Gold scales new record high; nears $4,200/oz on Fed easing bets, trade tensions

Introduction & Market Context

Midland States Bancorp, Inc. (NASDAQ:MSBI) reported a significant net loss of $54.8 million, or ($2.52) per diluted share, for the fourth quarter of 2024. The loss primarily stemmed from strategic decisions to exit high-risk loan portfolios and aggressive credit management actions. Despite these short-term financial impacts, the bank highlighted several positive underlying trends, including an expanded net interest margin and strong noninterest income.

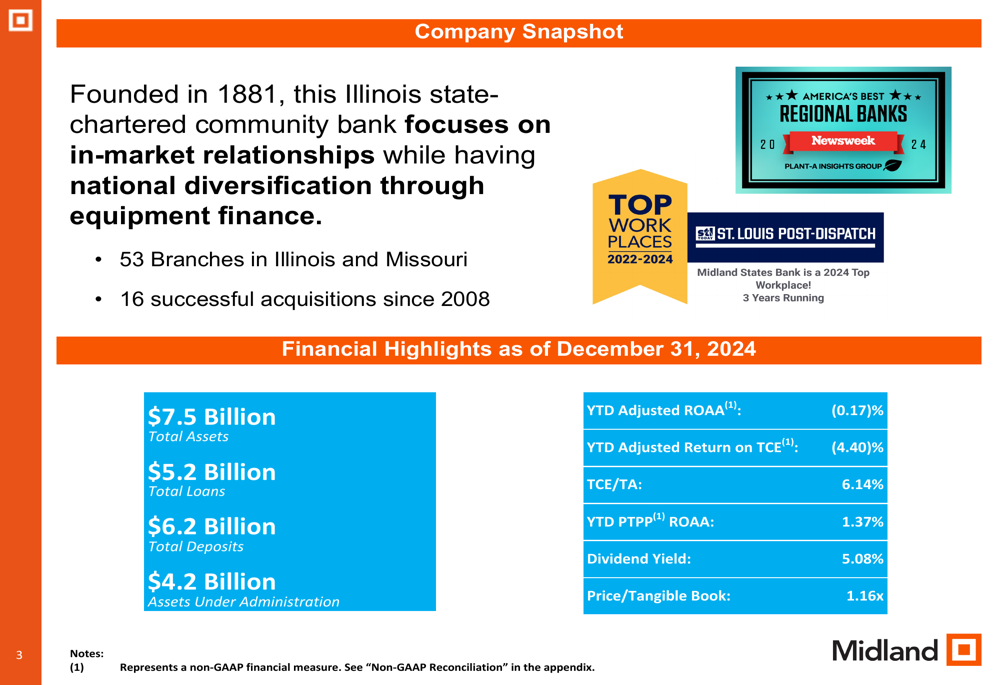

The Illinois and Missouri-based regional bank, founded in 1881, operates 53 branches and manages $7.5 billion in total assets. Management emphasized that these strategic moves position the institution for improved performance in 2025 by reducing credit risk and refocusing on relationship-based community banking.

Quarterly Performance Highlights

Midland’s fourth quarter results reflect a company in transition, with significant one-time charges overshadowing some positive operational metrics. Pre-tax, pre-provision earnings remained solid at $21.5 million, while noninterest income was strong at $19.6 million.

The bank’s snapshot reveals its current financial position, with $5.2 billion in total loans, $6.2 billion in deposits, and $4.2 billion in assets under administration. However, profitability metrics reflect the impact of the quarter’s strategic decisions, with year-to-date adjusted return on average assets at -0.17% and return on tangible common equity at -4.40%.

As shown in the company overview:

