Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Magnora ASA (OSE:MGN) released its Q2 2025 presentation on July 18, highlighting the company’s continued expansion in the renewable energy sector despite reporting negative quarterly earnings. The pure-play renewable energy developer has maintained its asset-light approach while growing its project portfolio by 65% year-over-year to 8.0 GW.

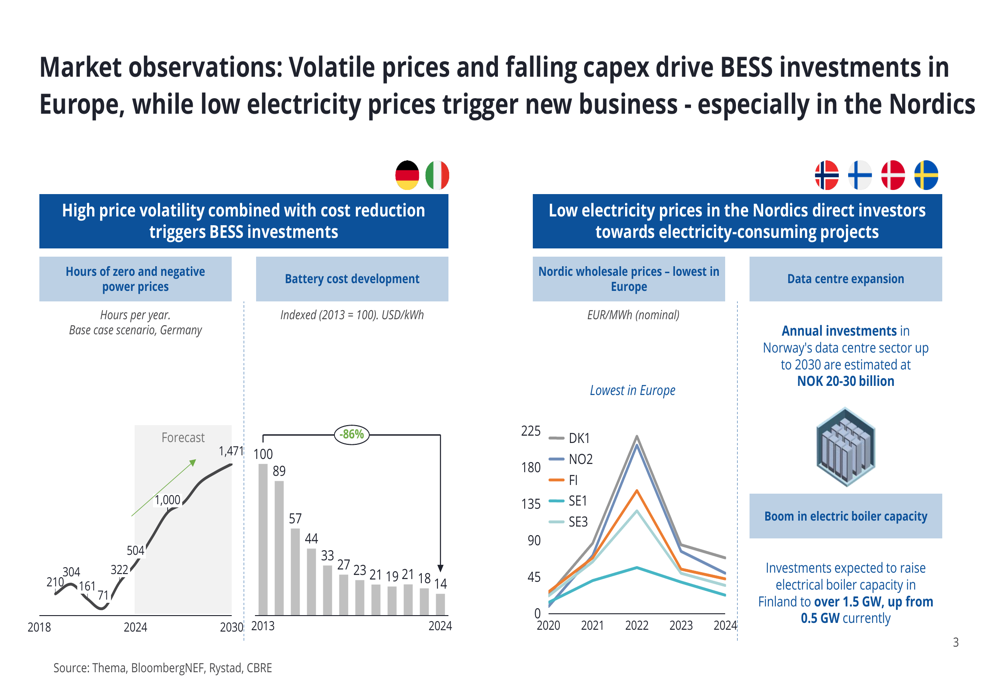

The presentation emphasized market trends driving Magnora’s strategy, including high price volatility combined with battery cost reductions triggering BESS (Battery Energy Storage System) investments, particularly in Germany. The company also noted how low electricity prices in the Nordics are directing investors toward electricity-consuming projects like data centers.

As shown in the following chart illustrating market observations regarding electricity prices and battery costs:

Quarterly Performance Highlights

Magnora’s Q2 2025 results showed a significant shift from the positive performance reported in Q1. The company posted an operating loss of NOK 27.8 million and a net loss of NOK 22.2 million for the quarter, contrasting with the NOK 8.6 million net profit reported in Q1 2025.

The company’s condensed profit and loss statement reveals the financial details of the quarter:

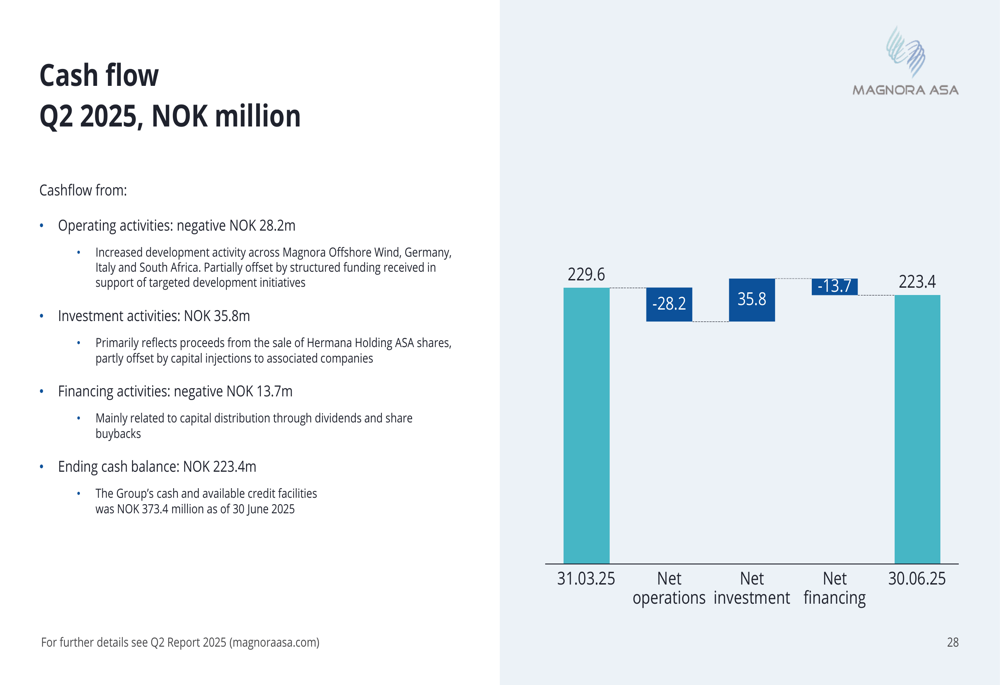

Despite the negative quarterly earnings, Magnora maintained its strong cash position of NOK 223 million, complemented by a NOK 150 million credit line. The company attributes the increased expenses to development activities across multiple regions, particularly in Magnora Offshore Wind, Germany, Italy, and South Africa.

The cash flow statement for Q2 2025 illustrates the financial movements:

A key achievement during the quarter was the company’s completed transition to a 100% renewable-energy business model following the successful divestment of Hermana Holding ASA shares.

Strategic Initiatives

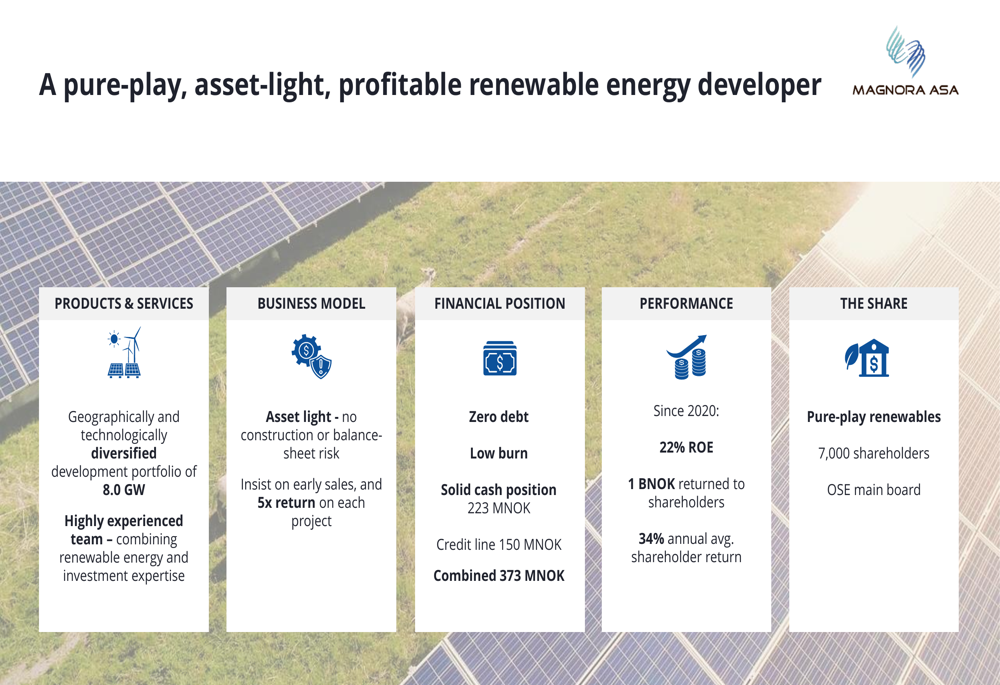

Magnora continues to position itself as a pure-play, asset-light, and profitable renewable energy developer with a geographically and technologically diversified portfolio. The company’s business model emphasizes early-stage investments with no construction or balance-sheet risk, targeting a minimum 5x return on each project.

