Adaptimmune stock plunges after announcing Nasdaq delisting plans

Millrose Properties Inc (NYSE:MRP) presented its second quarter 2025 earnings results on July 31, showcasing solid financial performance and strategic expansion beyond its core relationship with Lennar Corporation. The company reported net income of $112.8 million ($0.68 per share) and maintained a conservative leverage profile while expanding its third-party investment portfolio.

Introduction & Market Context

Millrose Properties, which operates as a land banking platform for homebuilders, delivered consistent results in an environment characterized by structural housing undersupply. The company’s stock closed at $31.08 on the earnings release date, up 1.38% in regular trading, though it declined 1.48% in aftermarket trading to $30.62.

The company continues to benefit from favorable industry dynamics, including historically low housing inventory levels and strong homebuilder margins, while executing on its strategy to diversify its customer base beyond its foundational relationship with Lennar.

Quarterly Performance Highlights

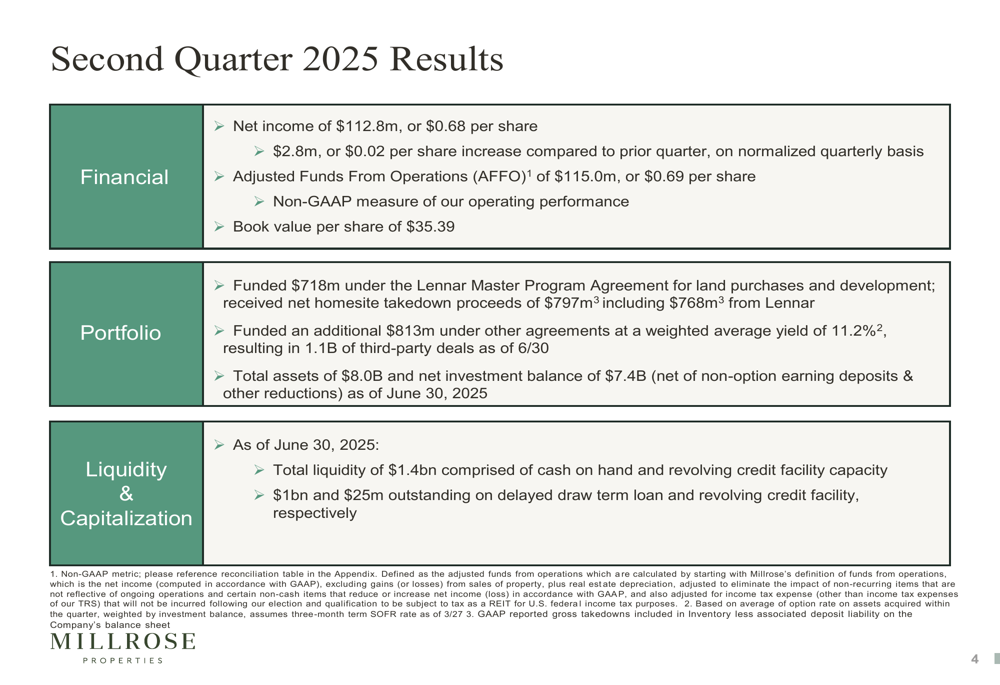

Millrose reported Q2 2025 net income of $112.8 million, or $0.68 per share, representing a $0.02 per share increase from the previous quarter on a normalized basis. Adjusted Funds From Operations (AFFO) reached $115.0 million, or $0.69 per share, supporting a quarterly dividend of the same amount.

As shown in the following comprehensive financial overview:

The company maintained a book value per share of $35.39 while generating a 7.8% annualized return on shareholder equity, an increase of 20 basis points compared to the prior quarter. Total assets grew to $8.0 billion, with a net investment balance of $7.4 billion as of June 30, 2025.