Credit Management Actions

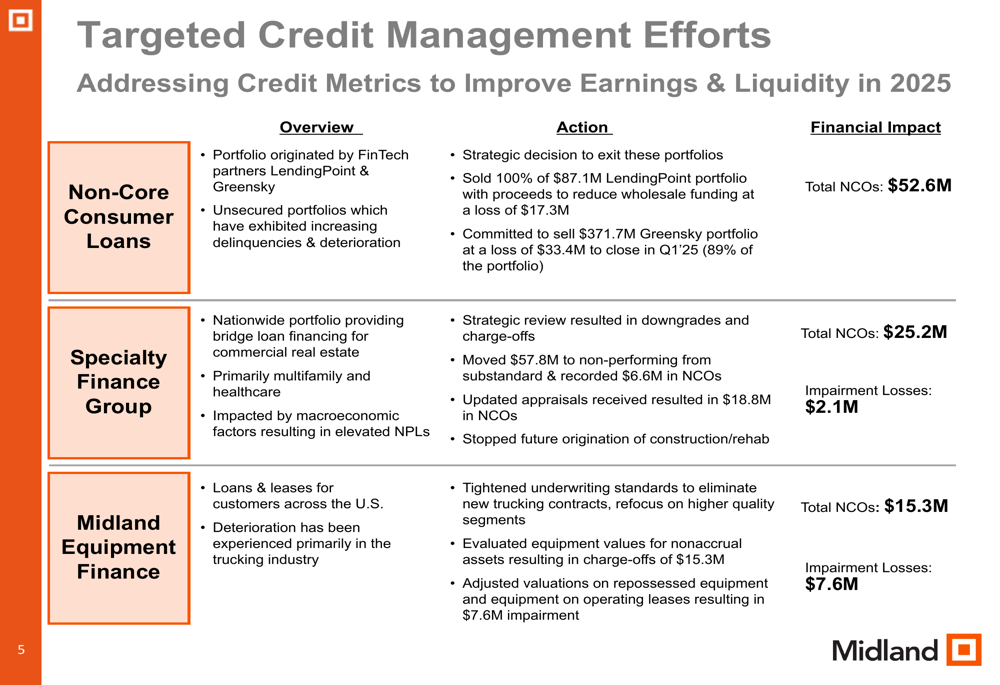

The most significant driver of Midland’s quarterly loss was its targeted credit management efforts across several portfolios. Management characterized these actions as necessary steps to improve earnings and liquidity in 2025.

In the non-core consumer segment, Midland sold 100% of its $87.1 million LendingPoint portfolio at a loss of $17.3 million. Additionally, the bank committed to sell $371.7 million (89%) of its Greensky (NASDAQ:GSKY) portfolio at a loss of $33.4 million, with that transaction expected to close in Q1 2025.

The Specialty Finance Group underwent a strategic review resulting in $25.2 million in net charge-offs and $2.1 million in impairment losses. Similarly, the Midland Equipment Finance division recorded $15.3 million in net charge-offs and $7.6 million in impairment losses, while tightening underwriting standards to eliminate new trucking contracts.

These targeted credit actions are clearly detailed in the following slide:

Core Business Performance

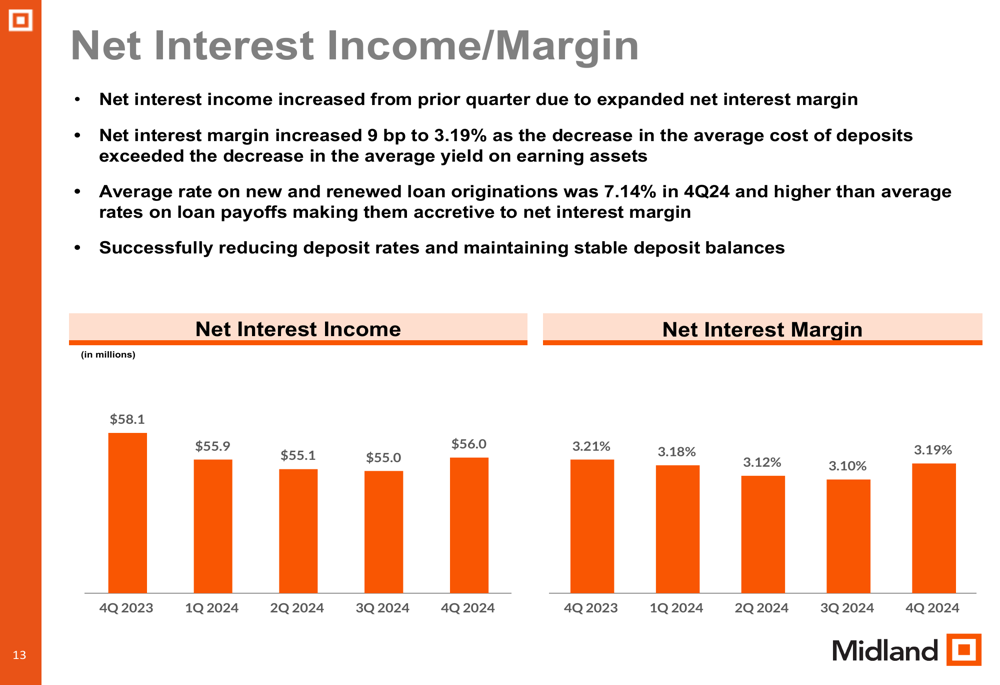

Despite the significant charges, Midland’s core banking business showed several positive trends. The net interest margin expanded 9 basis points to 3.19%, as the decrease in deposit costs outpaced the decline in earning asset yields. This improvement occurred despite the overall reduction in the loan portfolio.

