Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Martin Marietta Materials Inc . (NYSE:MLM) presented its second quarter 2025 results on August 7, showcasing record-breaking performance in its aggregates business and unveiling strategic initiatives to enhance its market position. The company reported solid financial growth despite flat shipment volumes, highlighting its pricing power and operational efficiency in a market buoyed by infrastructure spending.

Quarterly Performance Highlights

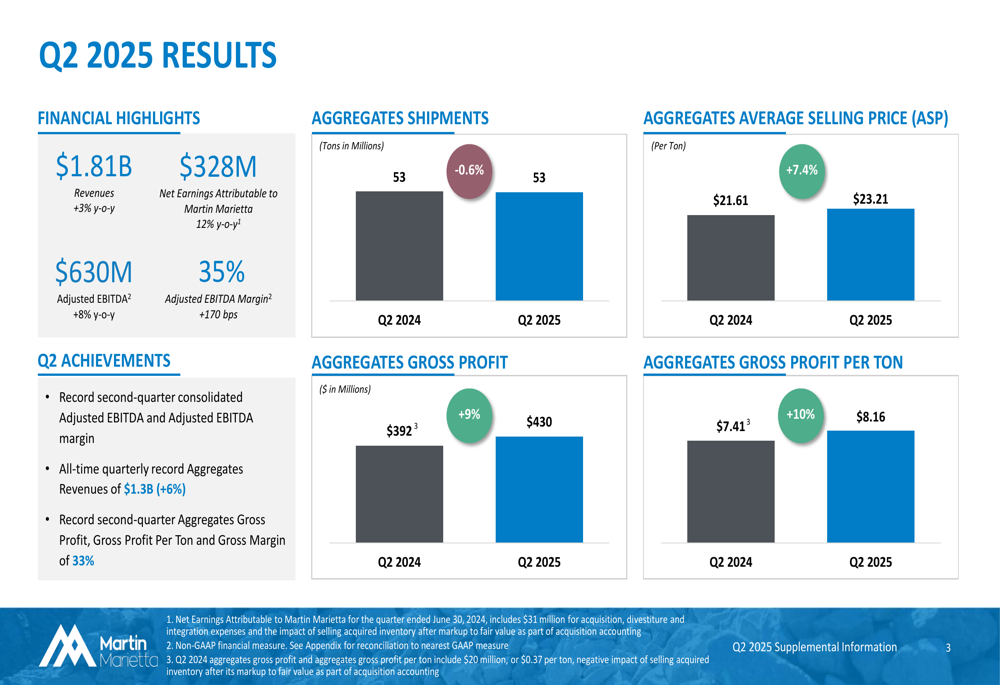

Martin Marietta delivered strong financial results for Q2 2025, with revenues reaching $1.81 billion, a 3% increase year-over-year. Net earnings attributable to the company rose 12% to $328 million, while adjusted EBITDA grew 8% to $630 million. The adjusted EBITDA margin expanded by 170 basis points to 35%, marking a record second-quarter performance.

The company’s aggregates business, which continues to be its primary focus, achieved all-time quarterly record revenues of $1.3 billion, up 6% from the previous year. While aggregates shipments remained relatively flat at 53 million tons (a slight decrease of 0.6%), average selling prices increased by 7.4% to $23.21 per ton, demonstrating the company’s strong pricing power.

As shown in the following quarterly performance chart:

This pricing strength, combined with operational efficiencies, drove aggregates gross profit up 9% to $430 million, with gross profit per ton increasing 10% to $8.16. The aggregates segment achieved a record second-quarter gross margin of 33%, reinforcing Martin Marietta’s strategy to prioritize its highest-margin business line.

