Gold prices slip lower; easing U.S.-China tensions curb haven demand

Introduction & Market Context

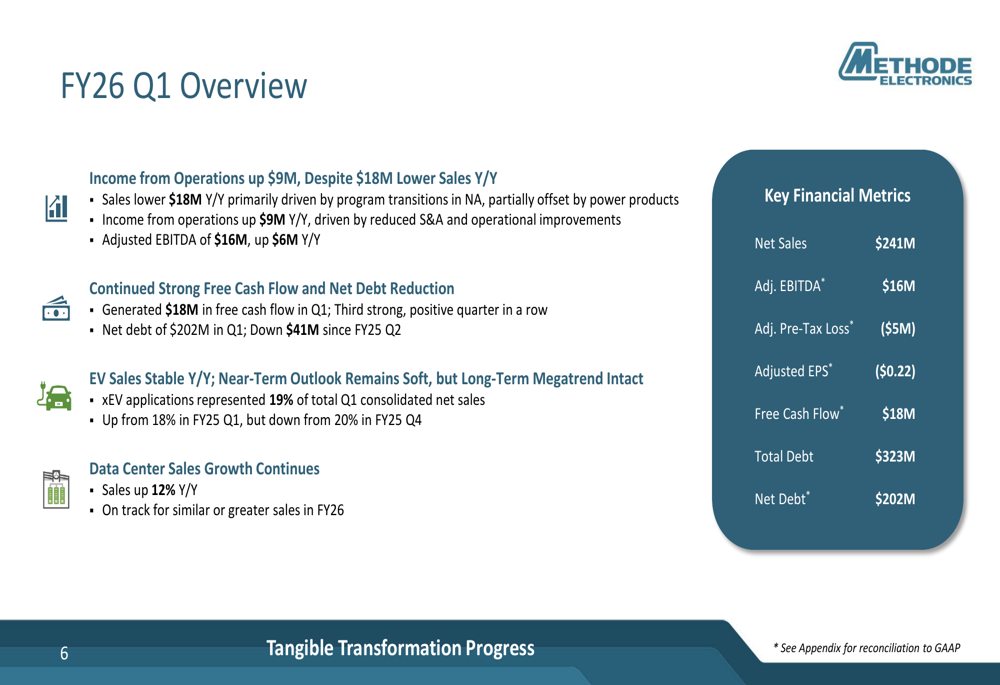

Methode Electronics Inc (NYSE:MEI) presented its first quarter fiscal 2026 earnings results on September 10, 2025, highlighting operational improvements that drove EBITDA growth despite lower sales. The company’s stock, which has traded between $5.08 and $17.45 over the past 52 weeks, closed at $7.40 prior to the presentation, up 2.07% for the day.

The presentation comes as Methode continues its corporate transformation efforts amid challenging market conditions, particularly in its traditional automotive segments. The company is strategically pivoting toward higher-growth areas like data centers and military/aerospace applications while implementing significant cost-cutting measures.

Quarterly Performance Highlights

Methode reported Q1 FY26 net sales of $240.5 million, down 7% year-over-year from $258.5 million in Q1 FY25. Despite this revenue decline, the company achieved notable improvements in profitability metrics, with adjusted EBITDA increasing to $15.7 million from $9.8 million in the same period last year.

As shown in the following comprehensive quarterly overview:

The company’s adjusted EBITDA margin expanded to 6.5% from 3.8% year-over-year, demonstrating the effectiveness of cost reduction initiatives. While still reporting an adjusted pre-tax loss of $5.1 million, this represents an improvement from the $9.1 million loss in Q1 FY25. Similarly, adjusted earnings per share improved to a loss of $0.22 from a loss of $0.31 in the prior-year quarter.

