NextEra Energy stock rises after Google power deal report

Introduction & Market Context

Loar Holdings LLC (NYSE:LOAR) released its Q1 2025 earnings presentation on May 14, 2025, revealing strong financial performance across all segments, particularly in defense. Despite the positive results, the stock has experienced volatility, closing at $67.62 on August 8, down 4.93% from its previous close.

The aerospace and defense component manufacturer continues to benefit from robust aftermarket demand and improving production environments for commercial OEMs. The company’s diversified portfolio across commercial, defense, and business aviation sectors has helped insulate it from market-specific challenges.

Quarterly Performance Highlights

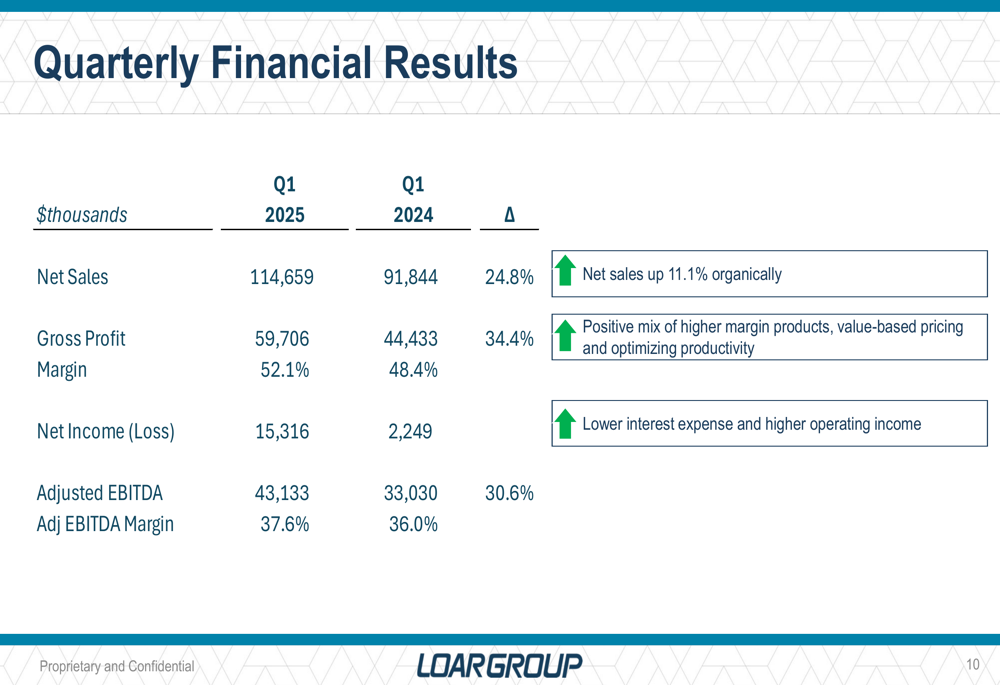

Loar Holdings reported Q1 2025 net sales of $114.7 million, representing a 24.8% increase compared to Q1 2024. Organic growth contributed 11.1% to this increase, with the remainder coming from acquisitions, including Applied Avionics which closed in Q3 2024.

The company achieved significant margin expansion, with gross profit increasing 34.4% year-over-year to $59.7 million. Gross profit margin improved to 52.1%, up from 48.4% in the prior year period. This improvement reflects a positive mix of higher margin products, value-based pricing, and productivity optimization initiatives.

As shown in the following quarterly financial results:

Net income saw a dramatic improvement, reaching $15.3 million compared to just $2.2 million in Q1 2024. This substantial increase reflects lower interest expense and higher operating income. The company’s adjusted EBITDA grew 30.6% to $43.1 million, with adjusted EBITDA margin expanding to 37.6% from 36.0% in the prior year period.

