TSX lower as gold rally takes a breather

Introduction & Market Context

Metso (OTC:MXTOF) Oyj (HEL:METSO) shares rose 2.06% to €9.01 following the release of its first quarter 2025 results on April 24, 2025. The Finnish mining and aggregates equipment manufacturer demonstrated resilience in a challenging market environment, maintaining solid profitability despite a slight decline in sales compared to the same period last year.

President and CEO Sami Takaluoma presented results that showed equipment orders growing in both the company’s key segments, while the adjusted EBITA margin remained robust at 16.5%. The company’s performance comes amid increasing concerns about the potential impact of tariffs, particularly in the US market, which accounts for approximately 15% of Metso’s sales.

Quarterly Performance Highlights

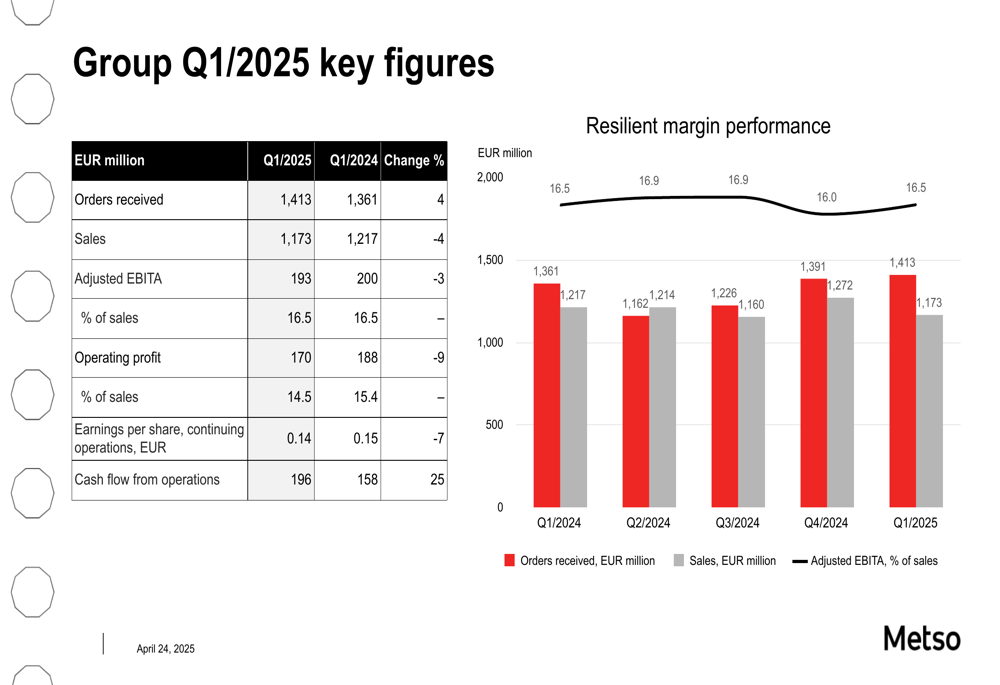

Metso reported orders received of €1,413 million in Q1 2025, representing a 4% increase year-over-year, while sales declined 4% to €1,173 million. Despite the sales decrease, the company maintained a solid adjusted EBITA of €193 million, only 3% lower than the previous year, resulting in a 16.5% margin. Operating profit fell 9% to €170 million, with earnings per share declining 7% to €0.14.

As shown in the following chart of key financial figures and margin performance:

A particularly bright spot was the company’s cash flow from operations, which increased 25% to €196 million, demonstrating Metso’s ability to generate strong cash even in a challenging environment.

