Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

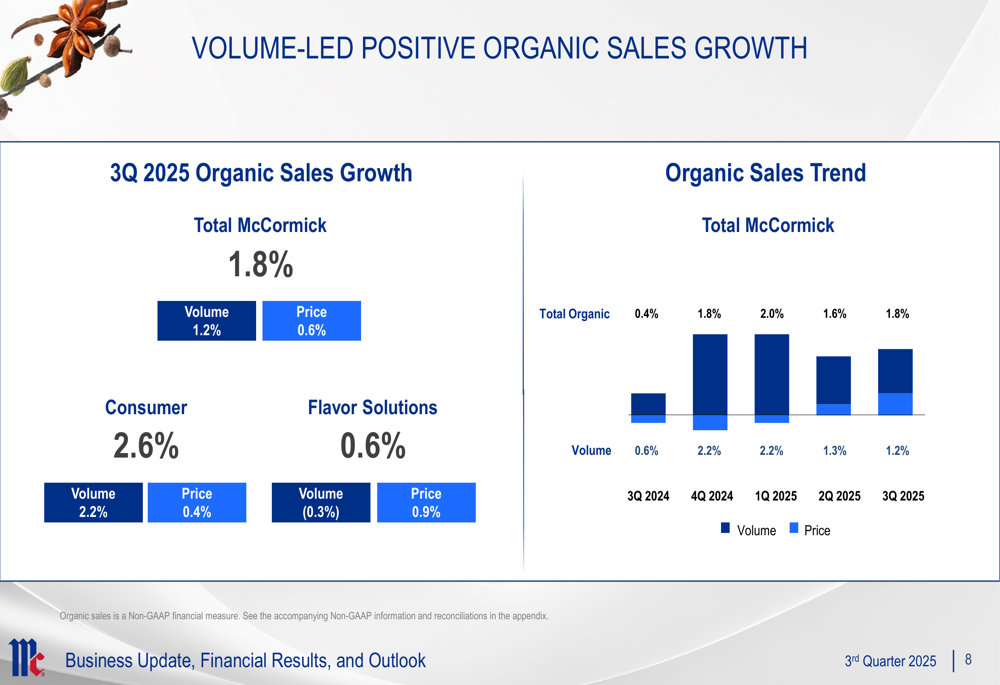

McCormick & Company (NYSE:MKC) presented its third-quarter 2025 results on October 7, highlighting volume-led growth despite ongoing challenges from tariffs and commodity costs. The spice and flavoring manufacturer reported modest organic sales growth of 1.8%, driven primarily by volume increases rather than pricing actions.

The company’s stock traded down 1.14% in premarket at $67.51, suggesting investors may have expected stronger results or were concerned about the maintained cautious outlook for the full year.

