Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

Lockheed Martin Corporation (NYSE:LMT) released its second quarter 2025 results on July 22, revealing significant operational challenges despite stable sales. The defense giant’s stock tumbled 7.28% in premarket trading to $426.99 following the earnings release, as investors reacted to substantial program losses and reduced profit guidance.

The disappointing Q2 results mark a stark reversal from the company’s strong first quarter performance, when Lockheed Martin exceeded analyst expectations with earnings per share of $7.28 against a forecast of $6.35. The defense contractor’s presentation highlighted several major program losses that severely impacted profitability while maintaining its sales outlook.

Quarterly Performance Highlights

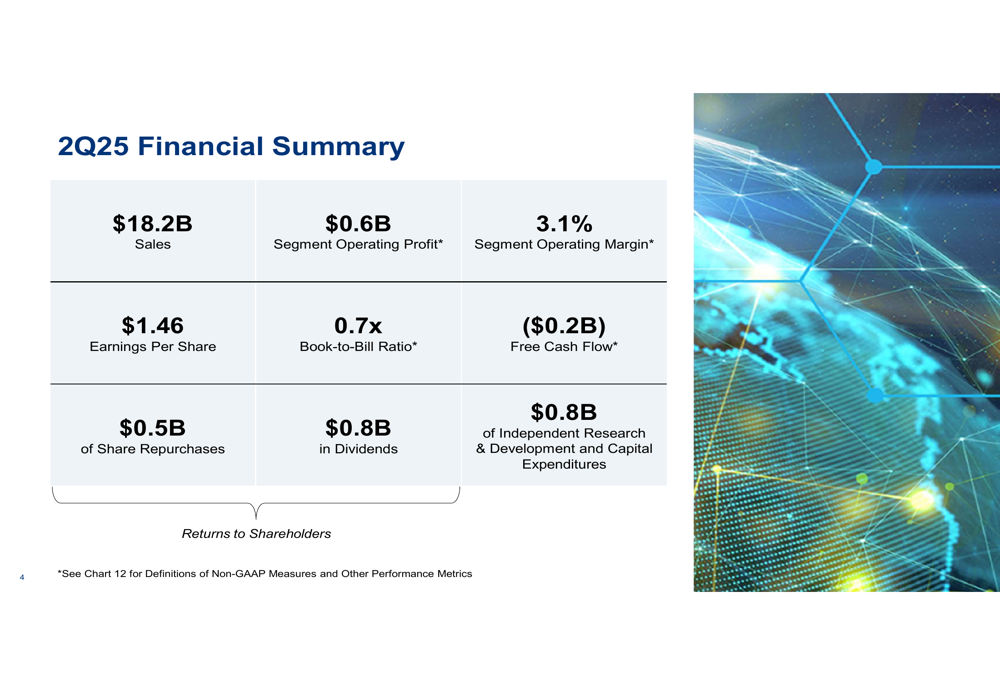

Lockheed Martin reported second quarter sales of $18.2 billion, essentially flat compared to the same period last year. However, segment operating profit plummeted to $0.6 billion, resulting in a segment operating margin of just 3.1% – a dramatic decline from 11.3% in Q2 2024. Earnings per share fell to $1.46, while free cash flow turned negative at ($0.2 billion).

As shown in the following financial summary:

Despite the operational challenges, Lockheed Martin continued returning capital to shareholders, with $0.5 billion in share repurchases and $0.8 billion in dividends during the quarter. The company’s book-to-bill ratio of 0.7x indicates slower order intake relative to recognized revenue.

