Novo Nordisk, Eli Lilly slide after Trump comments on weight loss drug pricing

Introduction & Market Context

Mativ Holdings Inc (NYSE:MATV) shares surged over 30% following the release of its second quarter 2025 earnings presentation on August 7, 2025. The stock jumped to $8.20, up from the previous close of $6.28, as investors responded positively to operational improvements and forward guidance despite continued GAAP losses. This dramatic price movement represents a significant recovery for a stock that had been trading near its 52-week low of $4.34.

The market’s enthusiastic reaction comes after a challenging first quarter where Mativ missed earnings expectations with a reported EPS of -$0.14 against a forecast of $0.12. The second quarter results suggest the company’s strategic initiatives may be gaining traction.

Quarterly Performance Highlights

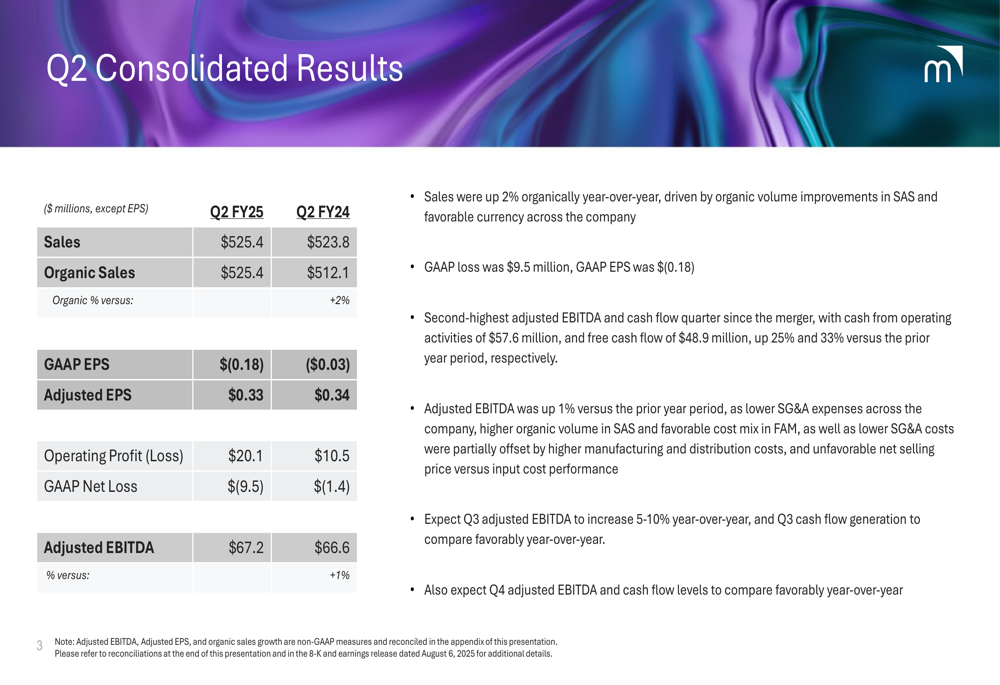

Mativ reported Q2 2025 sales of $525.4 million, representing a slight increase from $523.8 million in Q2 2024 and organic growth of 2% year-over-year. While the company posted a GAAP net loss of $9.5 million (compared to a $1.4 million loss in Q2 2024) and a GAAP EPS of -$0.18 (versus -$0.03 in the prior year), operating profit more than doubled to $20.1 million from $10.5 million in Q2 2024.

As shown in the following consolidated results:

The company’s adjusted EBITDA showed modest improvement, reaching $67.2 million, up 1% from $66.6 million in the same period last year. Adjusted EPS came in at $0.33, slightly below the $0.34 reported in Q2 2024. Management highlighted that this represents the second-highest adjusted EBITDA and cash flow quarter since the merger.