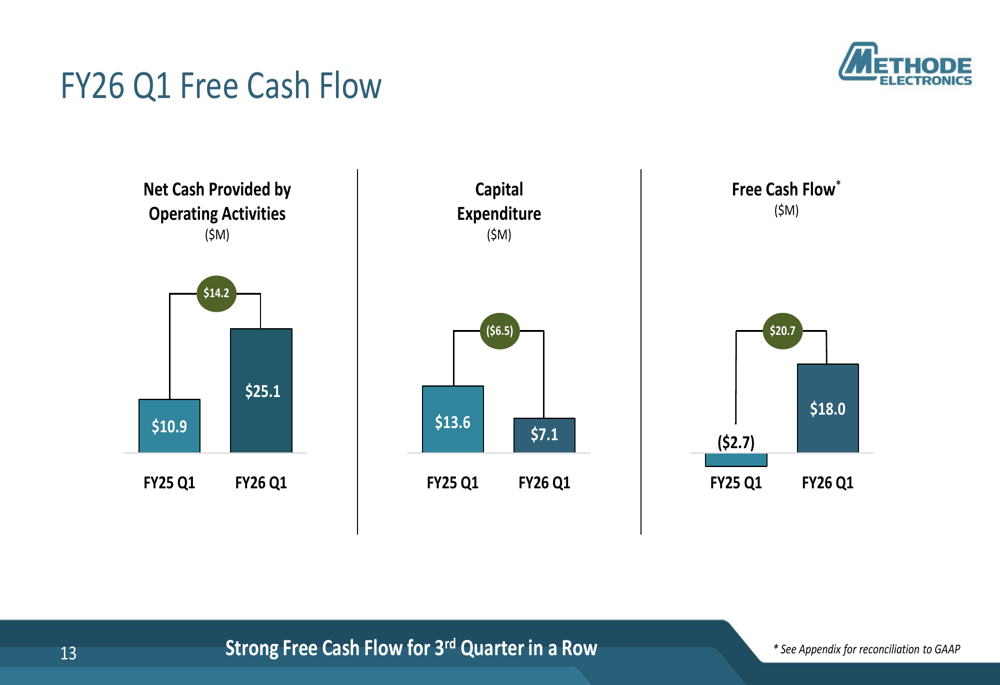

One of the most significant achievements was Methode’s free cash flow generation of $18 million, marking the third consecutive quarter of strong cash flow performance. This represents a substantial improvement from the negative $2.7 million reported in Q1 FY25.

Detailed Financial Analysis

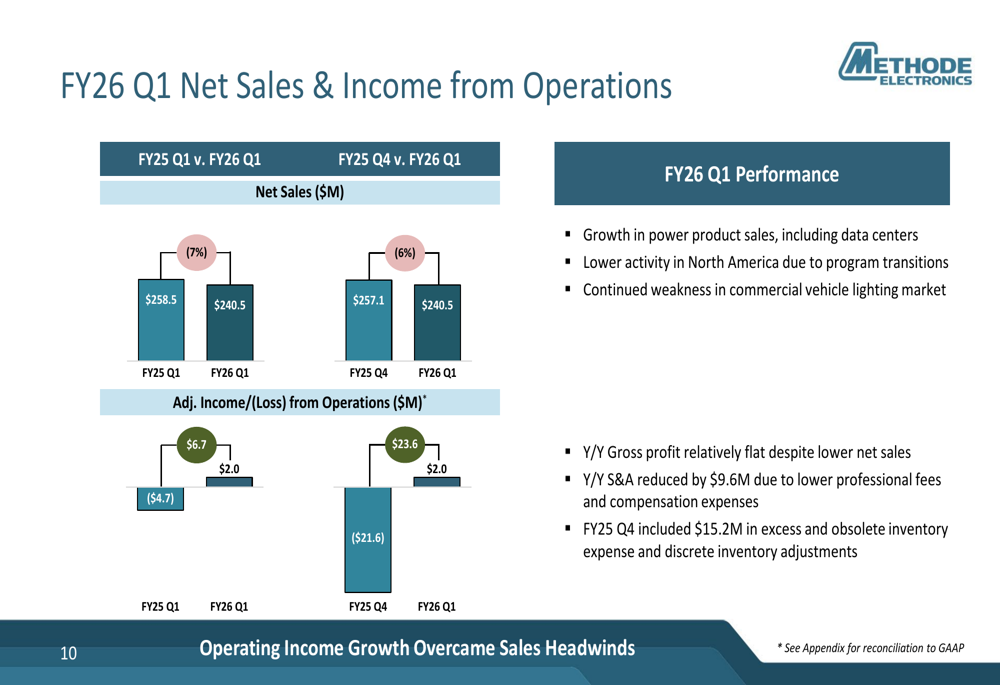

The company’s sales decline was primarily attributed to program transitions in North America, partially offset by growth in power products. Despite lower revenues, Methode maintained relatively flat gross profit year-over-year through operational improvements.

A key driver of improved profitability was the $9.6 million reduction in selling and administrative expenses, achieved through lower professional fees and compensation expenses. This cost discipline helped offset the impact of lower sales volumes.