Segment Analysis

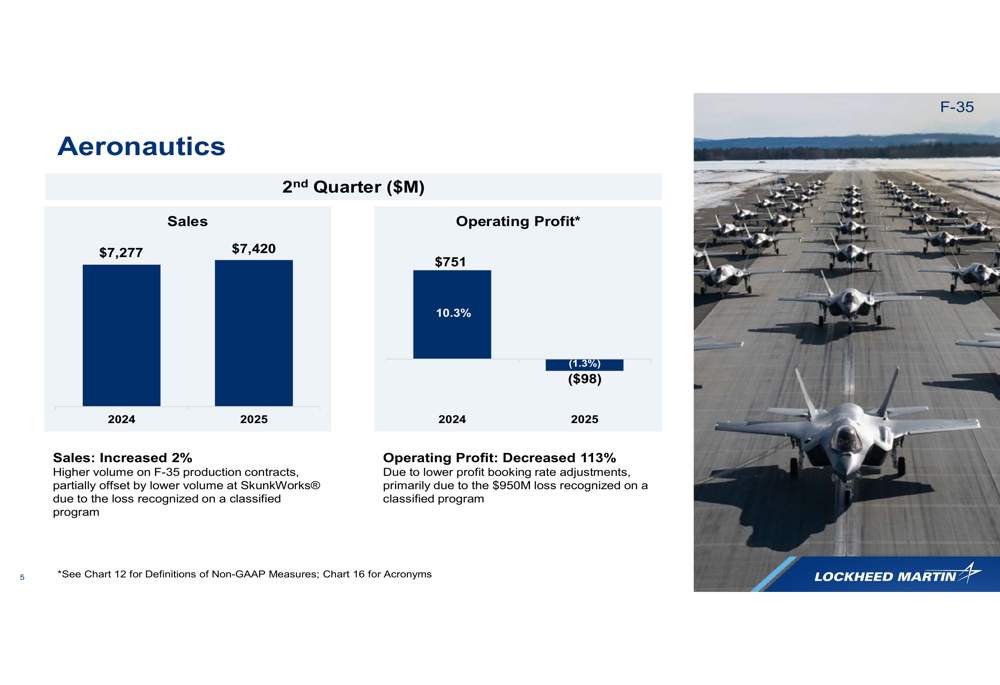

The Aeronautics segment, Lockheed’s largest business unit, reported a 2% increase in sales to $7.42 billion but recorded an operating loss of $98 million – a 113% decline from the $751 million profit in Q2 2024. This dramatic reversal was primarily attributed to a $950 million loss recognized on a classified program.

The following chart illustrates the Aeronautics segment performance:

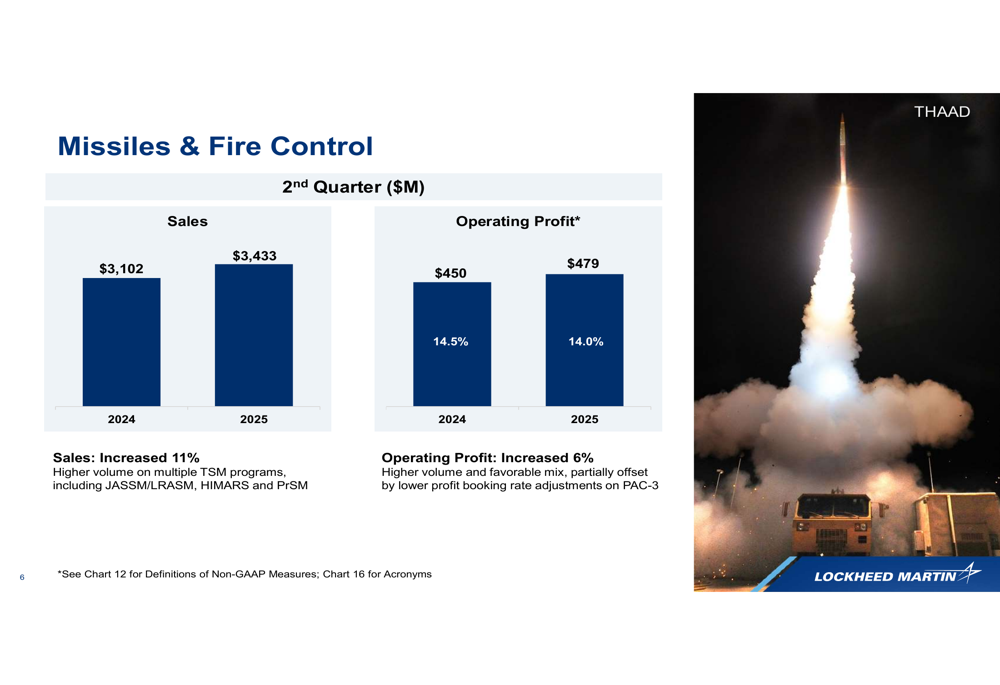

The Missiles & Fire Control segment provided a bright spot, with sales increasing 11% to $3.43 billion and operating profit rising 6% to $479 million. This growth was driven by higher volumes across multiple tactical strike missile programs, including JASSM/LRASM, HIMARS, and PrSM systems.

