its business trajectory.

The company expects total gross margin to range from 28% to 29%, with adjusted EBITDA between $80 million and $86 million (12% to 13% margin). Limbach also anticipates strong cash flow generation, with free cash flow conversion targeted at 75% of adjusted EBITDA.

The 2025 financial guidance is summarized in the following slide:

Limbach maintains a strong balance sheet to support its growth initiatives. As of June 30, 2025, the company reported cash and cash equivalents of $38.9 million, working capital of $85.5 million, and total debt of $33.2 million. This financial position provides Limbach with the flexibility to fund organic growth and pursue additional acquisitions while investing in expanded offerings.

Competitive Industry Position

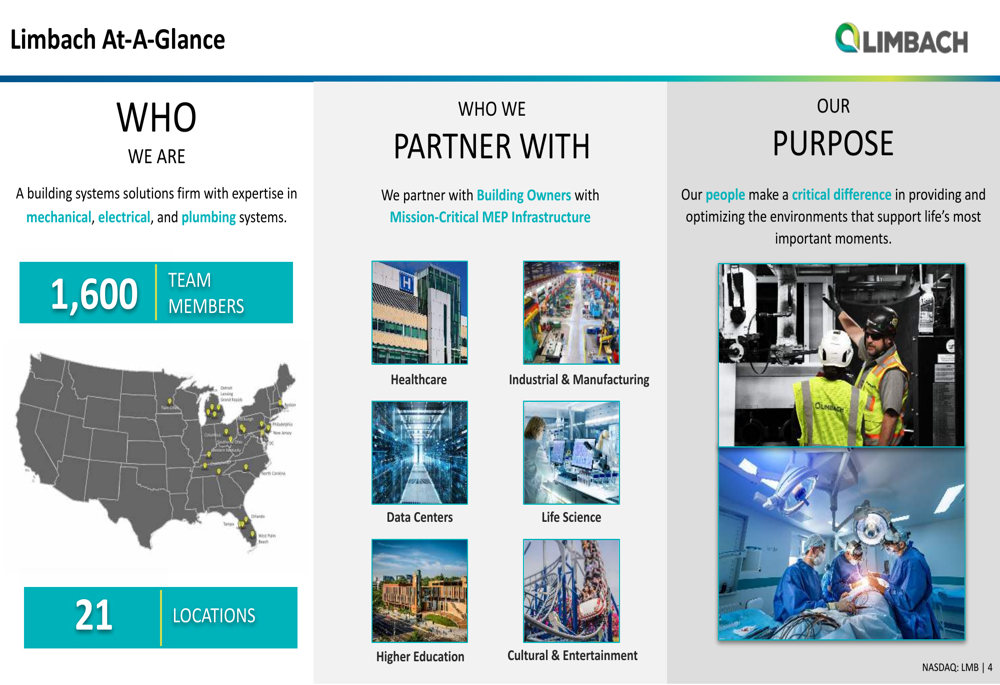

Limbach has positioned itself as a specialized building systems solutions firm focused on existing infrastructure, differentiating from OEM firms, contractors, property managers, and consulting and engineering firms. This positioning allows the company to target mission-critical vertical markets including healthcare, industrial and manufacturing, data centers, life sciences, higher education, and cultural and entertainment facilities.

The company’s focus on existing infrastructure provides several competitive advantages: macroeconomic resilience (equipment breaks regardless of economic conditions), fast-paced execution, budget agility (spanning both operating and capital expenditure budgets), and deep integration with customer facility operations.

As shown in the following slide, Limbach serves diverse vertical markets that provide durable demand through economic cycles:

Forward-Looking Statements

Looking ahead, Limbach aims to continue its strategic transformation by further increasing the proportion of ODR revenue to approximately 80% of total revenue. The company plans to expand its margins through evolved offerings, targeting a long-term gross margin of 35-40%.

Limbach’s acquisition strategy will remain a key component of its growth plan, with a focus on companies that have consistent and scalable business models. The company is targeting acquisitions that can contribute $8-10 million in adjusted EBITDA, with specific criteria for both tuck-in acquisitions in existing markets and expansion into new geographies.

The company’s stockholder value drivers include a strong growth strategy combining organic expansion and strategic acquisitions, durable and recurring demand through economic cycles, a resilient business model supported by a strong balance sheet, and a scalable business platform focused on revitalizing existing infrastructure.

As Limbach continues to execute its three-pillar growth strategy, investors can expect continued focus on high-margin ODR business, expanded service offerings, and strategic acquisitions to drive long-term value creation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.