The following chart illustrates the company’s net sales and income from operations performance:

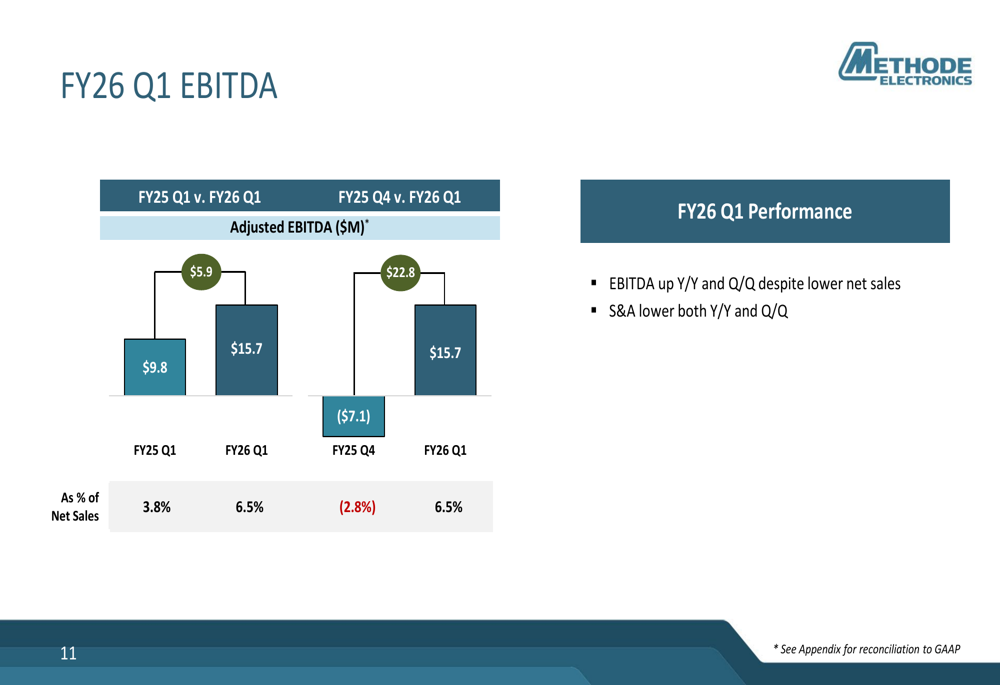

Methode’s EBITDA performance was particularly noteworthy, showing improvement both year-over-year and sequentially despite the sales decline:

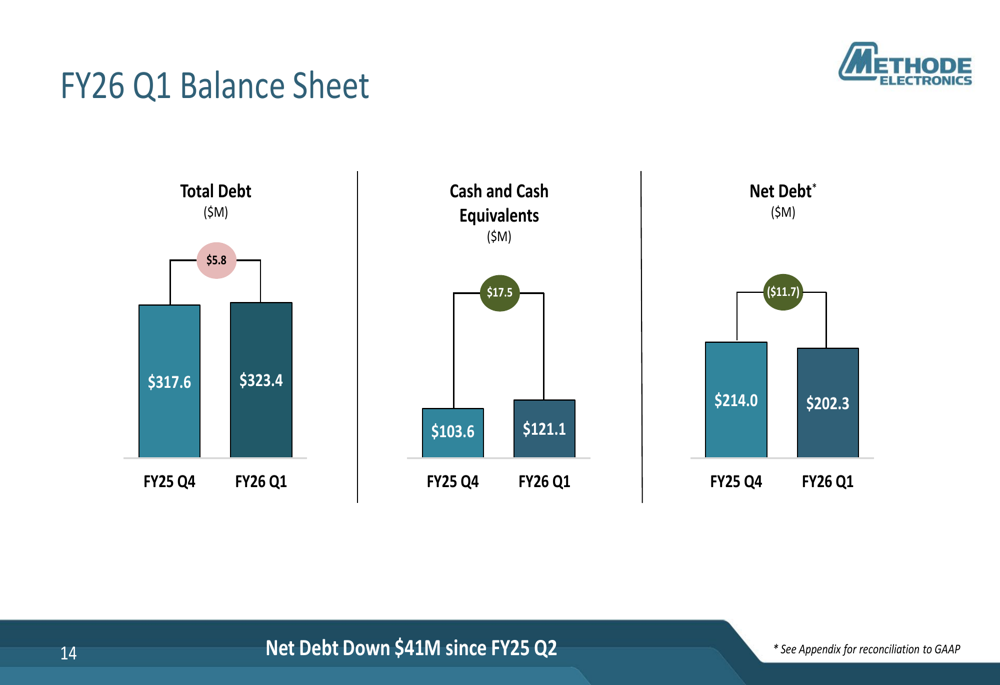

On the balance sheet front, Methode continued to strengthen its financial position by reducing net debt to $202.3 million, down $41 million since Q2 FY25. The company maintained a healthy cash position of $121.1 million as of the end of Q1 FY26.

