European shares fall: Trump threatens ’massive’ tariff increase on China

Introduction & Market Context

Moderna , Inc. (NASDAQ:MRNA) released its second quarter 2025 financial results on August 1, 2025, revealing a significant year-over-year revenue decline alongside substantial progress in cost reduction initiatives. The company’s shares dropped 3.42% in premarket trading to $28.55, extending a challenging period that has seen the stock decline 8.06% in the previous session and trade well below its 52-week high of $91.99.

The biotechnology company continues to navigate a post-pandemic environment with diminished COVID-19 vaccine demand while advancing its broader pipeline of mRNA-based therapeutics and vaccines. Despite revenue challenges, Moderna highlighted three new FDA approvals during the quarter and positive Phase 3 data for its flu vaccine candidate.

Quarterly Performance Highlights

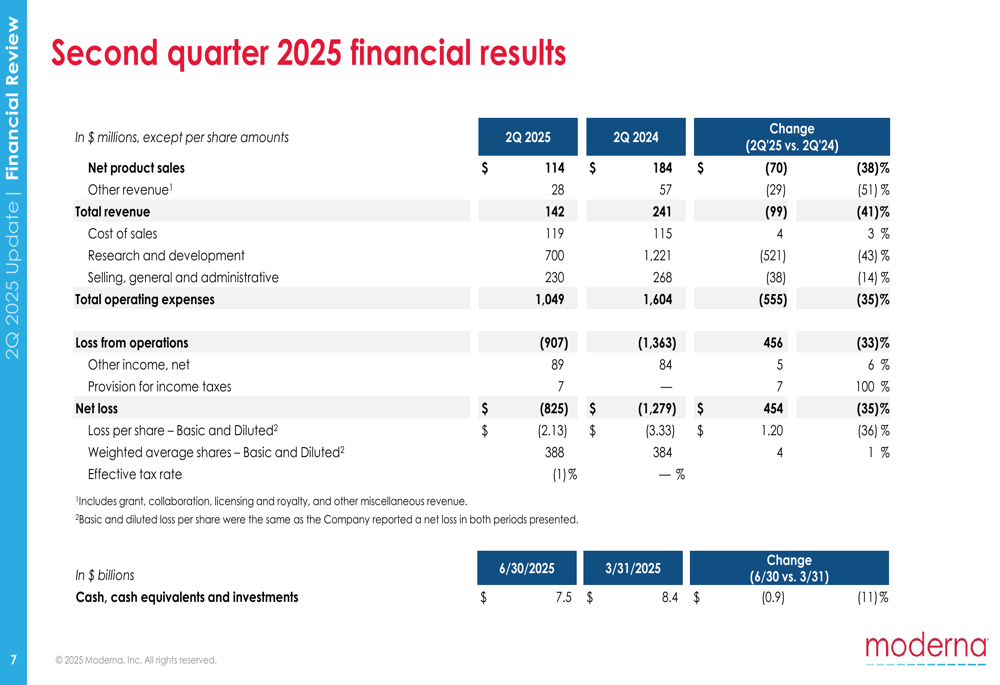

Moderna reported total revenue of $142 million for Q2 2025, representing a 41% decrease from $241 million in the same period last year. Net product sales fell 38% to $114 million, while other revenue declined 51% to $28 million. The company posted a net loss of $825 million, or $2.13 per share, which represents a 35% improvement from the $1.28 billion loss ($3.33 per share) recorded in Q2 2024.

As shown in the following detailed financial breakdown:

The company ended the quarter with $7.5 billion in cash and investments, down 11% from $8.4 billion at the end of Q1 2025. This cash position provides Moderna with significant runway as it continues to invest in its pipeline while implementing cost-cutting measures.