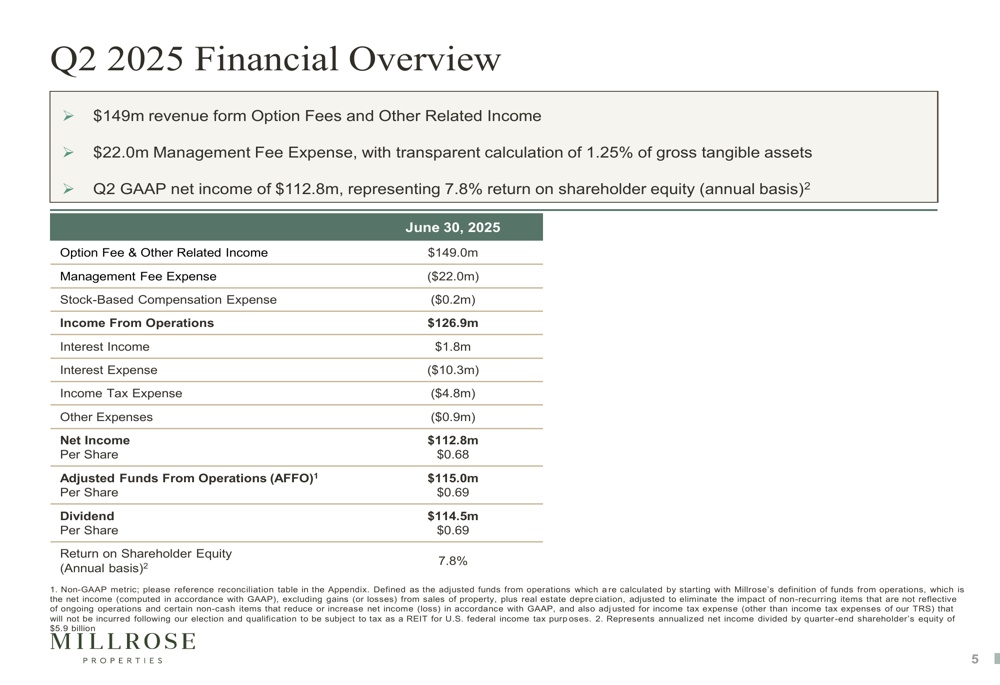

The financial results breakdown reveals strong revenue generation from option fees:

Strategic Initiatives

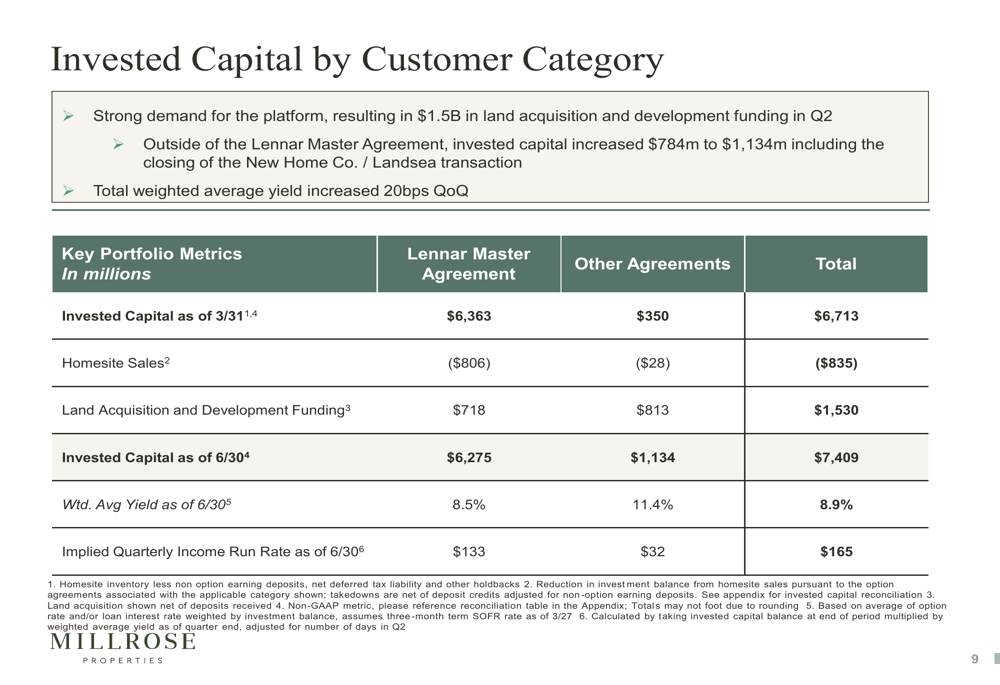

A key strategic development for Millrose is its continued diversification beyond Lennar. While Lennar remains its largest customer, the company significantly expanded its third-party investment portfolio during Q2, increasing from $350 million to $1.13 billion. This expansion included closing the New Home Co./Landsea transaction and deploying $813 million under agreements with third parties at an attractive weighted average yield of 11.2%.