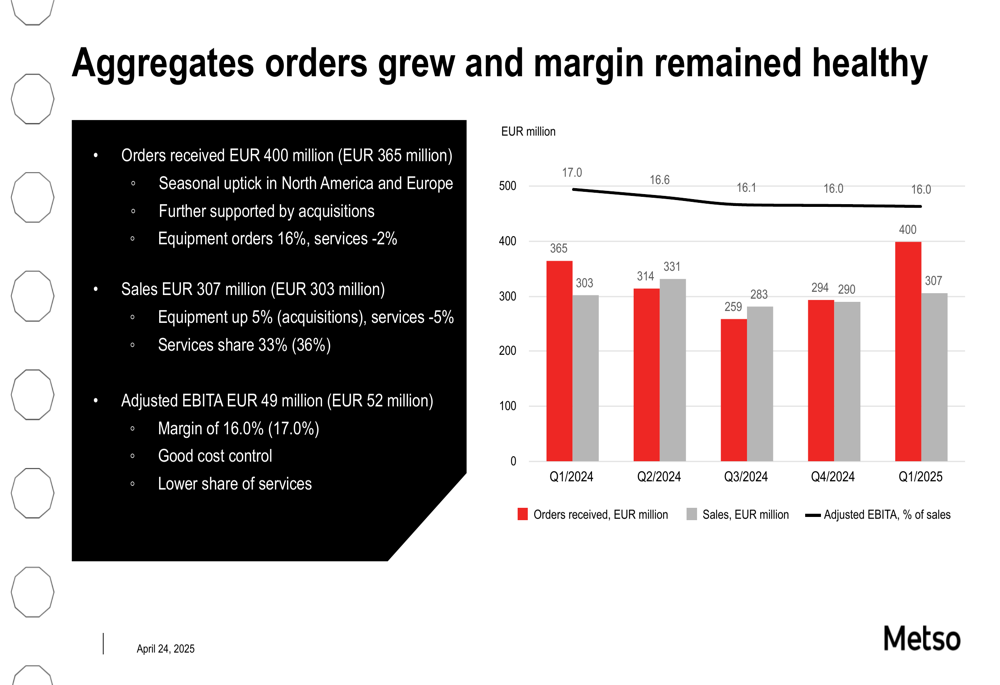

The Aggregates segment showed positive momentum with orders received of €400 million, up from €365 million in Q1 2024. Sales increased slightly to €307 million, though adjusted EBITA declined to €49 million from €52 million. The company noted a seasonal uptick in North America and Europe, with further support from acquisitions.

The following chart illustrates the Aggregates segment performance:

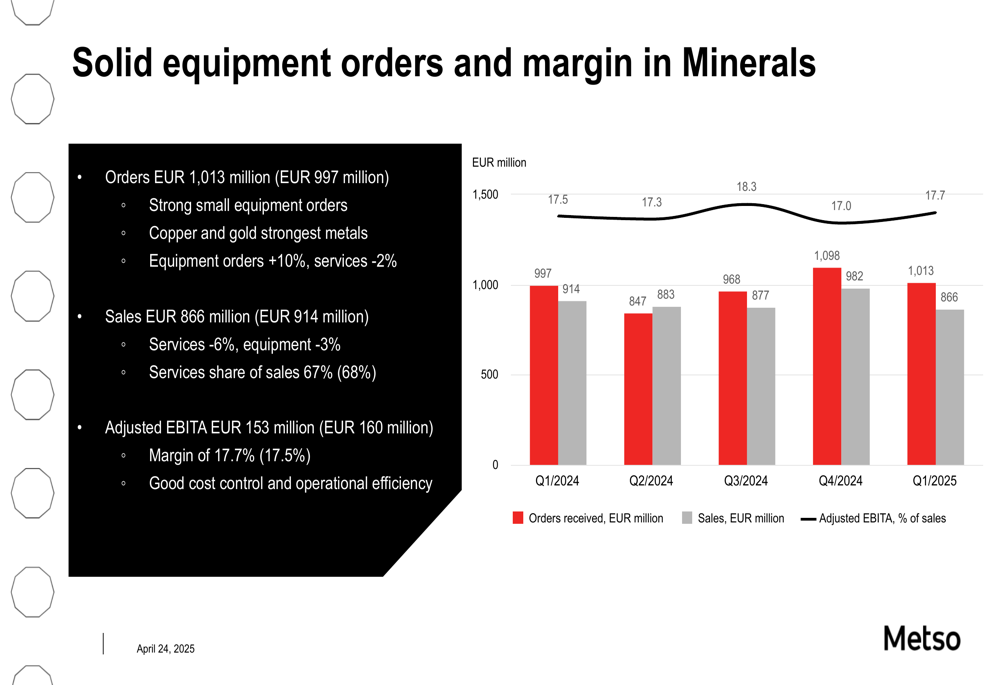

In the Minerals segment, which represents the larger portion of Metso’s business, orders received grew to €1,013 million from €997 million in the prior year. Sales declined to €866 million from €914 million, with adjusted EBITA falling to €153 million from €160 million. The company highlighted strong small equipment orders, with copper and gold being the strongest metals. Equipment orders increased 10%, while services orders decreased 2%.