Strategic Initiatives

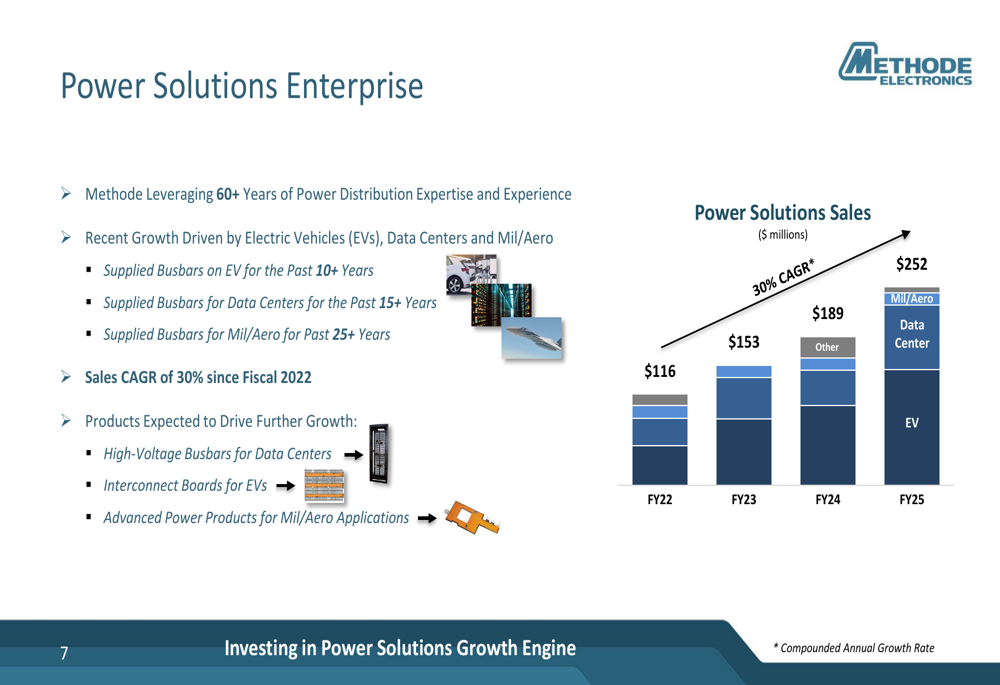

A bright spot in Methode’s portfolio is its Power Solutions Enterprise, which has achieved a 30% compound annual growth rate since fiscal 2022. This segment leverages the company’s 60+ years of power distribution expertise and has seen recent growth driven by electric vehicles, data centers, and military/aerospace applications.

The following chart demonstrates the impressive growth trajectory of the Power Solutions segment:

Data center sales grew 12% year-over-year, continuing a positive trend for the company. Meanwhile, electric vehicle sales remained stable, representing 19% of total Q1 sales. This diversification helps offset weakness in traditional automotive segments.