As illustrated in the net interest income and margin trends:

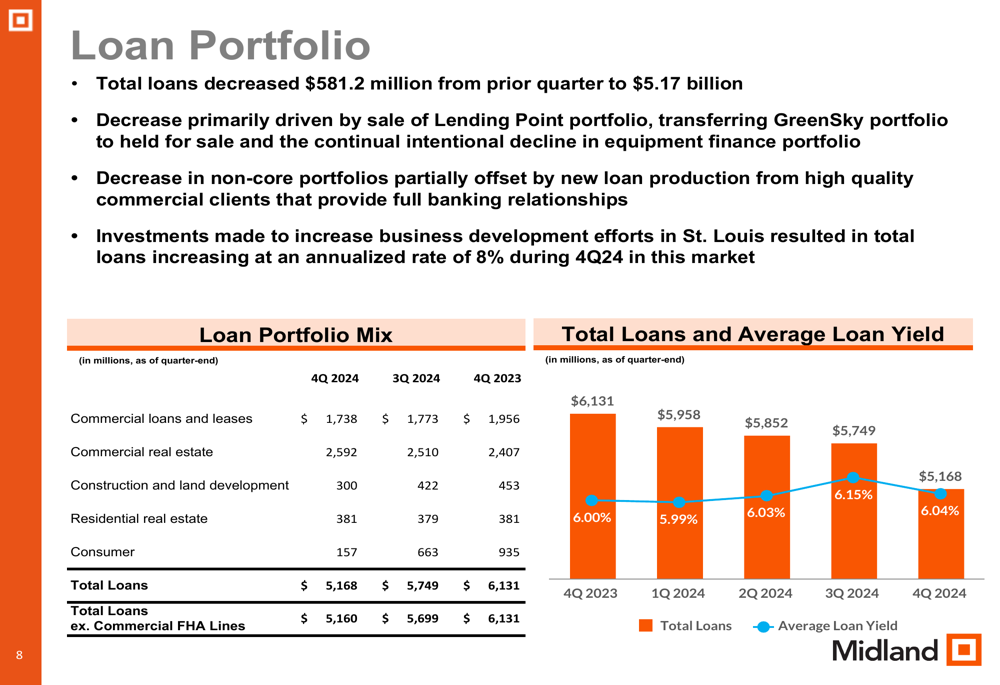

The loan portfolio decreased by $581.2 million from the previous quarter to $5.17 billion, primarily due to the strategic sale of consumer portfolios and intentional reduction in equipment finance. However, the company noted that its community banking segment showed stable performance, with growth in high-quality commercial relationships, particularly in the St. Louis market where loans increased at an annualized rate of 8% during the quarter.

The composition of the loan portfolio is shifting toward in-market commercial and industrial (C&I) and commercial real estate (CRE) loans, which management believes will result in higher quality assets:

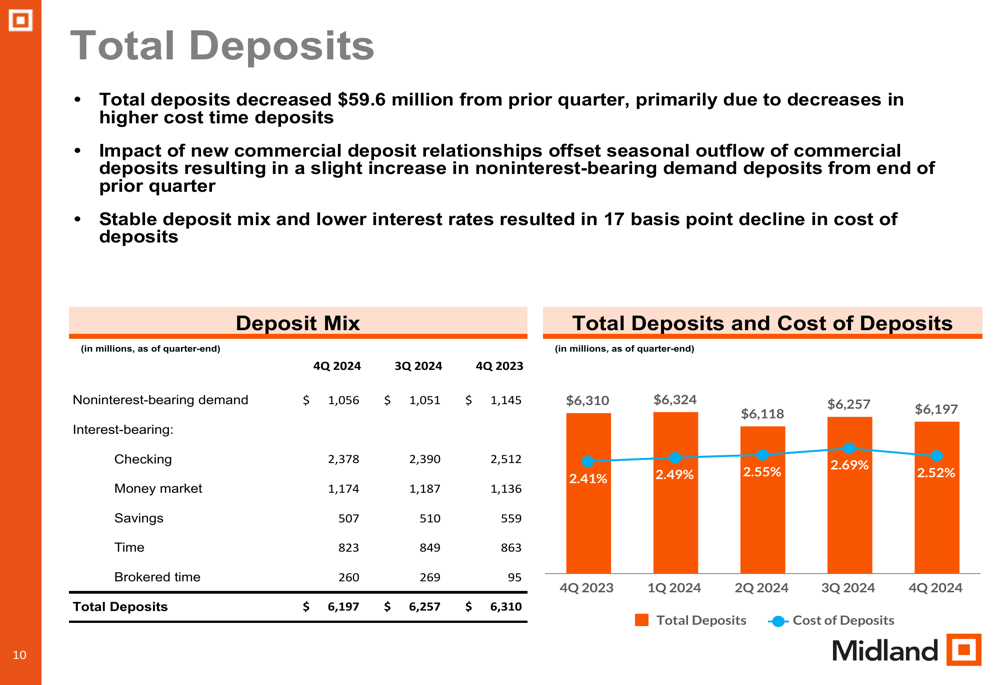

On the deposit side, total deposits decreased by $59.6 million to $6.2 billion, primarily due to reductions in higher-cost time deposits. The bank maintained a stable deposit mix, with noninterest-bearing demand deposits slightly increasing from the previous quarter. The cost of deposits declined by 17 basis points, benefiting from both the stable deposit mix and lower interest rates.

Wealth management continued to be a bright spot, with revenue increasing due to additional trust and estate fees collected in the quarter. The bank noted that the continual hiring of wealth advisors is positively impacting new business development, which should support future growth in this segment.

Strategic Initiatives & Forward Outlook

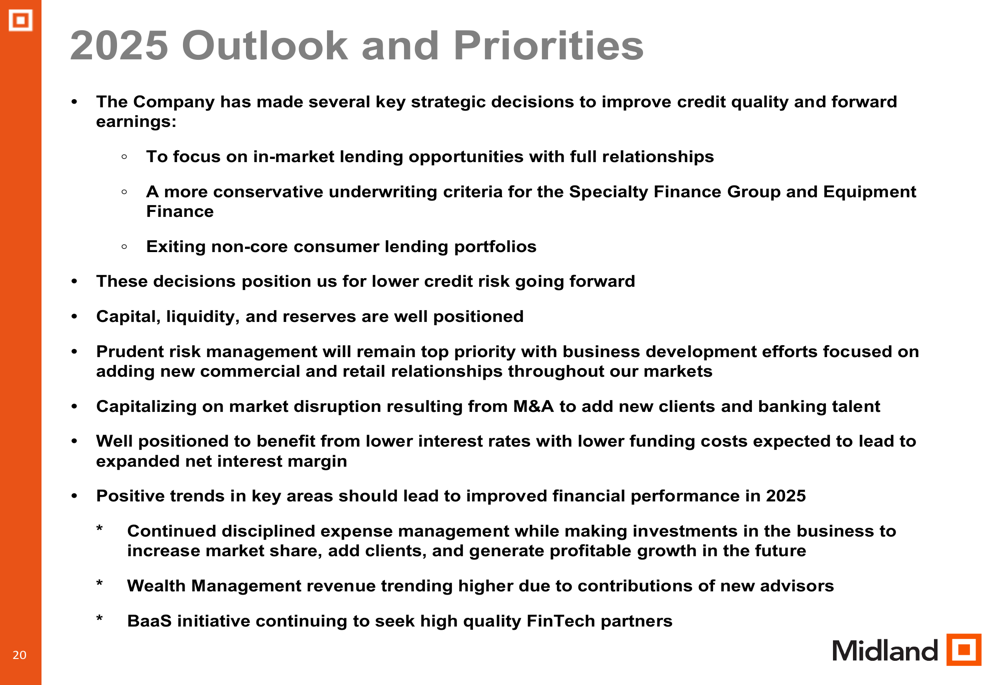

Looking ahead to 2025, Midland outlined several strategic priorities focused on improving credit quality and earnings. The bank plans to concentrate on in-market lending opportunities with full banking relationships, implement more conservative underwriting criteria for specialty finance and equipment finance, and complete its exit from non-core consumer lending portfolios.

Management expressed confidence that these decisions position the bank for lower credit risk going forward, with capital, liquidity, and reserves well-positioned to support future growth. The bank also expects to benefit from lower interest rates, with reduced funding costs projected to lead to an expanded net interest margin.