The Minerals segment performance is illustrated in this chart:

Detailed Financial Analysis

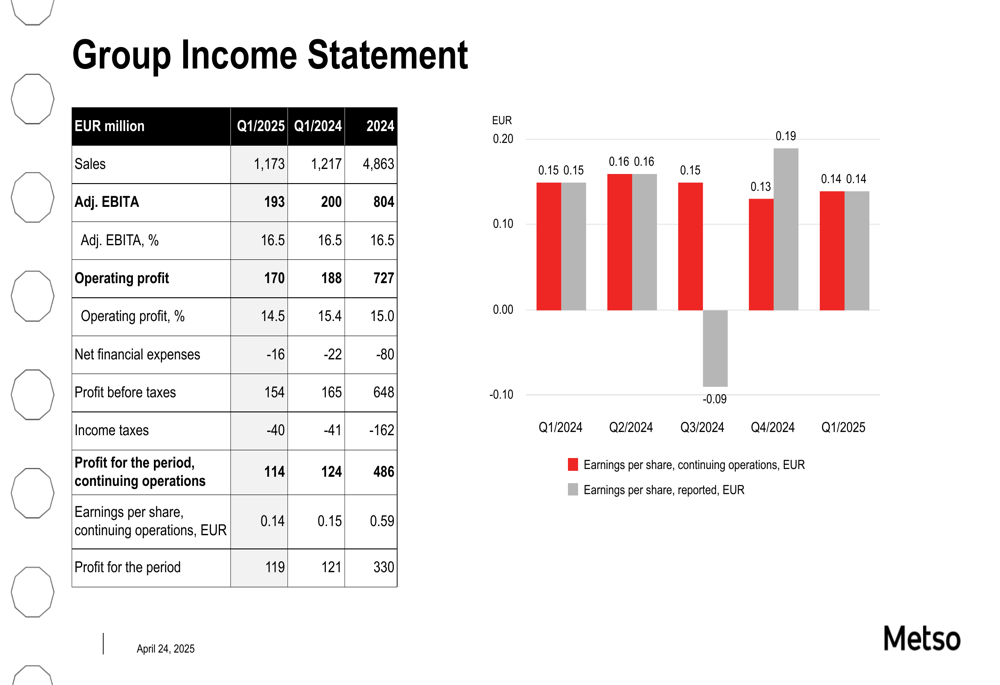

Metso’s income statement reflected the challenging market conditions, with a 4% decline in sales to €1,173 million. Despite this, the company maintained a solid adjusted EBITA margin of 16.5%, demonstrating effective cost management. Operating profit was €170 million, representing 14.5% of sales, while profit before taxes came in at €154 million.

The following income statement details provide a comprehensive view of Metso’s Q1 2025 performance:

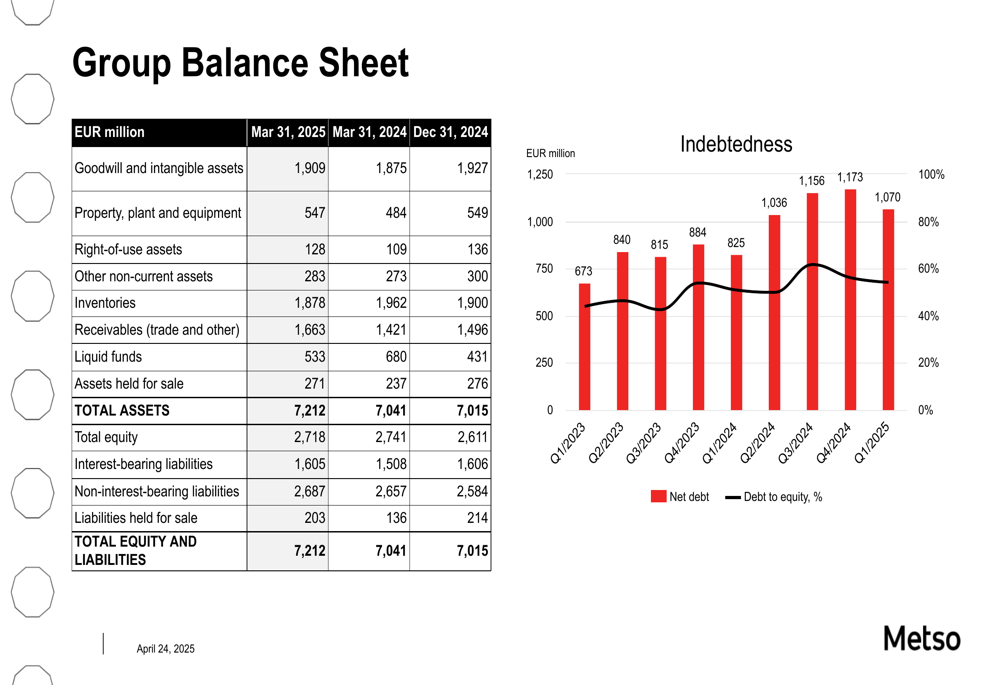

The balance sheet remained strong, with total assets of €7,212 million. Inventories stood at €1,878 million, while liquid funds were €533 million. Total (EPA:TTEF) equity was €2,718 million, resulting in an equity-to-assets ratio of 43.0%.

The balance sheet strength is illustrated in this chart:

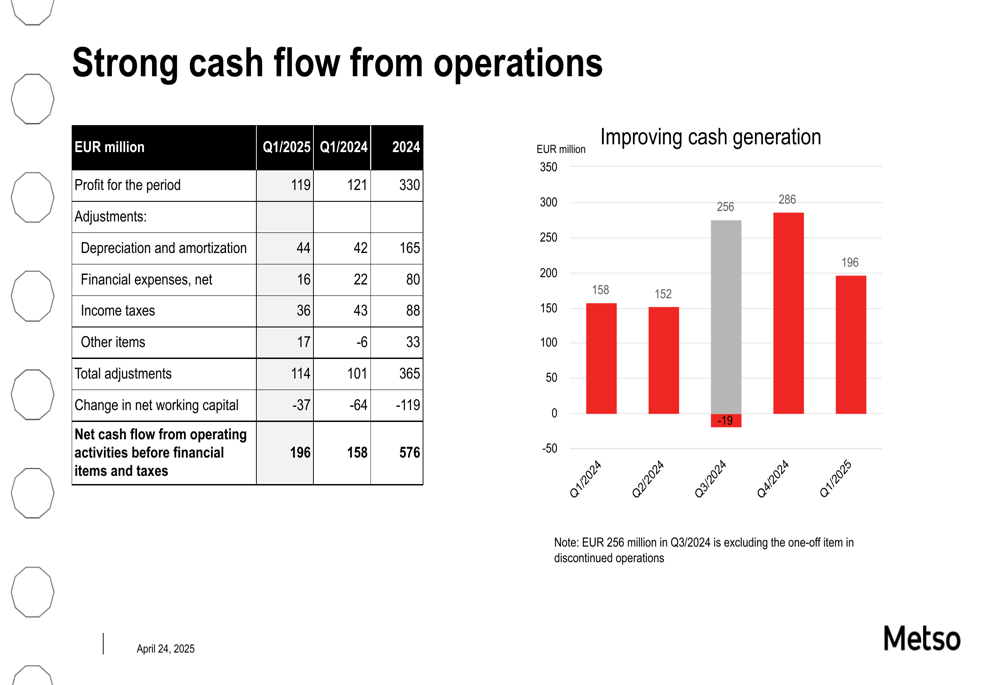

Cash flow performance was particularly impressive, with net cash flow from operating activities before financial items and taxes reaching €196 million, a 25% increase from the previous year. This strong cash generation provides Metso with financial flexibility to navigate market uncertainties.