Segment Performance

Loar’s defense segment was the standout performer in Q1 2025, with sales increasing 30% year-over-year. This growth was driven by strong aftermarket demand across platforms and market share gains. The commercial aftermarket segment also performed well, with sales up 13%, benefiting from an aging commercial aircraft fleet and slower than anticipated production rate increases at OEMs. Commercial OEM sales increased by 8%, reflecting an improving production environment.

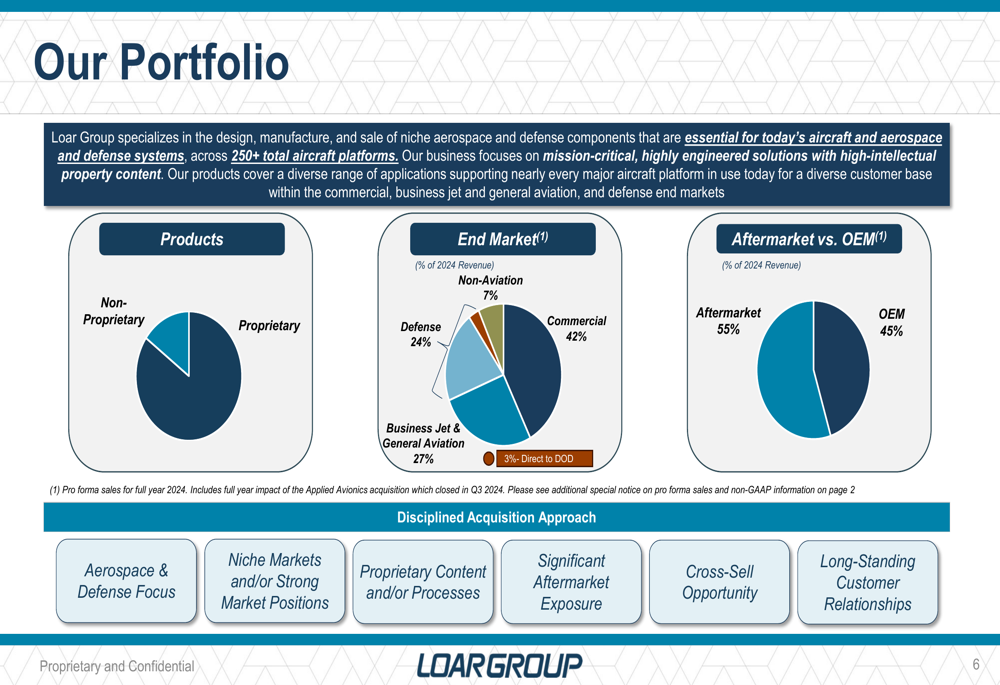

The company’s portfolio remains well-diversified across end markets, with commercial representing 42% of revenue, business jet and general aviation 27%, defense 24%, and non-aviation 7%. Notably, aftermarket sales account for 55% of total revenue, providing a stable and high-margin revenue stream.

As illustrated in the company’s portfolio breakdown:

Strategic Initiatives

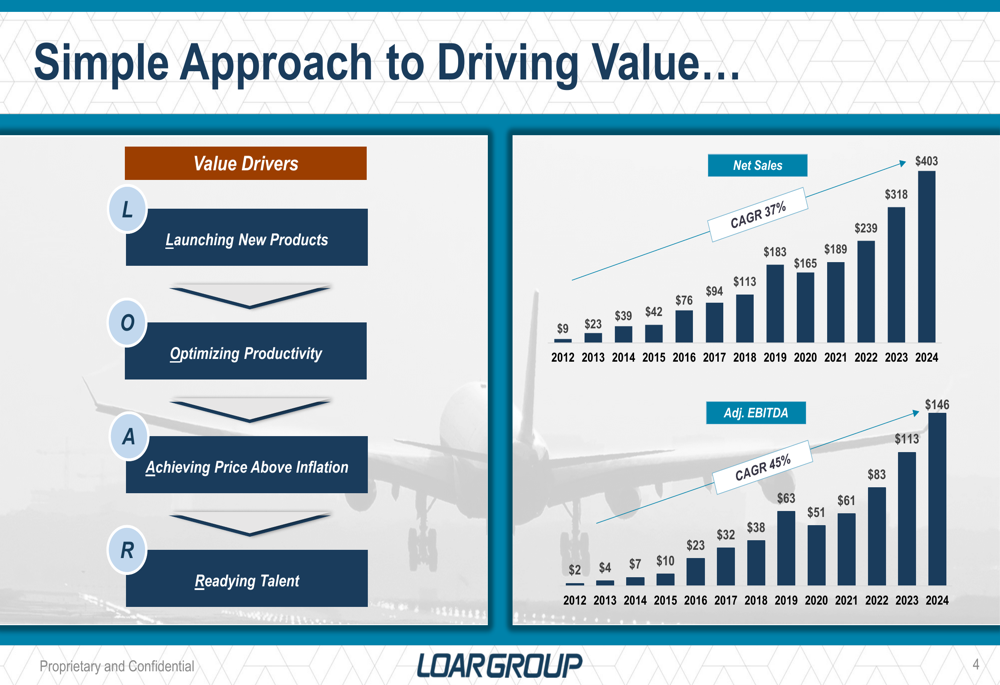

Loar Holdings continues to execute on its value-driving strategy, represented by the "LOAR" acronym: Launching New Products, Optimizing Productivity, Achieving Price Above Inflation, and Readying Talent. This approach has delivered impressive long-term results, with net sales growing at a 37% CAGR and adjusted EBITDA at a 45% CAGR from 2012 to 2024.

The company’s strategic focus is illustrated in the following chart showing its approach to driving value:

One notable product development highlighted in the presentation is the secondary cockpit barrier created in partnership with Airbus. The company developed this best-in-class design by collaborating across the group, moving from a clean sheet to prototype in just six months. Delivery of parts began in May 2025, and the barriers will be featured on new production aircraft in the US.

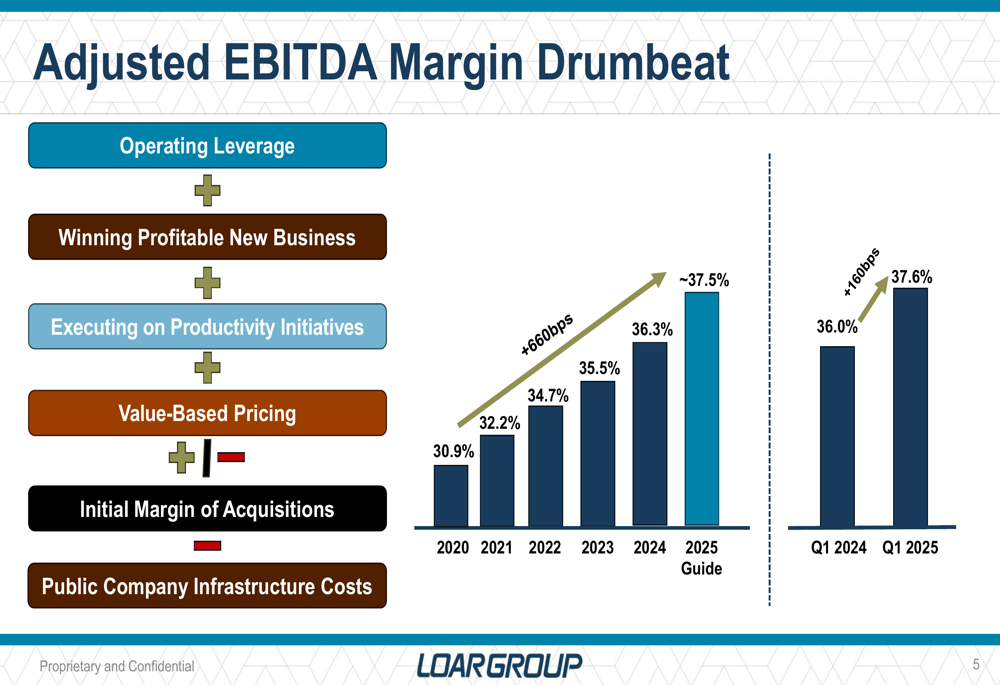

The company’s adjusted EBITDA margin has shown consistent improvement over time, increasing from 30.9% in 2020 to 37.6% in Q1 2025. This "margin drumbeat" has been driven by operating leverage, winning profitable new business, executing on productivity initiatives, and value-based pricing.