Strategic Initiatives

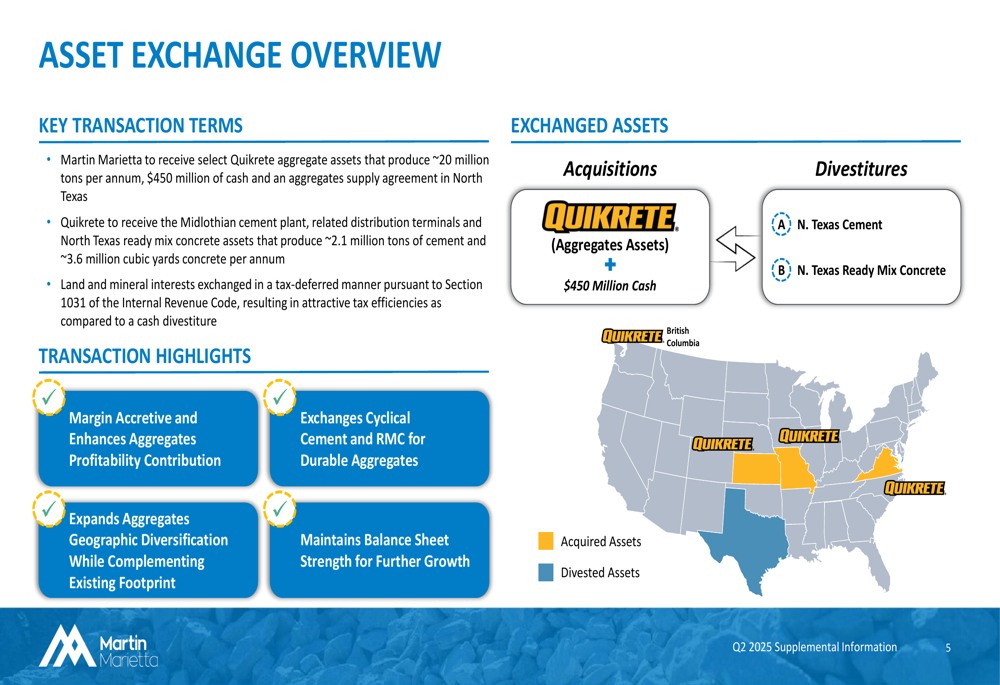

A centerpiece of Martin Marietta’s presentation was the announcement of a significant asset exchange with Quikrete, designed to enhance the company’s focus on its core aggregates business. Under the terms of the exchange, Martin Marietta will receive select Quikrete aggregate assets producing approximately 20 million tons per annum, $450 million in cash, and an aggregates supply agreement in North Texas.

In return, Quikrete will acquire Martin Marietta’s Midlothian cement plant and North Texas ready-mix concrete assets. The transaction is structured as a tax-deferred exchange and is described as margin accretive, expanding geographic diversification while maintaining balance sheet strength.

The strategic repositioning is illustrated in the following map showing the acquired and divested assets:

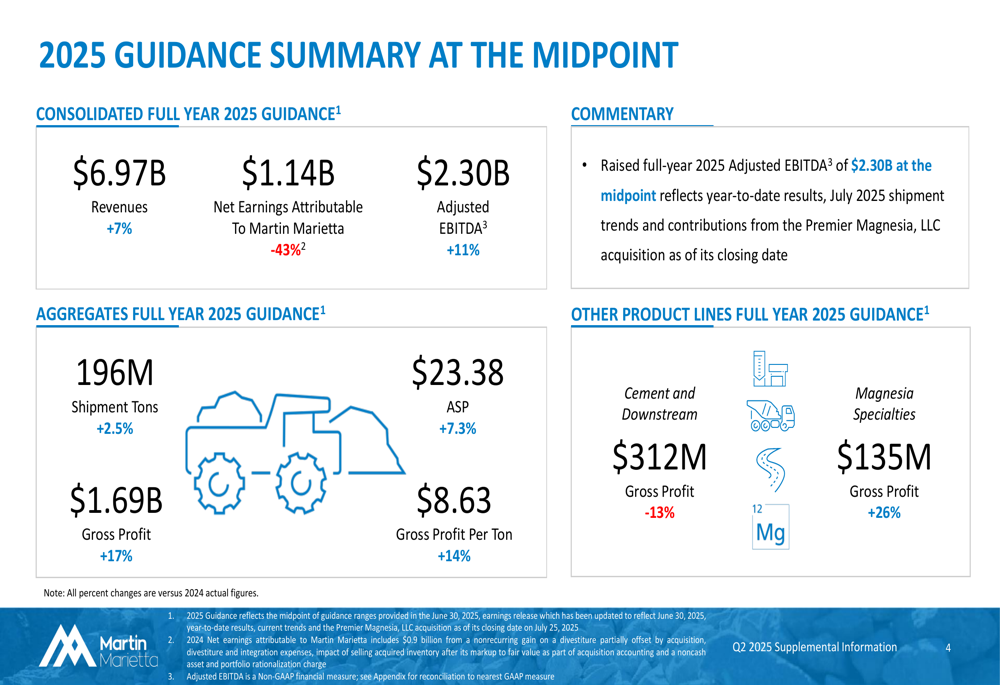

The company also referenced its acquisition of Premier Magnesia as contributing to its raised full-year guidance, indicating a continued strategy of portfolio optimization through both divestments and targeted acquisitions.

Forward-Looking Statements

Martin Marietta raised its full-year 2025 guidance, reflecting confidence in its business outlook and the impact of recent strategic moves. At the midpoint of guidance, the company now projects:

- Revenues of $6.97 billion, up 7% year-over-year

- Adjusted EBITDA of $2.30 billion, an 11% increase

- Aggregates shipments of 196 million tons, up 2.5%

- Aggregates average selling price of $23.38 per ton, up 7.3%

- Aggregates gross profit of $1.69 billion, a 17% increase

The detailed guidance breakdown is presented in the following slide:

Notably, the guidance shows a projected 43% decrease in net earnings attributable to Martin Marietta, reaching $1.14 billion. This significant decline contrasts with the growth in revenue and adjusted EBITDA, potentially indicating one-time gains in the previous year or accounting effects related to the asset exchange with Quikrete.

The company also announced its upcoming Capital Markets Day on September 3, 2025, in New York City, where management will highlight the SOAR 2030 growth strategy, suggesting a focus on long-term strategic planning beyond current market conditions.