As detailed in the company’s outlook:

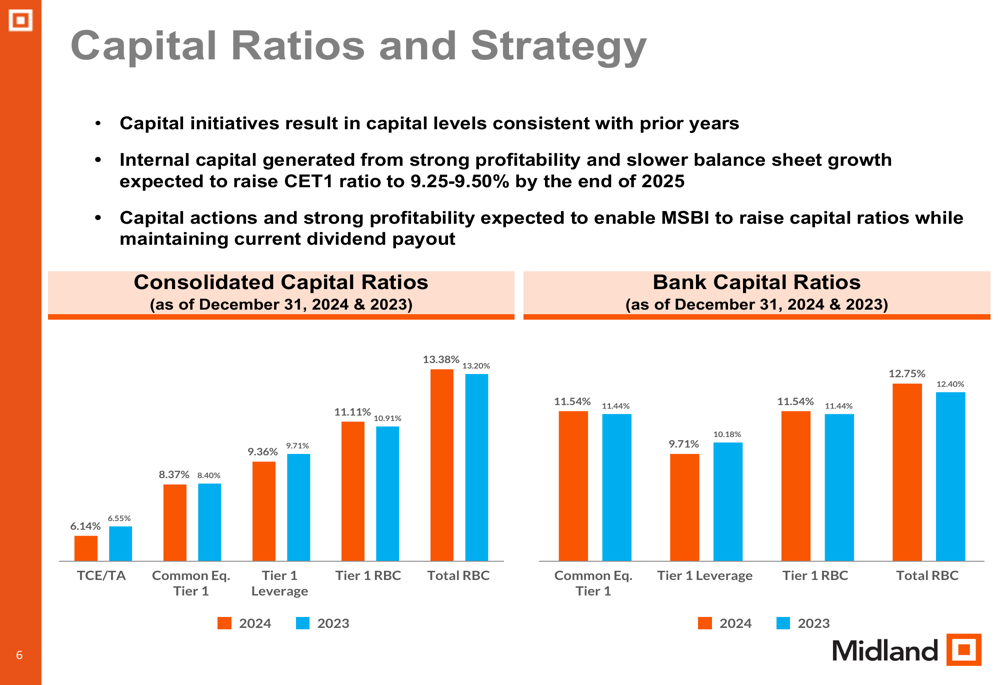

The bank’s capital strategy aims to raise its Common Equity Tier 1 (CET1) ratio to 9.25-9.50% by the end of 2025 through internal capital generation from improved profitability and slower balance sheet growth. Management indicated that capital actions and strong profitability should enable the bank to raise capital ratios while maintaining its current dividend payout, which currently yields 5.08%.

Midland is also capitalizing on market disruption resulting from merger and acquisition activity to add new clients and banking talent. The bank continues to pursue its Banking-as-a-Service (BaaS) initiative, seeking high-quality FinTech partners to expand this business line.