As shown in the following chart of adjusted EBITDA margin progression:

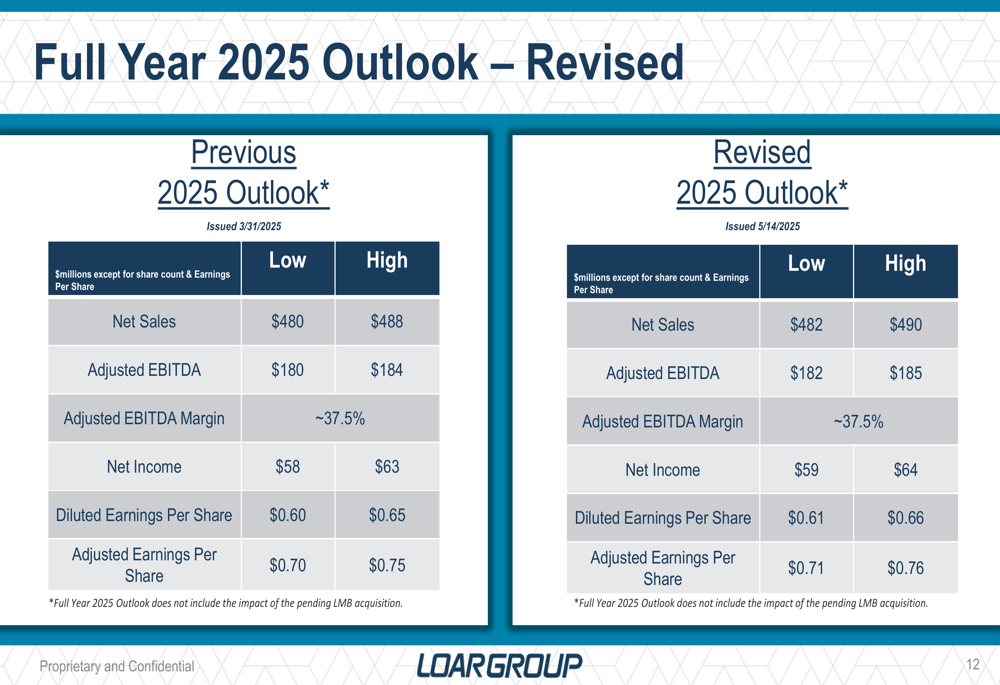

Revised Outlook

Based on strong Q1 performance, Loar Holdings has raised its full-year 2025 guidance. The company now expects net sales of $482-490 million (up from $480-488 million), adjusted EBITDA of $182-185 million (up from $180-184 million), and adjusted earnings per share of $0.71-0.76 (up from $0.70-0.75).

The revised outlook is presented in the following comparison table:

The company’s market assumptions for 2025 include high single-digit growth in commercial, business jet, and general aviation OEM; low double-digit growth in the aftermarket (upgraded from high single-digit previously); and high double-digit growth (17-20%) in defense.

Notably, the full-year 2025 outlook does not include the impact of the pending LMB acquisition, suggesting potential upside to the current guidance. The company expects capital expenditures of approximately $14 million, interest expense of about $28 million, and an effective tax rate of around 30% for the full year.

With a strong balance sheet, diversified product portfolio, and growing presence in high-growth segments like defense, Loar Holdings appears well-positioned to continue its growth trajectory through 2025, despite recent stock price volatility.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.