The following slide summarizes Magnora’s core identity and business approach:

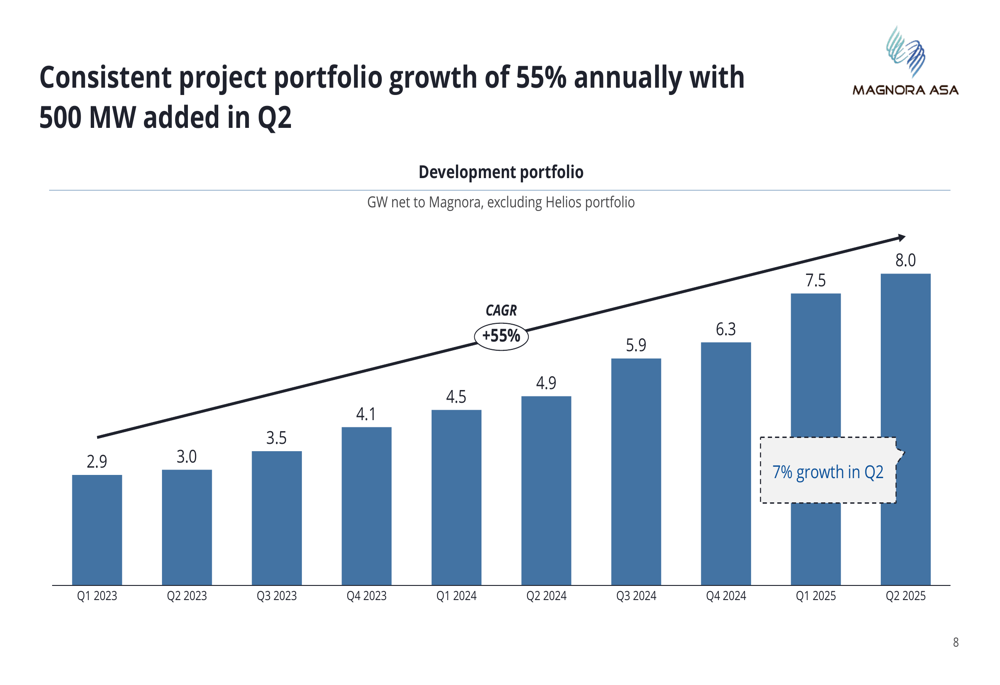

The company’s portfolio has shown consistent growth, reaching 8.0 GW in Q2 2025, representing a 55% CAGR annually with 500 MW added in the most recent quarter:

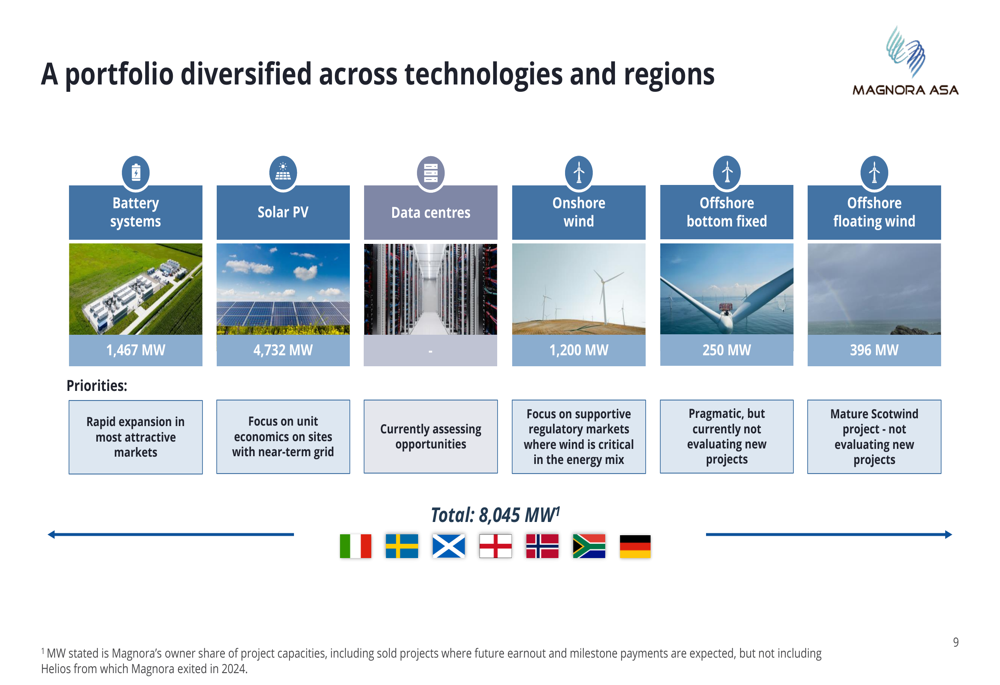

Magnora’s portfolio diversification across technologies and regions provides resilience and multiple growth avenues. The company has strategically allocated resources to battery systems and solar PV in Germany and Italy, while maintaining positions in offshore wind in Scotland and Sweden:

A notable strategic development is Magnora’s entry into the data center market, which the company views as complementary to its renewable energy portfolio. The Nordic data center market is expected to grow significantly, with power demand forecasted to increase from 11 TWh in 2024 to 62 TWh in 2050.