Detailed Financial Analysis

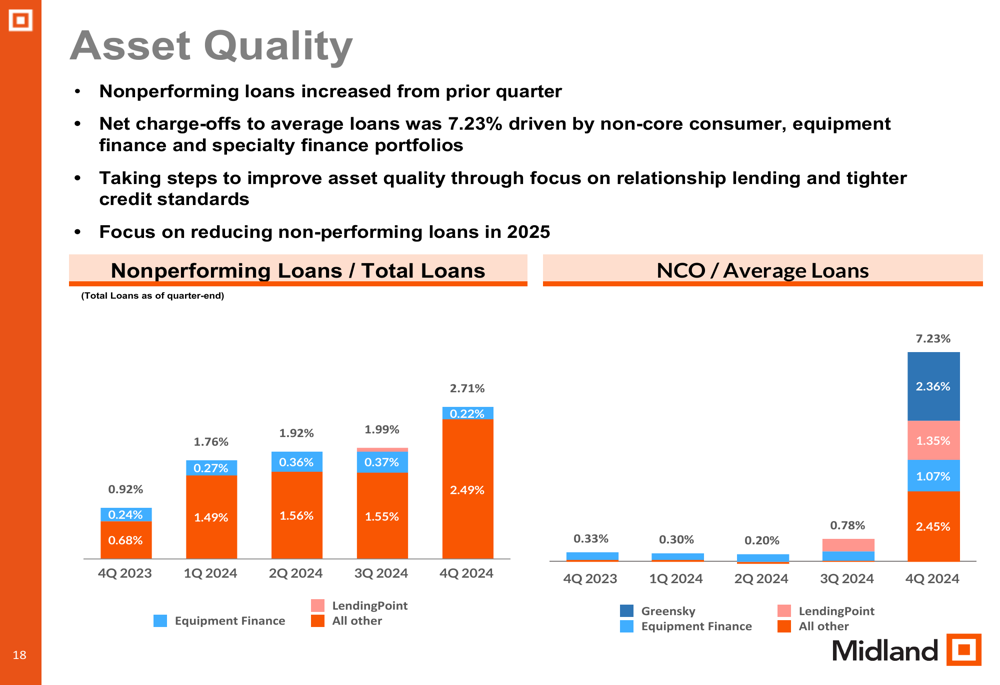

Asset quality metrics reflected the significant credit actions taken during the quarter. Nonperforming loans increased from the prior quarter, and net charge-offs to average loans reached 7.23%, driven primarily by the strategic exits from non-core consumer, equipment finance, and specialty finance portfolios.

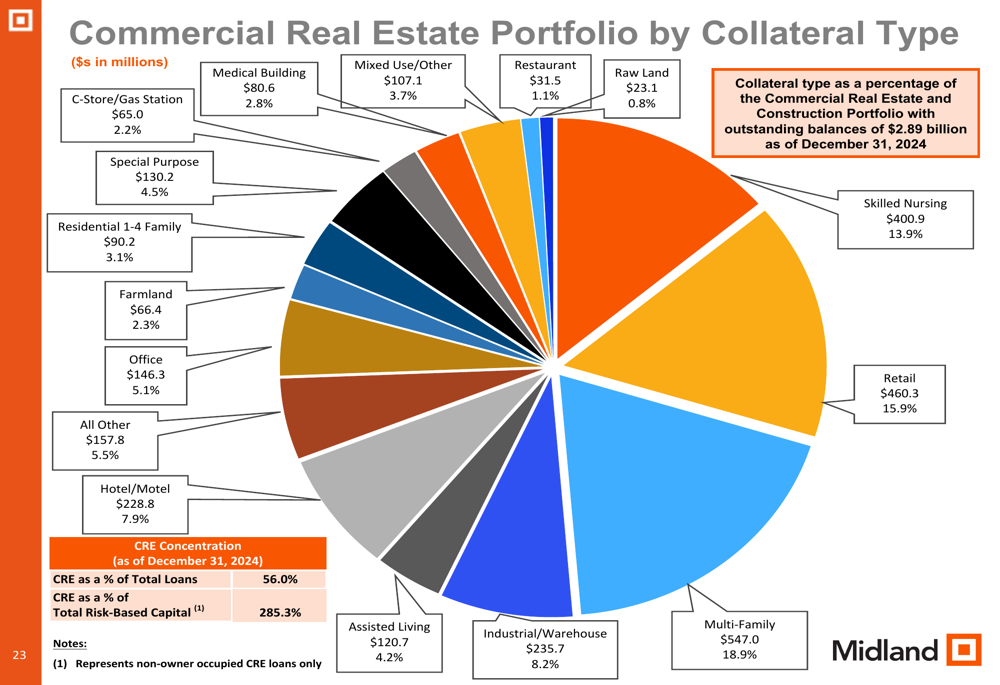

The bank’s commercial real estate portfolio, which represents 56% of total loans and 285.3% of total risk-based capital, remains diversified across various property types. Multi-family (18.9%), retail (15.9%), and skilled nursing (13.9%) represent the largest segments of the CRE portfolio.

Midland’s efficiency ratio increased to 71.4% in Q4 2024 from 62.8% in the previous quarter, reflecting the impact of impairment charges. Excluding these one-time items, management expects a near-term operating expense run-rate of approximately $48.5-$49.0 million per quarter.

The bank’s liquidity position improved during the quarter, with total estimated liquidity increasing to $2.62 billion from $2.29 billion at the end of the third quarter. The loan-to-deposit ratio decreased to 83.4% from 91.9%, providing additional flexibility for future growth.

In summary, while Midland States Bancorp’s fourth quarter results reflect significant short-term pain from strategic portfolio exits and credit management actions, the bank appears to be positioning itself for improved performance in 2025 through a renewed focus on relationship banking, tighter credit standards, and strategic growth initiatives in its core markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.