Pilgrim Global buys Sable Offshore (SOC) shares worth $14.7m

Lincoln National Corporation (NYSE:LNC) presented its second quarter 2025 earnings results on July 31, showing strong performance across multiple business segments. The financial services company reported a 32% year-over-year increase in adjusted operating income, with particularly strong results in its Group Protection business and a notable recovery in its Life Insurance segment.

Quarterly Performance Highlights

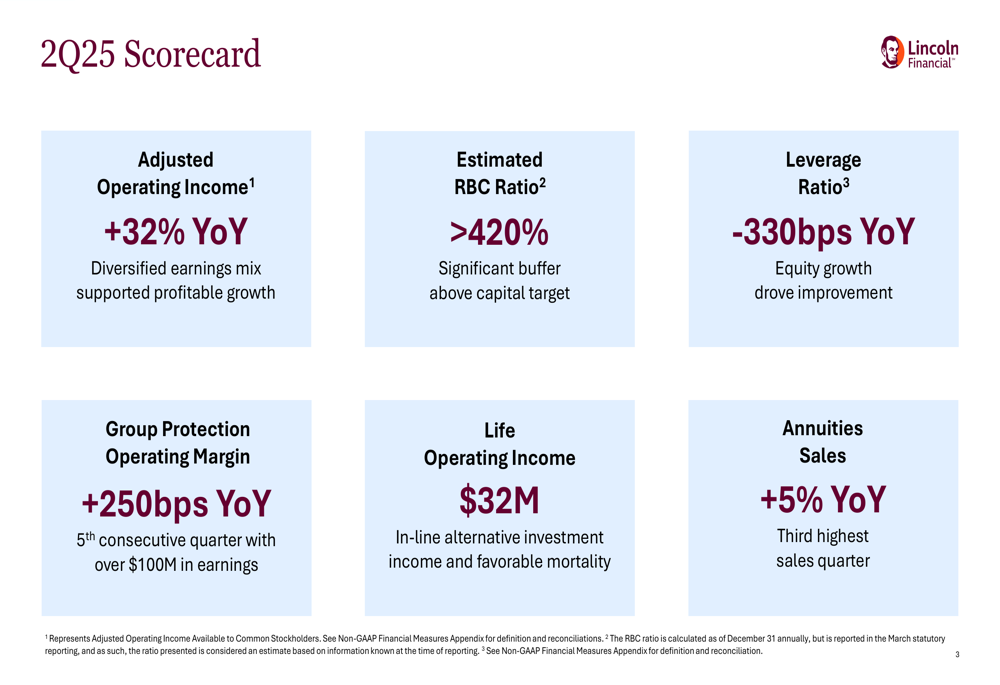

Lincoln National reported adjusted operating income of $427 million ($2.36 per share) for Q2 2025, representing a 32% increase compared to the same period last year. The company’s stock responded positively to these results, closing at $39.24 on October 14, up 2.57% for the day.

The company highlighted its diversified earnings mix as a key driver of profitable growth, alongside an estimated Risk-Based Capital (RBC) ratio exceeding 420%, providing a significant buffer above the company’s capital target.

As shown in the following quarterly scorecard, Lincoln National achieved growth across several key metrics while maintaining strong capital positions:

"We are building a stronger Lincoln grounded in a more resilient foundation and positioned to realize greater potential," said CEO Ellen Cooper in the recent earnings call, emphasizing the company’s strengthened foundation.

