Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Micron Technology (NASDAQ:MU) reported record financial results for its fiscal third quarter 2025 on June 25, showcasing the company’s continued momentum in the memory and storage market. The semiconductor manufacturer delivered $9.3 billion in revenue, significantly exceeding the $8.8 billion guidance provided in its previous earnings report, demonstrating strong execution amid growing demand for AI-related memory products.

Following the earnings release, Micron’s stock fell 1.28% in aftermarket trading to $126.27, after closing regular trading at $127.91. Despite this short-term reaction, the stock has shown remarkable strength over the past year, trading well above its 52-week low of $61.54.

Quarterly Performance Highlights

Micron’s fiscal third quarter delivered record revenue of $9.3 billion, representing a 15% increase quarter-over-quarter and an impressive 37% jump year-over-year. This performance significantly exceeded the company’s previous guidance, demonstrating accelerating momentum in key segments.

As shown in the following revenue breakdown:

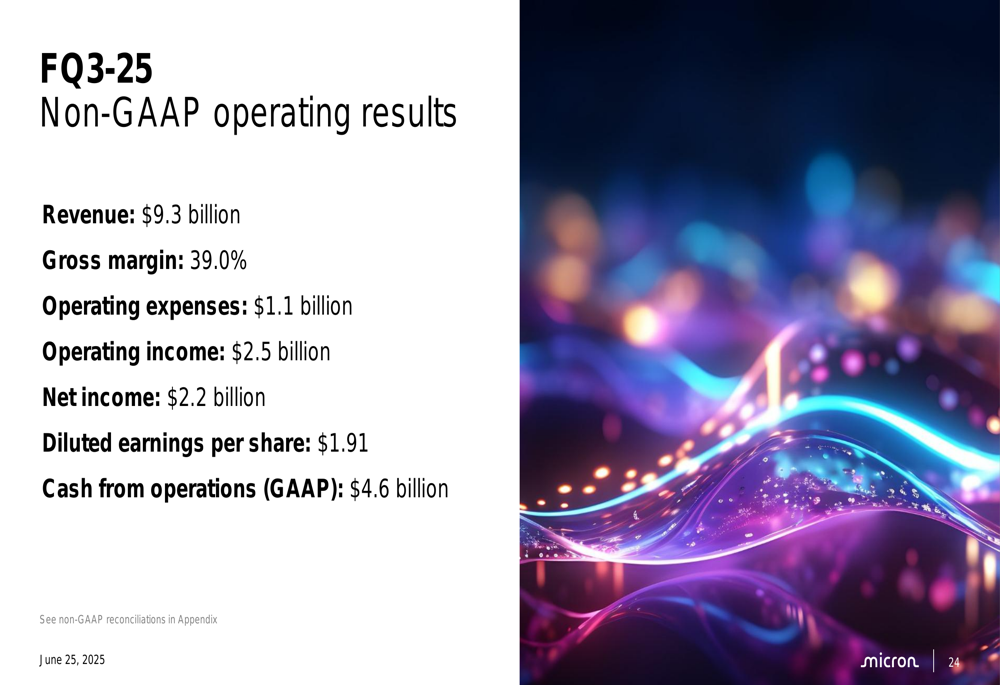

The company’s non-GAAP gross margin reached 39.0%, operating income hit $2.5 billion, and diluted earnings per share came in at $1.91. These results reflect substantial improvement over the same period last year and sequential growth from the previous quarter.

The comprehensive financial results highlight Micron’s strengthening profitability:

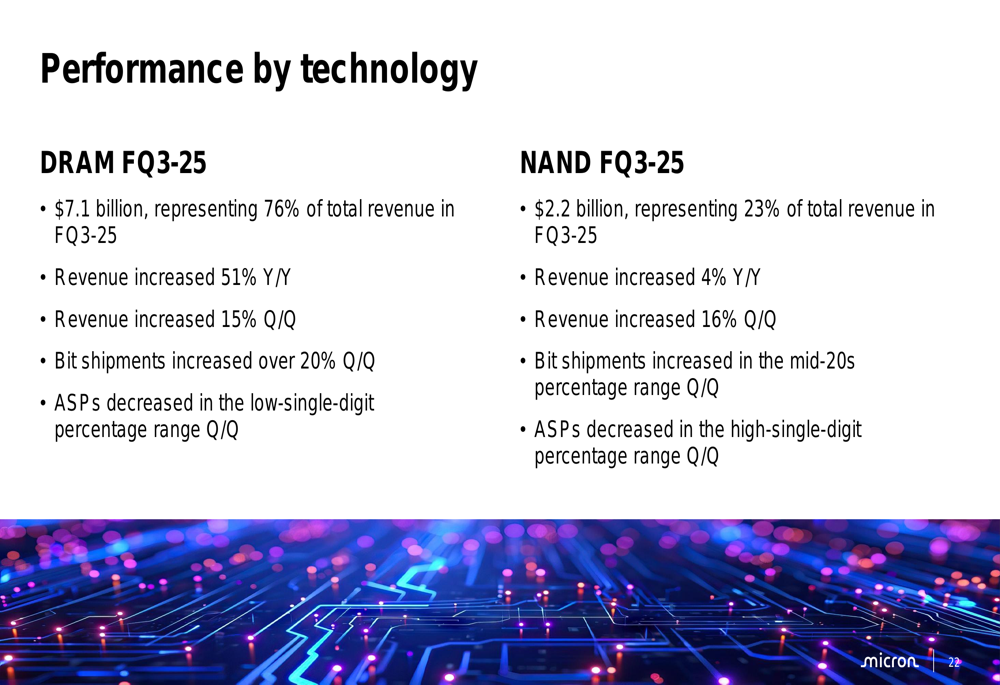

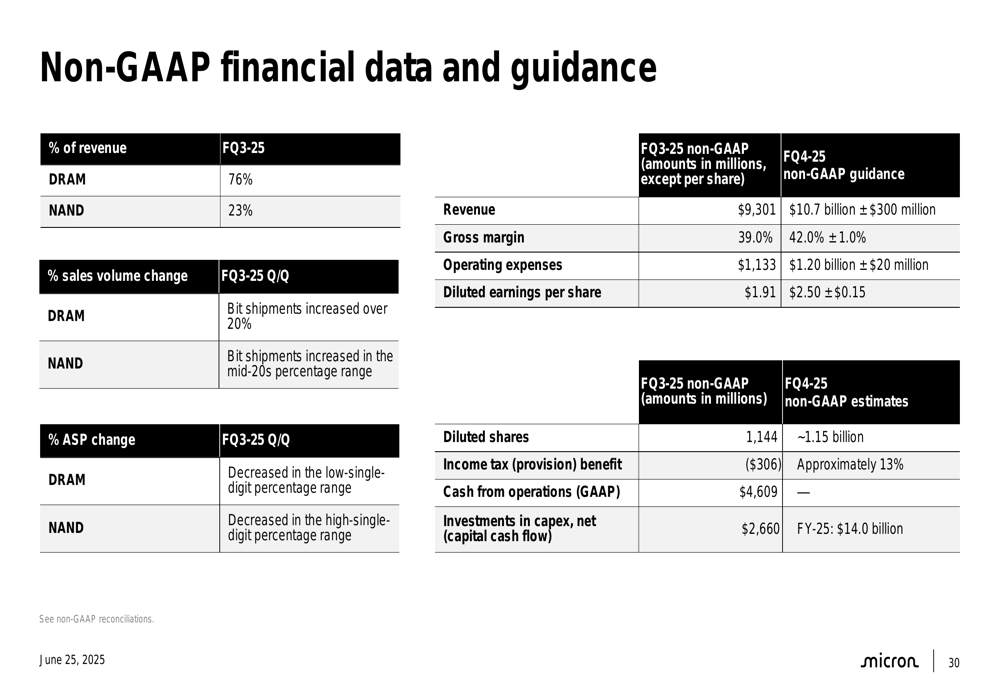

DRAM products continued to be the primary revenue driver, accounting for 76% of total revenue at $7.1 billion, up 51% year-over-year and 15% quarter-over-quarter. NAND flash revenue contributed $2.2 billion, representing 23% of total revenue, with more modest growth of 4% year-over-year and 16% quarter-over-quarter.

The performance breakdown by technology shows the diverging growth rates:

Detailed Financial Analysis

Micron’s business units showed varying performance, with the Compute and Networking Business Unit (CNBU) leading the way at $5.1 billion in revenue, up 11% sequentially and an extraordinary 97% year-over-year. This growth was primarily driven by data center demand, particularly for AI applications.

The Mobile Business Unit (MBU) demonstrated the strongest sequential growth at 45%, reaching $1.6 billion, though it remained slightly below year-ago levels. The Embedded Business Unit (EBU) grew 20% sequentially to $1.2 billion, while the Storage Business Unit (SBU) increased 4% to $1.5 billion.