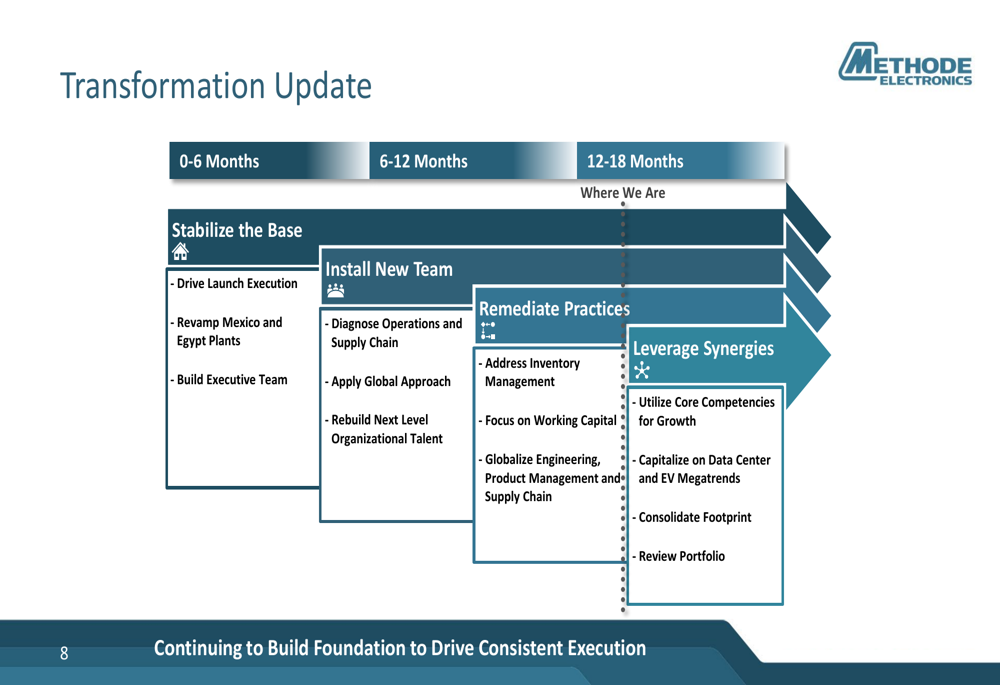

Methode’s transformation process is progressing according to plan, with the company currently in the second phase of its three-phase approach. The transformation roadmap includes stabilizing the base business, installing a new team, and leveraging synergies:

Forward-Looking Statements

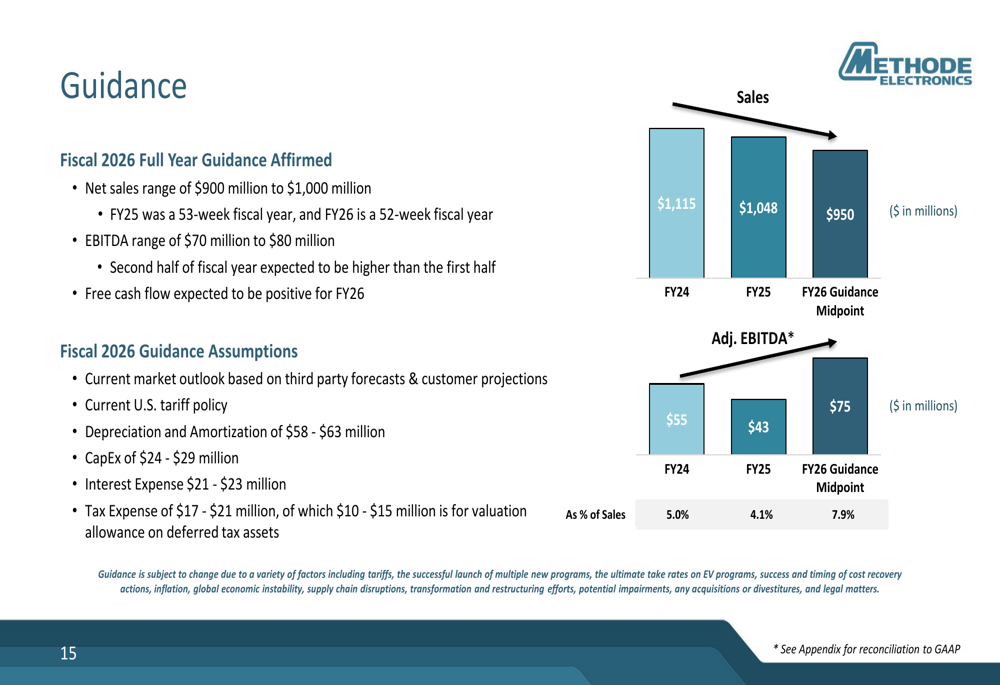

Methode affirmed its fiscal 2026 full-year guidance, projecting net sales between $900 million and $1 billion, and EBITDA between $70 million and $80 million. The company expects the second half of the fiscal year to be stronger than the first half, with free cash flow remaining positive throughout FY26.

The guidance reflects a projected EBITDA margin improvement to 7.9% at the midpoint, up from 4.1% in FY25, despite anticipated lower sales. This outlook incorporates current market conditions, including U.S. tariff policies and customer projections.

Management’s guidance assumptions include depreciation and amortization of $58-$63 million, capital expenditures of $24-$29 million, interest expense of $21-$23 million, and tax expense of $17-$21 million (including $10-$15 million for valuation allowance on deferred tax assets).

These projections align with statements made during the company’s previous earnings call, where CEO John DeGaynor noted that fiscal 2026 would be a "reset year" due to EV program delays. The current presentation confirms the company’s strategy of improving operational efficiency to offset revenue challenges while positioning for future growth in emerging segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.