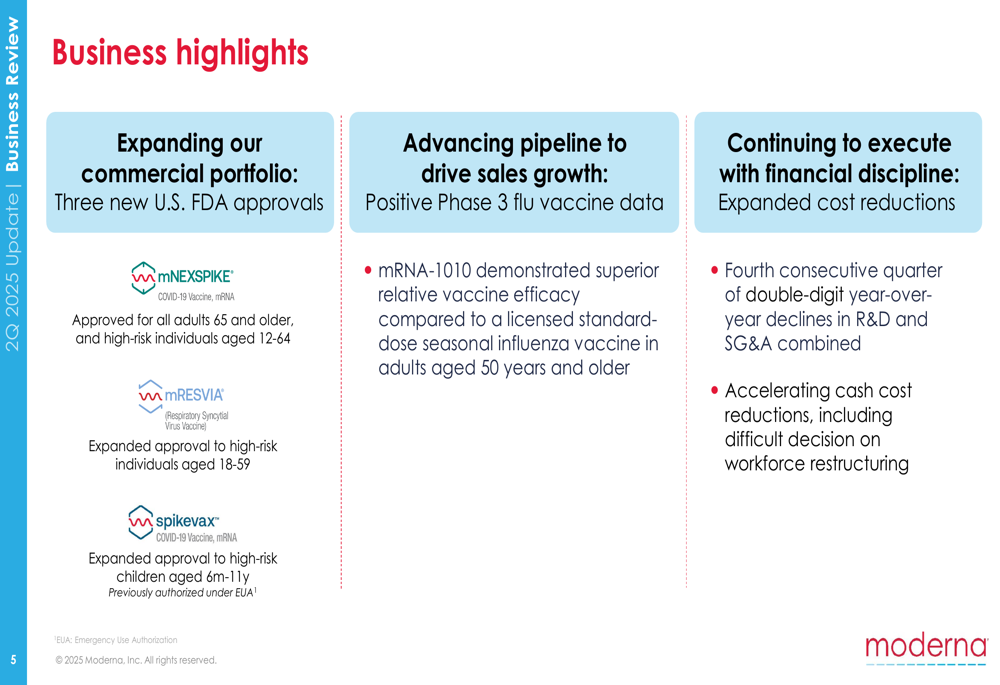

Key business highlights for the quarter included expanded regulatory approvals and positive clinical data:

Detailed Financial Analysis

Moderna’s cost-cutting initiatives showed significant progress, with total operating expenses decreasing 35% year-over-year to $1.05 billion. Research and development expenses saw the most dramatic reduction, falling 43% to $700 million, while selling, general and administrative expenses decreased 14% to $230 million.

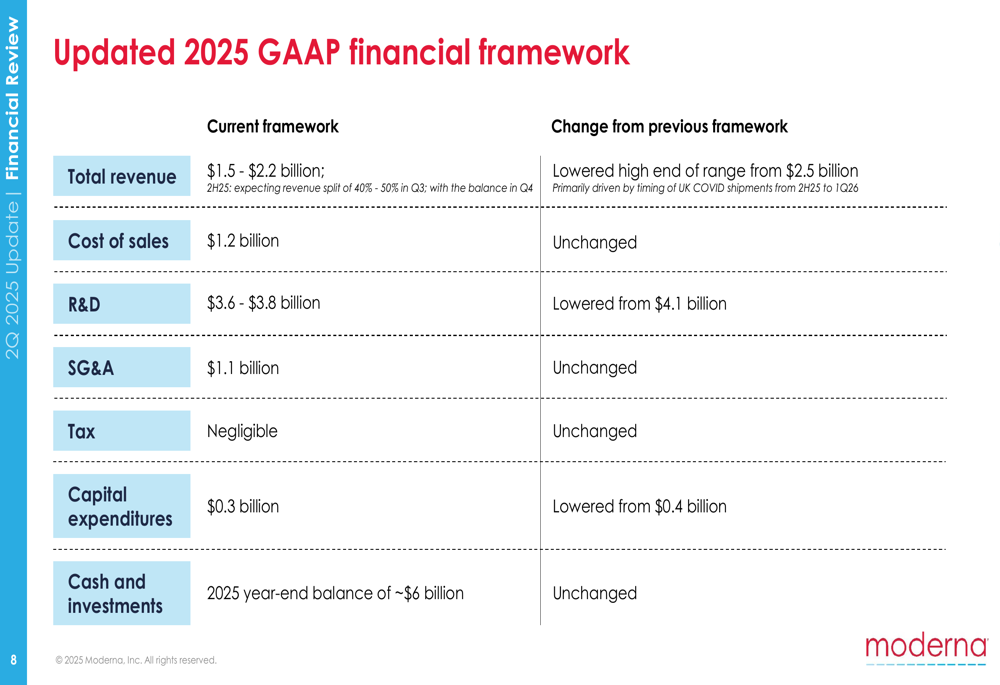

The company has updated its 2025 GAAP financial framework, lowering the high end of its revenue guidance from $2.5 billion to $2.2 billion, while also reducing projected R&D expenses from $4.1 billion to $3.6-3.8 billion:

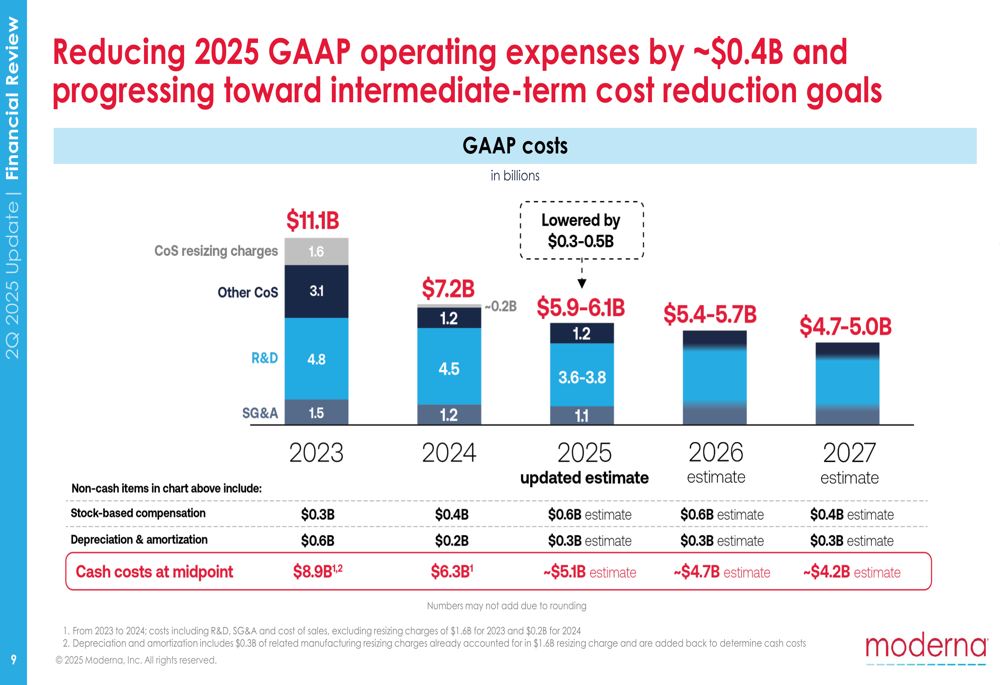

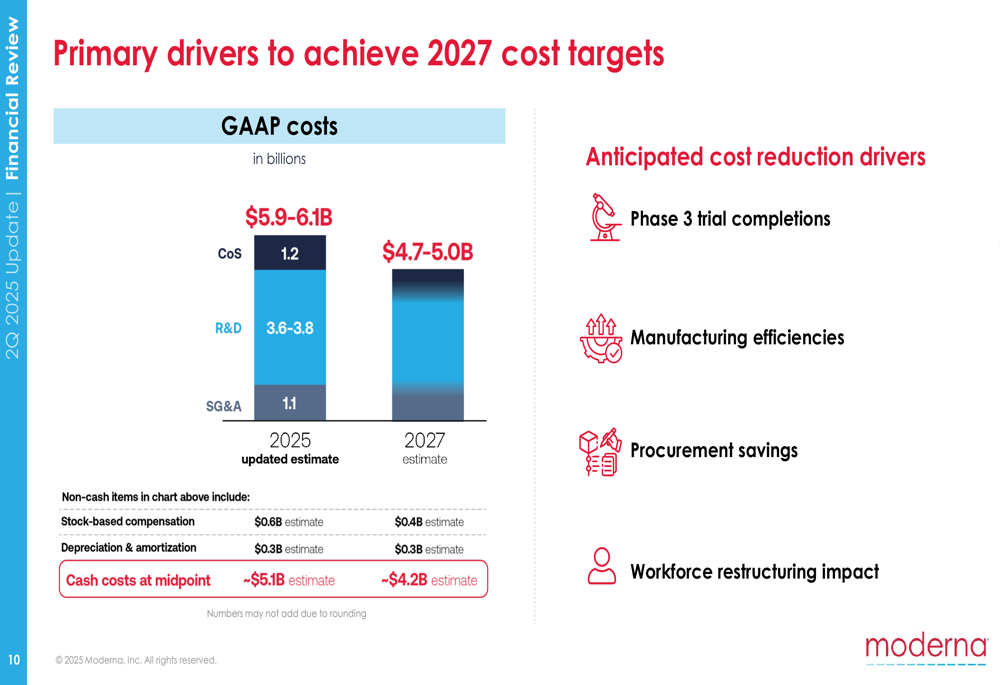

Moderna’s long-term cost reduction strategy aims to decrease GAAP costs from $11.1 billion in 2023 to $4.7-5.0 billion by 2027, as illustrated in this chart:

The company identified several key drivers to achieve these cost targets, including Phase 3 trial completions, manufacturing efficiencies, procurement savings, and workforce restructuring:

Strategic Initiatives

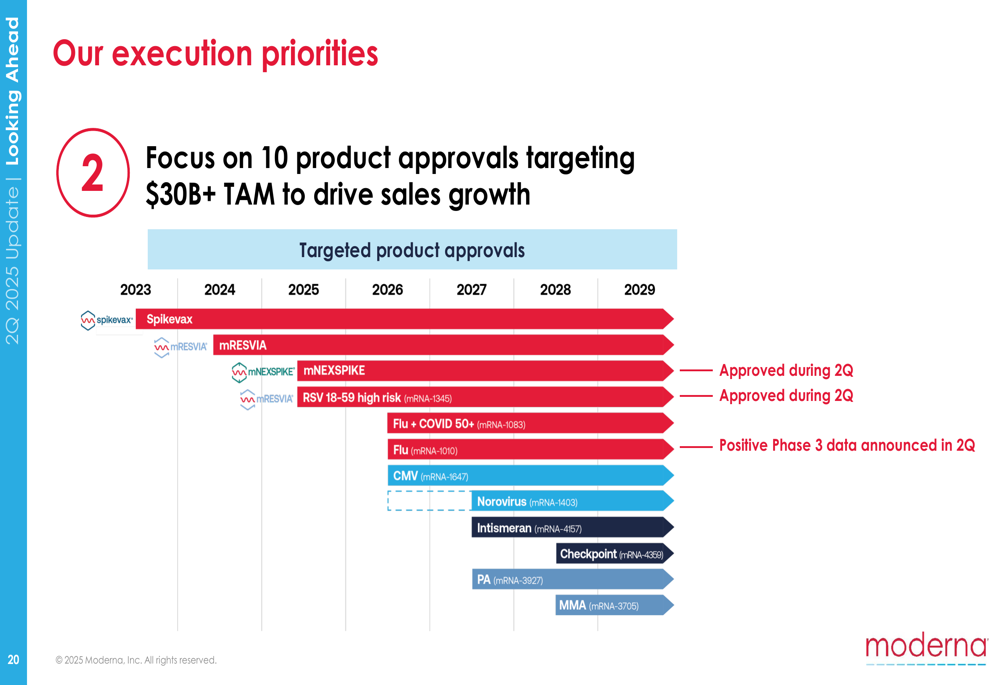

Moderna outlined three core execution priorities: driving use of approved vaccines, focusing on 10 product approvals to drive sales growth, and delivering cost efficiency across the business.

The company’s pipeline progress was highlighted by three new FDA approvals during the quarter: MNEXSPIKE for COVID-19 in adults 65+ and high-risk individuals 12-64, expanded approval for MRESVIA in high-risk adults 18-59, and expanded approval for Spikevax in high-risk children 6 months to 11 years.