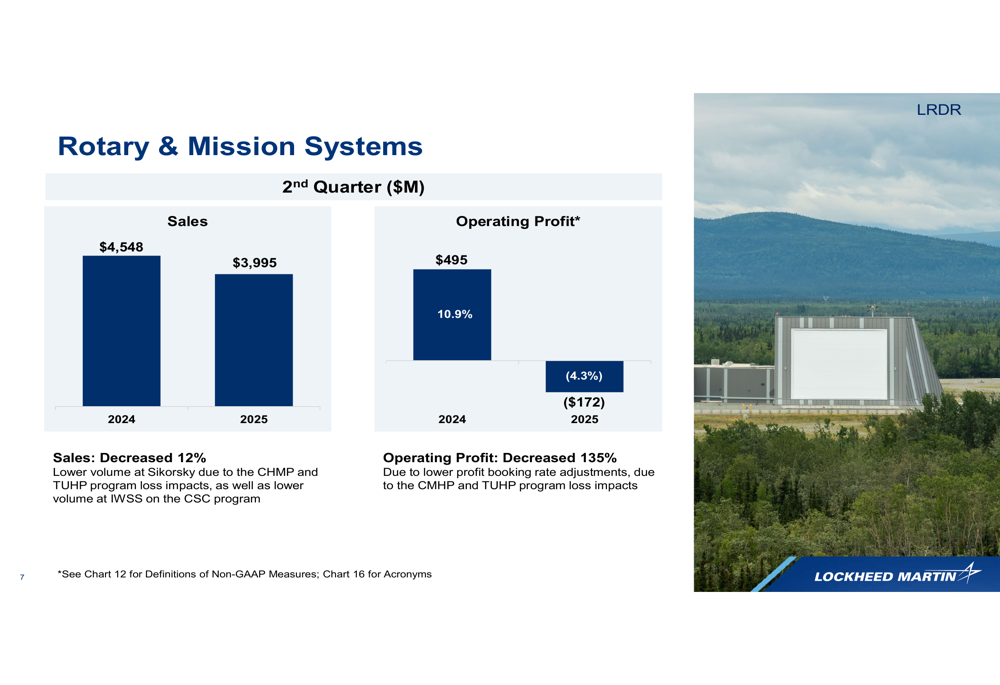

Rotary & Mission Systems experienced significant challenges, with sales declining 12% to $3.99 billion and an operating loss of $172 million compared to a $495 million profit in Q2 2024. The 135% profit decline was attributed to losses on the CHMP and TUHP helicopter programs at Sikorsky.

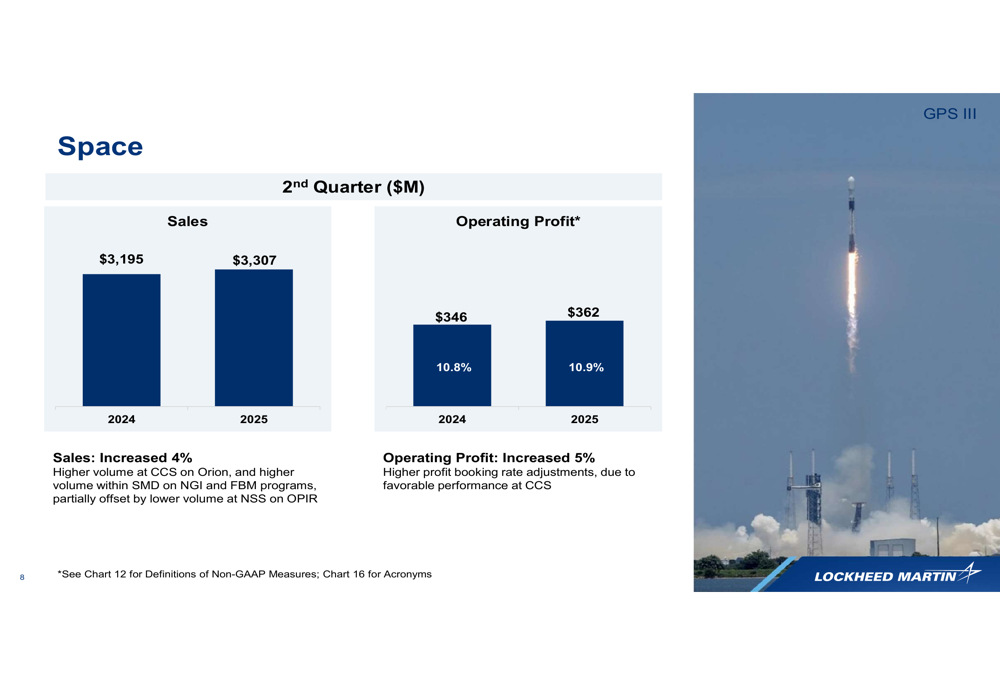

The Space segment delivered modest growth with sales up 4% to $3.31 billion and operating profit increasing 5% to $362 million. This improvement was driven by higher volume on the Orion spacecraft program and favorable performance adjustments.