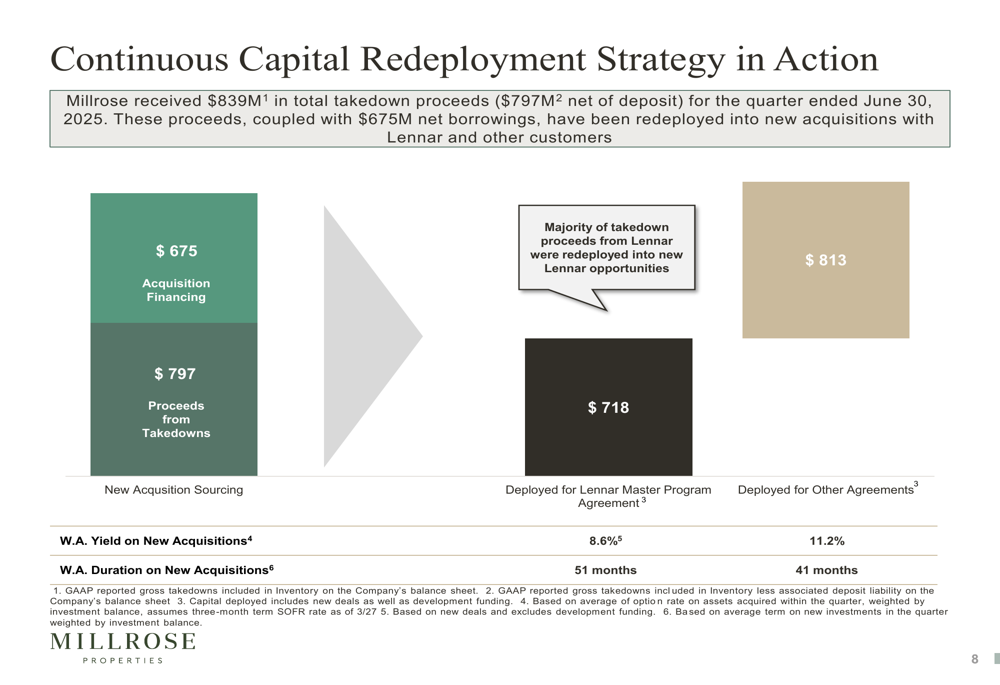

The company’s capital redeployment strategy demonstrates how it’s recycling capital from homesite takedowns into new acquisitions:

Notably, Millrose announced a significant new partnership with Taylor Morrison after the quarter closed. On July 23, 2025, Taylor Morrison and Kennedy Lewis Investment Management established a $3 billion financing facility agreement for built-to-rent communities under their "Yardly" platform, with Millrose securing right-of-first-refusal for funding during the 2.5-year exclusivity period.

"Our innovative home site option purchase platform isn’t just a solution. It’s a fundamental shift in how capital flows to meet robust housing demand," CEO Darren Richmond stated during the earnings call.

Detailed Financial Analysis

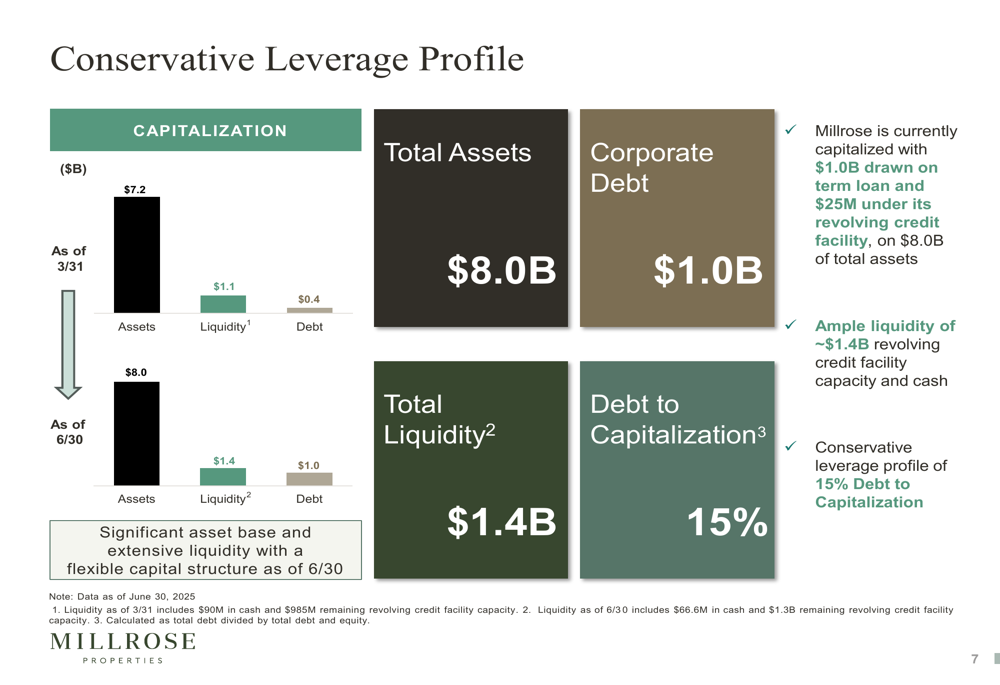

Millrose maintains a conservative financial position with ample liquidity of $1.4 billion and a debt-to-capitalization ratio of just 15%, as illustrated in the following leverage profile:

The company’s investment portfolio continues to evolve, with the proportion of capital deployed to customers other than Lennar growing significantly. This diversification has contributed to an increase in the total weighted average yield by 20 basis points quarter-over-quarter, reaching 8.9%.

The breakdown of invested capital by customer category shows this strategic shift:

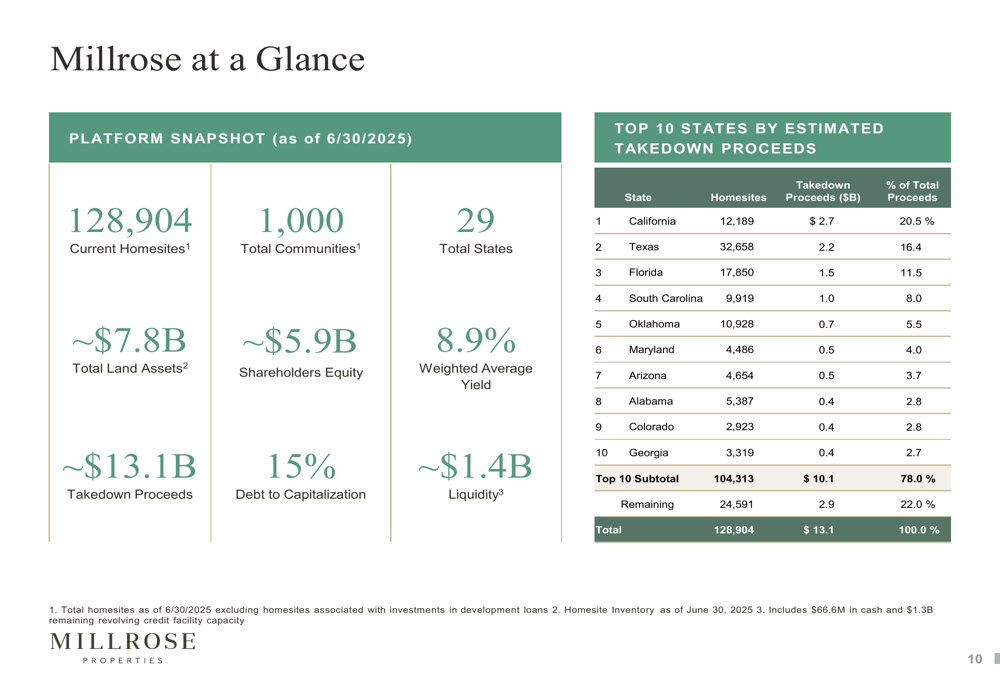

Millrose’s geographic diversification spans 29 states with 1,000 total communities and nearly 129,000 homesites. California (20.5%), Texas (16.4%), and Florida (11.5%) represent the largest concentrations by estimated takedown proceeds.