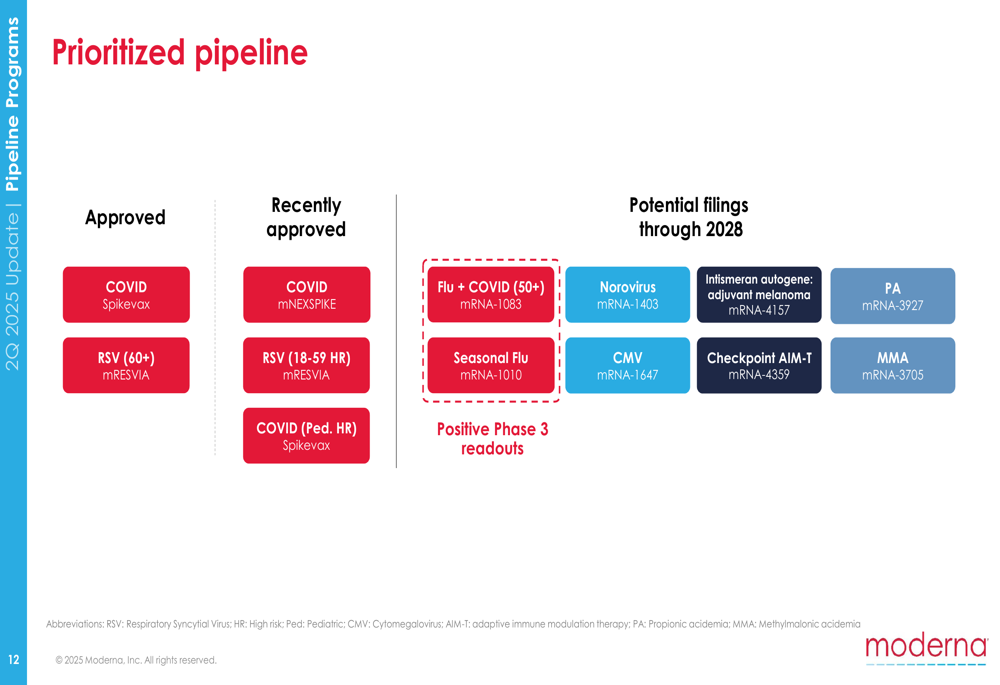

Moderna’s prioritized pipeline shows a mix of approved products and candidates with potential filings through 2028:

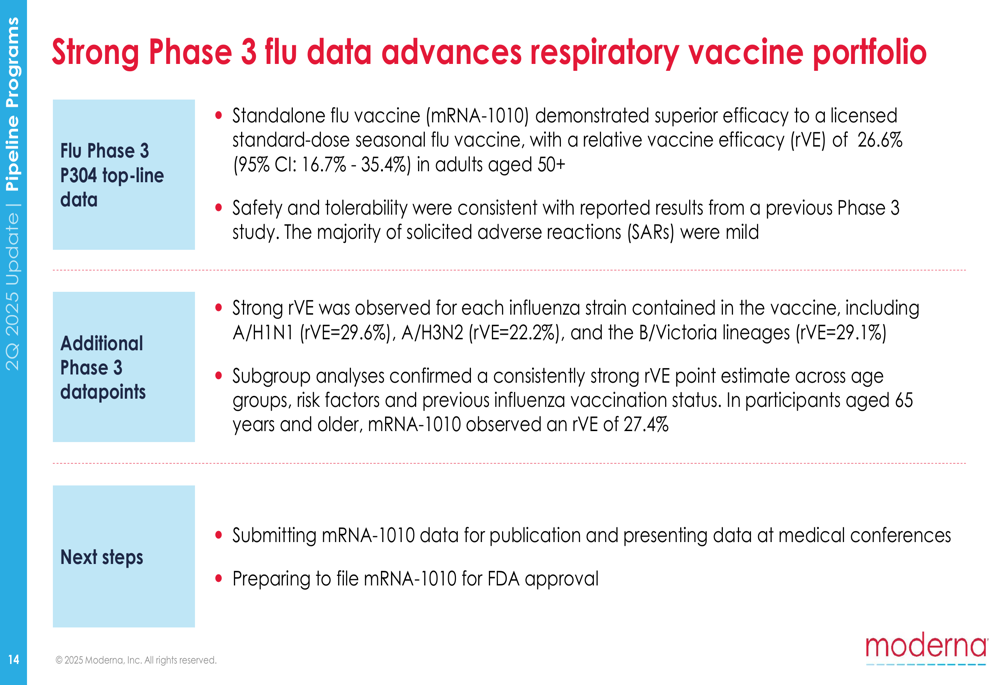

A significant development was the positive Phase 3 data for Moderna’s standalone flu vaccine (mRNA-1010), which demonstrated superior efficacy compared to a licensed standard-dose seasonal flu vaccine, with a relative vaccine efficacy of 26.6% in adults aged 50 and older:

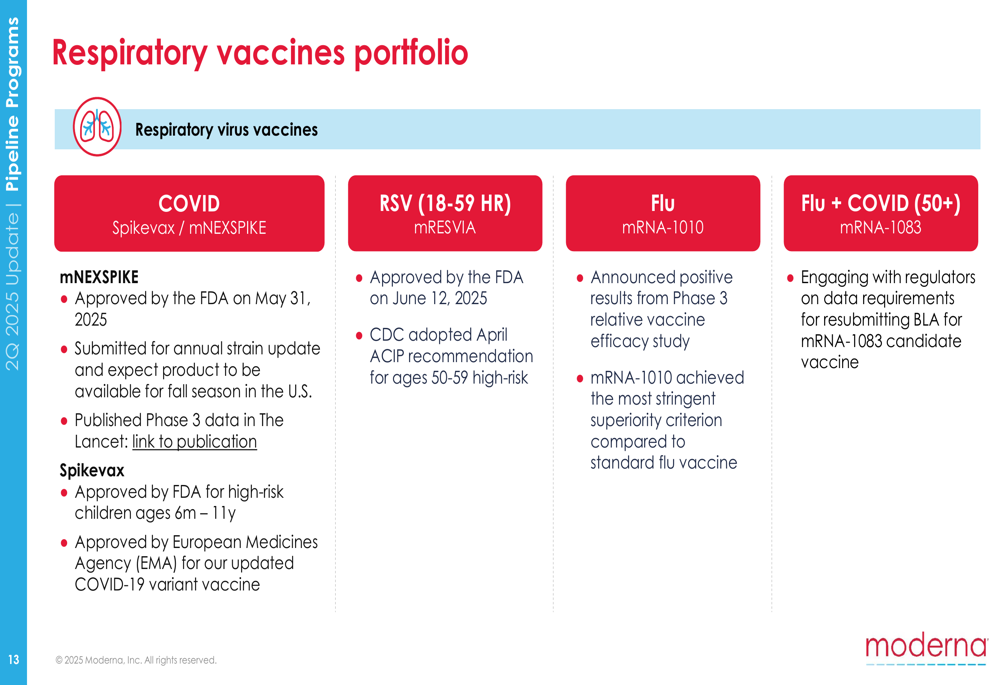

The company is also advancing its respiratory vaccines portfolio, which includes COVID-19, RSV, flu, and combination vaccines:

Forward-Looking Statements

Moderna is targeting 10 product approvals to drive future sales growth, addressing what it estimates as a $30 billion+ total addressable market:

The company continues to target cash breakeven in 2028, with ongoing cost reduction initiatives expected to improve financial performance in the coming years. Moderna highlighted its increasing use of AI across the company, with GPT usage growing from 731,000 instances in Q3 2024 to 1.6 million in Q2 2025, which it credits with enabling faster development, stronger insights, and better decision-making.

Upcoming catalysts include potential approvals for seasonal flu and the flu+COVID combination vaccine for adults 50+, as well as data readouts for CMV, norovirus, intismeran, checkpoint AIM-T, PA, and MMA programs.

Despite near-term revenue challenges, Moderna’s management remains focused on its mission to "deliver the greatest possible impact to people through mRNA medicines," with a strategy centered on expanding its commercial portfolio beyond COVID-19 vaccines while maintaining financial discipline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.