Google launches Gemini Enterprise AI platform for workplace automation

Introduction & Market Context

Maytronics (TLV:TASE:MTRN) reported a challenging second quarter for 2025, with significant declines in both revenue and profitability amid intensifying competition and macroeconomic headwinds. The company’s stock fell 11.84% to 470 ILS following the August 20 earnings call, as investors reacted to results that fell short of guidance.

The swimming pool equipment manufacturer faces mounting pressure from Chinese competitors, particularly in the online space, while also contending with US tariffs and logistics challenges in North America. Despite these obstacles, management highlighted progress on cost-cutting initiatives and inventory reduction efforts.

Quarterly Performance Highlights

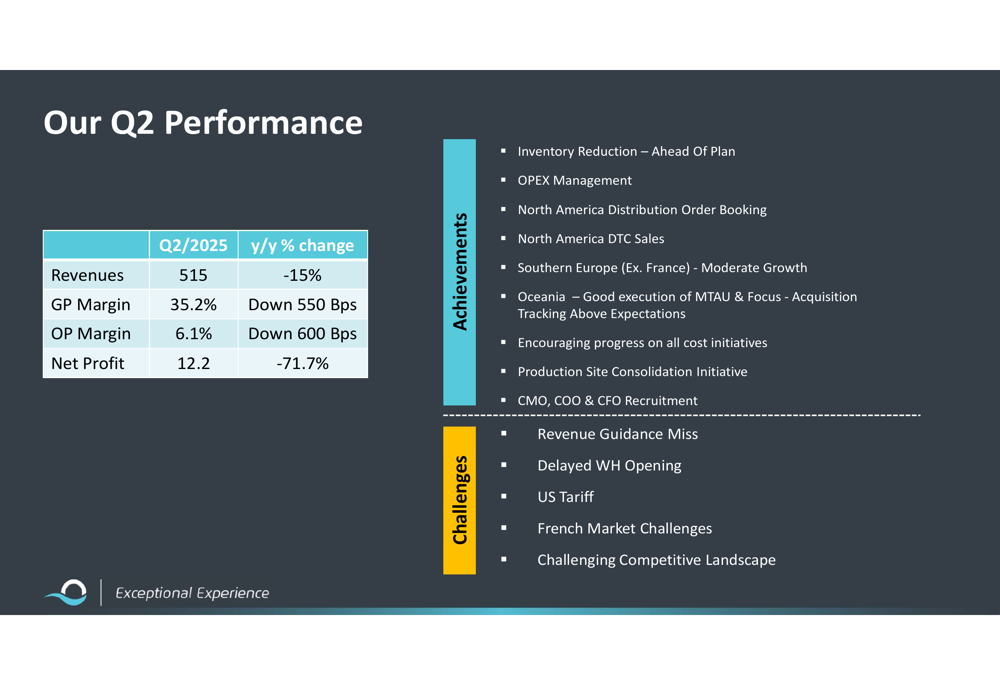

Maytronics reported Q2 2025 revenue of 515 million ILS, representing a 15% year-over-year decline. Profitability metrics deteriorated significantly, with gross profit margin falling 550 basis points to 35.2%, operating profit margin dropping 600 basis points to 6.1%, and net profit plummeting 71.7% to just 12.2 million ILS.

As shown in the following comprehensive performance summary:

The company’s achievements during the quarter included inventory reduction ahead of plan, effective OPEX management, and encouraging progress on cost initiatives. However, these positives were overshadowed by revenue guidance misses, US tariff impacts, and challenges in the French market.