Market Outlook & Forward-Looking Statements

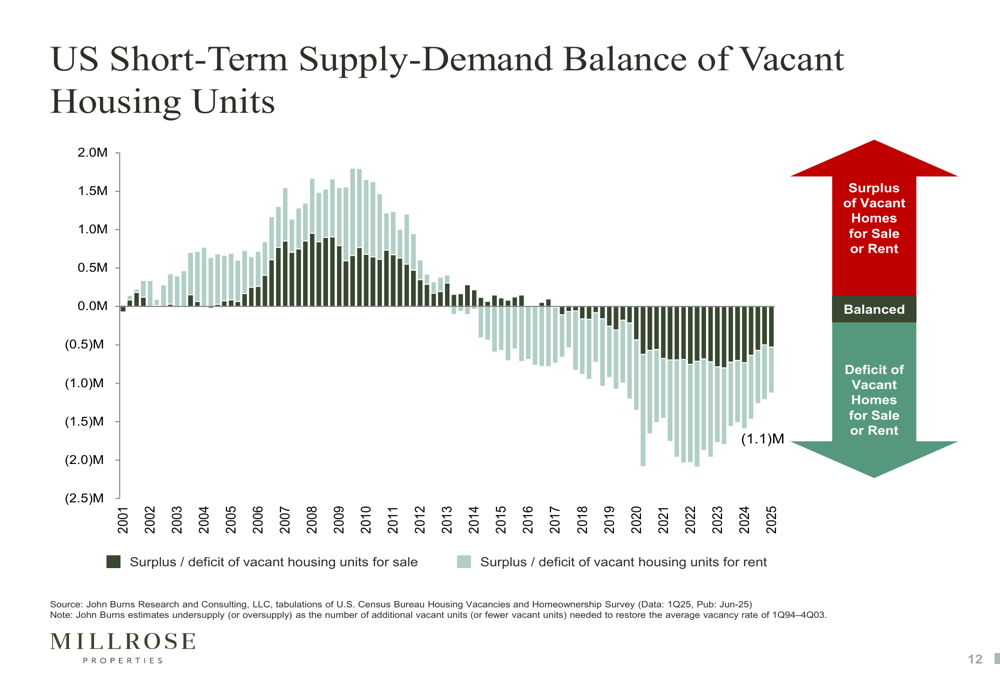

Millrose continues to operate in a housing market characterized by structural undersupply, as illustrated by the deficit of vacant housing units:

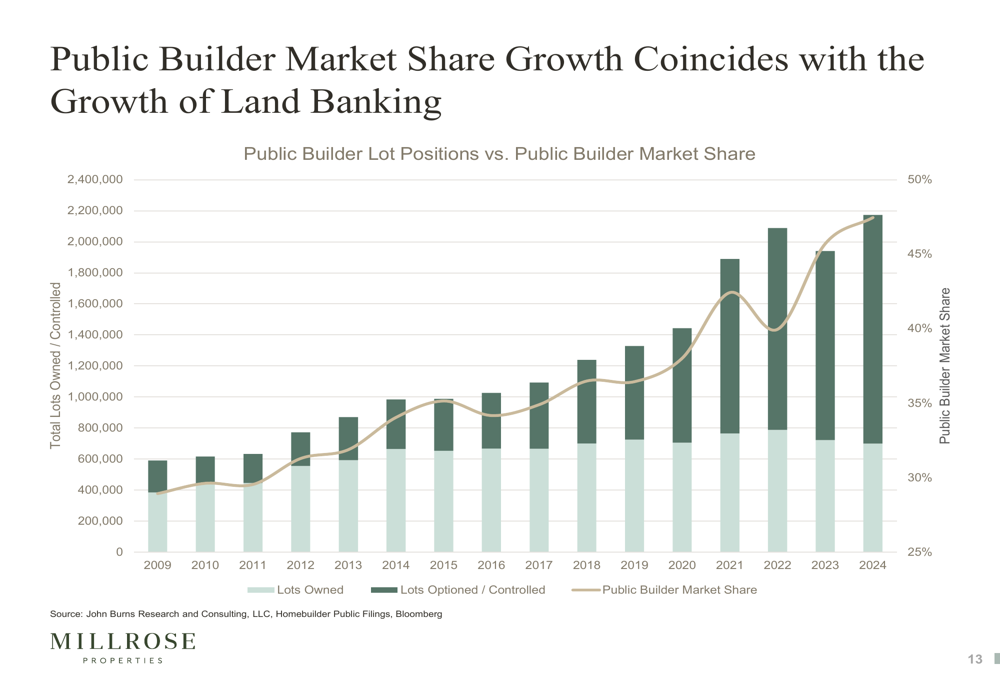

The company is capitalizing on the trend of increasing public builder market share coinciding with the growth of land banking services:

According to the earnings call, Millrose raised its year-end quarterly AFFO per share guidance to between $0.70 and $0.73, reflecting confidence in its continued growth trajectory. The company targets a $2 billion investment balance outside the Lennar agreement and expects the average yield to compress closer to 11%.

However, management acknowledged potential challenges, including affordability constraints in the housing market, elevated mortgage rates that may suppress transaction activity, and softening market conditions in regions like Florida and Texas.

Despite these challenges, Millrose’s positioning in a structurally undersupplied housing market, combined with its expanding customer base and conservative financial approach, appears to provide a solid foundation for continued performance. The company’s strategic pivot toward diversification beyond Lennar represents a significant evolution in its business model that investors will be watching closely in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.