Quarterly Performance Highlights

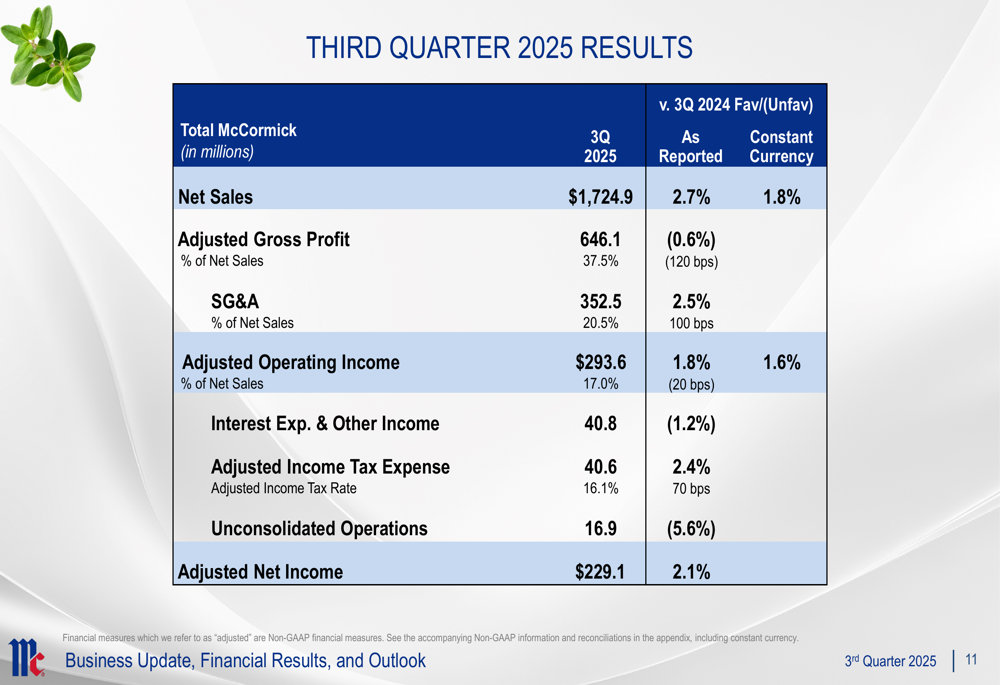

McCormick reported net sales of $1,724.9 million for Q3 2025, representing 2.7% growth on a reported basis and 1.8% in constant currency. The company achieved adjusted earnings per share of $0.85, a modest improvement from $0.83 in the same period last year.

As shown in the following financial results summary:

The company’s adjusted operating income reached $293.6 million, up 1.8% from the prior year. This growth came despite pressure on gross margins, which declined slightly year-over-year as the company absorbed higher commodity costs and tariff impacts.

Cash flow from operations reached $420 million year-to-date, with the company returning $362 million to shareholders through dividends while investing $138 million in capital expenditures.

Segment and Regional Analysis

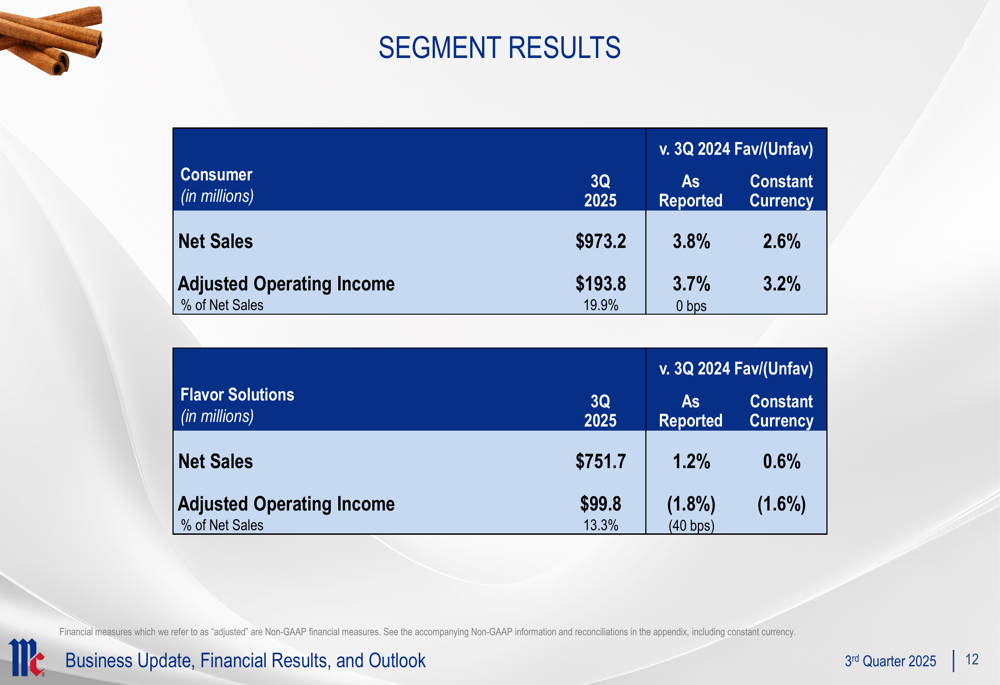

McCormick’s performance showed significant variation across segments and regions. The Consumer segment outperformed Flavor Solutions, with organic sales growth of 2.6% compared to just 0.6% for Flavor Solutions.

The volume-led growth is clearly illustrated in this breakdown:

Within the Consumer segment, EMEA led the way with impressive 4.4% organic growth, while Americas delivered 2.7% growth. The APAC region was the only consumer market to decline, falling 0.8% primarily due to softness in China’s foodservice business.