Revenue Analysis by Segment

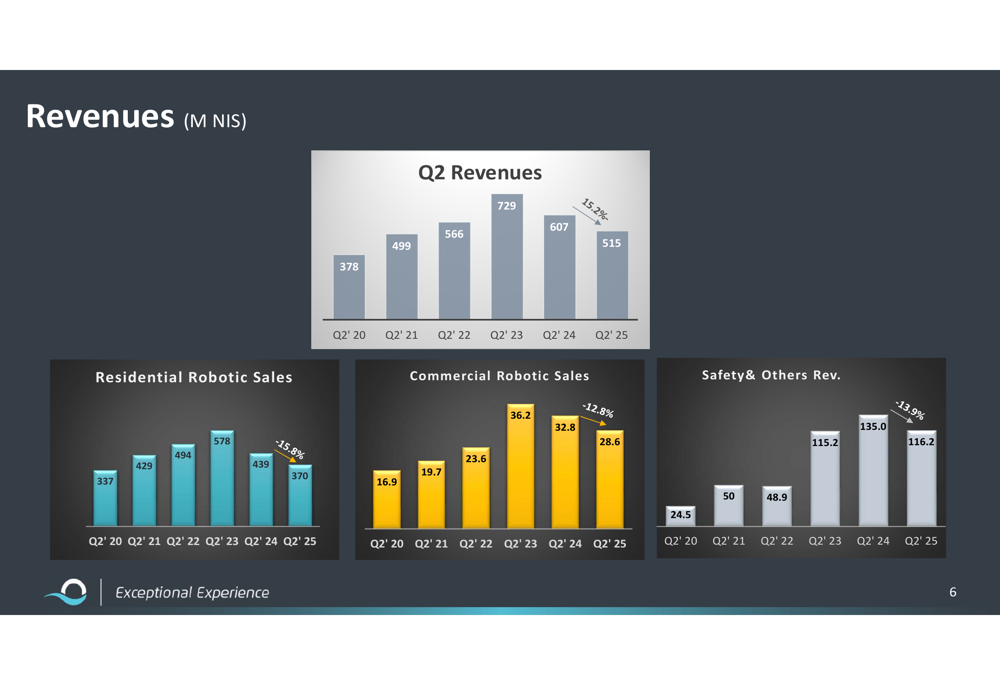

A detailed breakdown of Maytronics’ revenues reveals declines across most product categories. Residential robotic sales, the company’s core business, fell 15.8% to 370 million ILS in Q2 2025. Commercial robotic sales decreased 12.8% to 28.6 million ILS, while Safety & Others revenue dropped 13.9% to 116.2 million ILS.

The following chart illustrates the revenue trends across categories from 2020 through 2025:

Regional Performance Analysis

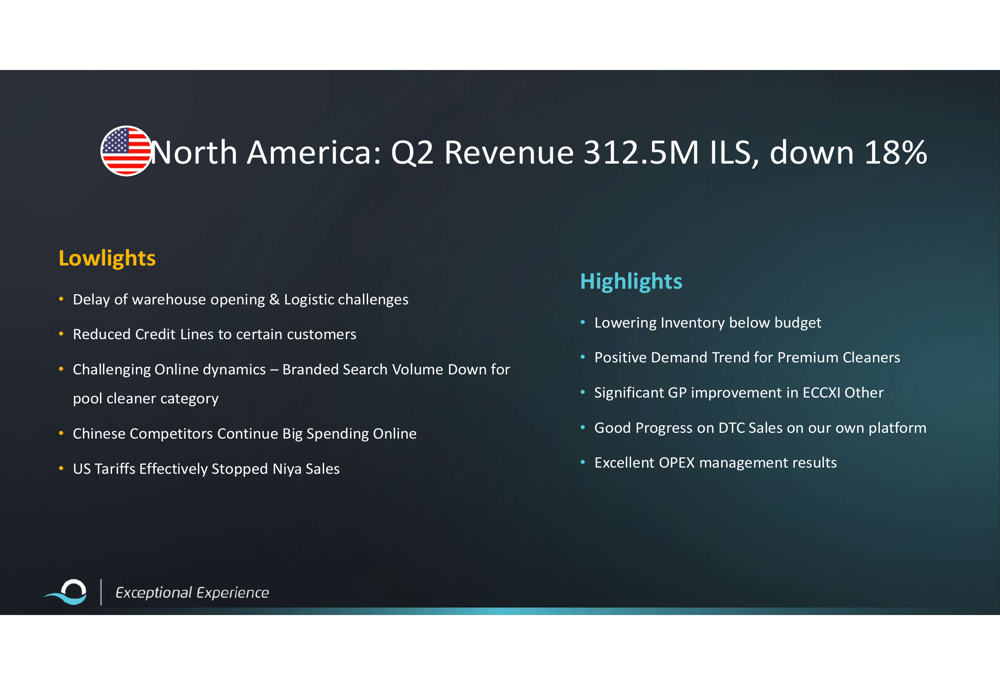

Maytronics experienced varying performance across its key geographic markets. North America, the company’s largest market, saw revenue decline 18% to 312.5 million ILS. The region faced multiple challenges including warehouse opening delays, logistical issues, reduced credit lines to certain customers, and US tariffs that effectively halted Niya sales.