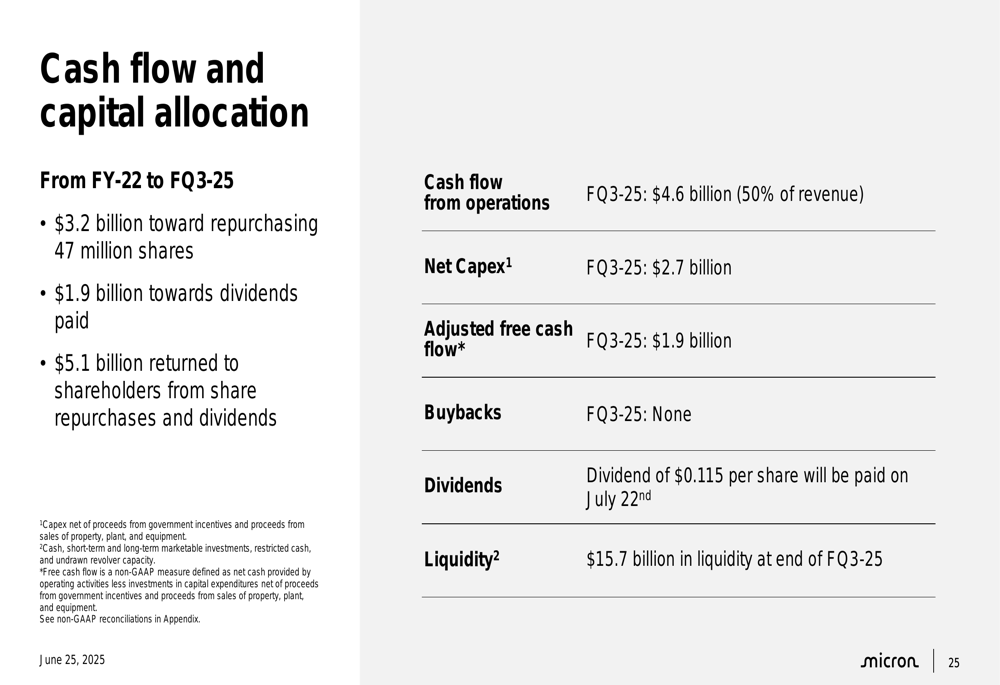

Cash flow generation was particularly impressive, with operations generating $4.6 billion (50% of revenue) and adjusted free cash flow of $1.9 billion. The company maintained strong liquidity of $15.7 billion at the end of the quarter.

The following slide details Micron’s cash flow and capital allocation strategy:

Strategic Initiatives

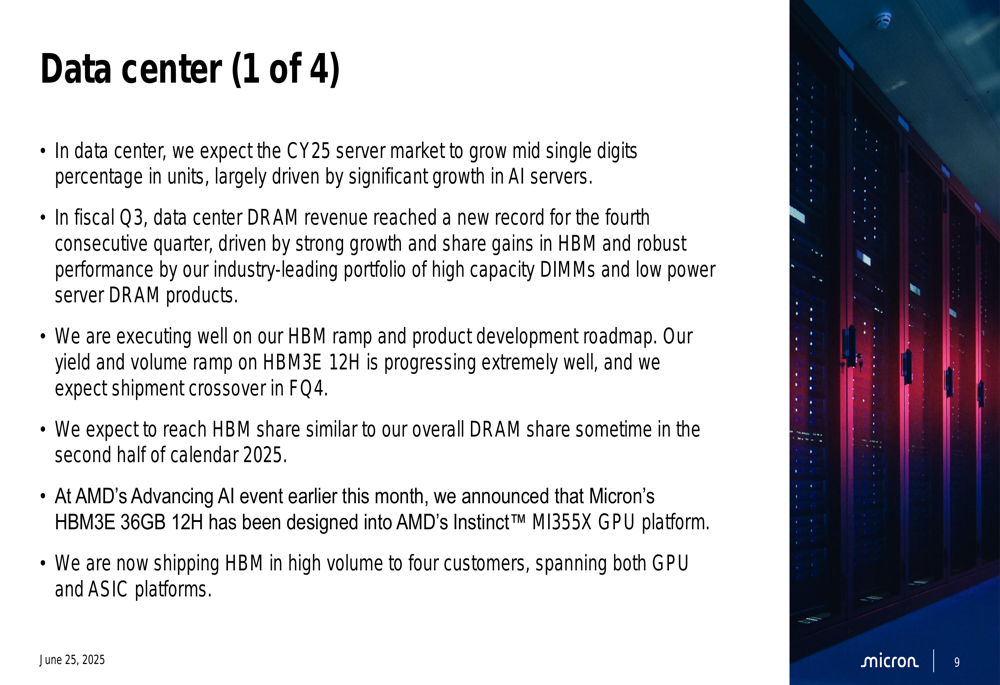

Micron’s presentation highlighted several strategic initiatives centered around AI and advanced memory technologies. The company reported that data center revenue more than doubled year-over-year, reaching record levels, with High Bandwidth (NASDAQ:BAND) Memory (HBM) revenue growing nearly 50% sequentially.