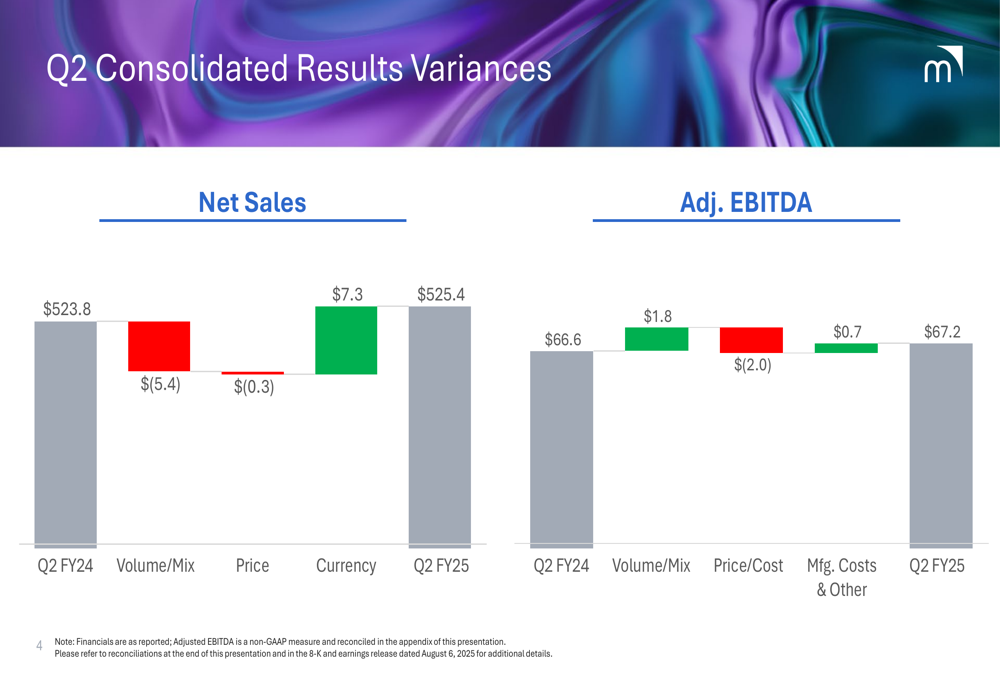

A detailed breakdown of the quarter’s performance variances reveals that currency effects provided a $7.3 million boost to sales, offsetting negative impacts from volume/mix and pricing:

Segment Performance

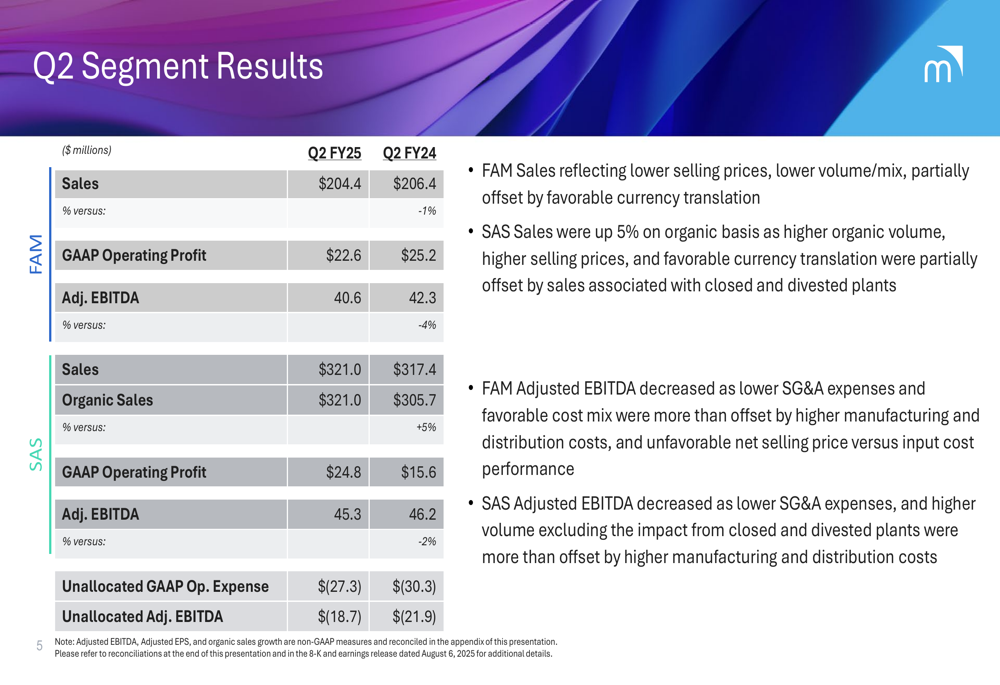

Mativ’s performance varied across its two main business segments. The Fiber-Based Materials (FAM) segment saw sales decline 1% to $204.4 million, with adjusted EBITDA decreasing 4% to $40.6 million, reflecting lower selling prices and reduced volume.

In contrast, the Sustainable and Adhesive Solutions (SAS) segment demonstrated stronger performance with sales of $321.0 million, representing 5% organic growth. However, adjusted EBITDA for this segment also declined slightly by 2% to $45.3 million, despite higher sales volumes.

The segment breakdown illustrates these contrasting performances:

Strategic Initiatives

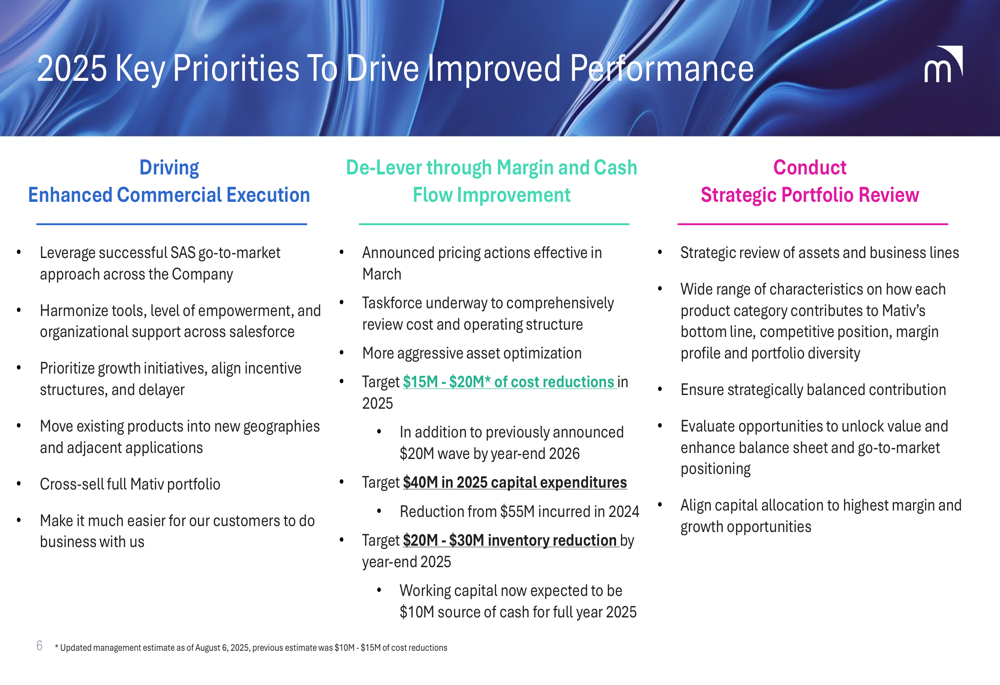

Mativ outlined three key strategic priorities for 2025 aimed at improving performance. These include enhancing commercial execution by leveraging the SAS go-to-market approach, deleveraging through margin and cash flow improvement, and conducting a strategic portfolio review.

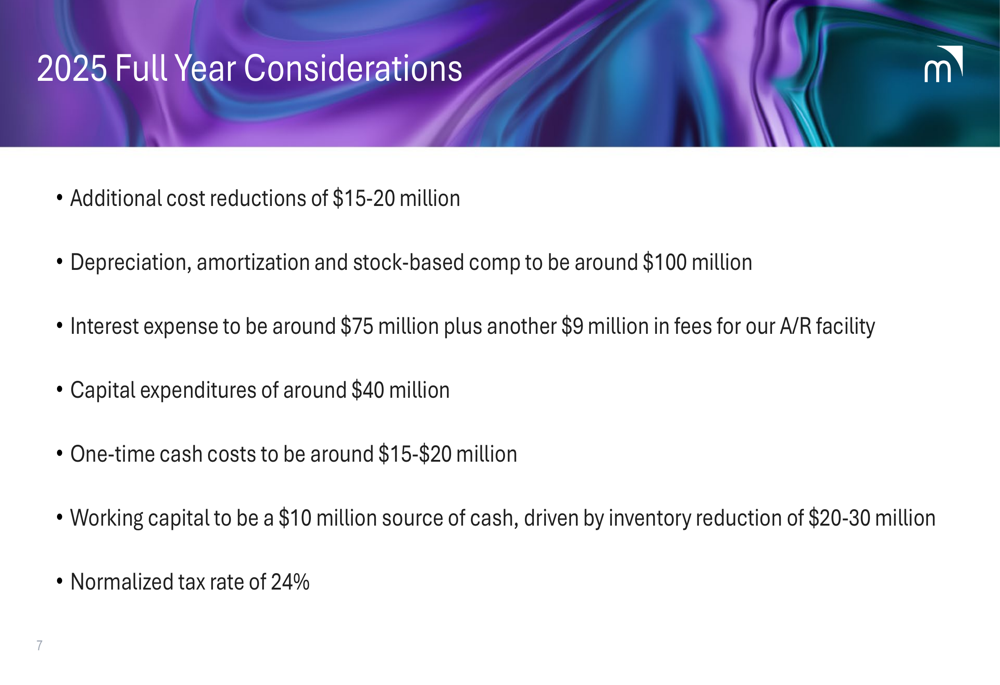

The company is targeting $15-20 million in additional cost reductions, $40 million in capital expenditures, and $20-30 million in inventory reduction to strengthen its financial position. These initiatives are part of a broader effort to optimize assets and improve the balance sheet.

The strategic priorities are detailed in the following slide:

Forward-Looking Statements

Looking ahead, Mativ provided several key considerations for the remainder of 2025. The company expects Q3 adjusted EBITDA to increase 5-10% year-over-year and anticipates favorable Q4 adjusted EBITDA and cash flow levels compared to the prior year.

Management projects depreciation, amortization, and stock-based compensation to be around $100 million for the full year, with interest expense estimated at approximately $75 million plus an additional $9 million in fees for the company’s accounts receivable facility.

The financial outlook includes:

Market Reaction

The market’s strongly positive reaction to Mativ’s Q2 results—with the stock up over 30% following the earnings release—suggests investors are focusing on operational improvements and forward guidance rather than current GAAP losses. This represents a significant shift in sentiment from the previous quarter when the company missed earnings expectations.

The stock movement is particularly noteworthy given that Mativ has been trading at depressed valuations, with previous reports indicating it was valued at just 0.32 times book value. The current rally may reflect growing investor confidence in the company’s cost-cutting initiatives and deleveraging strategy.

With a clear focus on margin improvement, inventory reduction, and strategic portfolio review, Mativ appears to be addressing the concerns that had previously weighed on its stock price. If the company can deliver on its projected Q3 and Q4 improvements, the positive momentum could continue as it works toward its longer-term leverage targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.