The following breakdown highlights both challenges and bright spots in the North American market:

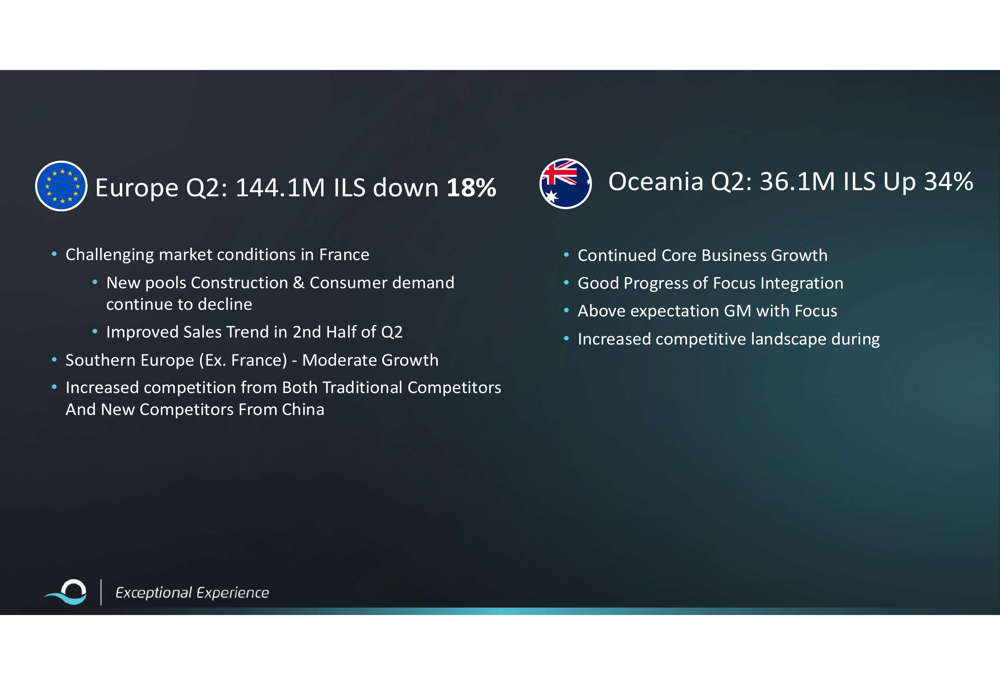

Europe also struggled with an 18% revenue decline to 144.1 million ILS, primarily due to challenging conditions in France where new pool construction and consumer demand continued to fall. Southern Europe (excluding France) managed to achieve moderate growth despite the overall regional decline.

In contrast, Oceania emerged as a bright spot with revenue increasing 34% to 36.1 million ILS, driven by core business growth and successful integration of the Focus acquisition. The following slide details the performance across Europe and Oceania:

Margin Compression and Cost Management

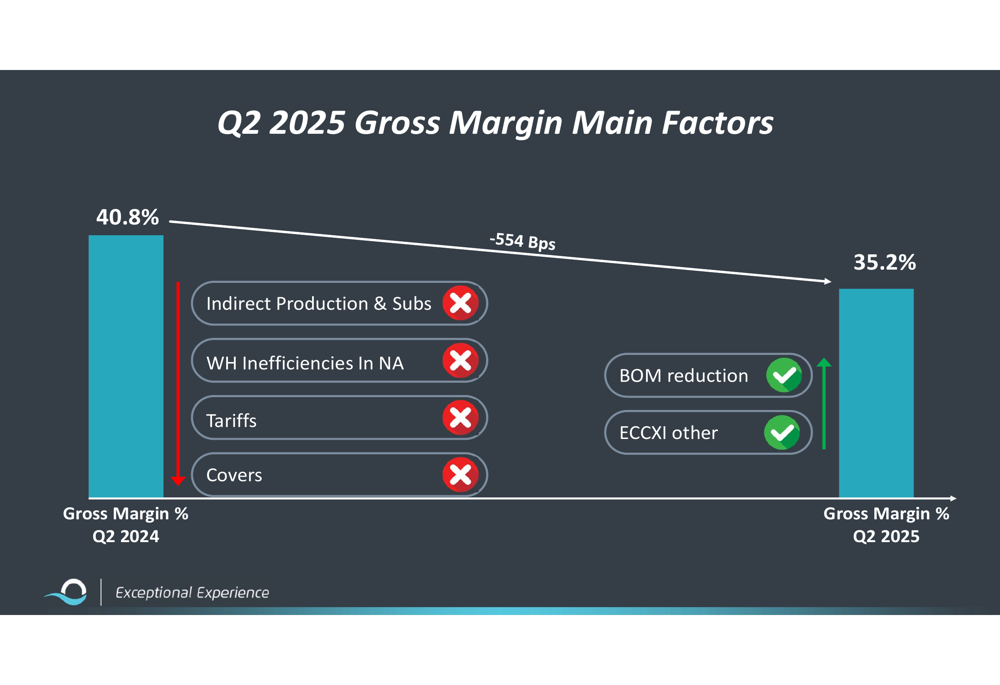

Gross margin deteriorated significantly to 35.2% in Q2 2025, down from 40.8% in Q2 2024. This 554 basis point decline was primarily attributed to indirect production costs, warehouse inefficiencies in North America, tariffs, and covers-related expenses. These negative factors were partially offset by BOM (bill of materials) reduction and improvements in ECCXI other.

The following chart details the key factors impacting gross margin:

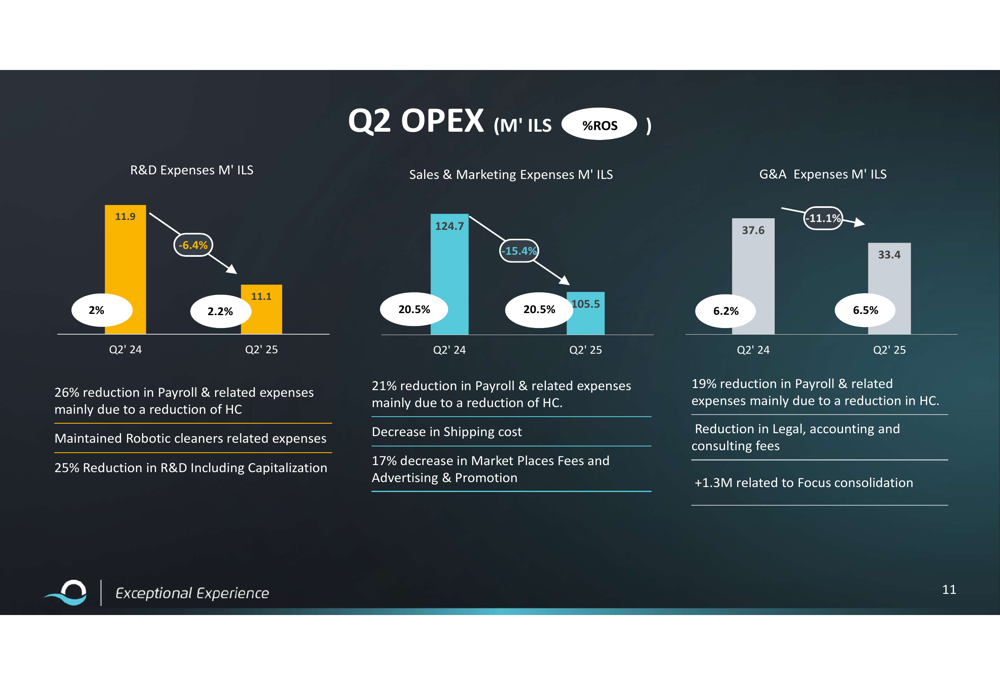

To address profitability challenges, Maytronics has implemented comprehensive cost-cutting measures across the organization. The company’s OPEX analysis reveals reductions in all major expense categories, with particular emphasis on payroll and related expenses through headcount reduction.