The company’s focus on data center and AI applications is evident in its technological advancements:

On the manufacturing front, Micron announced approximately $200 billion in planned U.S. investments over 20+ years, with $150 billion allocated to manufacturing and $50 billion to R&D. This includes an additional $30 billion investment beyond previously announced plans, featuring a second leading-edge memory fabrication facility in Boise, Idaho, expansion in Manassas, Virginia, and advanced packaging capabilities.

The company also highlighted progress on its 1-gamma DRAM technology node, which is ramping ahead of record pace. This technology offers 30% improvement in bit density, more than 20% lower power consumption, and up to 15% higher performance compared to previous generations.

CEO Sanjay Mehrotra summarized the company’s strategic position in his closing remarks:

Forward-Looking Statements

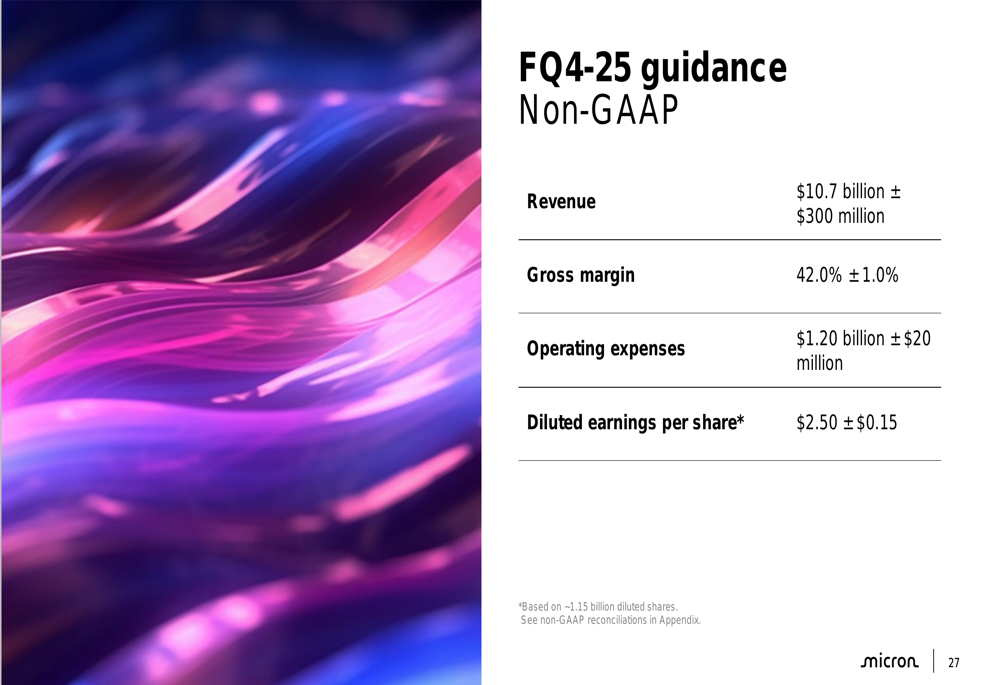

Looking ahead, Micron provided strong guidance for its fiscal fourth quarter 2025, projecting revenue of $10.7 billion (±$300 million), which represents approximately 15% sequential growth. The company also expects further margin expansion, with non-GAAP gross margin projected at 42.0% (±1.0%) and diluted earnings per share of $2.50 (±$0.15).

The detailed guidance for the upcoming quarter shows continued momentum:

For the broader market, Micron expects calendar year 2025 industry DRAM bit demand growth to be in the high-teens percentage range and NAND bit demand growth in the low double-digit percentage range. The company plans to manage its bit supply growth below industry demand growth for both DRAM and NAND, supporting a favorable pricing environment.

Micron anticipates exiting fiscal 2025 with tight DRAM inventories and reduced NAND inventories, positioning the company well for continued strong performance. The company also expects continued growth in AI-enabled devices across segments, including PCs, smartphones, and automotive applications, driving memory content growth.

The comprehensive financial data and guidance provide a clear picture of Micron’s expectations:

Micron’s FQ3 2025 presentation demonstrates the company’s strong execution and strategic positioning in high-growth memory markets, particularly those related to AI applications. With record revenue, expanding margins, and robust cash flow generation, the company appears well-positioned to capitalize on growing demand for advanced memory solutions across multiple end markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.