Detailed Financial Analysis

Magnora’s financial strategy continues to emphasize capital discipline and shareholder returns despite the negative quarterly earnings. The company maintained its capital distribution program with regular dividends of NOK 12 million in both Q1 and Q2, along with share buybacks totaling NOK 1.6 million in Q2.

The company’s development and M&A expenses increased to NOK 19.0 million in Q2 2025, reflecting its accelerated investment in project development across multiple markets. This contributed to the negative EBITDA of NOK 24.4 million for the quarter.

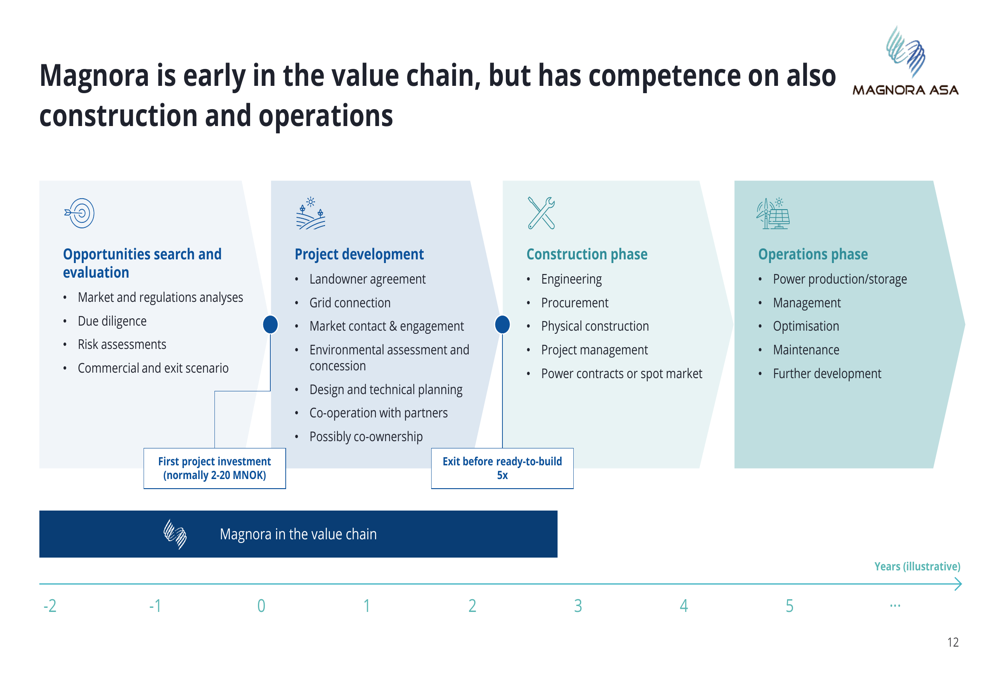

Magnora’s business model positions the company early in the renewable energy value chain, focusing on opportunities search, evaluation, and project development while avoiding the capital-intensive construction and operations phases:

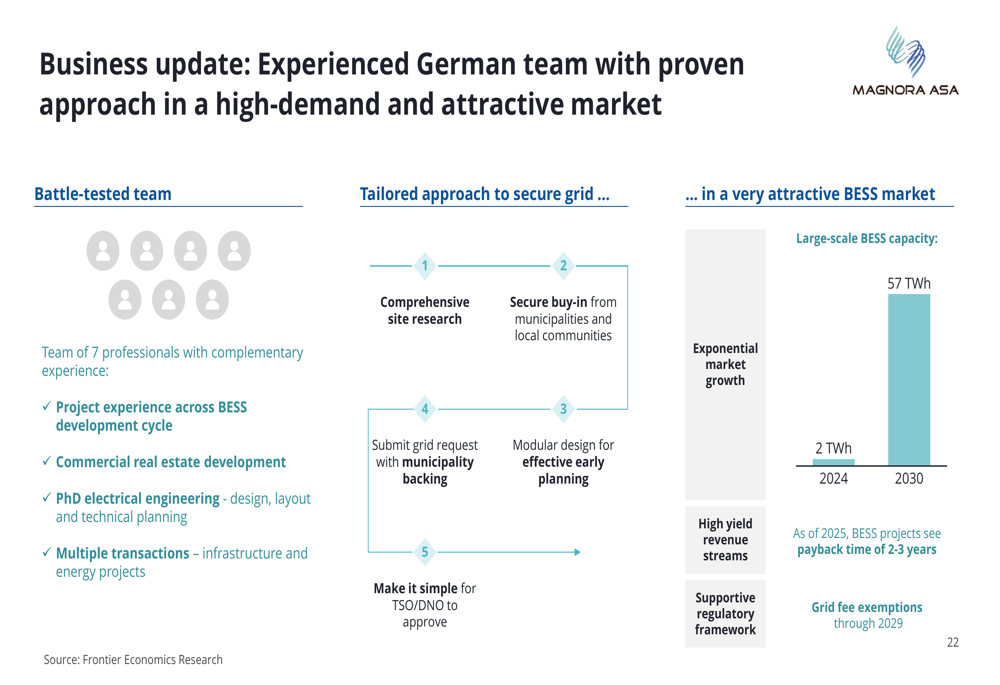

In Germany, Magnora has assembled an experienced team to capitalize on the attractive BESS market, where capacity is expected to grow from 2 TWh in 2024 to 57 TWh in 2030. The company secured its first site in Germany during Q2 through a Letter of Intent with a leading European infrastructure investor:

Forward-Looking Statements

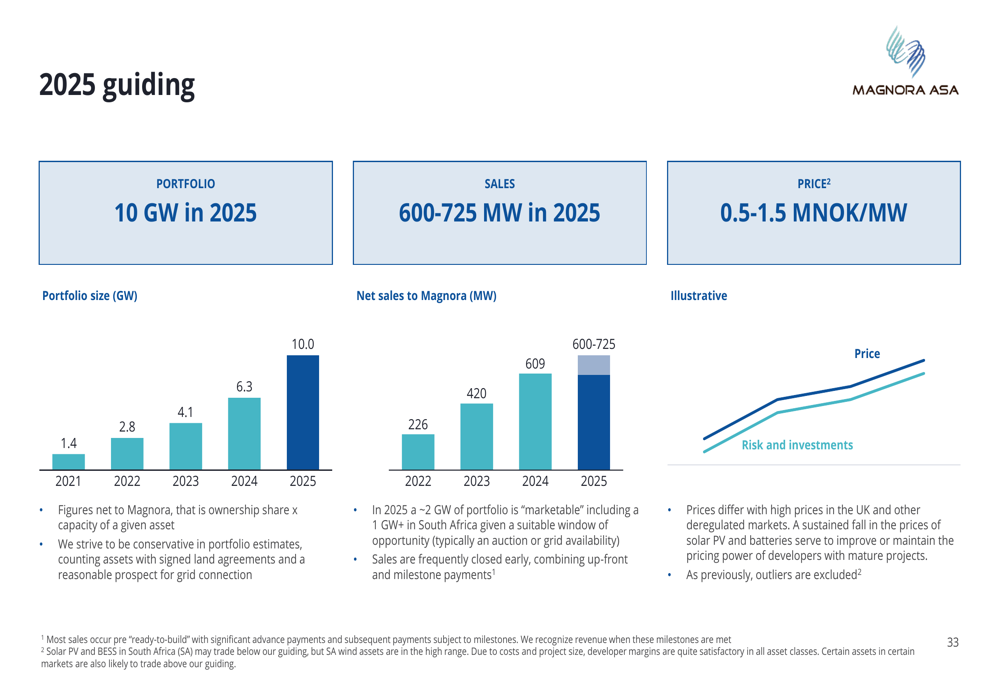

Looking ahead, Magnora maintained its 2025 guidance with a portfolio target of 10 GW, sales target of 600-725 MW, and price target of 0.5-1.5 MNOK/MW. The company expects to accelerate development efforts and advance commercial initiatives through farm-downs and sales.

The following chart illustrates Magnora’s 2025 guiding figures:

In South Africa, Magnora reported ongoing sales processes for approximately 500 MW of projects, including ~250 MW of solar and ~250 MW of wind. The company’s Red Sands project reached financial close, triggering the final milestone payment.

In Italy, Magnora is scaling its team and portfolio for MACSE auctions, with 450 MW of mid-stage BESS projects targeting auctions in 2026 and 2027. The company added 200 MW to its Italian portfolio in Q2 alone.

Magnora’s stock closed at NOK 23.65 on July 17, 2025, down 0.63% for the day. The company’s shares have traded between NOK 18.70 and NOK 33.00 over the past 52 weeks, reflecting market volatility but maintaining a position well above the yearly low.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.