Market Outlook

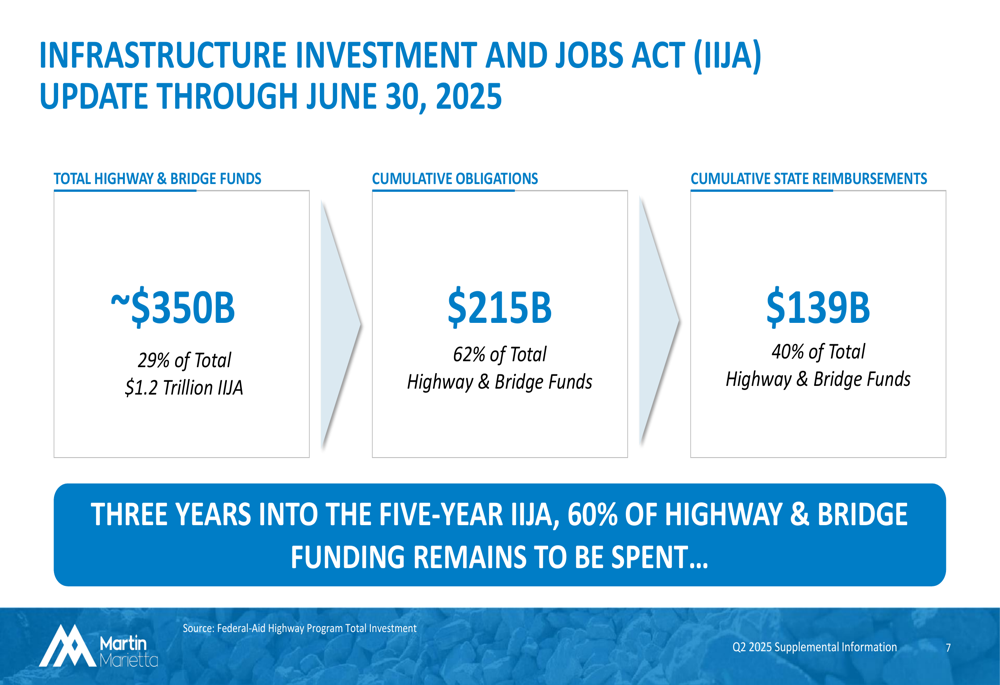

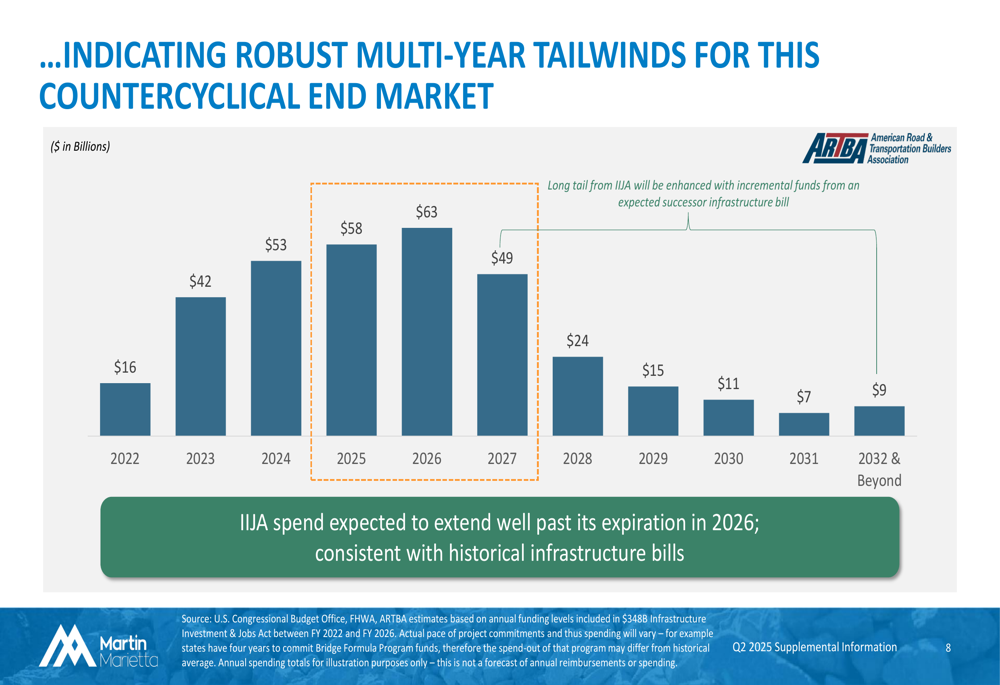

Martin Marietta’s presentation emphasized robust multi-year tailwinds across its end markets, particularly in infrastructure. The company provided an update on the Infrastructure Investment and Jobs Act (IIJA), noting that three years into the five-year program, 60% of highway and bridge funding remains to be spent. Total (EPA:TTEF) highway and bridge funds amount to approximately $350 billion, representing 29% of the total $1.2 trillion IIJA.

The following chart illustrates the current status of IIJA funding deployment:

The company expects infrastructure spending to extend well beyond the IIJA’s 2026 expiration, consistent with historical patterns from previous infrastructure bills. This projection is supported by data showing continued spending through 2032 and beyond:

Beyond infrastructure, Martin Marietta identified positive trends in nonresidential construction, highlighting data centers, warehouses, and manufacturing facilities as key drivers. In the residential sector, both single-family and multi-family housing were noted as contributing to demand, though specific growth rates were not provided.

Conclusion

Martin Marietta’s Q2 2025 presentation portrays a company successfully executing its strategy of focusing on high-margin aggregates while strategically repositioning its asset portfolio. The combination of strong pricing power, operational efficiency, and strategic transactions has enabled the company to deliver record margins despite flat shipment volumes.

With raised guidance for 2025 and the upcoming unveiling of its SOAR 2030 strategy, Martin Marietta appears confident in its ability to capitalize on infrastructure spending and other market tailwinds. However, investors may seek clarity on the projected decline in net earnings despite growth in other financial metrics, as well as more details on the long-term impact of the Quikrete asset exchange.

The company’s stock closed at $598.04 on August 6, 2025, down 1.56% from the previous close, suggesting some market reaction to the Q2 results and strategic announcements.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.