The following regional breakdown provides more detail on Consumer segment performance:

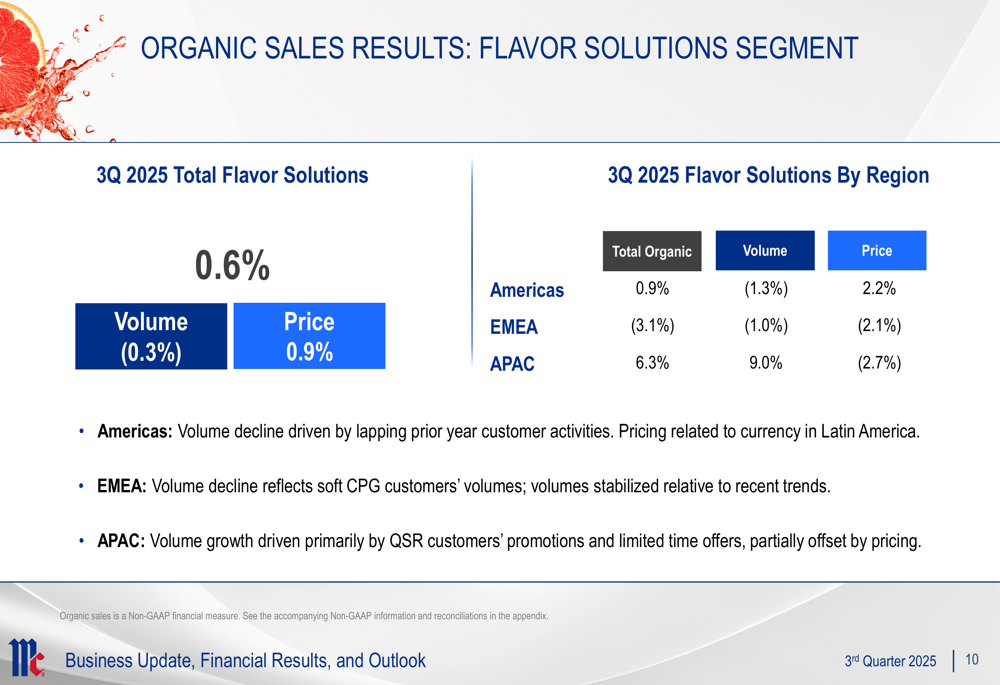

The Flavor Solutions segment faced greater challenges, particularly in EMEA where organic sales declined 3.1%, reflecting soft volumes from CPG customers. The APAC region was the bright spot, growing 6.3% on strong QSR customer promotions and limited-time offers.

The segment results further highlight the divergence in performance:

Tariff Impact and Mitigation Strategies

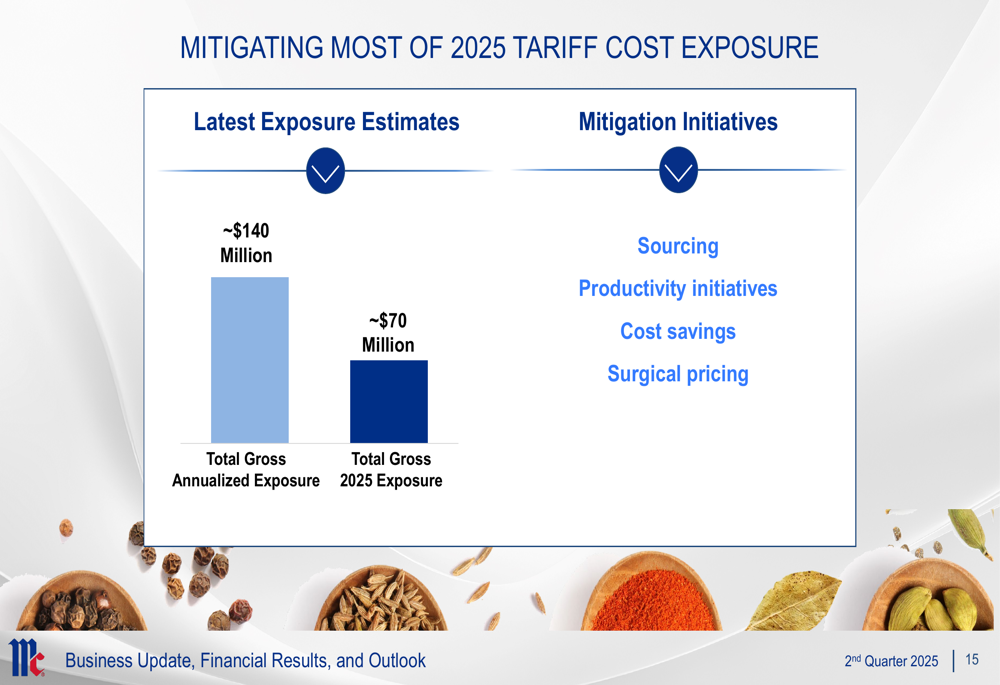

A significant focus of the presentation was McCormick’s approach to managing tariff impacts. The company faces approximately $140 million in annualized tariff exposure, with about $70 million impacting 2025 results.

Management outlined a comprehensive strategy to mitigate these costs:

These mitigation efforts are critical as the company works to protect margins while maintaining volume growth. During the previous quarter’s earnings call, CEO Brendan Foley had emphasized the company’s focus on flavor enhancement rather than competing for calories, a strategy that appears to be supporting volume growth despite economic pressures.

2025 Outlook and Strategic Initiatives

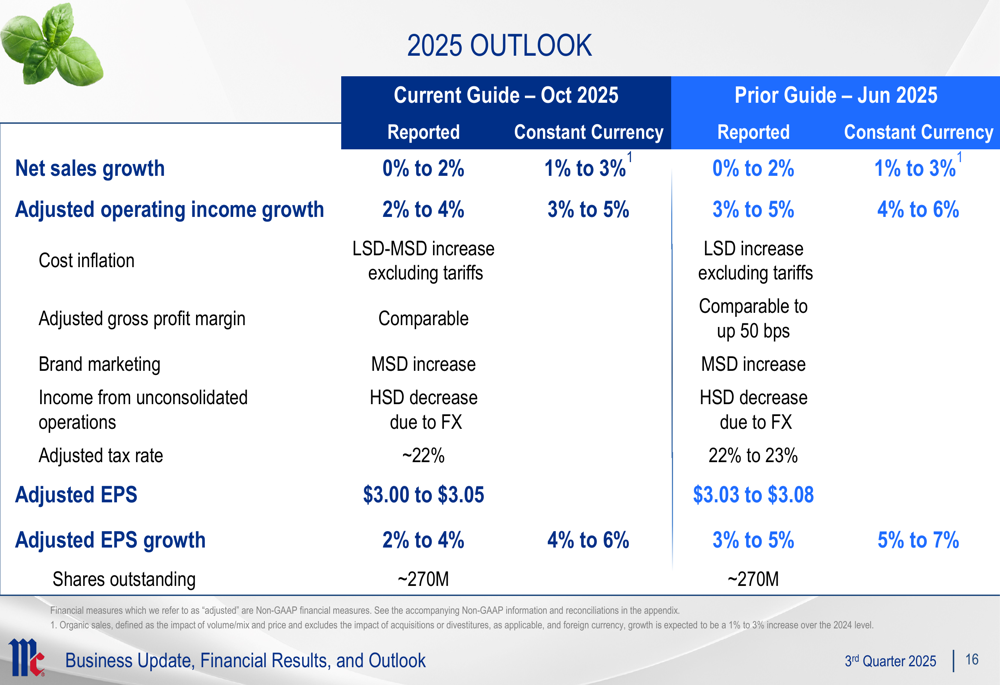

McCormick maintained its cautious outlook for 2025, projecting net sales growth of 0-2% and adjusted operating income growth of 2-4%. This represents a slight tightening from the 1-3% sales growth guidance mentioned in the Q2 earnings report.

The outlook reflects both ongoing challenges and the company’s confidence in its growth strategies:

The company continues to execute on multiple growth initiatives across category management, brand marketing, innovation, and proprietary technologies:

These strategic initiatives appear to be yielding results in key areas, with the presentation highlighting strong volume growth in Spices and Seasonings across all regions, continued share gains in Mustard, and solid Hot Sauce performance.

However, challenges remain, including pressure on Americas’ Recipe Mixes, softness in China Foodservice, and weakness in CPG customer volumes in Americas and EMEA.

As McCormick navigates these mixed market conditions, its focus on volume-led growth while implementing tariff mitigation strategies will be crucial to meeting its full-year targets and positioning for longer-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.