Segment Performance Analysis

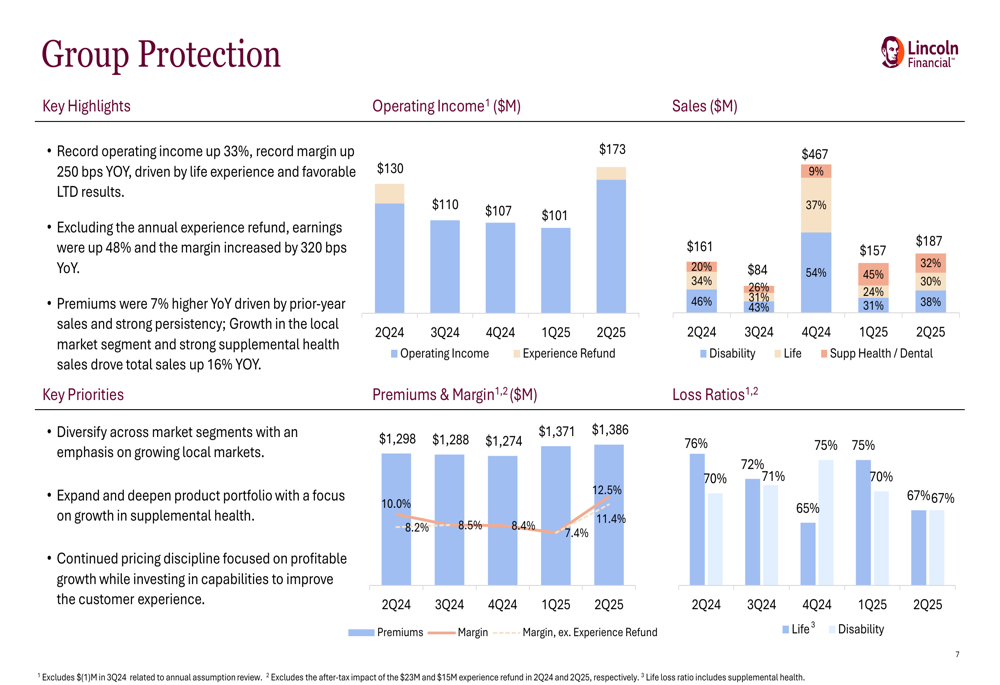

The Group Protection segment delivered record results, with operating income increasing 33% year-over-year to $173 million. This marks the fifth consecutive quarter with earnings exceeding $100 million. The segment’s operating margin improved by 250 basis points year-over-year, driven by favorable life experience, improved disability results, and sustained growth in supplemental health.

The following chart illustrates the Group Protection segment’s consistent performance improvement:

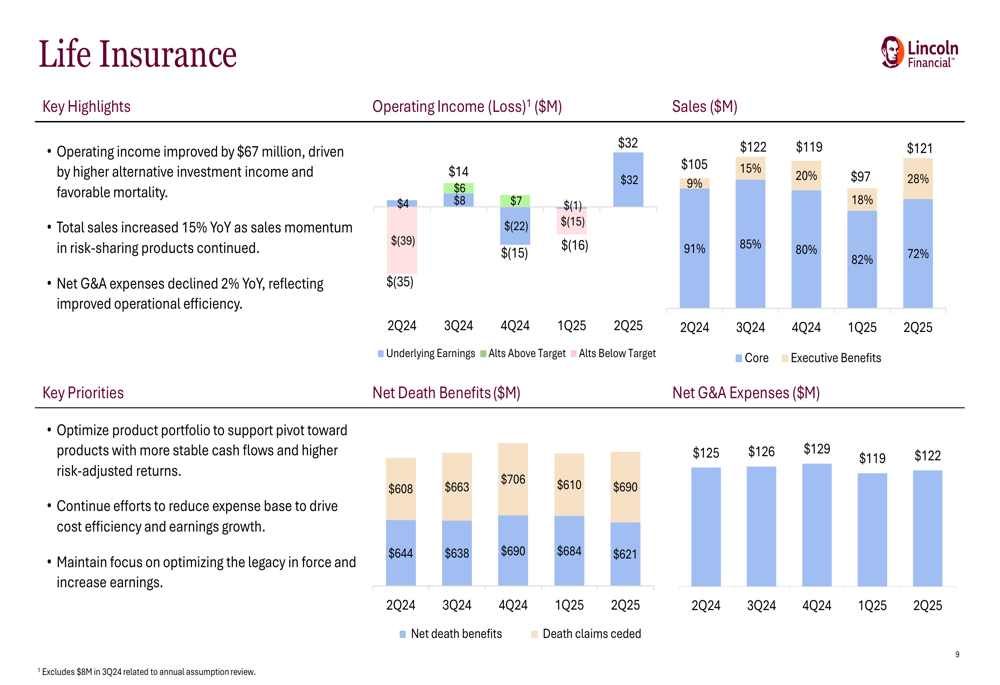

The Life Insurance segment showed significant improvement, with operating income of $32 million compared to a $35 million loss in Q2 2024. This $67 million improvement was attributed to higher alternative investment income, favorable mortality experience, and lower net general and administrative expenses. Life Insurance sales increased 15% year-over-year.

The Life Insurance segment’s turnaround is clearly visible in the following performance data:

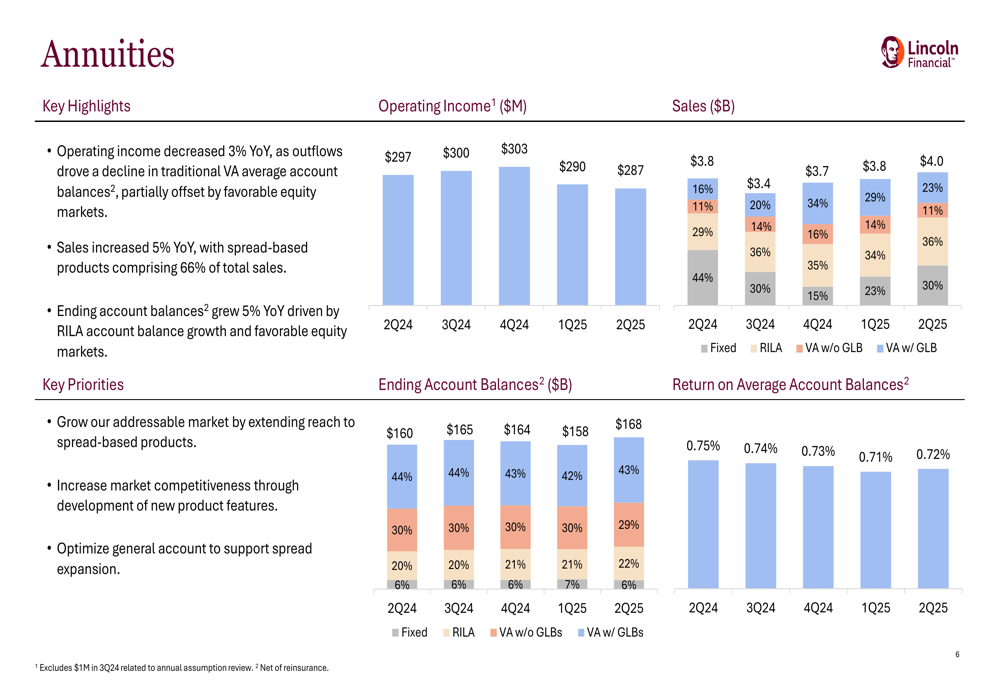

The Annuities segment saw a slight 3% year-over-year decrease in operating income to $287 million, despite a 5% increase in sales to $4 billion. Lincoln noted this was the third highest sales quarter for the segment. Ending account balances grew 5% year-over-year to $168 billion, benefiting from favorable equity markets.

The following chart shows the Annuities segment’s performance trends:

Retirement Plan Services experienced an 8% year-over-year decrease in operating income to $37 million. However, first-year sales grew almost 50%, driven by strong stable value sales, and ending account balances increased 8% year-over-year to $47 billion.

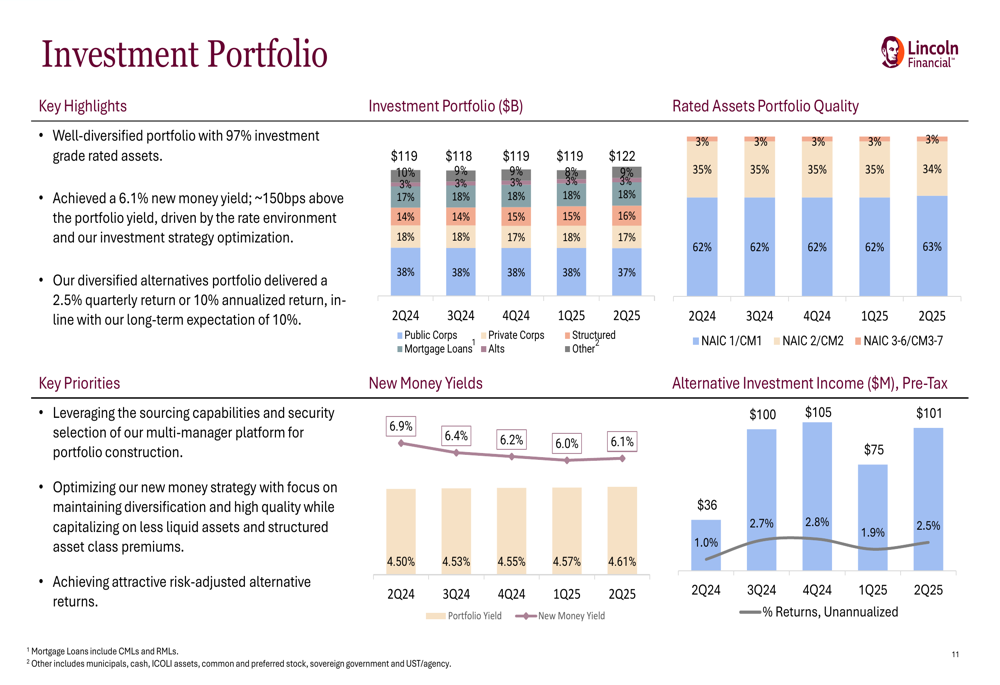

Capital Position and Investment Portfolio

Lincoln National reported significant improvement in its capital position, with the leverage ratio improving by 330 basis points year-over-year to 25.6%. The company maintained a well-diversified investment portfolio with 97% investment-grade rated assets and achieved a 6.1% new money yield.

The company’s alternative investments portfolio delivered a 2.5% quarterly return, contributing positively to overall results as shown in the following portfolio breakdown:

CFO Chris Nezipour highlighted the company’s strategic flexibility in the earnings call, stating, "Our strong capital position provides flexibility to strategically allocate resources."

Forward-Looking Statements

Looking ahead, Lincoln National remains optimistic about its future prospects. The company projects a group business margin of over 9% for the year and anticipates positive net flows in its Retirement Plan Services in Q3 2025.

The company is targeting a 45-60% free cash flow conversion by 2026, underscoring its focus on optimizing its legacy life portfolio. Lincoln also plans to deploy its Bain Capital investment over the next 18 months.

Despite these positive projections, investors should consider potential risks including market volatility, regulatory changes, competitive pressures, and broader economic conditions that could impact Lincoln’s performance.

With a price-to-book ratio of 0.89 and nine analysts revising their earnings estimates upward according to recent data, Lincoln National shows promising signs for value-oriented investors as it continues to execute on its strategic initiatives focused on innovation and operational efficiency.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.