The following chart demonstrates Metso’s strong cash flow performance:

The company maintained its investment-grade credit ratings, with S&P Global rating Metso ’BBB’ with a stable outlook and Moody’s assigning a ’Baa2’ long-term rating with a stable outlook. Net debt stood at €1,070 million, resulting in a gearing ratio of 39.4% and a debt-to-capital ratio of 35.1%.

Strategic Initiatives

Metso’s management outlined several key priorities for the near term, including maximizing the potential of the current market, continuing to normalize inventory levels, ensuring successful ERP implementation, finalizing the strategy process, and developing the company culture.

A significant focus area is mitigating the potential impact of tariffs, particularly in the US market. Metso noted that its local US manufacturing is limited to three brands selling mobile aggregates equipment and a few smaller product lines. The company is working to mitigate tariff impacts through customer price adjustments and supply chain optimization, while leveraging its extensive geographical footprint to support deliveries from multiple countries.

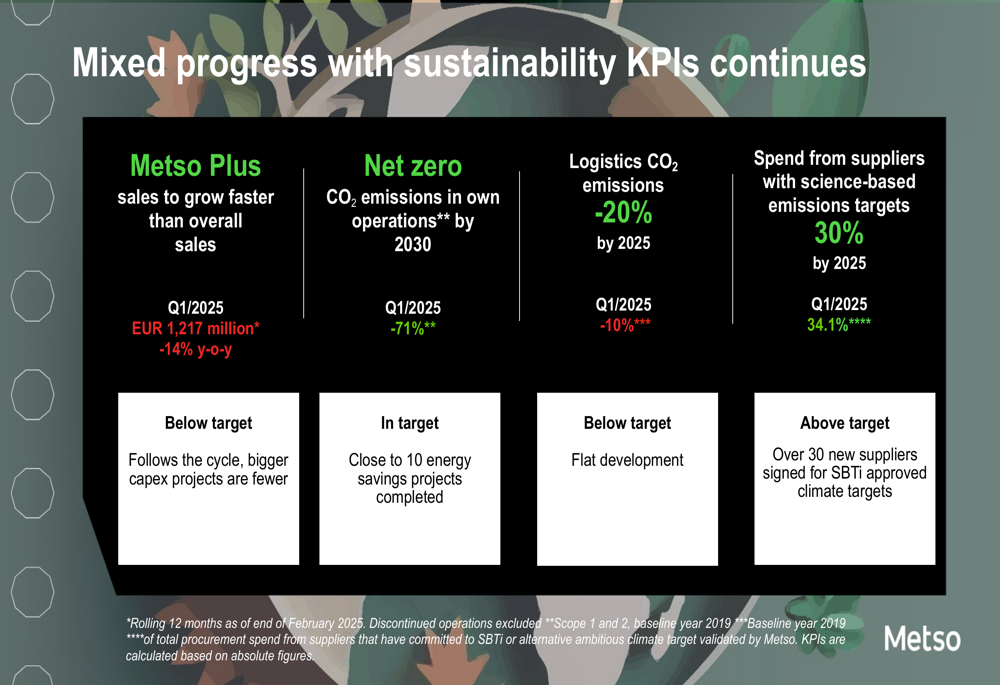

Sustainability remains a priority, though progress has been mixed across key performance indicators. Metso Plus sales, which represent the company’s more sustainable product offerings, reached €1,217 million in Q1 2025, a 14% year-over-year decline. However, the company has made significant progress in reducing CO2 emissions in its own operations (down 71%) and is ahead of target in spending from suppliers with science-based emissions targets (34.1% versus a 30% goal).

The following chart illustrates Metso’s progress on sustainability goals:

Forward-Looking Statements

Looking ahead, Metso expects market activity in both the Minerals and Aggregates segments to remain at current levels. However, the company cautioned that tariff-related turbulence could potentially affect global economic growth and market activity.

The management team emphasized their focus on maximizing opportunities in the current market environment while continuing to normalize inventory levels. The company’s strong cash flow generation and solid balance sheet position it well to navigate potential market challenges, though the uncertain global trade environment remains a concern.

Metso’s resilient margin performance despite the sales decline demonstrates the company’s operational efficiency and ability to adapt to changing market conditions. With equipment orders growing in both segments and a strong financial position, Metso appears well-positioned to maintain its competitive standing in the mining and aggregates equipment market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.