The OPEX breakdown shows:

The company’s organizational alignment initiative is expected to deliver approximately 40 million ILS in full-year impact for 2025, compared to 13.2 million ILS in 2024. These savings are primarily coming from wages, rent, and other operating expenses.

Outlook and Forward Guidance

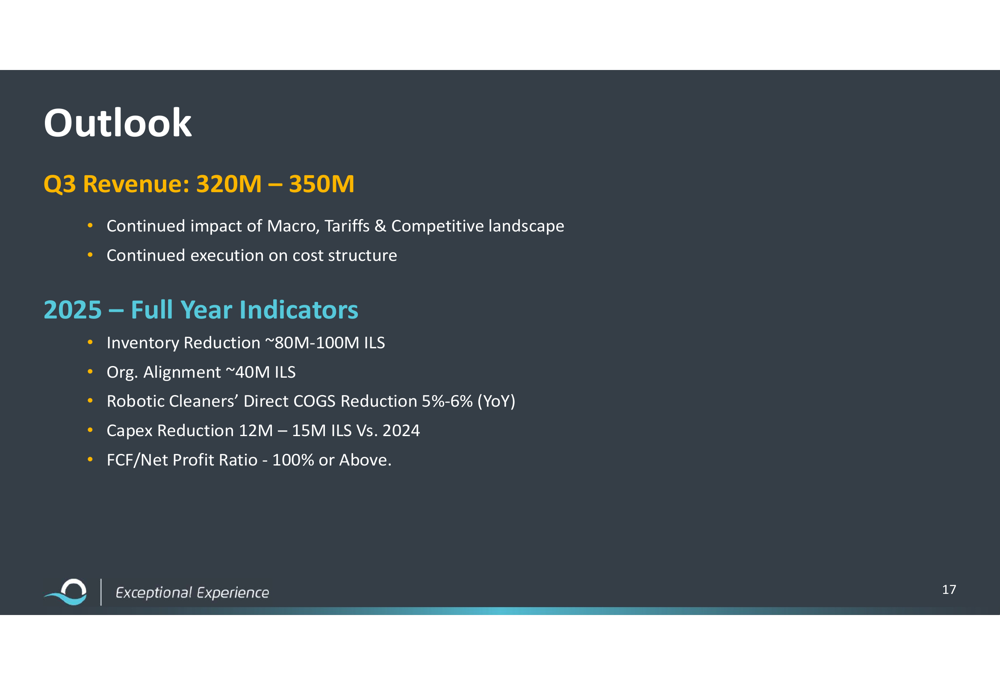

Looking ahead, Maytronics provided Q3 2025 revenue guidance of 320-350 million ILS, acknowledging continued impacts from macroeconomic conditions, tariffs, and the competitive landscape. For the full year 2025, the company outlined several key indicators including:

- Inventory reduction of approximately 80-100 million ILS

- Organizational alignment savings of approximately 40 million ILS

- Robotic cleaners’ direct COGS reduction of 5-6% year-over-year

- Capex reduction of 12-15 million ILS versus 2024

- Free cash flow to net profit ratio of 100% or above

The following slide details the company’s outlook:

Strategic Initiatives

Despite current challenges, Maytronics is making progress on several strategic fronts. The company has successfully recruited key executives including a CMO, COO, and CFO. In North America, the company is seeing positive demand trends for premium cleaners and making good progress on direct-to-consumer sales through its own platform.

The Oceania region continues to be a success story, with the Focus acquisition tracking above expectations and showing above-expected gross margins. The company also highlighted its production site consolidation initiative as part of broader cost-saving efforts.

Inventory management remains a priority, with the company reducing inventory levels from over 1 million ILS in December 2022 to approximately 708 million ILS by June 2025. This reduction is ahead of plan and contributes positively to cash flow.

As the swimming pool equipment market continues to evolve amid increased competition and changing consumer behavior, Maytronics’ ability to execute on its cost initiatives while maintaining market share will be crucial for its recovery in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.