Guidance Revisions

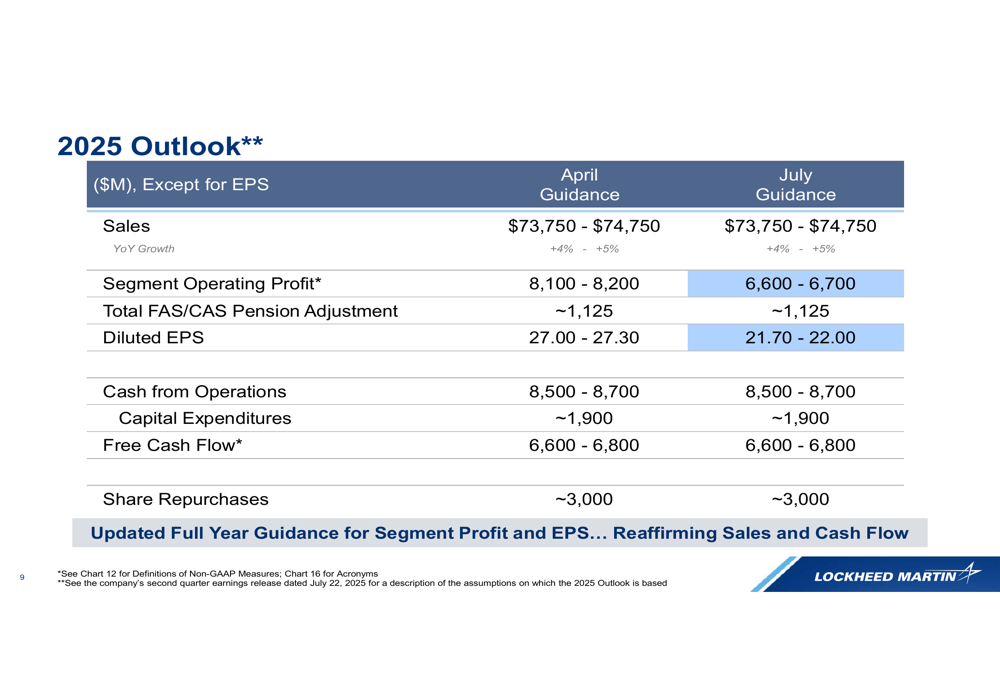

While maintaining its full-year sales guidance of $73.75-$74.75 billion (representing 4-5% year-over-year growth), Lockheed Martin significantly reduced its profit outlook. The company slashed segment operating profit guidance from $8.1-$8.2 billion to $6.6-$6.7 billion and cut diluted EPS guidance from $27.00-$27.30 to $21.70-$22.00.

The following chart details these guidance revisions:

Despite the profit challenges, Lockheed Martin reaffirmed its cash flow targets of $8.5-$8.7 billion in cash from operations and $6.6-$6.8 billion in free cash flow. The company also maintained its commitment to approximately $3 billion in share repurchases for 2025.

Strategic Initiatives & Forward Outlook

Lockheed Martin’s presentation emphasized that its products continue to prove their value in active theaters, particularly highlighting the F-35, F-22, PAC-3, THAAD, and AEGIS systems supporting operations in the Middle East. The company also noted strong demand signals from the administration and budget activities, specifically mentioning initiatives like Golden Dome, munitions programs, and the CH-53K helicopter.

In its summary, management stated they are "Setup to Deliver 2nd Half Results and Full Year Outlook" and remain "Focused on Operational Excellence to Achieve Customer Commitments." The company maintains it is "Poised to Drive Long-term Growth & Value Creation for Shareholders" despite the current operational challenges.

The revised segment guidance shows Aeronautics expecting full-year sales of $28.95-$29.35 billion with operating profit of $2.0-$2.04 billion. Missiles & Fire Control is projected to generate $14.05-$14.35 billion in sales with $1.96-$1.99 billion in operating profit. Rotary & Mission Systems anticipates $17.8-$18.0 billion in sales with $1.34-$1.36 billion in operating profit, while Space is expected to contribute $12.95-$13.05 billion in sales and $1.31-$1.32 billion in operating profit.

The significant reduction in profit guidance while maintaining sales targets suggests Lockheed Martin faces substantial margin pressure as it works through the program challenges identified in the second quarter. Investors will likely focus on whether these operational issues are contained or if they could spread to other programs in the company’s extensive defense portfolio.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.